ID : MRU_ 433153 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

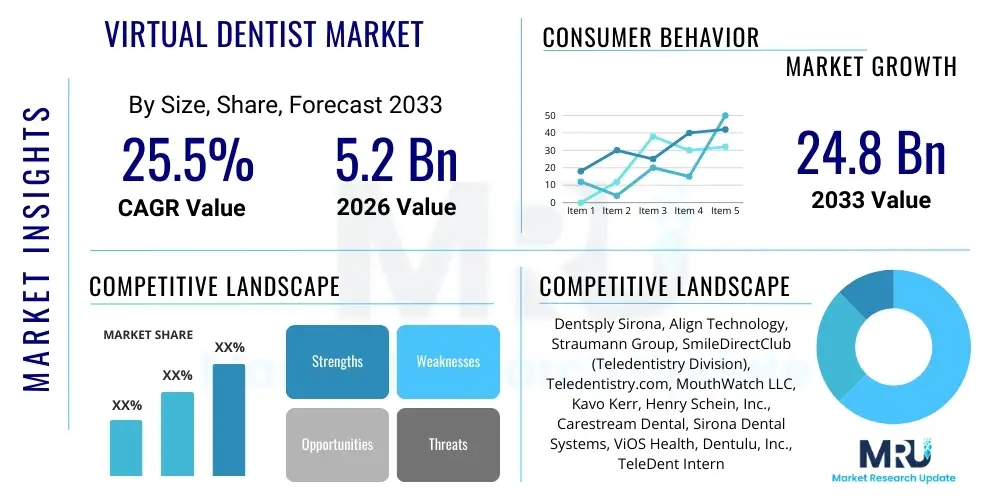

The Virtual Dentist Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.5% between 2026 and 2033. The market is estimated at USD 5.2 Billion in 2026 and is projected to reach USD 24.8 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the increasing integration of telehealth infrastructure within traditional healthcare systems, coupled with rising patient demand for convenient and accessible dental care solutions. The shift towards preventive oral health management, facilitated by remote monitoring and AI-powered diagnostic tools, is a crucial accelerator of this market valuation growth. Furthermore, enhanced regulatory clarity regarding reimbursement for teledentistry services across major developed economies is solidifying the market's commercial viability, attracting significant investments from technology providers and established dental organizations.

The Virtual Dentist Market, often synonymous with advanced teledentistry, encompasses the provision of dental care services, education, and consultations through digital technology platforms, facilitating interaction between dental professionals and patients remotely. This market leverages sophisticated communication tools, including high-resolution video conferencing, secure data exchange systems, remote monitoring devices, and specialized software for diagnostic image review. Products range from synchronous (real-time video calls) and asynchronous (store-and-forward) communication tools to advanced diagnostic algorithms that analyze patient-submitted data, such as intraoral scans or photographs. The primary applications span routine consultations, emergency triage, post-operative monitoring, and specialized orthodontic check-ups, effectively bridging geographical barriers and increasing access to specialized dental expertise, particularly in underserved rural areas.

The core benefits driving rapid market adoption include reduced overhead costs for providers, significant time savings for patients by minimizing travel and waiting times, and improved continuity of care through frequent, non-invasive check-ins. Moreover, virtual dentistry enhances patient engagement and adherence to treatment plans, particularly in long-term restorative or orthodontic treatments, by providing flexible communication options. Key driving factors include the massive global penetration of smartphones and high-speed internet, coupled with a fundamental shift in healthcare consumer behavior demanding digital-first services. Additionally, the shortage of dental professionals in various regions and the increased focus on preventative care modalities post the global health crisis have solidified the strategic importance of virtual platforms.

The market environment is characterized by intense technological innovation focused on improving diagnostic accuracy and integrating advanced artificial intelligence capabilities. This includes developing user-friendly home-use kits for oral scanning and remote examination, ensuring data security compliance, and achieving seamless integration with existing Electronic Health Record (EHR) systems. The convergence of hardware (remote cameras, smart mirrors) and specialized software (AI-powered pathology detection, treatment planning optimization) is creating a robust ecosystem. As regulatory bodies continue to establish guidelines for cross-border practice and data privacy, the Virtual Dentist Market is poised for sustained, high-growth expansion, transforming traditional models of dental service delivery globally.

The Virtual Dentist Market is experiencing a paradigm shift, characterized by accelerated technology adoption across clinical and administrative workflows. Current business trends indicate a strong move toward subscription-based service models, where dental practices license comprehensive software suites incorporating scheduling, patient communication, and AI diagnostic support. Strategic partnerships between established dental equipment manufacturers and specialized software developers are vital for creating end-to-end digital solutions that integrate remote monitoring hardware directly into the patient's home environment. Furthermore, venture capital funding is increasingly focused on startups that address regulatory hurdles through compliant data handling and security protocols (HIPAA, GDPR), thus boosting market confidence and scalability.

Regionally, North America maintains market dominance due to early and aggressive adoption of telehealth policies, favorable reimbursement landscapes, and high per capita expenditure on advanced dental care. However, the Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR), driven by massive population density, government initiatives promoting digital healthcare infrastructure, and the necessity to provide basic dental care to geographically dispersed populations. Europe is showing steady growth, primarily led by countries with strong national health service frameworks integrating virtual care to improve access and efficiency. Latin America and MEA are emerging markets, focusing primarily on basic teledentistry consultations and educational services to overcome immediate access challenges.

Segmentation trends highlight the Software segment’s crucial role, particularly platforms specializing in Artificial Intelligence (AI) for image analysis and preliminary diagnostics. Among applications, remote monitoring and follow-up care represent the fastest-growing area, as practices seek to optimize chair time and improve patient compliance for procedures like clear aligner therapy and implant maintenance. In terms of end-users, specialty dental clinics and orthodontic practices are leading the adoption curve, leveraging virtual tools to manage large patient cohorts efficiently. Conversely, large hospital systems are beginning to integrate teledentistry modules into their overall telemedicine portfolios, recognizing its potential for reducing emergency department visits for non-critical dental issues.

Common user questions regarding AI's influence in the Virtual Dentist Market revolve primarily around diagnostic accuracy, data privacy, and the potential displacement of human dentists. Users frequently ask: "How accurate are AI algorithms in detecting early-stage caries or periodontal disease from home-submitted images?" and "Will AI handle the initial consultation, reducing the need for an in-person visit?" The core theme of user concern centers on reliability and trust—ensuring that remote, AI-assisted diagnosis is clinically equivalent to traditional examination. There are high expectations for AI to automate administrative tasks, optimize scheduling, and personalize treatment plans, leading to faster service delivery and reduced costs. Conversely, users express caution regarding the ethical implications of algorithmic bias and the stringent requirements for securing highly sensitive patient dental data (radiographs, 3D scans) transmitted virtually and processed by automated systems.

The integration of Artificial Intelligence is the single most transformative factor reshaping the Virtual Dentist Market. AI algorithms are fundamentally enhancing diagnostic capabilities by automatically analyzing intraoral scans, photographs, and radiographic images for pathologies such as decay, gum disease, and orthodontic misalignments. This capability allows dental professionals to prioritize urgent cases and allocate resources more effectively, making asynchronous teledentistry highly efficient. Furthermore, machine learning models are being utilized for predictive analytics, identifying patients at high risk of developing specific dental conditions, thereby shifting the focus from reactive treatment to proactive, preventative care facilitated entirely through virtual check-ups and targeted patient education materials.

AI also plays a critical role in streamlining the clinical workflow, contributing significantly to scalability. Automated pre-screening tools manage initial patient intake, categorize symptoms, and generate structured reports, ensuring that the human dentist begins the consultation with a comprehensive, AI-vetted overview. This efficiency not only improves patient throughput but also lowers the potential for human error in monotonous diagnostic tasks. While AI is rapidly augmenting the dentist's capacity, the expectation remains that complex treatment planning and final patient communication require professional human judgment and ethical oversight, positioning AI as a powerful assistive technology rather than a replacement for the dental practitioner.

The Virtual Dentist Market’s expansion is influenced by a complex interplay of Drivers, Restraints, and Opportunities (DRO), which collectively shape the competitive landscape and growth trajectory. The primary drivers revolve around the inherent efficiencies offered by digital healthcare, including overcoming geographical access barriers, particularly for specialized care, and the sustained consumer preference for convenient, on-demand services. Opportunities arise mainly from technological convergence—integrating 5G networks for high-fidelity video consultations, leveraging advanced cloud infrastructure for secure data storage, and the untapped potential of direct-to-consumer models for non-complex cosmetic procedures like teeth whitening and minor alignment corrections. Simultaneously, the market faces significant restraints, notably the lack of standardized global regulatory frameworks concerning patient data sovereignty and cross-jurisdictional practice licensing, which can hamper the international scalability of service providers.

Impact Forces, categorized under Porter’s Five Forces analysis, indicate a moderate to high intensity of competition. The threat of new entrants is moderate; while the initial investment in secure software development is high, the market is attractive due to high growth prospects, leading to constant influx of specialized tech startups. The bargaining power of suppliers (of hardware, cloud services, and specialized sensors) is generally moderate, as many components are commoditized, but high-end specialized imaging technology suppliers maintain stronger influence. The bargaining power of buyers (large dental service organizations and hospitals) is substantial, as they often negotiate volume discounts for enterprise software licenses, demanding high levels of customization and security compliance. Substitute products, primarily traditional in-person dental care, remain strong, although the convenience factor of virtual care is eroding this strength.

The greatest long-term opportunity lies in penetrating the corporate wellness sector and forming strategic partnerships with insurance providers to integrate virtual dental screenings into employee health benefit packages. This proactive approach not only expands the user base but also validates the preventative financial returns of teledentistry. Addressing the major restraint—regulatory fragmentation—through industry consortiums advocating for unified telemedicine guidelines across major economic blocs is critical for unlocking the market's full potential. Successful players will be those who can demonstrate clinical efficacy, robust data security, and seamless integration capabilities with existing practice management systems, making their virtual platform an indispensable tool rather than a supplementary service.

The Virtual Dentist Market is comprehensively segmented based on Component, Application, and End-User, reflecting the diverse technologies and deployment strategies employed across the industry. This detailed segmentation allows stakeholders to analyze specific high-growth areas, allocate resources effectively, and tailor product development to meet specialized user needs. The core distinction lies between the tangible infrastructure (Hardware) and the digital intelligence (Software and Services) that enables remote interaction and diagnosis. Understanding the dynamics within each segment, such as the rapid innovation cycle in AI-driven software versus the stability of remote monitoring hardware, is essential for strategic market positioning and achieving segment penetration.

The Virtual Dentist Market value chain is structured around four critical stages: upstream component manufacturing, core service/software development, distribution, and downstream service delivery. The upstream segment involves the production of necessary hardware components, such as high-resolution cameras, specialized remote sensors, and data storage solutions. Key players in this stage include electronic manufacturers and medical device suppliers who provide the foundational technology. Efficiency at this stage is crucial, focusing on minimizing manufacturing costs while ensuring high data fidelity and compliance with medical device standards, particularly regarding accuracy for diagnostic imaging. Strategic sourcing and inventory management are primary value drivers in the upstream process.

The core value creation stage involves software development, including the design of secure, compliant, and user-friendly platforms. This mid-stream segment is dominated by specialized healthcare IT companies and dedicated teledentistry platform providers. Value is added through the integration of AI for diagnostics, seamless interoperability with existing EHR/EMR systems, and robust security features (end-to-end encryption). The distribution channel links these solutions to end-users, involving both direct sales teams targeting large Dental Service Organizations (DSOs) and indirect channels through partnerships with telecommunication providers, medical distributors, and Value-Added Resellers (VARs). The selection of the channel depends heavily on the target market's regulatory environment and technological maturity.

The downstream analysis focuses on the final service delivery, where the virtual platform is utilized by dental professionals for patient care. Direct service provision involves providers using their own purchased or licensed platforms (e.g., a dental clinic providing remote monitoring services). Indirect value is created through partnerships with third-party consultation networks, where specialists provide remote expertise on a contract basis. Optimization at this stage focuses on enhancing the patient experience, ensuring high service uptake, minimizing technical latency, and maximizing clinical efficiency. The effectiveness of the overall value chain is highly dependent on the speed of data transfer and the security assurances provided at every transition point, ensuring regulatory compliance from device manufacture to final diagnosis.

The primary consumers and end-users of virtual dentistry solutions span a wide spectrum, ranging from large, integrated healthcare networks focused on optimizing patient throughput to individual patients seeking convenient and cost-effective alternatives to traditional visits. Dental Service Organizations (DSOs) represent a significant customer segment. DSOs leverage virtual platforms to centralize specialist expertise, standardize intake protocols across multiple locations, and manage the logistics of multi-site operations more efficiently. For these large groups, the value proposition centers on scalability, enhanced patient capture rates, and optimizing the utilization of high-value clinical chair time by offloading routine check-ups to virtual channels.

Specialty dental practices, particularly those in orthodontics and periodontics, are rapidly adopting virtual solutions. Orthodontists use remote monitoring technology to track clear aligner treatment progress, drastically reducing the required in-person appointments, which is a major driver of cost savings and patient satisfaction. Periodontists utilize store-and-forward technology for secondary opinions on complex cases and remote monitoring of patients with chronic gum conditions. For these specialists, the ability to manage complex cases efficiently and expand their geographical service area without physical expansion provides a crucial competitive edge. Furthermore, the adoption is driven by the necessity to maintain consistent communication with long-term patients requiring careful, interval-based observation.

Another rapidly emerging customer base is the direct-to-consumer (D2C) market, encompassing individual patients and caregivers using personal devices for self-monitoring and general wellness. While regulatory constraints limit the extent of D2C diagnosis, patients are increasingly purchasing remote monitoring kits and subscribing to apps for basic consultations, triage, and oral hygiene education. Rural populations and individuals with mobility issues also constitute a high-priority segment, as virtual dentistry eliminates significant access barriers. Finally, public health agencies and governmental organizations are potential customers, using teledentistry to conduct community-wide screenings and deliver preventative education in schools and remote clinics, aiming to address systemic oral health disparities through scalable digital means.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 5.2 Billion |

| Market Forecast in 2033 | USD 24.8 Billion |

| Growth Rate | 25.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Dentsply Sirona, Align Technology, Straumann Group, SmileDirectClub (Teledentistry Division), Teledentistry.com, MouthWatch LLC, Kavo Kerr, Henry Schein, Inc., Carestream Dental, Sirona Dental Systems, ViOS Health, Dentulu, Inc., TeleDent International, Consult-A-Dent, General Dental, Remote Dental Solutions, Pacific Dental Services, Microsoft (Healthcare Division), Google Health, Philips Healthcare |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Virtual Dentist Market is highly dynamic, centered on enhancing remote diagnostic accuracy and ensuring secure, real-time communication. The foundational technology involves secure cloud computing and high-definition video conferencing (synchronous care), requiring low latency and high bandwidth to replicate the detail required for clinical evaluation. Specialized hardware, such as portable, high-resolution intraoral cameras and standardized remote monitoring kits that patients use at home, forms a critical part of this ecosystem. These devices must be intuitive for non-clinical users while maintaining professional-grade imaging capabilities necessary for a reliable remote diagnosis, often integrating directly with proprietary mobile applications for easy data transmission.

A major technological focus is the development and deployment of sophisticated Artificial Intelligence and Machine Learning (AI/ML) algorithms. These technologies are applied primarily in analyzing image data (photographs, 2D radiographs, 3D cone-beam computed tomography scans) to automate the detection of common pathologies such as dental caries, periodontal bone loss, and specific orthodontic malocclusions. AI integration significantly accelerates the asynchronous teledentistry workflow by pre-analyzing data before the human dentist reviews the case. Furthermore, these platforms utilize natural language processing (NLP) to manage patient inquiries and automate charting, thereby improving administrative efficiency and reducing documentation time for dental professionals, allowing them to focus more on complex clinical judgments.

Interoperability and data security standards are foundational to the widespread adoption of these technologies. Virtual platforms must adhere strictly to international regulatory requirements (e.g., HIPAA in the U.S., GDPR in Europe) concerning patient data privacy and security. Technology providers are investing heavily in advanced encryption protocols, blockchain technology for immutable data logs, and seamless API integration capabilities that allow their virtual solutions to communicate effortlessly with existing dental Practice Management Systems (PMS) and hospital Electronic Health Records (EHR). The convergence of 5G connectivity is also a key technological enabler, promising to overcome current bandwidth limitations, making high-fidelity 3D imaging and complex data transfers feasible even in mobile or remote settings, drastically improving the quality and scope of virtual diagnosis and consultation.

The Virtual Dentist Market is projected to exhibit a robust Compound Annual Growth Rate (CAGR) of 25.5% between the forecast years of 2026 and 2033, driven primarily by technological advancements and increasing regulatory acceptance of teledentistry models.

AI algorithms analyze patient-submitted data, such as high-resolution photographs and digital scans, to rapidly identify subtle signs of pathology like early-stage caries or periodontal disease, augmenting the dentist's capacity for accurate remote diagnosis and triage.

The Software segment, particularly platforms focusing on AI-driven diagnostics and seamless integration with existing Practice Management Systems (PMS), is expected to demonstrate the highest growth potential, capitalizing on the demand for enhanced efficiency and remote monitoring capabilities.

Key regulatory challenges include the fragmentation of professional licensing across different jurisdictions, which restricts cross-state or cross-country practice, and the rigorous demands for securing sensitive patient data (HIPAA, GDPR) in cloud-based virtual environments.

North America currently holds the largest market share in the Virtual Dentist Market, attributable to favorable reimbursement policies for telehealth, high consumer digital literacy, and the strong presence of major technology innovators and established dental service organizations (DSOs).

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.