ID : MRU_ 433069 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

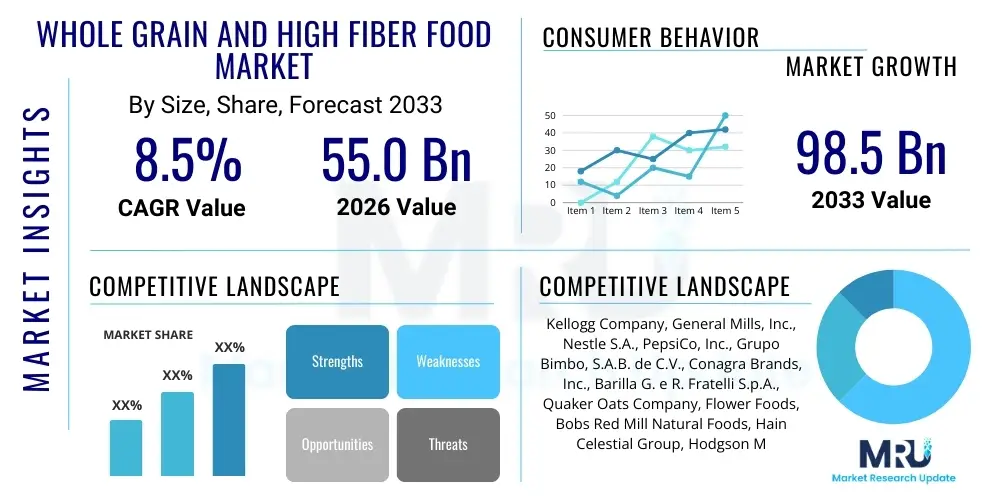

The Whole Grain and High Fiber Food Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at $55.0 Billion USD in 2026 and is projected to reach $98.5 Billion USD by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by a global paradigm shift toward preventative healthcare and increasing consumer awareness regarding the profound long-term benefits associated with dietary fiber intake, particularly in managing chronic conditions such as cardiovascular disease and type 2 diabetes. Furthermore, continuous innovation in taste and texture, moving whole grain products beyond traditional offerings into appealing snack and ready-to-eat formats, significantly contributes to market traction across diverse demographic segments.

The Whole Grain and High Fiber Food Market encompasses a wide variety of food products formulated or enriched with ingredients derived from whole grains, such as wheat, oats, barley, and rye, alongside products featuring high concentrations of soluble and insoluble dietary fiber. These foods are recognized globally for their superior nutritional profiles, providing essential micronutrients, phytochemicals, and complex carbohydrates crucial for maintaining optimal digestive health, regulating blood sugar levels, and lowering cholesterol. Major applications span across breakfast cereals, bakery products, functional snacks, and specialized dietary supplements, targeting consumers focused on health, wellness, and weight management.

Key benefits driving consumer adoption include improved gut microbiota health, enhanced satiety leading to better weight control, and a documented reduction in the risk profile for major non-communicable diseases. The market landscape is characterized by intense product development, focusing on overcoming sensory barriers traditionally associated with high-fiber foods. Driving factors include escalating rates of obesity and lifestyle diseases globally, aggressive health promotion campaigns by governmental bodies, and a steady increase in disposable income allowing consumers to choose premium, functional food items over conventional alternatives. This convergence of consumer education and regulatory encouragement firmly positions the market for sustained growth.

The global Whole Grain and High Fiber Food Market is characterized by robust business trends centered on clean label movements, product premiumization, and strategic mergers and acquisitions aimed at expanding ingredient sourcing capabilities and retail distribution networks. Business strategies are increasingly focused on developing hybrid products that successfully integrate whole grains into convenient formats, such as plant-based meat alternatives and nutritional bars, capturing the rapidly expanding on-the-go consumption segment. Furthermore, the push towards sustainable and ethical sourcing of grains is becoming a non-negotiable factor for leading industry players, influencing procurement practices and consumer trust.

Regional trends indicate that North America and Europe currently dominate the market, propelled by strong regulatory standards defining whole grain content and high levels of consumer education and acceptance. However, the Asia Pacific region is demonstrating the highest growth trajectory, primarily fueled by rising middle-class disposable incomes, the rapid Westernization of diets, and increasing awareness of preventative nutrition, particularly in urban centers of China and India. Segmentation trends highlight that the fortified/functional bakery segment remains a key revenue generator, while the high-fiber snack category, including chips, crackers, and nutritional mixes, is registering the fastest growth, appealing directly to the younger, health-conscious demographic.

Common user questions regarding AI’s impact on the Whole Grain and High Fiber Food Market revolve around supply chain predictability, personalized nutrition development, and automation in quality control (QC). Users frequently inquire about AI's ability to predict optimal planting and harvest times for specialty grains to mitigate climate risk, and how machine learning algorithms can analyze individual dietary requirements to formulate bespoke high-fiber food products. Concerns often focus on the investment required for integrating AI systems into traditional milling and processing plants, and the potential displacement of manual labor in QC. Overall, the theme is one of efficiency and hyper-personalization, with expectations that AI will significantly streamline production from farm to consumer plate, minimizing waste and maximizing nutritional efficacy through predictive modeling.

The application of Artificial Intelligence is revolutionizing the processing and distribution of whole grains by enhancing operational efficiencies and enabling unprecedented product customization. In raw material management, AI-driven analytics systems process vast amounts of data—including soil health, climate predictions, and historical yield—to optimize grain sourcing, ensuring consistent supply of high-quality ingredients like specialized oats or ancient grains. This predictive capability significantly reduces supply chain volatility, which is crucial given the agricultural dependency of this market segment. Furthermore, AI facilitates better inventory management and demand forecasting for perishable bakery items, minimizing food waste and improving profitability.

On the consumer side, AI algorithms are fundamental to the emerging personalized nutrition sector. By analyzing data derived from wearable technology, consumer genetic profiles, and self-reported dietary intake, AI can guide food manufacturers in formulating products specifically tailored to optimize an individual’s gut microbiome health or address specific nutritional deficiencies. This personalization extends to marketing, where AI determines optimal channels and messaging to target specific consumer segments interested in high-fiber solutions for specific health outcomes (e.g., digestive support versus cardiac health). This hyper-segmentation ensures marketing spend is highly efficient and resonates deeply with the target audience seeking functional food benefits.

The Whole Grain and High Fiber Food Market is propelled by powerful Drivers, yet constrained by notable Restraints, simultaneously presenting diverse Opportunities, all shaped by internal and external Impact Forces. The primary driver is the accelerating consumer recognition of the link between gut health, mental well-being, and overall immunity, solidifying the perception of fiber as a foundational functional ingredient. Restraints often center on the higher cost of production and ingredients compared to refined alternatives, alongside sensory challenges, as consumers sometimes perceive whole grain products as having a less appealing texture or taste profile. Opportunities lie in the exploitation of specialized ancient grains (like teff, farro, and amaranth) and the incorporation of novel fiber sources (such as resistant starches and specific types of prebiotics) into mainstream foods, extending the category beyond traditional cereal and bread formats. These forces collectively dictate the speed and direction of market penetration and product innovation.

Impact forces significantly shaping this environment include stringent global food safety regulations requiring verifiable claims for whole grain content, which enhances consumer trust but increases compliance costs for manufacturers. Societal shifts, particularly the global aging population, amplify the demand for foods supporting chronic disease management, creating a sustained market pull. Furthermore, intense competition from the supplement industry, which often provides fiber in convenient capsule or powder forms, acts as an external competitive force requiring constant product innovation from food manufacturers to maintain relevance. Technological advancements in food science, particularly in microencapsulation techniques, are critical internal forces allowing fibers to be incorporated into foods without altering their desired texture or flavor, thereby mitigating a major historical restraint and expanding application possibilities into beverages and confectionery.

The Whole Grain and High Fiber Food Market is meticulously segmented based on Product Type, Application, and Distribution Channel, allowing manufacturers to precisely target consumer needs. Product type segmentation distinguishes between baked goods (breads, pastries, muffins), breakfast cereals (ready-to-eat and hot cereals), snacks (bars, crackers, crisps), and others (including pastas, flours, and specialized ingredients). Application segmentation categorizes products based on their primary consumption purpose, such as health and wellness, weight management, and disease prevention, reflecting the increasing functional role of these foods. Analysis of these segments is crucial for identifying areas of high growth, such as the increasing demand for whole grain components in plant-based food manufacturing and the premiumization of gluten-free whole grain options.

The market structure is deeply influenced by the Distribution Channel, which includes supermarkets and hypermarkets, convenience stores, online retail, and specialized health food stores. The online retail segment is particularly dynamic, leveraging digital platforms to educate consumers about product benefits and facilitating direct-to-consumer sales for niche, high-value ancient grain products. Understanding the relative growth rates across these channels helps stakeholders optimize logistics and inventory strategy. For instance, while supermarkets still hold the largest share due to volume sales, specialized health food stores often drive initial adoption and testing of new, innovative high-fiber ingredients before they transition to mass market retail, providing valuable early indicators of market acceptance.

The Value Chain for the Whole Grain and High Fiber Food Market begins with the highly specialized Upstream Analysis, focusing on the sourcing and sustainable cultivation of various whole grains (oats, quinoa, spelt, etc.) and fiber sources (inulin, chicory root). This stage involves rigorous quality control measures, often including blockchain technology for traceability back to the farm, ensuring organic or non-GMO status, and minimizing pesticide residue. Milling and primary processing constitute the crucial transformation step, where advanced techniques are required to separate grains while preserving the bran, germ, and endosperm—a key differentiator from refined grain processing. Strategic alliances with certified sustainable farmers and specialized ingredient suppliers are essential at this stage to guarantee consistent quality and volume.

The Midstream component involves sophisticated processing and manufacturing, where raw ingredients are formulated into final products like breads, cereals, and snack bars. This stage is characterized by R&D investment focused on shelf-life extension and sensory improvement, often utilizing specialized blending and extrusion technologies to maintain desired texture while maximizing fiber content. Downstream Analysis centers on distribution and retail. The distribution channel is often complex, involving cold chain logistics for fresh baked goods and specialized warehousing for dried goods. The channel includes Direct sales (e-commerce for specialized products), and Indirect sales (major supermarkets and food service providers). Effective logistics management is paramount due to the typically lower shelf stability of whole grain products compared to refined, heavily processed alternatives.

The role of specialized marketing and consumer education is integrated throughout the chain, acting as a crucial element in converting consumer interest into purchase behavior. Since whole grain claims are often regulated, transparent labeling and effective communication about the nutritional benefits are critical for success at the retail level. Direct distribution, primarily through online platforms, allows manufacturers to capture higher margins and establish stronger brand loyalty by providing detailed product information and personalized nutritional advice, contrasting with the volume-driven, competitive pricing landscape characteristic of indirect sales through large retailers.

The Whole Grain and High Fiber Food Market targets a broad yet defined spectrum of End-Users/Buyers, with a central focus on health-conscious consumers spanning across all age demographics. The primary customer segment includes individuals aged 35 to 65 who are actively seeking dietary solutions for the prevention or management of chronic lifestyle diseases such as hypertension, high cholesterol, and type 2 diabetes. These buyers prioritize ingredient purity, verifiable health claims, and are often willing to pay a premium for certified whole grain or high-fiber products that simplify their nutritional management regimen.

A second crucial segment comprises Millennials and Gen Z who prioritize gut health, holistic wellness, and sustainable food sourcing. This younger demographic drives demand for innovative, convenient formats such as high-fiber functional beverages, nutrient-dense breakfast bowls, and whole grain snack alternatives. They are highly influenced by digital information, seek out clean-label products, and demand transparency regarding sourcing and environmental impact. Furthermore, institutional buyers, including hospitals, schools, and corporate cafeterias, represent a significant B2B segment, increasingly constrained by public health mandates to integrate more whole grain options into their meal planning, often requiring bulk, cost-effective solutions without compromising certified quality standards.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $55.0 Billion USD |

| Market Forecast in 2033 | $98.5 Billion USD |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Kellogg Company, General Mills, Inc., Nestle S.A., PepsiCo, Inc., Grupo Bimbo, S.A.B. de C.V., Conagra Brands, Inc., Barilla G. e R. Fratelli S.p.A., Quaker Oats Company, Flower Foods, Bobs Red Mill Natural Foods, Hain Celestial Group, Hodgson Mill, Cargill, Incorporated, Ardent Mills, ADM (Archer Daniels Midland Company), Associated British Foods plc, Limagrain Cereal Ingredients, Kashi Company, Whole Foods Market (Amazon), SunOpta Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The manufacturing of whole grain and high fiber foods relies heavily on precision technology to overcome challenges related to flavor, texture, and shelf stability, without compromising the nutritional integrity of the final product. A foundational technology is Advanced Milling Techniques, specifically designed to process the entire kernel (bran, germ, and endosperm) while minimizing damage to fragile oils and vitamins. Techniques like roller milling modifications and specialized grinding processes ensure that whole grain flours maintain superior nutritional profiles compared to traditionally milled varieties. Furthermore, High-Pressure Processing (HPP) and aseptic packaging technologies are increasingly employed, particularly for ready-to-eat whole grain snacks and beverages, extending shelf life naturally without relying on chemical preservatives, aligning with the consumer demand for clean labels and minimal processing.

Extrusion Technology is another crucial process, particularly for whole grain breakfast cereals, snack pellets, and pasta. Modern extruders are highly sophisticated, allowing manufacturers to control shear, heat, and moisture precisely to create complex shapes and textures while integrating various fiber sources, such as resistant starch or soluble fibers, into the matrix. This technology is vital for producing palatable and highly digestible products. Moreover, Food Science advancements in Flavor Masking and Sensory Modification are critical; natural compounds and specialized processing aids are developed to neutralize the bitter or gritty notes often associated with high fiber content, making whole grain consumption more appealing across diverse product applications, including fortified dairy and confectionery.

Finally, the integration of Digital Traceability Systems, powered by blockchain, is transforming supply chain integrity. Given the premium nature and certification requirements (e.g., Whole Grains Council stamp, organic status), consumers and regulators demand proof of provenance. Blockchain provides an immutable, transparent ledger tracking the grain from the farm field through processing to the final retail shelf. This technology not only ensures compliance and authenticity but also acts as a powerful marketing tool, building consumer trust in the high quality and certified nature of the whole grain ingredients used, distinguishing premium market offerings from conventional competitors.

The global consumption landscape for whole grain and high fiber foods presents significant regional disparities in maturity, growth rate, and product preferences. North America, encompassing the United States and Canada, currently holds the largest market share, characterized by high consumer awareness, strong regulatory support from entities like the FDA, and a mature industry infrastructure capable of mass production and innovation. The regional demand is heavily skewed towards convenience, driving the success of fortified whole grain breakfast items, nutritional bars, and whole wheat bread alternatives. High rates of obesity and associated chronic diseases ensure sustained investment in functional whole grain solutions.

Europe represents a highly discerning market, with countries like Germany, the UK, and Scandinavian nations showing robust consumption patterns driven by established health cultures and strict governmental guidelines regarding nutritional labeling and whole grain claims. The European market prioritizes sustainability and organic certification; therefore, ancient grains and specialty fibers sourced locally often command premium prices. Regulatory bodies in the European Union have actively promoted the consumption of fiber for public health, which continues to underpin steady market expansion and product diversification into healthy ready-meals and artisan bakery items utilizing whole grain flours.

Asia Pacific (APAC) is projected to be the fastest-growing region, presenting substantial untapped potential. Economic growth, rapid urbanization, and the consequent shift away from traditional diets towards Western dietary patterns—coupled with increasing rates of chronic illness—are fueling demand, particularly in China, India, and Japan. While traditional staples like rice and noodles still dominate, there is exponential growth in whole grain snacks, fortified biscuits, and ready-to-eat whole grain cereals, especially among the affluent, health-conscious urban population. Manufacturers are focusing on localized product formulations, such as whole grain variations of popular local snacks, to penetrate this high-growth market effectively. Latin America and the Middle East & Africa (MEA) are emerging markets, where growth is currently concentrated in urban centers, driven largely by imported high-value products and increasing awareness campaigns targeting nutritional deficiencies.

The primary driver is the global increase in chronic lifestyle diseases, such as cardiovascular issues and type 2 diabetes. Consumers are actively seeking preventative dietary solutions, recognizing the scientific evidence linking high-fiber and whole grain intake to improved long-term health outcomes and better digestive function, propelling demand across all segments.

AI significantly enhances production efficiency by optimizing supply chain logistics and improving quality control. Machine learning algorithms predict grain yield variability and contaminant risks, while personalized nutrition platforms guide R&D to formulate high-fiber products that meet specific consumer dietary needs, reducing waste and increasing product efficacy.

The high-fiber snack and nutritional bar category is experiencing the fastest rate of innovation. This segment focuses on convenience, sensory appeal, and the integration of novel ingredients like ancient grains (e.g., teff, quinoa) and specialized prebiotics, directly targeting younger, health-conscious consumers who require on-the-go functional foods.

The primary restraints include the relatively higher cost of certified whole grain ingredients compared to refined flours and the sensory challenges associated with high-fiber content, such as perceived bitterness or gritty texture. Manufacturers must invest heavily in flavor masking technologies and advanced processing to overcome these barriers effectively.

The Asia Pacific (APAC) region, specifically emerging economies like China and India, presents the most significant future opportunity. This growth is driven by rising disposable incomes, shifting dietary habits towards Western-style convenience foods, and growing awareness of preventative health, leading to substantial untapped consumer demand for nutrient-dense whole grain options.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.