ID : MRU_ 435363 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

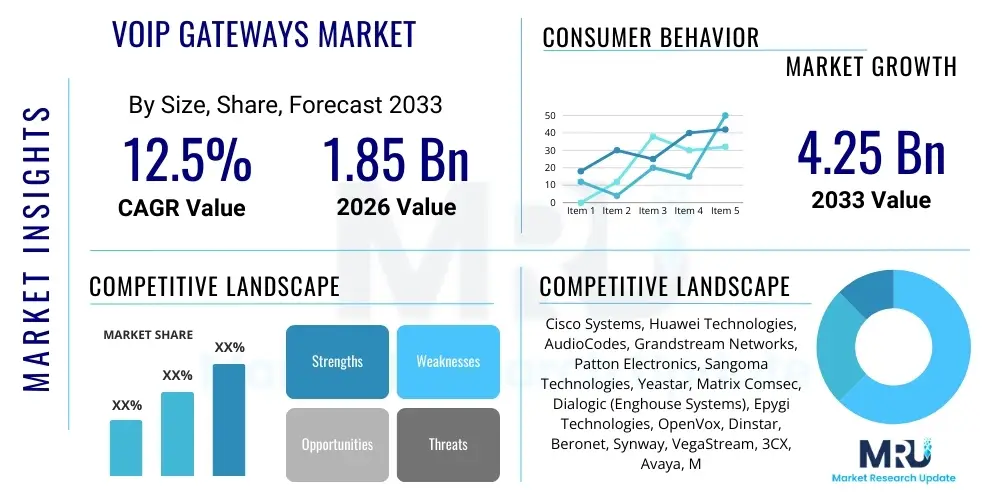

The VoIP Gateways Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 1.85 Billion in 2026 and is projected to reach USD 4.25 Billion by the end of the forecast period in 2033.

VoIP Gateways are essential hardware components that facilitate the integration of traditional telephony infrastructure, such as the Public Switched Telephone Network (PSTN), with Voice over Internet Protocol (VoIP) networks. These devices convert analog voice signals into digital packets for transmission over IP networks and vice versa, enabling seamless communication between legacy systems, like Private Branch Exchanges (PBXs) or standard analog phones, and modern internet-based communication platforms. The core functionality of a VoIP gateway revolves around protocol conversion, compression, and handling quality of service (QoS) to ensure reliable voice delivery, making them indispensable for enterprises undergoing digital transformation and for telecom service providers transitioning to all-IP networks.

Major applications of VoIP Gateways span across various industries, including large enterprises utilizing unified communications (UC) platforms, Small and Medium Enterprises (SMEs) seeking cost-effective communication upgrades, and particularly, telecom carriers employing them for network access and trunking. Products range from Analog Telephone Adapters (ATAs) designed for individual residential or small office use, which connect standard analog phones to a VoIP network, to highly scalable Digital Gateways (E1/T1/PRI) used in carrier-grade environments and large contact centers. The primary benefit realized by adopting this technology is substantial operational cost reduction, particularly concerning long-distance calls, coupled with the flexibility and advanced features inherent in IP telephony, such as softphones, video conferencing, and integrated messaging services.

The market expansion is fundamentally driven by several critical factors, notably the global proliferation of unified communications as a Service (UCaaS) platforms and the accelerating mandate among incumbent telecom operators to decommission legacy Time-Division Multiplexing (TDM) infrastructure. Further impetus comes from the growing adoption of hybrid work models globally, necessitating robust, reliable, and secure remote communication solutions that often require VoIP gateways to bridge the gap between corporate headquarters infrastructure and remote endpoints. Enhanced data security features, improved interoperability with Session Initiation Protocol (SIP) standards, and the requirement for efficient bandwidth utilization continue to fuel sustained demand across established and emerging economies.

The VoIP Gateways market is undergoing significant transformation, characterized by strong business trends centered around the integration of virtualization and software-defined networking (SDN) principles, shifting the focus from proprietary hardware to highly scalable, often containerized, gateway solutions. Enterprises are prioritizing gateways that offer superior security protocols, including robust encryption and enhanced protection against Distributed Denial of Service (DDoS) attacks and toll fraud, reflecting heightened cybersecurity concerns in the telecommunications sector. Furthermore, the market is seeing increased merger and acquisition activity among key players, driven by the need to consolidate intellectual property, expand geographic reach, and acquire expertise in emerging areas such as WebRTC and 5G network integration, solidifying the trend toward converged voice and data infrastructure.

Regionally, North America remains the dominant market, propelled by high levels of digital adoption, the presence of major technology providers, and continuous infrastructure modernization efforts across enterprise and carrier segments. However, the Asia Pacific (APAC) region is demonstrating the highest growth trajectory, primarily fueled by rapid urbanization, significant investments in telecommunications infrastructure, and the massive scale of SME growth, particularly in countries like India and China, where mobile and IP connectivity are expanding rapidly. Europe presents a stable but mature market, where regulatory mandates concerning network resilience and data privacy are shaping product development, pushing vendors to innovate on compliance and security features within their gateway offerings.

Segmentation trends indicate a robust demand for Digital Gateways (E1/T1/PRI) within the Carrier and Large Enterprise segments, driven by the need for high-density trunking capacity required for massive call volumes and integration with existing high-capacity PBXs. Simultaneously, the Analog Gateway (FXS/FXO) segment maintains stability, largely due to its necessity in connecting ubiquitous legacy devices like fax machines, elevators, and alarm systems to modern IP networks, often in environments where a complete overhaul of endpoint devices is cost-prohibitive. The fastest-growing segment, however, is likely the integration of VoIP gateway functions into broader Unified Communications as a Service (UCaaS) platforms, often deployed virtually or through specialized Session Border Controllers (SBCs) that incorporate gateway capabilities, streamlining enterprise communication architecture.

Common user inquiries regarding AI's influence on the VoIP Gateways market predominantly revolve around three key areas: how AI can enhance security and combat fraud (specifically toll fraud), the application of machine learning for proactive Quality of Service (QoS) management, and the potential for AI to automate gateway configuration and network optimization. Users express concern about legacy gateway systems becoming vulnerabilities but also hold high expectations for AI-driven anomaly detection to identify and mitigate threats in real-time. There is also significant interest in using AI algorithms to analyze traffic patterns passing through gateways, predicting network congestion before it impacts voice quality, thereby moving network management from reactive troubleshooting to predictive maintenance. This synthesis suggests users view AI not as a replacement for the gateway hardware but as a powerful layer of intelligence critical for operational excellence and robust security in complex modern communication networks.

AI technologies, specifically machine learning algorithms, are fundamentally altering how VoIP gateways are deployed and managed, leading to profound operational efficiencies and enhanced service reliability. By analyzing massive datasets of call detail records (CDRs), network latency metrics, and signaling errors, AI systems deployed alongside or integrated within gateways can swiftly identify patterns indicative of service degradation, potential equipment failures, or sophisticated fraud attempts that traditional rule-based systems might miss. This predictive capability significantly reduces Mean Time To Resolution (MTTR) for service disruptions and minimizes financial losses associated with unauthorized network access or usage, enhancing the overall value proposition of the gateway infrastructure to both carriers and enterprises.

Furthermore, AI is instrumental in advancing the intelligence of traffic routing and load balancing within complex gateway deployments. Instead of relying on static routing tables, AI-powered systems can dynamically assess real-time network conditions, including latency, jitter, and packet loss across multiple potential pathways, ensuring that each call is routed optimally to maintain the highest possible voice quality (HD Voice standards). This optimization is crucial for supporting global UCaaS environments and large contact centers where milliseconds of delay can negatively affect customer experience. The integration of AI also facilitates automatic provisioning and self-healing network segments, drastically simplifying the deployment and ongoing maintenance of large fleets of geographically dispersed VoIP gateways.

The dynamics of the VoIP Gateways Market are shaped by a complex interplay of Drivers (D), Restraints (R), and Opportunities (O), exerting significant impact forces across the industry value chain. Key drivers include the overwhelming global migration toward unified communications and the undeniable cost savings associated with IP telephony compared to legacy PSTN services, compelling organizations of all sizes to invest in gateway technology to ensure interoperability during the transition phase. Opportunities are primarily centered around integrating emerging technologies such as 5G and IoT, where gateways will serve as critical communication hubs for high-density, low-latency applications, creating specialized market niches. These strong driving and opportunity forces frequently clash with prevailing restraints, notably heightened concerns over security vulnerabilities, including sophisticated cyberattacks and regulatory compliance complexities, requiring vendors to continuously prioritize product innovation in robust security features and adherence to regional data privacy laws.

The primary driving force remains the relentless global effort by service providers and large enterprises to decommission aging, expensive TDM infrastructure, which necessitates the deployment of SIP-compliant VoIP gateways to manage the final-mile connection to existing analog and digital devices. The proliferation of remote and hybrid work environments, accelerated since 2020, has also substantially increased the demand for reliable, scalable communication infrastructure, where gateways serve as the crucial link between disparate office and home networks and core communication servers. Furthermore, the standardization of Session Initiation Protocol (SIP) has significantly reduced integration complexity, encouraging broader market adoption and lowering barriers to entry for new vendors, fostering a competitive and rapidly evolving market landscape focused on feature richness and interoperability.

However, the market faces significant restraints, chiefly related to security and operational complexity. VoIP networks are inherently susceptible to various security threats, particularly toll fraud, denial-of-service (DoS) attacks, and unauthorized access, demanding continuous investment in security patches and specialized Session Border Controller (SBC) functionalities often bundled with or layered upon gateway technology. Another restraint is the persistent issue of interoperability between gateways manufactured by different vendors and varying legacy PBX systems, which can lead to complex integration challenges and potential voice quality issues. Nevertheless, substantial opportunities exist in the specialization of gateway solutions for vertical markets, such as healthcare (for connecting specialized medical monitoring devices) and smart city initiatives (for managing large-scale public communication endpoints), and the eventual integration of advanced gateway capabilities directly into software-based cloud communication environments.

The VoIP Gateways Market is comprehensively segmented based on three primary factors: Type (which reflects the signal being handled), Interface Density, and End-User Application (which determines scalability requirements). This segmentation provides a granular view of market demand, highlighting how different organizational needs necessitate specific gateway configurations. For instance, the distinction between Analog and Digital gateways is fundamental, dictating the device's compatibility with existing infrastructure. Analog gateways (FXS/FXO) cater to legacy phone sets and small office environments, prioritizing cost-effectiveness, while Digital gateways (E1/T1/PRI) are essential for large-scale, high-density environments like carrier core networks or sizable contact centers, focusing on throughput and robust call handling capacity.

Segmentation by interface density also plays a critical role in procurement decisions, ranging from small 2-port devices suitable for residential use up to carrier-grade chassis capable of handling hundreds of simultaneous calls across multiple E1/T1 interfaces. The choice of interface directly impacts the total cost of ownership (TCO) and the scalability potential of the communication solution. Furthermore, the segmentation by end-user application delineates the specific feature requirements; Small and Medium Enterprises (SMEs) typically require basic features such as simple routing and cost management, whereas Large Enterprises and Telecom Providers demand advanced features, including high availability (HA), robust security firewalls, complex routing logic, and comprehensive management systems.

The ongoing trend towards virtualization is blurring the lines between hardware and software segmentation, yet the fundamental need for physical interfaces to bridge the IP network to the physical world ensures the continued relevance of physical gateway segmentation. Understanding these segments is vital for vendors to align their product development with specific customer needs, whether focusing on high-margin, feature-rich digital solutions for carriers or high-volume, cost-effective analog solutions for the global SME market transitioning away from older PBX systems. This structured segmentation analysis is key to forecasting growth areas and strategic market positioning.

The value chain of the VoIP Gateways Market commences with the Upstream Analysis, dominated by component suppliers that provide essential semiconductor chips, specialized Digital Signal Processors (DSPs) necessary for compression and voice quality, and proprietary firmware components. This stage is characterized by high technical expertise and reliance on global supply chains, often centered in East Asia, for high-volume manufacturing of core electronic components. Effective supply chain management and strategic sourcing of stable, high-performance chipsets are crucial for manufacturers to maintain competitive pricing and ensure the reliability and longevity of the gateway hardware, as quality components directly influence voice clarity and system stability.

The manufacturing and assembly phase follows, where Original Equipment Manufacturers (OEMs) design, integrate, and test the gateway units. Following manufacturing, the Downstream Analysis focuses heavily on the Distribution Channel. Due to the technical nature of gateway deployment, distribution is largely handled through specialized Value-Added Resellers (VARs), System Integrators (SIs), and authorized distributors who possess the necessary expertise to provision, configure, and integrate the gateways into complex enterprise or carrier networks. Direct sales channels are typically reserved for large-scale carrier contracts or major global accounts, whereas indirect channels, comprising partners and resellers, manage the vast majority of SME and regional enterprise sales, providing localized support and maintenance services.

The post-sale segment involves installation, configuration, and ongoing maintenance, often executed by the same system integrators or specialized Managed Service Providers (MSPs). The final link in the chain is the end-user deployment within various organizations, where the gateway facilitates the critical bridge between internal IP communications and the external PSTN. The value generation in this market increasingly shifts towards the services provided post-hardware sale, including network optimization, security policy enforcement, and compliance support, differentiating vendors beyond mere hardware specifications. Strong partnerships between manufacturers and certified integrators are paramount to ensuring successful implementation and maximizing customer lifetime value.

Potential customers for VoIP Gateways are exceptionally diverse, encompassing any organization that currently utilizes or plans to integrate legacy telephone systems with modern IP-based communication infrastructure. The primary End-Users/Buyers include Small and Medium Enterprises (SMEs) that are upgrading their decades-old PBX systems but wish to retain their existing analog endpoint devices (such as fax machines, door entry systems, or specific desk phones) while accessing the cost benefits of SIP trunking and VoIP services. For these users, Analog Gateways (FXS/FXO) are essential components allowing a gradual, cost-controlled migration without a full rip-and-replace strategy for all hardware.

Large Enterprises constitute another significant customer base, particularly those with multiple geographically dispersed branch offices. These organizations deploy high-density Digital Gateways (E1/T1/PRI) to manage trunking connections with massive call volumes, integrate large-scale contact centers, and ensure business continuity by providing a reliable failover mechanism between their internal IP network and external carrier services. The requirements here are focused on scalability, high availability, advanced security features, and seamless interoperability with Tier-1 communication platforms like Microsoft Teams or Cisco Call Manager.

The third, and often largest, buyer segment comprises Telecommunication Service Providers (Carriers) and Internet Service Providers (ISPs). These entities purchase carrier-grade VoIP Gateways (often bundled within Session Border Controllers) to manage access networks, provide SIP trunking services to their business clientele, and facilitate the massive migration of their core infrastructure from legacy TDM switching networks to Next-Generation Networks (NGN) built entirely on IP. Their purchasing decisions are heavily influenced by regulatory compliance, robust reliability, signaling protocol flexibility, and the device’s ability to handle high-density traffic with guaranteed Quality of Service (QoS) metrics.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 4.25 Billion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Cisco Systems, Huawei Technologies, AudioCodes, Grandstream Networks, Patton Electronics, Sangoma Technologies, Yeastar, Matrix Comsec, Dialogic (Enghouse Systems), Epygi Technologies, OpenVox, Dinstar, Beronet, Synway, VegaStream, 3CX, Avaya, Microsoft (through partnerships), Ericsson, ZTE |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the VoIP Gateways market is constantly evolving, driven by the need for increased reliability, enhanced security, and seamless integration with next-generation networks. Session Initiation Protocol (SIP) remains the cornerstone protocol, mandating continuous development in SIP compliance and interoperability testing to ensure seamless communication across diverse vendors and platforms. A critical technological focus is on high availability (HA) architecture, utilizing features like redundant power supplies, active/standby configurations, and automatic failover mechanisms to guarantee uptime, which is non-negotiable for carrier-grade and mission-critical enterprise applications. Furthermore, support for advanced codecs, including Opus and HD Voice standards, is crucial for delivering superior voice clarity while optimizing bandwidth usage, especially relevant for international and remote connectivity.

The shift towards network function virtualization (NFV) represents a major technological inflection point. Vendors are increasingly offering Virtual Network Function (VNF) versions of their gateways, allowing the core gateway functionality to be deployed as software on commodity servers or in cloud environments. This virtualization drastically improves scalability, reduces hardware footprint, and simplifies management through centralized orchestration platforms, aligning the VoIP infrastructure with modern cloud computing paradigms. This facilitates rapid deployment and resource elasticity, key benefits for managed service providers and large telecommunication carriers seeking to modernize their core networks and adopt agile operational models that minimize reliance on specialized, proprietary hardware.

Security technologies are integrated directly into the gateway architecture. Essential features include built-in firewalls, encryption capabilities (SRTP/TLS) to secure signaling and media streams, and sophisticated mechanisms to detect and mitigate common VoIP threats like registration hijacking and toll fraud. The emerging importance of WebRTC integration also influences gateway design, as these devices must efficiently translate WebRTC signaling (often utilizing DTLS-SRTP for security) into standard SIP/RTP traffic, allowing web browser-based communication to interact seamlessly with the traditional telephony environment. This convergence necessitates gateways that act as sophisticated media relay and protocol translation points, enhancing the overall versatility and future-proofing of the communication network investment.

North America maintains its position as the market leader in the VoIP Gateways sector, primarily due to the rapid adoption rate of Unified Communications as a Service (UCaaS) among enterprises and aggressive network modernization efforts by major telecom operators in the United States and Canada. The region benefits from a highly mature IT infrastructure, robust regulatory frameworks that encourage competition and technology investment, and the dominant presence of key global VoIP and UC vendors. The high demand is also fueled by the extensive deployment of large-scale contact centers and the early implementation of hybrid work models, which necessitate robust, secure, and scalable gateway solutions to manage diverse call traffic volumes and ensure connectivity between cloud-based services and premise-based legacy systems. This technological readiness and significant enterprise spending on communication upgrades solidify North America's value share.

The Asia Pacific (APAC) region is projected to exhibit the fastest growth over the forecast period, driven by unparalleled growth in internet penetration, massive investment in mobile and fixed broadband infrastructure, and the burgeoning small and medium enterprise (SME) sector, particularly in economies such as China, India, and Southeast Asian nations. Governments in these regions are actively promoting digital transformation initiatives, leading to widespread adoption of cost-efficient communication technologies like VoIP. Although the market is highly price-sensitive, the sheer volume of new deployments and the ongoing transition from 2G/3G networks directly to 4G/5G and IP-based services ensure substantial market opportunity for vendors providing flexible, scalable, and localized gateway solutions capable of handling diverse regional signaling protocols and regulatory requirements.

Europe represents a highly competitive and mature market, characterized by stringent regulatory standards, especially related to data privacy (GDPR) and network resilience. Western European countries exhibit high saturation but continuous replacement cycles, focusing on feature upgrades, enhanced security, and energy efficiency. Eastern Europe and certain peripheral nations, however, are still undergoing significant TDM to IP migration, offering pockets of high growth potential, particularly for digital gateways connecting established enterprise PBXs to modern SIP trunks. The Middle East and Africa (MEA) region show promising growth, propelled by large-scale smart city projects and governmental initiatives aimed at upgrading telecom infrastructure, demanding robust, high-capacity gateways suitable for harsh operating environments and high-security requirements, often procured through large, multi-year carrier contracts.

The primary function of a VoIP Gateway is to serve as a protocol converter, translating voice traffic between a traditional circuit-switched network (PSTN/TDM, using protocols like PRI or SS7) and a packet-switched IP network (VoIP, using protocols like SIP). This conversion allows legacy hardware, such as analog phones and traditional PBXs, to communicate seamlessly with modern, cost-effective IP-based communication systems and vice versa, facilitating enterprise migration to unified communications platforms.

Analog Gateways (FXS/FXO) connect standard analog devices (like telephones or fax machines) directly to the IP network and are typically used for small deployments or connecting specific legacy endpoints. Digital Gateways (E1/T1/PRI) handle multiple voice channels (24 or 30 channels per interface) simultaneously and are designed for high-density traffic requirements. Large enterprises and carriers exclusively utilize Digital Gateways for efficient, high-capacity trunking connections to the PSTN or large, existing digital PBX systems.

Network Function Virtualization (NFV) is allowing vendors to offer gateway functionality as software (Virtual Network Functions or VNFs) running on commercial off-the-shelf (COTS) hardware or in cloud environments. While this reduces the need for specialized physical gateway appliances in core networks, physical hardware remains essential at the network edge to provide the necessary analog and digital interfaces to connect physical endpoints and trunks to the virtualized IP network, ensuring the hardware market remains viable.

Major security risks include Denial of Service (DoS) attacks, unauthorized network access, and severe financial losses due to toll fraud, where external attackers exploit gateway vulnerabilities to make expensive international calls. Mitigation involves deploying Session Border Controllers (SBCs) alongside gateways, mandatory encryption (SRTP/TLS), strict firewall policies, robust authentication mechanisms, and utilizing AI-driven anomaly detection tools to monitor call patterns and identify fraudulent activity in real time.

The Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR). This accelerated growth is primarily attributed to the massive scale of ongoing telecom infrastructure development, rapid adoption of digital technologies across emerging economies like India and China, substantial growth in the SME sector driving demand for cost-effective communication upgrades, and widespread government initiatives pushing the retirement of older communication networks in favor of all-IP solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.