ID : MRU_ 432869 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

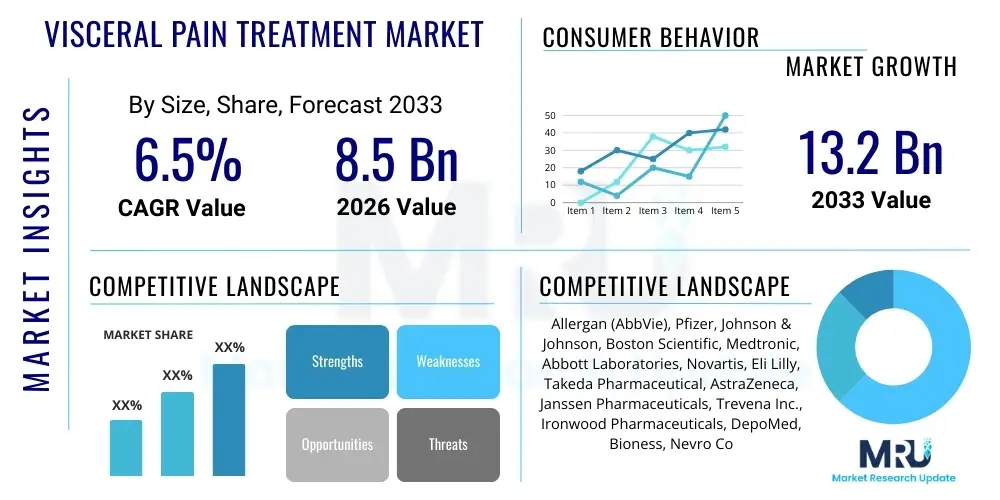

The Visceral pain treatment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 8.5 Billion in 2026 and is projected to reach USD 13.2 Billion by the end of the forecast period in 2033.

Visceral pain refers to discomfort originating from internal organs (viscera) and is characterized by being poorly localized, deep, and often radiating. It is a common symptom in chronic conditions such as Irritable Bowel Syndrome (IBS), Crohn’s disease, interstitial cystitis, and various forms of cancer. The market for visceral pain treatment encompasses a wide array of pharmacological and non-pharmacological interventions aimed at alleviating this specific type of nociception, which significantly impairs patients' quality of life. Treatment modalities range from traditional analgesics and antispasmodics to advanced neuromodulation techniques and targeted biological therapies, addressing the complex pathophysiology involving central sensitization, peripheral inflammation, and nerve fiber activity.

The core product offerings in this specialized therapeutic area include both symptomatic relief drugs and disease-modifying agents. Pharmacological treatments primarily feature opioid and non-opioid analgesics, anti-depressants (used for their analgesic properties in chronic pain), gabapentinoids, and drugs specifically targeting gastrointestinal motility or bladder function, depending on the underlying cause. Furthermore, specialized interventions like nerve blocks, ablation therapies, and minimally invasive surgical procedures form a crucial part of the comprehensive treatment landscape, catering to patients refractory to conventional medical management. The complexity of diagnosing and treating visceral pain—often involving multiple organ systems—drives the demand for personalized and multimodal treatment strategies.

Major applications of visceral pain treatment span across gastroenterology, urology, oncology, and gynecology. Key driving factors accelerating market growth include the rising global prevalence of chronic visceral conditions, particularly functional gastrointestinal disorders (FGIDs); increasing research into the distinct mechanisms of visceral hypersensitivity; and growing patient and physician acceptance of non-opioid pain management alternatives, fueled by the global opioid crisis. The market benefits from continuous pipeline development focusing on novel receptors and pathways specific to visceral nociception, promising more effective and targeted therapeutic solutions compared to broad-spectrum pain relievers.

The Visceral Pain Treatment Market is experiencing robust expansion, driven by significant advancements in understanding gut-brain axis interactions and subsequent development of targeted drug candidates. Business trends indicate a strong move toward specialization, with pharmaceutical companies investing heavily in biologics and small molecules designed to modulate specific inflammatory and neural pathways associated with chronic visceral conditions like inflammatory bowel diseases and endometriosis. Strategic collaborations between biotech startups focusing on neuroinflammation and established pharmaceutical giants are defining the competitive landscape, aiming to commercialize innovative non-addictive pain relief options. Furthermore, the market is characterized by increasing adoption of multidisciplinary treatment approaches, integrating pharmacotherapy with interventional procedures and digital therapeutics for holistic patient care, thereby expanding the revenue potential across multiple segments.

Regional trends highlight North America and Europe as dominant forces, primarily due to high healthcare expenditure, established clinical guidelines for pain management, and the rapid uptake of premium, advanced therapies, including spinal cord stimulation and targeted nerve blocks. However, the Asia Pacific (APAC) region is poised for the fastest growth, propelled by the rising incidence of visceral diseases, expanding access to specialized pain clinics, and governmental initiatives supporting affordable healthcare infrastructure development. Segment trends show that pharmacological treatments, particularly those focused on G-protein coupled receptors (GPCRs) and nerve growth factor (NGF) inhibitors, maintain the largest market share, while neuromodulation devices are rapidly gaining traction due to proven efficacy in managing refractory pain and favorable long-term cost-effectiveness profiles.

The overall market trajectory is influenced by regulatory shifts emphasizing patient safety and the reduction of opioid dependency. This regulatory environment acts as a strong catalyst for innovation in non-opioid pharmacotherapies. The chronic nature of visceral pain ensures a stable demand base, while technological breakthroughs in imaging and diagnostic tools allow for earlier and more precise intervention. The market must navigate challenges related to the high cost of advanced therapies and the diagnostic complexity inherent in differentiating visceral pain from somatic pain, but the unmet medical need for effective, long-term relief remains the primary market driver.

Common user questions regarding the impact of AI in visceral pain treatment center around how Artificial Intelligence can improve diagnostic accuracy, personalize treatment plans, and optimize drug discovery processes for novel analgesics. Users frequently inquire about AI's role in identifying complex pain patterns and phenotypes that elude traditional clinical evaluation, particularly in conditions like functional abdominal pain. A key theme is the expectation that AI and Machine Learning (ML) can analyze vast datasets—including genetic, imaging, and electronic health record (EHR) data—to predict patient response to specific drugs (e.g., antidepressants or antispasmodics) and reduce the reliance on empirical prescribing. Concerns also revolve around data privacy, algorithmic bias, and the validation of AI-driven diagnostic tools in diverse patient populations affected by chronic visceral disorders. The consensus expectation is that AI will streamline the clinical trial process for new pain treatments and enhance remote patient monitoring through predictive analytics.

The dynamics of the Visceral Pain Treatment Market are significantly shaped by a confluence of accelerating drivers, critical restraints, and substantial opportunities, collectively forming potent impact forces. Key drivers include the escalating global burden of chronic visceral diseases such as IBS, IBD, and chronic pelvic pain, which necessitate long-term therapeutic interventions. A primary restraint is the inherent complexity and heterogeneity of visceral pain pathophysiology, often leading to misdiagnosis and suboptimal treatment outcomes, alongside regulatory hurdles associated with developing non-addictive pain therapies. Opportunities are abundant in the integration of precision medicine approaches, leveraging biomarkers for targeted therapy development, and the expansion of non-pharmacological modalities like neurostimulation. These forces combine to push the market toward innovative, mechanism-based treatments that prioritize efficacy and patient safety over traditional, broad-spectrum analgesics.

The dominant impact force is the widespread necessity to move away from chronic opioid prescriptions for non-cancer pain management. This public health crisis has compelled research into novel G-protein coupled receptor targets and ion channel modulators, accelerating investment in non-opioid pain relief. Furthermore, growing clinical evidence supporting the efficacy of peripheral and central neuromodulation techniques (e.g., spinal cord stimulation, sacral nerve stimulation) is shifting the standard of care, offering viable long-term solutions for refractory patients. Conversely, the high cost associated with developing and commercializing specialized biologics and advanced neuromodulation devices acts as a limiting factor, particularly in cost-sensitive healthcare systems, posing a restraint on rapid global adoption.

The market environment is highly receptive to disruptive technologies, presenting opportunities in digital health and personalized diagnostics. The increasing sophistication of molecular diagnostics allows for better phenotyping of patients with functional pain syndromes, enabling the selection of the most appropriate existing drug or identifying candidates for experimental therapies. The combined effect of high unmet need (Opportunity) and stringent safety requirements (Restraint) results in a highly focused research environment (Driver), favoring companies that can successfully navigate the regulatory pathway with clinically superior, mechanism-specific treatment options. The inherent chronic and relapsing nature of these conditions ensures a persistent demand curve, stabilizing market growth despite competitive pressures.

The Visceral Pain Treatment Market is primarily segmented based on the type of intervention (pharmacological and non-pharmacological), the indication (the underlying disease causing the pain), and the distribution channel. The pharmacological segment, which historically dominates, is further refined by drug class, including opioids, non-steroidal anti-inflammatory drugs (NSAIDs), antispasmodics, tricyclic antidepressants, and specialized therapies such as Nerve Growth Factor (NGF) inhibitors and targeted biologics. Non-pharmacological interventions encompass advanced medical devices, including implantable neuromodulation systems (e.g., sacral and spinal cord stimulation), neuroablation devices, and specialized physical therapies and behavioral techniques. Segmentation by indication is critical, differentiating treatments for highly prevalent conditions like Irritable Bowel Syndrome (IBS) and chronic pancreatitis from those targeting cancer-related visceral pain or pelvic pain syndromes.

The largest contributing segment remains the pharmacological category, driven by the immediate accessibility and broad prescription base of generic treatments like tricyclic antidepressants (TCAs) and specific antispasmodics used off-label or on-label for functional bowel disorders. However, the fastest growth is observed in the non-pharmacological device segment. This growth is fueled by advancements in miniaturization, improved battery life, and enhanced efficacy of neuromodulation technologies, which provide superior, long-term pain control with a reduced risk of systemic side effects or addiction compared to chronic pharmacological management. The segmentation underscores the trend towards individualized patient care, where the selection of therapy is increasingly dependent on the precise etiology and severity of the patient's visceral pain phenotype, moving beyond a one-size-fits-all analgesic approach.

The value chain for the Visceral Pain Treatment Market commences with rigorous upstream analysis focused on basic research and development (R&D) of novel therapeutic targets, involving academic institutions and specialized biotech firms. This phase encompasses the identification of specific receptors (e.g., TRP channels, NK1 receptors, opioid receptors) and neural pathways implicated in visceral hypersensitivity. Procurement and manufacturing then involve the sourcing of high-purity active pharmaceutical ingredients (APIs) or, in the case of devices, complex components like microelectrodes and neurostimulators, where stringent quality control is paramount. The high regulatory requirements for both drug and device approval significantly influence the complexity and cost associated with this upstream segment, driving strategic partnerships to mitigate risk.

Midstream activities involve the clinical testing, manufacturing, and formulation of the final products. For pharmacological agents, this includes formulation stability, dosage development, and large-scale manufacturing under Good Manufacturing Practices (GMP). For advanced devices, assembly, sterilization, and software integration are key. Distribution forms a critical link, segmented into direct and indirect channels. Direct distribution is often used for high-cost, specialized products like implantable neurostimulators, requiring specialized sales teams and direct hospital relationships. Indirect distribution, leveraging major wholesalers and retail pharmacy chains, handles the volume sales of established generic and branded pharmacological treatments, ensuring broad patient access across primary care settings.

The downstream analysis focuses heavily on market penetration, physician education, and patient adherence. The end-users—hospitals, specialized pain clinics, and outpatient settings—are targeted through specialized marketing campaigns that emphasize clinical efficacy and long-term cost-benefit analyses, particularly for interventional therapies. The complexity of diagnosing visceral pain necessitates significant investment in post-market surveillance and continuous medical education for healthcare providers to ensure appropriate product utilization. The value chain is constantly optimized to shorten the time from discovery to patient access, particularly for breakthrough non-opioid solutions that address significant unmet clinical needs in chronic pain management.

The primary end-users and buyers of products within the Visceral Pain Treatment Market are segmented across several key institutional and individual categories, reflecting the multidisciplinary nature of pain management. Hospitals, particularly those with dedicated pain management centers, gastroenterology departments, urology clinics, and oncology units, represent major institutional buyers, procuring high volumes of both pharmacological treatments and specialized interventional devices like radiofrequency ablation systems and neurostimulators. These institutions prioritize products offering superior efficacy, patient safety, and those aligned with clinical guidelines for complex, chronic pain syndromes, often making bulk purchasing decisions driven by formulary approval committees.

Specialized Pain Clinics and Ambulatory Surgical Centers (ASCs) constitute another significant customer base, focusing heavily on non-pharmacological, interventional procedures. ASCs are particularly inclined to adopt minimally invasive techniques, such as nerve blocks and advanced neuromodulation, due to favorable reimbursement structures and the ability to manage patients efficiently in an outpatient setting. Their purchasing decisions are often influenced by procedure volume, equipment durability, and the technical support provided by manufacturers. Furthermore, individual patients, though not direct buyers of prescription drugs in institutional settings, drive demand through their utilization of retail and specialty pharmacies, seeking relief for chronic conditions often managed in primary care settings.

Finally, governmental healthcare organizations and private insurance payers act as critical indirect customers, influencing market adoption through reimbursement policies and coverage decisions. Their focus is on cost-effectiveness and demonstrated clinical outcomes, particularly favoring therapies that reduce long-term healthcare utilization, such as avoiding costly hospital readmissions or chronic dependency on high-risk medications like opioids. The targeting of potential customers requires specialized strategies addressing clinical validation for physicians, formulary adherence for hospitals, and cost-benefit analysis for payers, tailored to the specific segment of the visceral pain continuum they address.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 13.2 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Allergan (AbbVie), Pfizer, Johnson & Johnson, Boston Scientific, Medtronic, Abbott Laboratories, Novartis, Eli Lilly, Takeda Pharmaceutical, AstraZeneca, Janssen Pharmaceuticals, Trevena Inc., Ironwood Pharmaceuticals, DepoMed, Bioness, Nevro Corp., Teva Pharmaceutical, Grunenthal, Merck & Co., and Sunovion Pharmaceuticals. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Visceral Pain Treatment Market is rapidly evolving, driven by the need for therapies that offer superior efficacy with minimal side effects compared to traditional broad-spectrum analgesics. A significant technological focus is on targeted drug delivery systems and novel small molecules that modulate specific receptors involved in visceral hypersensitivity. For instance, technologies targeting the peripheral sensitization pathways, such as antagonists for the transient receptor potential (TRP) channels (e.g., TRPV1 and TRPA1) and inhibitors of Nerve Growth Factor (NGF), represent cutting-edge pharmacological developments. These targeted approaches aim to desensitize the afferent nerve endings in the viscera without the central nervous system side effects associated with opioids or gabapentinoids. Continuous research is optimizing drug formulation to ensure high bioavailability at the site of visceral pathology, such as utilizing enteric-coated or sustained-release formulations for gastrointestinal applications.

In the non-pharmacological domain, the advancements in neuromodulation devices are perhaps the most transformative technological shift. Key technologies include high-frequency and dorsal root ganglion (DRG) stimulation systems offered by major medical device manufacturers. DRG stimulation, in particular, allows for highly localized nerve targeting, providing effective pain relief for specific, intractable visceral pain conditions like chronic pelvic pain or post-surgical nerve injury. Furthermore, the development of miniaturized, leadless neurostimulators and sophisticated battery management systems has improved patient convenience and reduced the invasiveness of these procedures. Technology is also integrating digital platforms, utilizing wireless sensors and wearable devices for real-time monitoring of patient symptoms and activity, feeding data back into AI-driven systems for personalized feedback and treatment adjustments.

Another area of intense technological activity involves advanced imaging and interventional techniques. High-resolution ultrasound and sophisticated fluoroscopy are integral to performing precise nerve blocks and ablative procedures (e.g., celiac plexus block for pancreatic pain). Technologies such as focused ultrasound (FUS) and radiofrequency ablation (RFA) are being refined to minimize collateral tissue damage while effectively disrupting the painful nerve pathways originating from the viscera. The successful convergence of molecular biology—allowing for the identification of novel pain mediators—with engineering expertise—facilitating the creation of highly targeted delivery vehicles and sophisticated neuromodulation devices—defines the current and future trajectory of technology in this critical therapeutic area, promising more durable and side-effect-free solutions.

Somatic pain originates from the skin, muscles, or joints and is usually sharp and well-localized. Visceral pain originates from internal organs; it is poorly localized, deep, and often refers to distant sites. Treatment for visceral pain is often complex, requiring modulation of autonomic nervous system pathways and the use of specialized agents like antispasmodics or neuromodulators, rather than standard musculoskeletal analgesics.

The global effort to reduce chronic opioid use is a major market driver, leading to increased R&D and investment in non-opioid alternatives, including targeted biologics (e.g., NGF inhibitors), non-addictive small molecules, and sophisticated interventional pain management devices like spinal cord stimulation (SCS) systems, which offer long-term pain control without dependency risk.

The Neuromodulation and Advanced Interventional Therapies segment is anticipated to exhibit the fastest growth. This is driven by technological advancements (such as Dorsal Root Ganglion stimulation) and growing clinical evidence supporting their long-term efficacy and improved safety profile compared to chronic pharmacological management, especially for refractory visceral pain conditions.

The gut-brain axis is a critical focus area. Research into this connection drives the development of treatments targeting neuroinflammation, gut microbiota modulation, and specific neurotransmitter pathways that link intestinal dysfunction to central pain processing. Drugs modulating serotonin receptors or targeting mast cell stabilizers are examples of therapies developed based on gut-brain axis insights.

Key challenges include the heterogeneity of patient symptoms, lack of clear biomarkers for diagnosis and treatment response, and high rates of placebo response in clinical trials for functional disorders. These factors necessitate highly focused patient phenotyping and complex trial designs to demonstrate significant treatment efficacy over placebo, increasing R&D costs and regulatory complexity.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.