ID : MRU_ 431993 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

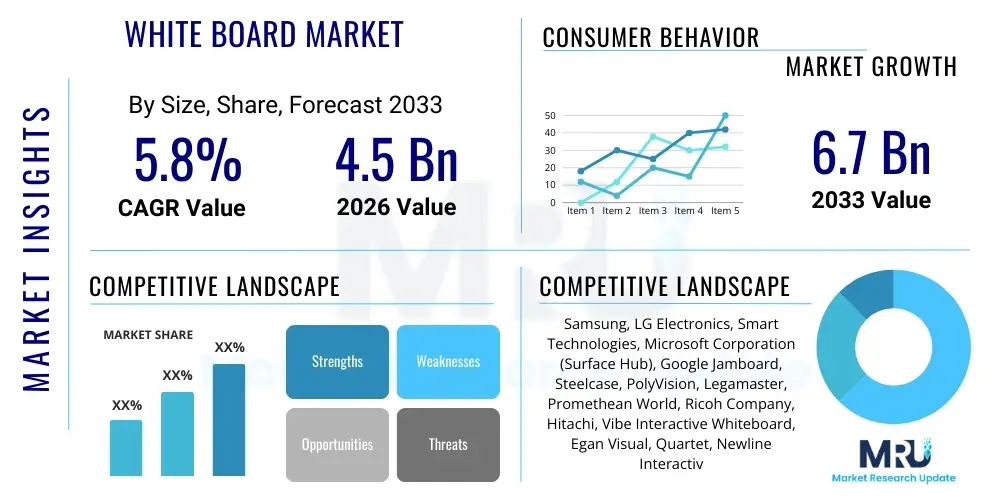

The White Board Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 6.7 Billion by the end of the forecast period in 2033. This consistent growth trajectory is driven primarily by the sustained demand in educational institutions, corporate training centers, and increasingly, small and medium enterprises (SMEs) adapting hybrid work models, requiring versatile visual collaboration tools.

The White Board Market encompasses a wide range of visual communication tools, traditionally defined by smooth, non-porous writing surfaces that allow for repeated marking and erasing. Modern whiteboards have evolved significantly, moving beyond simple melamine and porcelain surfaces to include high-tech solutions like interactive smart boards and digital collaborative platforms. Key products include traditional dry-erase boards, glass boards, mobile whiteboards, and digital interactive flat panels (IFPs) which integrate computing capabilities for enhanced collaborative sessions, remote learning, and sophisticated presentations.

Major applications of whiteboards span professional, educational, and personal sectors. In the corporate environment, they are indispensable for brainstorming, project planning, and agile development meetings. Educational institutions utilize them heavily for instructional delivery, replacing traditional chalkboards due to their cleaner use and compatibility with modern projection technology. The fundamental benefits driving market growth are their simplicity, low operational cost (for traditional boards), and their effectiveness in fostering immediate, spontaneous visual communication. Furthermore, the rise of specialized applications, such such as those in healthcare facilities for patient tracking or manufacturing for lean management visualization, continues to diversify demand.

The primary driving factors for the White Board Market include global initiatives favoring digitalization in education, the ongoing refurbishment and technological upgrade of corporate offices globally, and the increased focus on visual aids to improve information retention and engagement. While digital alternatives present competition, the tactile and easy-to-use nature of physical whiteboards ensures their continued relevance, particularly when integrated with technology, creating hybrid learning and working environments that leverage the strengths of both analog and digital communication methods.

The White Board Market exhibits robust growth, catalyzed by simultaneous trends in technological integration and renewed emphasis on visual, collaborative communication. Business trends highlight a significant pivot toward digital interactive whiteboards (IWBs) and smart displays, particularly within North American and European corporate sectors seeking to optimize meeting efficiency and support distributed teams. However, the Asia Pacific region maintains strong demand for conventional dry-erase boards due to large-scale infrastructure projects in developing educational sectors, balancing the overall market shift. Regional trends show APAC as the fastest-growing market, driven by expanding educational enrollment and government investments in digital literacy programs, while North America dominates in terms of revenue contribution due to the high adoption rate of premium, technology-enabled whiteboarding solutions.

Segment trends underscore the dominance of the Non-Interactive/Traditional whiteboard segment in volume, largely due to its affordability and wide application base in budget-conscious schools and smaller offices. Nevertheless, the Interactive White Board segment is rapidly increasing its market share in terms of value, supported by continuous innovations in touch sensitivity, software integration, and cloud compatibility. The educational end-user segment remains the cornerstone of the market, although the commercial sector, encompassing technology firms and corporate training centers, is demonstrating the highest CAGR, emphasizing products suitable for hybrid conferencing and instantaneous file sharing. Material innovations, specifically the increased adoption of glass whiteboards due to their superior durability and aesthetic appeal, also represent a crucial value-added segment influencing pricing and consumer preferences across developed economies.

Overall, the market dynamic is characterized by a dual push: maintaining steady sales of traditional, cost-effective boards while aggressively integrating advanced technology like IoT connectivity and sophisticated collaboration software into newer products. Key market players are focusing on expanding their digital ecosystems to offer seamless transition between physical and digital collaboration spaces, addressing the modern demands of flexible working and learning environments. This strategic alignment ensures that whiteboards remain relevant tools in an increasingly digitized global landscape, preventing obsolescence despite the rise of purely software-based visual tools.

User inquiries regarding AI's impact on the White Board Market primarily center on two areas: whether AI-powered software collaboration tools will render physical whiteboards obsolete, and conversely, how AI can enhance the functionality and utility of interactive whiteboards (IWBs). Key concerns revolve around the future of traditional surfaces versus advanced digital systems, with users seeking clarity on AI's role in automating meeting summaries, digitizing handwritten notes, and providing real-time coaching or content suggestion during brainstorming sessions. There is high expectation that AI integration will solve logistical challenges associated with documentation and archival of visual collaboration, making IWBs indispensable tools for data capture and knowledge management, rather than just display surfaces.

AI's primary influence is shifting the IWB from a mere input device to an intelligent collaborative hub. Natural Language Processing (NLP) and Optical Character Recognition (OCR) are critical applications that instantly translate handwritten notes, diagrams, and complex formulae into editable, searchable digital text, dramatically improving post-meeting productivity. Furthermore, AI algorithms are being developed to analyze meeting flow, recognize participant contributions, and automatically generate summarized action items or knowledge graphs, reducing the need for manual transcription and enhancing the immediate value proposition of using a smart board. This intelligence overlay transforms the market from selling hardware into providing integrated communication solutions.

For traditional whiteboards, the impact is less direct but significant. AI-driven companion apps, utilizing smartphone cameras, can accurately capture and enhance images of non-digital whiteboards, applying straightening and clean-up filters to achieve near-digital quality documentation. This bridging technology helps extend the longevity and utility of lower-cost, non-interactive surfaces, integrating them partially into the digital workflow. Ultimately, AI is positioned as a powerful differentiator for premium products, fueling innovation in gesture recognition, personalized user interfaces, and adaptive learning environments, solidifying the market’s pivot towards high-value digital solutions.

The White Board Market is shaped by a confluence of powerful drivers (D), significant restraints (R), and compelling opportunities (O), creating varied impact forces across different segments. Key drivers include the global expansion of digital classrooms, which mandates the integration of Interactive White Boards (IWBs) to facilitate blended learning and pedagogical innovation. Additionally, the proliferation of agile and lean management methodologies in the corporate sector drives demand for large, accessible, and often mobile, visualization tools essential for sprints, kanban tracking, and project oversight. These drivers collectively necessitate continuous hardware and software upgrades, supporting sustained market value growth, particularly in technologically advanced regions.

Conversely, the market faces notable restraints, primarily stemming from the high initial capital investment required for advanced IWBs, which often acts as a barrier to entry for institutions in developing nations or budget-constrained public schools. Furthermore, the rapid growth and availability of purely digital, software-based collaboration tools (such as virtual whiteboarding apps like Miro or Mural) pose a substitution threat, potentially cannibalizing the market share of hardware-focused solutions, especially in fully remote or cloud-native environments. Addressing user adoption challenges, particularly training staff on sophisticated IWB software functionality, also remains a consistent hurdle that slows deployment across heterogeneous organizational structures.

Opportunities within the market are vast, centering on the untapped potential within niche applications, such as specialized magnetic boards for healthcare logistics or ruggedized boards for industrial and manufacturing environments. The strongest opportunity lies in developing integrated hardware-software ecosystems that offer seamless cloud connectivity, enhanced security features, and cross-platform compatibility, targeting the burgeoning hybrid work model globally. Impact forces are heavily tilted towards technological change, where innovation in display technology (e.g., Ultra HD, OLED) and seamless user experience dictate competitive advantage, pushing traditional manufacturers to collaborate with software developers or invest heavily in proprietary operating systems to remain relevant.

The White Board Market is comprehensively segmented based on material, product type, end-user application, and geographical region, allowing for granular analysis of market dynamics and targeted strategic planning. Segmentation by material separates the market into high-durability surfaces like porcelain steel and glass, which command premium pricing, versus more economical options such as melamine, typically favored in short-term or low-traffic environments. Product type segmentation distinguishes between the traditional, non-interactive (dry-erase) boards, which account for the largest volume, and the rapidly growing interactive whiteboards (IWBs), which drive the majority of market value growth due to their advanced features and higher price points.

Crucially, the end-user segmentation reveals the structural demand landscape, classifying consumption into education (the historically largest segment), commercial/corporate (the fastest-growing segment driven by high-tech corporate offices and training facilities), and government/healthcare (focused on specific, durable, and often mobile applications). Understanding these segments allows vendors to tailor product features—for instance, focusing on compliance and durability for healthcare, or sophisticated cloud integration and security for corporate clients. The varying rates of digitalization across these end-user segments significantly impact the uptake of interactive versus traditional boards, with commercial and higher education sectors showing higher affinity for digital solutions.

Geographical segmentation provides insight into regional maturity and growth potential. North America and Europe typically prioritize sophisticated IWBs and high-end glass boards due to established digital infrastructure and high corporate IT budgets. Conversely, Asia Pacific and Latin America are the primary growth engines for traditional boards and entry-level digital whiteboards, driven by massive investments in foundational educational infrastructure and rapid urbanization. Analyzing these segmented demands is essential for optimizing supply chain logistics and marketing efforts to capitalize on regional spending priorities and technological readiness.

The value chain for the White Board Market commences with upstream analysis, focusing on the sourcing and processing of raw materials. This includes the manufacturing of core materials such as steel (for backing and porcelain coating), specialized glass (for premium boards), and chemicals used in the production of melamine surfaces and dry-erase markers. Key upstream activities involve quality control of magnetic substrates and the application of high-durability coatings like ceramic enamel. The profitability and stability of manufacturers are highly dependent on the cost fluctuations and supply reliability of these basic industrial materials, making relationships with primary steel and glass suppliers critical.

Midstream activities involve the primary manufacturing and assembly of the boards, including frame construction, installation of mounting hardware, and, critically for interactive boards, the integration of sensors, touch technology (e.g., infrared, electromagnetic, or capacitive), and computing modules. This stage is dominated by specialized OEMs and ODMs, who focus on optimizing production scale, minimizing manufacturing defects, and adhering to international standards for safety and environmental compliance. Differentiation at this stage is achieved through superior display technology integration, robust software development, and aesthetic design improvements, particularly for glass and mobile whiteboards designed for modern office spaces.

Downstream analysis centers on distribution channels, which are diverse and highly segmented. Traditional dry-erase boards are frequently sold through broad retail channels, office supply chains (both physical and e-commerce), and wholesale distributors serving small businesses and individual consumers. Conversely, interactive whiteboards often require a more specialized distribution model: direct sales to educational institutions and corporate clients, utilizing certified system integrators and specialized Value-Added Resellers (VARs). These VARs provide crucial services like installation, staff training, and ongoing technical support, acting as the indirect channel that drives adoption of high-value digital solutions. The direct channel is preferred for large-scale government and defense contracts where customization and security are paramount, streamlining the procurement process and ensuring compliance with stringent specifications.

Potential customers for the White Board Market are broadly categorized into institutions requiring large-scale visual collaboration tools and professional entities focused on advanced technological integration for complex decision-making processes. The largest enduring segment of end-users remains the global Education Sector, ranging from K-12 schools adopting foundational dry-erase boards to universities and technical colleges investing heavily in interactive panels for specialized lectures, distance learning infrastructure, and research collaborations. These buyers prioritize durability, ease of maintenance, educational software compatibility, and bulk purchasing discounts.

The second major segment is the Commercial and Corporate sector, including technology firms, consulting agencies, financial institutions, and specialized training centers. These customers are the primary drivers of demand for premium products, particularly high-aesthetic glass boards and advanced Interactive Flat Panels (IFPs). Corporate buyers seek seamless integration with existing Unified Communications (UC) platforms, high-resolution displays suitable for video conferencing, robust security features, and software that supports Agile project management frameworks. Their purchasing decisions are often dictated by return on investment related to meeting efficiency and collaboration improvement across geographically dispersed teams.

Further potential lies within the Governmental, Healthcare, and Industrial sectors. Healthcare facilities utilize whiteboards for operational purposes such as patient status tracking, scheduling, and procedural visualization, requiring specialized non-porous and easy-to-clean surfaces. Government agencies, including defense and public administration, demand secure and durable solutions for planning and briefing rooms. Industrial environments, especially manufacturing plants employing lean principles, utilize visual management boards (VMBs) to track quality, safety, and production metrics. These specialized customers prioritize robustness, mobility, and specific environmental resistance, representing highly lucrative, albeit smaller, niche markets for tailored whiteboarding solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 6.7 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Samsung, LG Electronics, Smart Technologies, Microsoft Corporation (Surface Hub), Google Jamboard, Steelcase, PolyVision, Legamaster, Promethean World, Ricoh Company, Hitachi, Vibe Interactive Whiteboard, Egan Visual, Quartet, Newline Interactive, Boxlight Corporation, ViewSonic, ClearOne, Panasonic, Dell Technologies |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the White Board Market is currently defined by the rapid convergence of traditional display mechanisms with sophisticated computing and sensor technologies, primarily centered around Interactive White Boards (IWBs) and Interactive Flat Panels (IFPs). Key technologies employed in this segment include various touch detection methods: Infrared (IR) technology, which utilizes LED arrays around the screen edge; Electromagnetic Resonance (EMR) technology, offering high precision typically for pen input; and Projected Capacitive (P-Cap) touch, increasingly favored for its multi-touch capabilities and sleek, bezel-less design akin to modern tablets. Software integration is equally critical, utilizing proprietary operating systems (often Android or Windows-based) optimized for collaborative applications, secure cloud storage, and integrated video conferencing capabilities.

Beyond touch interfaces, advancements in display technology, such as 4K and 8K resolution panels, are enhancing the visual appeal and clarity of digital whiteboards, crucial for large lecture halls and high-stakes corporate presentations. Furthermore, the integration of Internet of Things (IoT) connectivity allows IWBs to function as central hubs in smart classrooms and smart offices, enabling remote diagnostics, usage tracking, and seamless integration with room control systems and enterprise resource planning (ERP) platforms. This network connectivity extends the value proposition from a simple display to a complex, data-generating asset essential for organizational efficiency monitoring.

The innovation trajectory also includes significant development in pen and writing technology. Manufacturers are focusing on low-latency digital pens that mimic the feel of traditional dry-erase markers, incorporating pressure sensitivity and tilt recognition for a more natural writing and drawing experience. Additionally, cloud-based digital inking technology ensures that content written on one board can be instantly accessed and edited on another device globally, supporting distributed team collaboration. For traditional whiteboards, technological improvements are focused on optimizing surface coatings for reduced ghosting, enhanced erasability, and increased scratch resistance, extending the product lifecycle and maintaining functional superiority over basic paint-on surfaces.

North America holds a dominant position in terms of market value, driven by the high adoption rate of premium Interactive Flat Panels (IFPs) and advanced digital collaboration tools within the corporate sector. The United States, in particular, showcases high penetration in Fortune 500 companies and a significant trend towards modernizing existing office infrastructure to support flexible and hybrid work environments. The strong presence of technology giants and aggressive investment in Research and Development (R&D) leads to quick uptake of next-generation whiteboarding solutions incorporating AI, sophisticated gesture control, and robust cloud connectivity.

The regional market is characterized by a strong consumer preference for high-quality materials, such as glass whiteboards, which are favored for their aesthetic appeal, durability, and superior marker performance. Educational institutions, especially at the university level, are significant buyers, leveraging government funding and private endowments to integrate comprehensive distance learning systems centered around IWBs. This advanced infrastructure demand places North America at the forefront of market innovation, often setting the benchmark for feature sets and software compatibility that later cascade to other global markets.

Competitive dynamics in NA are intense, with major global technology players vying for market share by focusing heavily on ecosystem services, warranty packages, and integration support. Key market activities include strategic partnerships between hardware manufacturers and software providers to ensure seamless interoperability with corporate IT standards. The high disposable income and cultural acceptance of technology adoption ensure that while volume growth may be slower than APAC, the average selling price (ASP) and overall market revenue contribution remain superior.

The European market for whiteboards is mature and stable, exhibiting steady growth, particularly within the Interactive White Board segment. Key drivers include stringent regulatory standards promoting digital literacy and accessibility in schools (especially in Western European nations like Germany, the UK, and France) and robust investments in public sector digitization initiatives. Europe shows a balanced demand between high-end digital solutions for corporate boardrooms and high-quality, durable traditional boards for manufacturing and small to mid-sized educational facilities.

Regional variations are notable; Scandinavian countries exhibit extremely high adoption of smart classroom technology, favoring energy-efficient and highly integrated IWB solutions. Conversely, Central and Eastern European nations are experiencing rapid infrastructure development, driving significant initial demand for traditional, cost-effective dry-erase boards, though this is quickly followed by investments in foundational digital whiteboards. The emphasis across Europe is often placed on sustainability and local sourcing, influencing manufacturers to prioritize eco-friendly materials and energy-efficient display technologies.

Furthermore, Europe's decentralized corporate landscape fosters demand for highly flexible mobile whiteboarding solutions that support quick configuration changes in meeting spaces and project rooms. The emphasis on data privacy (GDPR compliance) significantly impacts the software features of interactive whiteboards, necessitating advanced encryption and secure local data storage options, which differentiate European product offerings from those primarily focused on simple cloud integration.

Asia Pacific is undeniably the most dynamic and fastest-growing region in the White Board Market, characterized by immense demand volume, fueled by rapid urbanization, massive population growth, and escalating government investments in educational infrastructure across populous countries like India, China, and Indonesia. While the digital segment (IWBs) is growing rapidly in developed economies such as Japan, South Korea, and Australia, the bulk of the volume growth originates from the Traditional White Board segment, driven by the sheer scale of new school construction and office establishment.

The APAC market is highly price-sensitive, leading to a strong competitive landscape for affordable melamine and basic porcelain steel boards. However, the corporate and higher education segments in metropolitan areas are quickly embracing high-end Interactive Flat Panels to compete globally, viewing them as essential tools for international collaboration and attracting top talent. China dominates regional manufacturing and consumption, with domestic players competing fiercely on price and feature integration tailored to local standards and curricula.

The transition from traditional to interactive boards is proceeding unevenly across the region. Developed coastal cities are often early adopters of high-tech solutions, whereas vast rural and interior areas rely on basic, durable, and low-maintenance solutions. This duality requires global vendors to maintain a dual strategy: offering cutting-edge digital products tailored for mature markets and scalable, cost-effective traditional solutions for emerging economies, making logistical complexity and efficient supply chain management paramount to success in APAC.

The Latin American White Board Market is steadily progressing, driven primarily by governmental initiatives aimed at improving public education infrastructure and increasing private sector investment in corporate training. Brazil and Mexico represent the largest markets within LATAM, exhibiting moderate growth in both the traditional and early-stage interactive segments. Economic volatility in several key economies poses a restraint, often causing large-scale public sector procurement projects to be delayed or scaled back, impacting the stability of long-term demand.

The primary growth driver is the replacement of outdated chalkboards in educational settings with basic dry-erase boards, representing a significant volume opportunity for entry-level products. In the commercial sector, the adoption of Interactive White Boards is slower than in North America and Europe, often limited to multinational corporation subsidiaries and high-growth technology startups that can afford the higher upfront investment. Affordability and localized technical support are key determinants of market penetration.

Vendors operating in LATAM must navigate complex import regulations and currency fluctuations. The market preference generally leans towards durable, ruggedized products that can withstand variable climate conditions and infrastructure limitations. Successful market entry often requires strong local partnerships, robust customer service networks, and the ability to offer flexible financing options to institutional buyers, mitigating the impact of large capital expenditures on tight organizational budgets.

The Middle East and Africa region presents a market of significant contrast. The Middle Eastern Gulf Cooperation Council (GCC) countries (e.g., UAE, Saudi Arabia, Qatar) are characterized by massive governmental investment in high-tech educational complexes and ambitious corporate diversification projects. These countries represent a high-value market for premium, state-of-the-art Interactive Flat Panels and sophisticated meeting technology, often integrating the latest technologies ahead of global adoption curves, supported by substantial oil wealth and strategic vision.

In stark contrast, the African market, particularly Sub-Saharan Africa, is dominated by demand for basic, durable, and highly cost-effective traditional whiteboards, essential for foundational education and burgeoning small businesses. The growth here is volume-driven, constrained by infrastructure deficits, limited access to reliable electricity, and lower IT budgets, making advanced IWB technology deployment challenging outside of major urban centers.

Market strategies in MEA must be bifurcated: a high-specification, service-intensive approach targeting the technologically advanced and wealthy Gulf states, focusing on installation, maintenance contracts, and luxury product lines; and a low-cost, high-volume distribution strategy for the African continent, focusing on reliability and logistics efficiency. The long-term opportunity in MEA is substantial as digital infrastructure continues to expand, promising future migration from traditional to digital whiteboarding solutions across the entire region.

The White Board Market is projected to exhibit a steady Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. This growth is primarily fueled by accelerated adoption of Interactive White Boards (IWBs) in education and corporate sectors globally.

Software-only tools pose a substitution threat, particularly in fully remote settings. However, hardware manufacturers are countering this by integrating advanced cloud connectivity, AI features, and cross-platform compatibility into Interactive Flat Panels, transforming them into hybrid, superior collaborative hubs.

The Commercial and Corporate sector currently represents the fastest-growing end-user segment for high-value IWBs, driven by the necessity for advanced tools to support agile methodology, hybrid work environments, and efficient video conferencing capabilities.

Premium whiteboards are differentiated by 4K/8K display resolution, high-precision Projected Capacitive (P-Cap) touch technology, low-latency digital inking, and embedded Artificial Intelligence (AI) for automated transcription and content summarization features.

The Asia Pacific (APAC) region, particularly emerging economies like India and China, demonstrates the highest volume demand for cost-effective, traditional (non-interactive) whiteboards due to large-scale investments in basic educational infrastructure and high population growth.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.