ID : MRU_ 439026 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

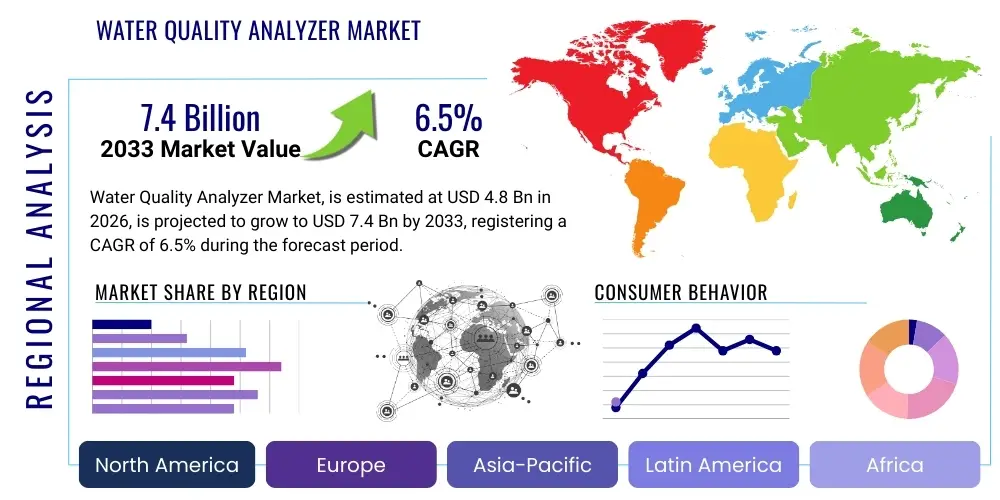

The Water Quality Analyzer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 7.4 Billion by the end of the forecast period in 2033.

The Water Quality Analyzer Market encompasses the manufacturing, distribution, and utilization of sophisticated instruments designed to measure and monitor various physical, chemical, and biological parameters of water across diverse applications. These analyzers are critical tools ensuring compliance with stringent regulatory standards related to drinking water safety, wastewater discharge limits, and industrial process control. Key components analyzed include pH, dissolved oxygen (DO), conductivity, turbidity, total organic carbon (TOC), and specific ions. The technological evolution in this domain emphasizes portability, real-time monitoring capabilities, and enhanced sensor accuracy, moving away from laborious laboratory testing towards in-situ and continuous analysis.

Water quality analyzers are essential in municipal water treatment plants, industrial facilities (such as power generation, pharmaceuticals, and food and beverage), environmental monitoring stations, and research laboratories. Their primary application lies in ensuring public health protection by detecting contaminants and preventing outbreaks caused by waterborne pathogens. Furthermore, industrial users rely on these devices to optimize manufacturing processes, prevent equipment corrosion, and adhere to environmental permits. The versatility of modern analyzers, spanning benchtop models for high-precision lab work to rugged, multi-parameter probes for field deployment, highlights their indispensable role in global water stewardship efforts.

Driving factors for sustained market growth include escalating global water pollution levels due to rapid urbanization and industrialization, leading to stricter governmental regulations regarding water usage and disposal. Increasing public awareness concerning water safety and the growing need for efficient resource management, especially in water-scarce regions, further stimulate demand for advanced monitoring solutions. The inherent benefits of utilizing these analyzers, such as improved operational efficiency, reduced risk of environmental non-compliance, and real-time data accessibility, solidify their importance in modern infrastructure and environmental protection strategies.

The Water Quality Analyzer Market is experiencing robust expansion driven by global necessity for safe water supplies and rigorous environmental compliance mandates. Business trends indicate a significant shift towards digitalization, integrating instruments with the Industrial Internet of Things (IIoT) platforms to facilitate cloud-based data storage, predictive maintenance, and remote monitoring capabilities. Key players are focusing on strategic partnerships and mergers to consolidate technology, particularly in sensor miniaturization and development of reagent-free measurement methods, aiming for lower operational costs and enhanced sustainability for end-users. The competitive landscape is characterized by innovation in portable and handheld devices that offer high accuracy and rapid response times, catering to growing demand in field testing and emergency response scenarios.

Regionally, Asia Pacific (APAC) dominates the market growth trajectory, fueled by massive infrastructure projects aimed at improving sanitation, treating industrial discharge from burgeoning manufacturing sectors, and meeting the potable water needs of densely populated urban centers, particularly in China and India. North America and Europe, characterized by established regulatory frameworks like the Safe Drinking Water Act and the Water Framework Directive, represent mature markets focused on replacing legacy systems with high-tech, automated, multi-parameter analyzers that can handle complex analytical requirements. The Middle East and Africa (MEA) and Latin America are poised for accelerated growth, supported by governmental investments in water purification and wastewater treatment infrastructure development spurred by climate change impacts and water scarcity challenges.

Segment-wise, portable analyzers are demonstrating the highest growth due to their flexibility and ease of use in diverse field applications, although laboratory-based instruments maintain their strong position in highly regulated testing environments requiring superior precision. Based on parameter type, the demand for TOC and nutrient (nitrate and phosphate) analyzers is escalating, reflecting increased concern over agricultural runoff and industrial contamination. The end-user segments show that municipal water and wastewater treatment remain the largest consumers, yet the industrial sector, particularly power generation and chemicals, is rapidly adopting advanced continuous monitoring systems to optimize operational efficiency and minimize process water usage.

User inquiries regarding the integration of Artificial Intelligence (AI) in the Water Quality Analyzer Market primarily center on transforming raw sensor data into actionable insights, predicting contamination events before they occur, and automating complex calibration and maintenance processes. Users are concerned about the accuracy and reliability of AI algorithms in interpreting highly variable water data and the necessary infrastructure investment for deploying sophisticated machine learning models. Expectations are high for AI to reduce false positives in contamination alerts, optimize chemical dosing in treatment plants based on real-time water chemistry fluctuations, and enhance the longevity and performance of installed sensor networks through proactive diagnostics. The key themes revolve around achieving predictive quality management, ensuring data security in cloud environments, and developing user-friendly AI interfaces for non-specialist operators.

The dynamics of the Water Quality Analyzer market are fundamentally shaped by stringent environmental regulations globally (Drivers), high initial capital outlay and complexities associated with calibration and maintenance (Restraints), the rapid adoption of smart, interconnected monitoring systems (Opportunities), and the significant influence of environmental activism and public health mandates (Impact Forces). The synthesis of these elements dictates the strategic direction for technology development and market penetration, pushing manufacturers toward creating highly accurate, reliable, and user-friendly monitoring solutions capable of meeting evolving regulatory thresholds for emerging contaminants. Market growth is sustained by continuous technological refinement addressing the logistical and cost barriers traditionally associated with water quality testing.

Key drivers include the global crisis of freshwater scarcity and pollution, necessitating real-time management of water resources. Governments worldwide are enforcing stricter effluent discharge standards, particularly for industrial wastewater, compelling businesses to invest in sophisticated analyzers for continuous monitoring and compliance verification. Furthermore, aging water infrastructure in developed nations necessitates comprehensive network monitoring to detect pipe leaks, intrusion events, and ensure the integrity of potable water distribution. Conversely, significant restraints impede faster adoption; these include the high initial cost of deploying extensive sensor networks and complex multi-parameter laboratory systems. Another critical restraint is the need for frequent calibration and maintenance of sensitive probes, especially in harsh environmental conditions, which requires specialized technical expertise and contributes to elevated long-term operational costs, particularly challenging for smaller municipalities or private entities.

Opportunities are abundant, primarily revolving around the deployment of cloud-connected, IoT-enabled sensors that offer remote diagnostics and predictive analytics, significantly lowering the total cost of ownership over time. The development of micro-electromechanical systems (MEMS) sensors and lab-on-a-chip technology promises miniaturization, improved portability, and lower reagent usage, expanding application scope into remote locations and personalized consumer water testing. Impact forces are predominantly driven by public health concerns and environmental watchdog groups advocating for transparency and better governmental oversight of water resources. Public pressure following water contamination incidents often triggers rapid policy changes and increased funding for monitoring infrastructure. Additionally, climate change and extreme weather events influence water quality unpredictability, serving as a powerful, non-negotiable force compelling the industry to develop robust, resilient monitoring tools capable of handling sudden and dramatic shifts in water matrix composition.

The Water Quality Analyzer Market is comprehensively segmented based on parameters measured, product type, application, and end-user, providing a granular view of demand drivers across various industries. Product segmentation distinguishes between laboratory-grade, highly precise benchtop instruments and rugged, field-deployable portable devices, along with continuous online analyzers crucial for industrial process control. Parameter segmentation highlights the varying needs for chemical, physical, and biological testing, with rapid growth observed in specialized analyzers for trace metals and emerging micropollutants. Understanding these segments is vital for targeted marketing strategies and product development focused on specific compliance requirements and operational environments.

The value chain for the Water Quality Analyzer Market begins with complex upstream activities involving the sourcing of highly specialized raw materials, including precise sensors, optical components, microprocessors, and sophisticated chemical reagents necessary for reliable measurement technology. Key upstream analysis focuses on semiconductor and advanced material suppliers whose innovations in sensor fabrication—such as ion-selective electrodes (ISEs) and advanced photometric detectors—directly influence the accuracy, stability, and lifespan of the final analyzer product. The manufacturing phase involves intricate assembly, calibration, and quality control processes to ensure compliance with international standards (like ISO and EPA methodologies). Efficiency in this stage relies heavily on lean manufacturing practices and stringent supply chain management to maintain high instrument precision while controlling production costs.

Distribution channel analysis reveals a dual structure encompassing both direct and indirect sales mechanisms. Direct channels are predominantly employed for high-value, complex, online continuous monitoring systems sold to large municipal utilities and major industrial clients, requiring specialized technical support, installation, and post-sales service delivered directly by the manufacturer or certified subsidiary. Indirect distribution involves leveraging a vast network of authorized distributors, system integrators, and independent local resellers to reach fragmented markets, including research laboratories, educational institutions, and smaller commercial enterprises. These intermediaries often provide localized inventory, basic maintenance services, and application-specific consulting, which are crucial for penetrating regional markets, especially in emerging economies where manufacturers do not have established direct footprints.

Downstream analysis centers on the installation, operation, maintenance, and data interpretation services provided to the end-users. The rising complexity of analytical instruments necessitates comprehensive training programs and robust service contracts. Service providers, often working in conjunction with manufacturers, specialize in calibration services, replacement of consumables (reagents, probes), and troubleshooting. The ultimate downstream value is realized through the effective use of generated data for decision-making—whether for regulatory reporting, process optimization, or public health protection. This emphasizes the growing importance of software integration, data analytics platforms, and cloud services in the value chain, shifting the focus beyond hardware manufacturing toward delivering holistic water intelligence solutions.

Potential customers for Water Quality Analyzers represent a broad spectrum of entities across the public and private sectors, all united by the necessity of managing, treating, or monitoring water quality to ensure operational efficacy, health compliance, or environmental stewardship. The largest single segment comprises municipal water and wastewater treatment facilities, which require continuous, high-volume monitoring solutions to manage influent quality, optimize treatment chemistry (e.g., coagulation, disinfection), and verify the quality of effluent before discharge or distribution. These customers typically purchase continuous online analyzers and robust laboratory benchtop systems for regulatory reporting, valuing long-term reliability, low maintenance costs, and integration capability with Supervisory Control and Data Acquisition (SCADA) systems.

The industrial sector constitutes a diverse and rapidly growing customer base. Within industries like power generation (boiler water quality control to prevent scaling and corrosion), chemicals and petrochemicals (process purity verification and effluent monitoring), and Food & Beverage (product consistency and sanitation validation), water quality analysis is integral to core operations. These customers frequently seek specialized, application-specific analyzers capable of handling extreme temperatures, pressures, or chemical compositions unique to their processes. The pharmaceutical and biotechnology industries are exceptionally demanding, requiring ultra-pure water (USP/EP standards) monitored by highly sensitive TOC and conductivity analyzers to prevent contamination that could compromise drug efficacy or regulatory approval.

Beyond municipal and core industrial users, significant potential exists within environmental monitoring agencies, research institutions, and the agriculture/aquaculture sectors. Environmental bodies utilize portable and remote sensing technologies for large-scale watershed monitoring, tracking non-point source pollution and ecological health. Agricultural irrigation schemes, particularly those employing reclaimed water, rely on basic analyzers for salinity and nutrient levels. Furthermore, the rising consumer interest in personal health and well-being is fostering a nascent market for simplified, smart home water testing devices, driven by increasing awareness of contaminants like lead and PFAS (Per- and polyfluoroalkyl substances) in public water supplies. These emerging markets favor low-cost, disposable sensors and user-friendly interfaces.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 7.4 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Danaher Corporation (Hach Company, OTT Hydromet), Xylem Inc., Thermo Fisher Scientific Inc., ABB Ltd., Endress+Hauser Group Services AG, Horiba, Mettler-Toledo International Inc., Emerson Electric Co., Yokogawa Electric Corporation, Agilent Technologies Inc., Lovibond Tintometer GmbH, WTW (Xylem Brand), Shimadzu Corporation, SUEZ, Swan Analytische Instrumente AG, General Electric (GE), Hanna Instruments, Myron L Company, Metrohm AG, LaMotte Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Water Quality Analyzer Market is undergoing a rapid transformation, shifting from traditional wet chemistry methods to advanced, sensor-based, digital analytical systems. A core focus is the development of intelligent sensors capable of continuous, autonomous operation with minimal recalibration. Non-reagent-based technologies, such as UV-Visible spectrophotometry and fluorescence sensors for organic matter and disinfection byproducts, are gaining prominence as they reduce operational costs and the environmental impact associated with chemical reagent disposal. Furthermore, advancements in Ion-Selective Electrode (ISE) technology are improving selectivity and stability for measuring trace elements and nutrients, overcoming historic challenges of interference and sensor drift, thus making them viable for long-term field deployment.

Miniaturization and integration are crucial technological trends, spearheaded by Micro-Electro-Mechanical Systems (MEMS) and Lab-on-a-Chip (LOC) platforms. These technologies enable the creation of highly compact, multi-parameter sensors suitable for portable and submersible applications, dramatically reducing sample volumes and analysis time. LOC devices facilitate complex chemical analysis, traditionally performed in full-scale laboratories, within a device the size of a credit card, opening up possibilities for point-of-care water testing and extensive distributed sensor networks. This integration is vital for the success of remote monitoring, allowing instantaneous data transmission from geographically dispersed monitoring points to centralized data platforms via satellite or cellular networks, essential for comprehensive watershed management.

The convergence of analytical instrumentation with digital infrastructure, specifically the Industrial Internet of Things (IIoT) and 5G connectivity, defines the current state-of-the-art. Modern analyzers are equipped with robust communication protocols (Modbus, Profibus, OPC UA) allowing seamless integration into SCADA and enterprise resource planning (ERP) systems. Data collected from distributed sensor nodes is increasingly processed using edge computing capabilities within the analyzer unit itself, ensuring faster response times for critical alarms before transmitting compressed, contextualized data to the cloud. This emphasis on digitalization not only improves operational efficiency through automated logging and compliance reporting but also enhances predictive capabilities through integration with sophisticated AI and machine learning platforms for anomaly detection and forecasting.

The global distribution of the Water Quality Analyzer market exhibits distinct patterns driven by regional economic development, regulatory stringency, and prevailing environmental challenges. North America maintains a strong position, characterized by mature regulatory oversight, high technological adoption rates, and substantial investment in replacing aging infrastructure. The region prioritizes advanced instrumentation for detecting emerging contaminants such as pharmaceutical residues and microplastics, driving demand for high-resolution mass spectrometry and sophisticated TOC analyzers. The emphasis on smart water networks in the United States and Canada fuels the market for integrated, IoT-enabled, continuous monitoring solutions that provide real-time integrity checks of extensive distribution systems.

Europe represents another key market, largely propelled by the ambitious goals set forth in the European Union’s Water Framework Directive (WFD) and the Drinking Water Directive. The market here is defined by a focus on environmental sustainability, demanding highly accurate, low-maintenance field analyzers for monitoring surface and groundwater ecology. Nordic countries and Germany, known for their strict effluent quality control, are significant early adopters of automated, process-optimized analysis systems. Innovation in Europe is geared towards developing environmentally friendly analysis methods that reduce reagent consumption and enhance the reliability of sensors in diverse ambient conditions.

Asia Pacific (APAC) is projected to be the fastest-growing region globally, attributed to rapid urbanization, explosive industrial expansion, and urgent governmental initiatives to address severe water pollution and ensure potable water accessibility for vast populations. Countries like China and India are making colossal investments in new wastewater treatment facilities and upgrading existing infrastructure, necessitating bulk procurement of both basic and advanced water quality analysis equipment. The market growth is particularly pronounced in the segment of continuous online analyzers used in thousands of newly established industrial zones for mandatory compliance monitoring of discharge streams.

Latin America and the Middle East & Africa (MEA) present significant long-term growth opportunities, although currently possessing smaller market shares compared to established regions. In Latin America, investment is concentrated in modernizing municipal treatment systems and addressing agricultural runoff pollution. The MEA region, grappling with extreme water scarcity and reliance on desalination, requires highly specialized analyzers to monitor parameters like salinity, fouling potential, and energy efficiency in large-scale reverse osmosis (RO) plants. Growth in MEA is highly dependent on governmental funding cycles and international development aid supporting water infrastructure projects.

The primary drivers include increasingly stringent global environmental regulations mandating real-time compliance reporting for industrial effluent discharge, the critical need for immediate contamination detection in municipal water distribution networks, and the integration of IIoT capabilities enabling remote monitoring and predictive maintenance, reducing operational expenditure.

AI significantly benefits water quality management by analyzing complex sensor data to predict pollution events before they manifest, optimizing chemical dosing in treatment processes for efficiency, automating sensor calibration schedules, and providing proactive diagnostics for instrument failures, thereby enhancing overall system reliability and response time.

The segmentation of portable and handheld multi-parameter analyzers exhibits the highest growth potential, driven by increased demand for efficient field testing, rapid deployment for environmental surveillance, and ease of use across diverse end-user segments, particularly in emerging economies and for non-specialist operations.

The main technical challenges involve achieving long-term sensor stability and accuracy in harsh matrices, mitigating drift that necessitates frequent calibration, developing affordable sensors for emerging contaminants (e.g., PFAS, microplastics), and ensuring cross-sensitivity reduction across multiple parameters in complex water samples.

APAC’s rapid growth is due to substantial governmental investment in new urban water and wastewater infrastructure, the necessity to manage severe pollution resulting from accelerated industrialization and population growth, and the subsequent implementation of mandatory environmental monitoring policies requiring large volumes of analytical instrumentation.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.