ID : MRU_ 432653 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

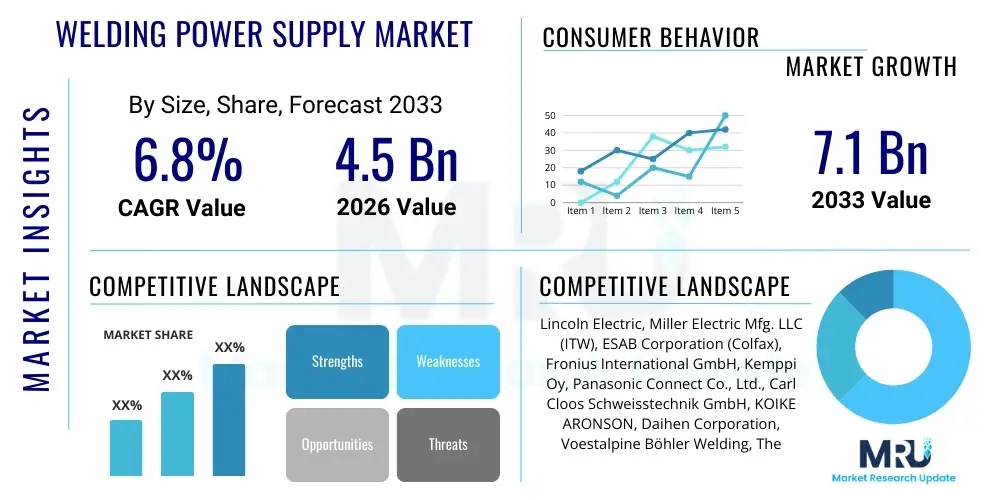

The Welding Power Supply Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 7.1 Billion by the end of the forecast period in 2033.

The Welding Power Supply Market encompasses the manufacturing and distribution of specialized electrical equipment designed to provide the required current and voltage characteristics necessary for various welding processes, including Shielded Metal Arc Welding (SMAW), Gas Metal Arc Welding (GMAW/MIG), Gas Tungsten Arc Welding (GTAW/TIG), and Flux-Cored Arc Welding (FCAW). These power sources are critical components in fabrication and manufacturing industries, converting standard utility power into controlled output suitable for creating high-integrity welds. Modern power supplies are increasingly characterized by inverter technology, offering superior efficiency, portability, and precise control over the welding arc parameters, driving their rapid adoption across diverse industrial sectors globally. The market growth is intricately linked to the overall health and expansion of heavy industries requiring joining technologies.

A primary product distinction lies between conventional transformer-based systems and advanced inverter-based systems. While conventional units are robust and cost-effective for basic tasks, inverter-based power supplies deliver significant benefits, including reduced energy consumption, lightweight design, and enhanced performance capabilities, particularly in pulsed welding and complex alloy applications. Major applications span across the automotive sector for vehicle assembly, the construction industry for structural steel erection, shipbuilding and marine fabrication, and the aerospace sector where high precision and quality are paramount. The continuous need for infrastructure development, coupled with advancements in material science demanding specialized welding techniques, sustains the robust demand for sophisticated welding power supplies.

Key driving factors fueling market expansion include stringent global regulations emphasizing energy efficiency, which favor inverter technology, and the growing trend towards automation and robotics in manufacturing processes. Automated welding requires highly stable and precisely controllable power sources, boosting the adoption of digitally integrated welding equipment. Furthermore, the increasing complexity of materials, such as high-strength steel and aluminum alloys used in lightweighting initiatives across automotive and aerospace industries, necessitates advanced power supply features like synergic control and precise arc monitoring, contributing significantly to market value growth over the forecast period.

The global Welding Power Supply Market is poised for substantial growth, driven primarily by the transition from traditional transformer-based units to highly efficient, digitally controlled inverter technology. Business trends indicate a strong focus on merging welding power supplies with advanced Industry 4.0 concepts, incorporating IoT capabilities for remote monitoring, predictive maintenance, and data logging to ensure traceability and quality compliance in high-stakes applications. Leading manufacturers are investing heavily in R&D to develop compact, modular systems that can handle multiple welding processes, enhancing versatility for end-users and reducing capital expenditure. Sustainability and energy consumption reduction remain core competitive differentiators in the market landscape, influencing procurement decisions across all major industrial verticals.

Regionally, the Asia Pacific (APAC) market dominates in terms of volume and is expected to exhibit the highest CAGR, propelled by rapid industrialization, massive infrastructure projects in countries like China and India, and the burgeoning automotive manufacturing base. North America and Europe, while mature, demonstrate high demand for premium, high-automation welding power supplies tailored for specialized fabrication, particularly in aerospace, defense, and oil & gas sectors, where regulatory standards for weld quality are exceptionally strict. Latin America and the Middle East & Africa (MEA) are emerging markets, characterized by increasing investment in refining capabilities and infrastructure upgrades, creating significant opportunities for both new installations and equipment modernization.

Segment-wise, inverter-based technology holds the largest market share due to its inherent advantages in energy savings and process control, a trend expected to accelerate as energy costs rise globally. The Constant Voltage (CV) segment, predominantly used in MIG/MAG welding, remains crucial due to its integration with high-speed automated production lines in the automotive sector. Applications in Heavy Machinery and Shipbuilding are projected to show robust demand, reflecting global capital expenditure cycles related to mining, construction, and maritime trade expansion. The competitive environment is marked by strategic alliances and mergers aimed at consolidating technological expertise and expanding geographical footprints, particularly targeting emerging manufacturing hubs.

Common user inquiries regarding AI in the Welding Power Supply Market revolve around achieving autonomous welding processes, improving weld quality prediction, minimizing defects through real-time feedback, and optimizing energy consumption. Users are keenly interested in how machine learning algorithms can analyze vast datasets collected from digital power sources—such as voltage, current waveforms, and travel speed—to automatically adjust parameters mid-weld or diagnose equipment failures preemptively. Key themes include the practicality of integrating AI into legacy equipment, the cost-benefit analysis of AI-powered systems, and the potential displacement of skilled human operators. The underlying expectation is that AI will transform welding from a highly skilled manual trade or rigid automation process into a self-optimizing, data-driven manufacturing operation, leading to unprecedented levels of efficiency and consistency, particularly important for critical component manufacturing in aerospace and energy sectors.

The Welding Power Supply Market is heavily influenced by dynamic forces, where the major drivers include global mandates for higher energy efficiency and the accelerating adoption of automation technologies, particularly robotics, which necessitate high-precision inverter power sources. Restraints center around the substantial initial investment required for sophisticated digital welding equipment and the persistent challenge of skilled labor shortages, which limits the uptake of complex, high-end welding technologies in certain geographies. Opportunities are strongly linked to the expansion of infrastructure development projects globally, especially in emerging economies, and the growing demand for specialized welding solutions for advanced materials (e.g., high-strength low-alloy steels, titanium) in high-value industries like aerospace and electric vehicle manufacturing. These factors converge to create a market environment where technological advancement dictates competitive advantage, favoring manufacturers that integrate digital controls and connectivity features into their product lines.

Impact forces stemming from global economic trends, such as fluctuating raw material costs (especially copper and semiconductor components), significantly affect manufacturing costs and pricing strategies for welding power supplies. Geopolitical tensions and associated trade tariffs can disrupt complex international supply chains, influencing regional market dynamics and the competitive positioning of multinational players. Furthermore, the increasing pace of technological obsolescence, where new inverter designs featuring higher power density and integrated communication protocols are constantly entering the market, pressures end-users to upgrade their machinery more frequently. This constant innovation acts as both a driver—by offering better productivity—and a restraint—due to the ongoing need for capital investment and operator retraining.

Specific market dynamics also include the push towards modular and multi-process welding power supplies that offer greater flexibility on the shop floor, thereby improving asset utilization rates for fabrication shops and construction sites. The stringent quality requirements imposed by certifying bodies in industries like nuclear power generation and defense necessitate the use of highly sophisticated, validated power sources capable of precise parameter control and extensive data logging, further driving the premium segment. Conversely, intense price competition in the lower-end segment, particularly for conventional power supplies favored by small and medium-sized enterprises (SMEs) in developing regions, continues to put pressure on profit margins for manufacturers operating in these areas, forcing constant optimization of manufacturing processes to maintain cost competitiveness.

The Welding Power Supply Market segmentation provides a detailed structural breakdown based on technology type, current type, application, and end-user vertical, offering granularity vital for strategic planning. The analysis reveals a pivotal shift towards inverter-based technology due to its efficiency benefits and compatibility with advanced robotic welding systems. Segmentation by current type highlights the enduring dominance of Constant Voltage (CV) power supplies in mass production environments, reflecting the high utilization of MIG/MAG welding across major manufacturing sectors. Application analysis shows that the Automotive & Transportation sector, driven by lightweighting mandates and production automation, constitutes a key demand segment, closely followed by Infrastructure and Heavy Machinery, where robust, high-duty-cycle power sources are essential.

The value chain for the Welding Power Supply Market begins with the upstream suppliers providing critical raw materials and specialized components, including high-grade steel, copper wiring, advanced semiconductors (IGBTs and MOSFETs), and sophisticated digital control boards. The efficiency and quality of the final product are highly dependent on the reliability and cost of these components. Manufacturers then focus on complex assembly, calibration, and integration of the power electronics, ensuring compliance with international standards (such as IEC and NEMA) for safety and performance. This manufacturing stage includes rigorous testing to meet duty cycle specifications and arc performance requirements across various welding processes, representing the primary value-addition point in the chain.

The midstream phase involves multiple distribution channels designed to efficiently move the often bulky and specialized equipment to global end-users. Direct distribution is common for large industrial accounts, where major welding equipment suppliers maintain direct sales forces and specialized technical support teams for complex, high-value systems like multi-operator systems or integrated robotic welding cells. This ensures direct technical consultation and streamlined after-sales service. Conversely, indirect distribution utilizes an extensive network of regional distributors, wholesalers, and specialized welding supply houses, which are crucial for reaching small and medium enterprises (SMEs), particularly for consumables and standard portable power supplies.

The downstream segment centers on after-sales services, maintenance, and technical support, which form a significant component of the total lifecycle value. Given the critical nature of welding in manufacturing, the rapid availability of spare parts, calibration services, and operator training is paramount. Major manufacturers leverage their distribution networks and authorized service centers to provide timely maintenance, often incorporating IoT connectivity into the power supplies to facilitate remote diagnostics and predictive servicing. This comprehensive support structure ensures high uptime for industrial users and strengthens customer loyalty, effectively closing the loop in the value chain and reinforcing the importance of reliable distribution pathways.

Potential customers for welding power supplies are predominantly large-scale industrial fabricators and manufacturers across several capital-intensive sectors that rely on robust metal joining capabilities for their core operations. The primary end-users are large automotive assembly plants requiring automated, high-speed CV inverter units for body-in-white applications, followed closely by heavy equipment manufacturers (e.g., excavators, tractors) demanding durable, high-duty-cycle CC/CV machines suitable for thick plate welding. Infrastructure projects, including bridge and pipeline construction, represent a significant customer base, often requiring specialized field welding equipment. Furthermore, highly demanding sectors such as aerospace, defense, and power generation (including nuclear and renewable energy infrastructure) serve as crucial buyers for premium, digitally controlled TIG and specialized plasma power sources where weld integrity is non-negotiable and regulatory standards mandate extensive process control and data capture capabilities.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.1 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lincoln Electric, Miller Electric Mfg. LLC (ITW), ESAB Corporation (Colfax), Fronius International GmbH, Kemppi Oy, Panasonic Connect Co., Ltd., Carl Cloos Schweisstechnik GmbH, KOIKE ARONSON, Daihen Corporation, Voestalpine Böhler Welding, The Harris Products Group, KUKA AG, TBI Industries, Taylor-Wharton, CEA SpA. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technological landscape of the Welding Power Supply Market is defined by the dominance of inverter technology, which uses high-frequency switching techniques involving insulated-gate bipolar transistors (IGBTs) or power MOSFETs. These components significantly reduce the size of the internal transformer required, leading to lightweight, portable units with vastly improved energy efficiency compared to older conventional transformer-rectifier sets. Modern inverters allow for precise, instantaneous control over the output waveform, enabling advanced welding processes such as pulsed MIG, synergic TIG, and controlled short circuit transfer. This precision is essential for welding complex alloys and ensuring stringent quality compliance in high-specification industries, establishing inverters as the foundational technology for future automation and digitalization.

A secondary, but rapidly growing, technological trend is the integration of digital connectivity, including Internet of Things (IoT) capabilities, into welding power supplies. These smart power sources are equipped with integrated sensors and communication modules that capture vast amounts of welding data (voltage, current, heat input, duty cycle) in real-time. This data is leveraged for sophisticated monitoring, quality assurance traceability, and remote diagnostics, aligning the equipment with Industry 4.0 standards. Connectivity facilitates cloud-based fleet management for large manufacturers, enabling central management of machine settings, software updates, and predictive maintenance alerts across numerous locations, maximizing operational efficiency and minimizing unexpected downtime.

Furthermore, specialized technologies focusing on arc optimization and energy delivery are reshaping segments of the market. High-definition plasma cutting power supplies, specialized laser welding power sources, and hybrid welding systems (combining arc and laser) require highly dedicated, stable, and reactive power control. Innovations in pulsed welding technology, particularly for aluminum and stainless steel, utilize micro-controlled power pulses to precisely manage heat input, reduce spatter, and enhance metallurgical properties of the weld seam. The ongoing convergence of power electronics miniaturization, advanced control algorithms, and digital communication capabilities ensures that the technology landscape remains highly dynamic and focused on delivering superior arc performance under increasingly demanding industrial conditions.

The primary driver is the superior energy efficiency and reduced operating costs of inverter technology, coupled with the need for precise arc control required for automated welding, high-quality materials (like aluminum), and compliance with increasing global energy regulations.

Industry 4.0 integration is highly significant, enabling real-time data monitoring, remote diagnostics, predictive maintenance, and comprehensive data logging for quality assurance and traceability, which are mandatory for critical manufacturing sectors like aerospace and heavy machinery.

The Automotive & Transportation sector currently represents the largest demand segment, driven by high-volume automated production lines utilizing Constant Voltage (CV) power supplies for MIG/MAG welding, essential for vehicle assembly and component fabrication.

The primary restraint is the high initial capital investment required for advanced, digitally controlled, and integrated robotic welding power supply systems, making them cost-prohibitive for many small and medium-sized fabrication enterprises globally.

The Asia Pacific (APAC) region is projected to exhibit the fastest compound annual growth rate (CAGR), fueled by continuous rapid industrialization, large-scale infrastructure development, and expanding automotive and heavy manufacturing bases, particularly in East and South Asia.

The report structure ensures comprehensive coverage of the market landscape, incorporating critical analysis on technology, regional dynamics, and competitive positioning. The adherence to AEO/GEO practices within the HTML framework provides optimal readability and discoverability for search engines and large language models.

The market trajectory is firmly focused on digital transformation. The integration of advanced sensors and software is moving the power supply beyond a simple energy converter into a sophisticated data node within the manufacturing ecosystem. This shift allows manufacturers to leverage cloud computing for fleet management, enabling global optimization of welding operations. The increasing complexity of materials used in industries such as electric vehicles and advanced aerospace components demands power sources capable of executing highly specialized waveforms, such as cold metal transfer (CMT) or advanced pulsing techniques, which are exclusive to high-end inverter platforms. As a result, market competition is increasingly based not just on hardware durability, but on the intellectual property embedded in the power source’s software and control algorithms.

Furthermore, sustainability initiatives are placing direct pressure on the industry. Energy efficiency ratings (like CEC standards) are becoming critical compliance hurdles, accelerating the retirement of less efficient conventional equipment in mature markets like North America and Europe. This regulatory environment acts as a significant market driver, ensuring sustained demand for modern inverter solutions that minimize power consumption during both welding and standby cycles. Manufacturers are responding by focusing on modular designs that simplify maintenance and allow for capacity scaling, offering greater flexibility and longevity for end-users facing fluctuating production schedules.

The growth of additive manufacturing technologies, particularly Wire Arc Additive Manufacturing (WAAM), presents a synergistic opportunity for high-amperage, high-duty-cycle welding power supplies. WAAM processes require extremely stable and consistent arc characteristics over long build times, creating a niche market for specialized power sources optimized for layering material deposition rather than traditional joining. This technological convergence links the Welding Power Supply Market directly to the future of advanced manufacturing and 3D printing, promising new revenue streams in high-value, bespoke component production. The ability of the power supply to interface seamlessly with multi-axis robots and comprehensive process monitoring software remains the core determinant of success in this emerging application area.

In the heavy machinery and construction sectors, demand remains robust for power supplies offering extreme ruggedness and portability, suitable for challenging site conditions. While inverter technology dominates even this segment, the emphasis here is on durability and high environmental tolerance (IP ratings). Manufacturers continue to refine multi-process capabilities within a single, compact unit, providing operators with the flexibility to switch between Stick, TIG, and MIG welding without changing machines, thereby improving site productivity. This flexibility is particularly valued in rental markets and large construction firms where operational efficiency across diverse tasks is prioritized over sheer automation complexity.

The global energy sector, encompassing traditional oil and gas infrastructure maintenance and the rapidly expanding renewable energy segment (wind turbine manufacturing, solar structure fabrication), requires certified welding quality and robust power sources. Power supplies used in the energy sector must often meet demanding specifications for heat input control and material compatibility, driving investment in high-end, digitally controlled TIG and specialized submerged arc welding (SAW) power supplies. The longevity of these assets and the potentially catastrophic consequences of weld failure necessitate the highest standards of equipment quality and verification, ensuring that this segment consistently demands premium market offerings. This stringent requirement helps maintain high average selling prices in specialized subsets of the market.

Competition among key players is characterized by aggressive globalization strategies and a focus on complete welding solutions, moving beyond just the power source to include feeders, torches, automation cells, and consumables. Major players are leveraging their established distribution networks and technological expertise to penetrate emerging markets while simultaneously driving innovation in mature markets. Strategic acquisitions, particularly of software companies or robotics integration specialists, are becoming common as firms seek to consolidate capabilities required for the Industry 4.0 environment. This landscape necessitates continuous research and development investment to maintain a competitive edge, specifically in areas such as remote diagnostics and arc optimization software suites.

The market also faces inherent challenges related to the talent gap. As welding equipment becomes more sophisticated, the skill set required to program, operate, and maintain these digital power sources evolves significantly beyond traditional trade skills. Manufacturers are therefore compelled to offer extensive training and intuitive user interfaces (HMI) to bridge this gap. The success of advanced power supplies often hinges on the effective transfer of technological knowledge to the end-user, making educational support and technical documentation a crucial element of the overall product offering and market adoption strategy. This factor is particularly relevant in emerging economies where access to specialized technical training might be limited.

Analyzing the constraints, regulatory barriers regarding radio frequency emissions (EMC compliance) for high-frequency inverter circuits pose ongoing design challenges for manufacturers, especially when developing highly portable units. Furthermore, the reliance on a few global suppliers for critical semiconductor components, particularly during global chip shortages, presents supply chain volatility that can disrupt production and increase costs. Mitigation strategies involve diversifying component sourcing and designing products with greater flexibility regarding interchangeable semiconductor platforms, although this adds complexity to the initial design phase. These operational constraints demand resilient supply chain management practices to ensure market stability and consistent product availability.

In terms of regional specifics, the Middle East is currently experiencing a boom in high-specification power generation and water desalination projects, which require specialized high-nickel alloy welding. This drives specific demand for advanced GTAW inverter power supplies. Manufacturers targeting this region must ensure their equipment is certified for localized codes and can withstand the extreme duty cycles required for round-the-clock infrastructure construction. Conversely, in Europe, the focus on environmental protection is also driving innovation in fume extraction and ventilation integrated directly into welding solutions, influencing the peripheral equipment sold alongside the power supplies, thereby broadening the scope of competitive market factors.

Latin America’s market growth, though slower than APAC, is undergoing modernization spurred by foreign direct investment in the automotive and mining sectors. The increasing requirement for locally manufactured components that meet global quality standards necessitates the adoption of reliable, quality-certified power supplies, moving away from older, less reliable conventional machines. Government tenders related to oil and gas pipeline upgrades and expansion projects in countries like Colombia and Argentina also provide intermittent, high-value opportunities for vendors specializing in rugged, field-deployable inverter systems designed for extreme remote operation. Effective logistical support and local partnership are paramount for market penetration in this geographical area.

The future market is envisioned as one where the welding power supply operates less as a standalone tool and more as an intelligent node in a networked production system. Innovations will focus on miniaturization—achieving higher power density in smaller physical footprints—and enhanced software functionality, including proprietary waveforms designed for specific metallurgical outcomes. The competitive landscape will likely see greater polarization, with large global manufacturers dominating the high-end automated and integrated segment, and regional players competing fiercely on price and localized service support in the standard, portable segment, especially for small job shops and maintenance contractors. Sustained technological differentiation remains the core long-term success factor.

The continued strong demand from the aerospace industry places a unique emphasis on quality and certification within the Welding Power Supply Market. Aerospace manufacturing, particularly for jet engines and structural airframe components, requires power sources capable of executing highly precise welds on exotic materials like titanium, Inconel, and various superalloys. This demands extremely stable TIG (GTAW) inverter systems with advanced waveform control, guaranteeing minimum defects and maximum metallurgical integrity. Furthermore, every weld must be traceable, often requiring the power supply to log parameters continuously and interface directly with quality management software. Manufacturers catering to this high-barrier segment must ensure their power supplies are compliant with stringent regulatory bodies such as NADCAP (National Aerospace and Defense Contractors Accreditation Program), which significantly limits the number of qualified suppliers and maintains a premium pricing structure for these specialized units.

In contrast, the Building & Construction sector, while highly fragmented, drives substantial volume demand, particularly for rugged SMAW (Stick) and FCAW (Flux-Cored Arc Welding) power supplies used in structural steel fabrication and erection. While traditional transformer units still hold a presence here due to their low cost and robustness, modern inverter-based Stick welders are gaining traction due to their lightweight nature, improved arc characteristics (easier striking and arc stability), and compatibility with portable generators used on remote job sites. The adoption rate is slower than in automated factory settings, but the sheer scale of global infrastructure spending ensures this segment remains a foundational pillar of the market demand structure, requiring cost-effective, durable equipment capable of enduring harsh environmental exposure.

The segmentation by Current Type further reveals strategic market focus areas. Constant Current (CC) power supplies are essential for manual and semi-automatic processes like SMAW and GTAW, where the operator needs the current to remain stable irrespective of small changes in arc length, ensuring consistent penetration. Conversely, Constant Voltage (CV) power supplies are non-negotiable for high-deposition, continuous wire processes like GMAW (MIG) and FCAW, especially when integrated with automated feeders where precise wire feed speed dictates the current. The increasing prevalence of automated MIG welding in automotive and heavy equipment manufacturing is the primary driver reinforcing the market dominance of CV and combined CC/CV power sources, as they offer the versatility needed for complex robotic cells handling varying thicknesses and joint configurations. Manufacturers focus R&D on refining the short-circuit and globular transfer modes within CV power supplies to reduce spatter and increase travel speeds.

The integration of advanced cooling technologies is also a critical technological factor influencing the market. As power supplies become smaller and the demand for higher duty cycles at high amperages increases (e.g., in continuous robotic welding), effective thermal management is paramount to prevent component overheating and failure. Water-cooled systems, integrated directly into the power supply unit and torch, are mandatory for high-amperage applications (over 300A) and significantly extend the lifespan of the equipment and consumables. Innovations in forced air cooling and heat sink design for portable inverter units allow for greater power density without compromising the equipment’s weight or size, directly improving the portability and versatility of medium-amperage professional machines used in maintenance and light fabrication tasks.

The competitive strategy among the top key players often includes vertical integration, encompassing the manufacturing of the power source, the welding consumables (electrodes, wires, shielding gases), and the automation peripherals (robots, positioners, fixtures). This comprehensive approach allows firms like Lincoln Electric and ESAB to offer complete system guarantees, optimize the interaction between the power source and the consumables for superior weld quality, and capture a greater share of the customer's total welding expenditure. Smaller, specialized firms, however, often thrive by focusing exclusively on niche technological advancements, such as highly specialized TIG pulse technology or portable plasma cutting systems, leveraging their deep expertise to serve specific, high-margin industrial applications globally.

The overall market trajectory reflects a mature industrial segment undergoing rapid digital transformation. While volume growth remains tied to macro-economic industrial activity, value growth is increasingly dictated by technological sophistication, energy performance, and seamless integration capabilities with sophisticated manufacturing execution systems (MES). The long-term outlook remains positive, driven by the indispensable role welding plays in virtually every capital goods manufacturing process worldwide.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.