ID : MRU_ 431706 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

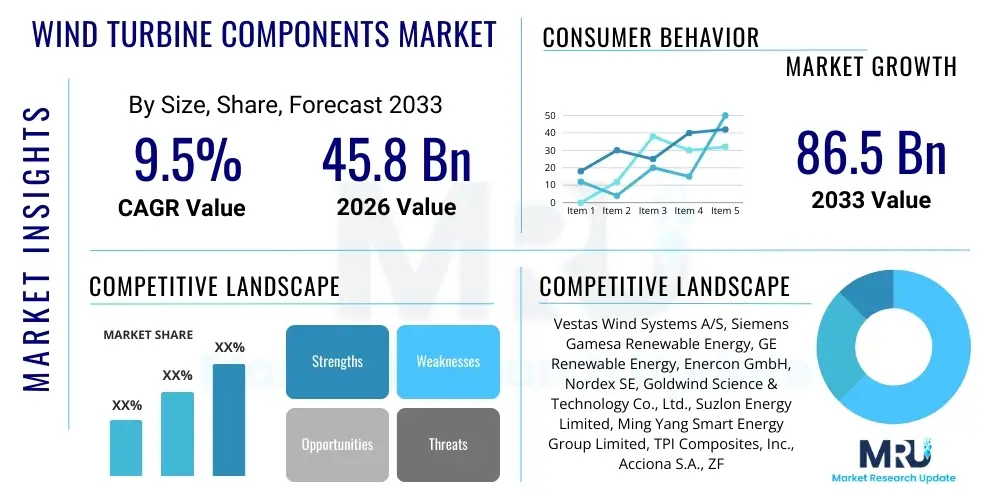

The Wind Turbine Components Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at USD 45.8 Billion in 2026 and is projected to reach USD 86.5 Billion by the end of the forecast period in 2033.

The Wind Turbine Components Market encompasses the manufacturing, distribution, and servicing of the essential elements that constitute a functional wind energy generation system. These components are critical for converting kinetic energy from the wind into electrical power, ranging from massive rotor blades that capture the energy, to the sophisticated nacelles housing the mechanical and electrical systems, and the robust towers that support the structure. The core product categories include blades, gearboxes, generators, towers, hubs, pitch systems, and yaw drives, all designed to maximize energy capture, ensure operational longevity, and withstand extreme environmental conditions.

Major applications of wind turbine components are bifurcated into onshore and offshore wind farms. Onshore installations traditionally represent the larger share due to lower capital expenditure and easier accessibility, though the trend is shifting towards larger, high-capacity offshore projects, particularly in Europe and Asia Pacific, which necessitate specialized, durable components capable of resisting corrosive marine environments and intense structural loads. The necessity for reliable energy sources and the global pivot towards decarbonization are primary drivers propelling the demand across both application segments. The continuous pursuit of higher capacity factors and reduced levelized cost of energy (LCOE) mandates innovation in component design, particularly focusing on lightweight, high-strength materials like advanced composites and carbon fiber.

The benefits associated with robust wind turbine components include enhanced energy production efficiency, extended operational lifespan, reduced maintenance cycles, and improved grid stability integration. Driving factors include supportive governmental policies such as production tax credits and renewable portfolio standards, significant cost reductions in wind energy technology over the past decade, and the urgent global requirement to mitigate climate change effects. Furthermore, technological advancements, such as the development of direct-drive generators and increasingly long blades (exceeding 100 meters), are continuously expanding the potential geographical scope and economic viability of wind power projects globally, reinforcing the market’s positive trajectory.

The global Wind Turbine Components Market exhibits robust growth, primarily driven by aggressive national renewable energy targets and substantial investment in large-scale offshore projects. Key business trends indicate a shift towards modular component design, facilitating easier transportation and installation, alongside heightened consolidation among major original equipment manufacturers (OEMs) seeking greater supply chain control and technological integration. Furthermore, there is a pronounced focus on digitalization and predictive maintenance solutions (Condition Monitoring Systems - CMS) integrated directly into components to minimize downtime and optimize energy yield, demonstrating a clear movement towards smart wind farm operations and servicing.

Regionally, the market is dominated by the Asia Pacific (APAC), led by China's massive installation capacity and ambitious long-term renewable energy commitments. Europe remains a critical hub, specifically for offshore wind technology innovation, driving demand for specialized, high-durability components such as corrosion-resistant towers and advanced pitch systems. North America is characterized by high demand for repowering older fleets and expanding capacity in land-constrained areas, necessitating highly efficient, next-generation components. These regional dynamics create varied demands for material science and manufacturing scale, influencing global component pricing and supply chain logistics significantly.

Segment trends reveal that the Blades segment, particularly those utilizing carbon fiber and advanced composite structures, is experiencing the fastest growth due to the pursuit of higher swept areas for increased power capture. The Generator segment is witnessing rapid adoption of permanent magnet synchronous generators (PMSGs) over doubly fed induction generators (DFIGs), especially in large offshore turbines, offering improved reliability and reduced need for complex gearboxes. This technological evolution across core components is leading to increased specialization among Tier 1 and Tier 2 suppliers, focusing on enhancing material durability and integration capabilities to support the ever-increasing size and complexity of modern wind turbines.

User inquiries regarding the impact of Artificial Intelligence (AI) in the Wind Turbine Components Market primarily revolve around operational efficiency, maintenance predictability, and design optimization. Common questions concern how AI can extend component lifespan, reduce catastrophic failures, and streamline complex manufacturing processes. Users are keenly interested in predictive maintenance models trained on vast datasets of vibration, temperature, and performance metrics collected via integrated sensors (IoT), aiming to predict component failure (especially in gearboxes and bearings) long before they occur, thus optimizing scheduled servicing. Furthermore, there is strong interest in using AI algorithms for load and fatigue analysis during the design phase of large components like blades, enabling engineers to create lighter yet stronger structures, ultimately reducing material costs and improving aerodynamic performance. This emphasis on enhancing reliability and efficiency through data-driven insights positions AI as a transformative tool across the entire component lifecycle.

The market is primarily driven by global governmental mandates favoring renewable energy adoption and the continuous decline in the LCOE of wind power, making it increasingly competitive against traditional fossil fuels. Restraints include significant supply chain bottlenecks, volatility in raw material prices (especially steel and rare earth minerals for generators), and the substantial upfront capital investment required for large-scale offshore infrastructure. Opportunities lie predominantly in repowering aging fleets in mature markets, the emergence of floating offshore wind technology opening up deeper water areas, and advancements in component recycling technologies addressing end-of-life concerns. These factors collectively determine market buoyancy and strategic investment decisions.

Key drivers include escalating energy demand in developing nations, coupled with stringent environmental regulations implemented globally to meet net-zero emissions goals. The increasing average size and capacity of newly installed wind turbines necessitate corresponding advancements in components, demanding stronger materials, larger bearing systems, and more robust electrical infrastructure. Technological leaps in component reliability, reducing the frequency and cost of maintenance activities, further enhance the economic viability of wind projects, acting as a crucial sustained driver for market expansion across all major geographical regions.

However, the market faces structural constraints related to logistics and infrastructure. Transporting massive components, such as blades exceeding 80 meters or oversized nacelles, presents significant logistical challenges requiring specialized transport vehicles and substantial route planning, particularly for onshore projects. Additionally, the limited number of specialized port infrastructure capable of handling the colossal components required for modern offshore wind installations acts as a bottleneck. These restraints, alongside geopolitical instability affecting key manufacturing hubs, exert continuous pressure on the lead times and overall cost structure of wind turbine components, demanding innovative solutions in modularity and localized production.

The Wind Turbine Components Market is segmented primarily based on the Type of component, the Application (Onshore or Offshore), and the Material utilized in manufacturing. This segmentation provides a granular understanding of demand drivers and technological focus areas within the industry. The Type segment is critical, as components like blades and gearboxes are high-value elements that dictate overall turbine performance and capital cost. Market dynamics differ significantly between the high-volume, cost-sensitive onshore sector and the high-specification, durability-focused offshore sector, necessitating distinct supply chains and material specifications across applications.

Further analysis of the segmentation reveals that the market for structural materials is evolving rapidly, moving away from conventional steel towards advanced composites and hybrid materials, particularly in high-stress components like towers and blades, to reduce weight while maintaining or increasing strength. This shift is crucial for realizing the economic benefits of larger turbines. Geographically, regional segments reflect varying levels of maturity; mature markets focus on replacements and upgrades, while emerging markets prioritize new installations, affecting the demand mix between standard and customized component specifications.

The value chain of the Wind Turbine Components Market begins with the upstream segment, which involves the sourcing and processing of critical raw materials, including steel, fiberglass, resins, carbon fiber, copper, and rare earth elements (like Neodymium) essential for permanent magnets in generators. Key upstream activities involve material extraction, advanced composite manufacturing, and precision forging and casting. Suppliers in this segment, such as chemical companies and steel producers, dictate the initial cost and quality profile of the final components. Stability and transparency in the upstream supply chain are paramount, given the increasing geopolitical risks associated with certain critical materials.

The midstream stage focuses on the manufacturing and assembly of the complex components themselves, carried out by specialized component manufacturers (Tier 1 and Tier 2 suppliers) and integrated Original Equipment Manufacturers (OEMs) like Vestas or Siemens Gamesa. This stage involves sophisticated processes such as large-scale blade molding, complex gearbox assembly, and the fabrication of massive steel towers. Distribution channels are highly complex, often involving direct sales contracts between component suppliers and OEMs or project developers. Due to the size and weight of many components, logistics and specialized transport (direct) play a critical role, often requiring localized manufacturing facilities or strategic port proximity to minimize transport costs and risks.

The downstream segment includes project development, installation, operations, and maintenance (O&M), and eventual repowering or decommissioning. End-users (potential customers) are typically utility companies, independent power producers (IPPs), and corporate energy buyers. Indirect distribution channels primarily involve service providers, consultants, and financiers who facilitate the procurement and integration of components into complete wind farms. The efficiency and longevity of the components directly impact the profitability and operational success in the downstream sector, linking component quality directly to long-term project viability and subsequent demand for replacement parts and upgrades over the turbine’s 20-30 year lifespan.

Potential customers and primary buyers in the Wind Turbine Components Market are primarily large-scale energy producers and developers responsible for constructing and operating wind farms globally. These entities include major utility companies that integrate wind power into their generation mix to meet regulatory mandates and customer demand for clean energy. Their procurement strategies are highly focused on component reliability, long-term warranty provisions, and standardized maintenance requirements, as system failure translates directly into significant revenue loss and increased operational expenditure.

Independent Power Producers (IPPs) represent another critical customer segment. IPPs typically develop, own, and operate power generation facilities, often selling electricity under long-term power purchase agreements (PPAs). For IPPs, component purchasing decisions are heavily influenced by the levelized cost of energy (LCOE) projections, leading them to favor cutting-edge components that offer the highest possible energy yield and lowest lifetime operational costs. They often engage directly with OEMs but exert significant influence over the selection of sub-components to ensure project financing milestones are met.

Furthermore, specialized segments such as corporate energy buyers (e.g., large tech companies seeking to source 100% renewable power) are increasingly acting as direct or indirect customers by commissioning bespoke wind projects. Additionally, maintenance and repair organizations (MROs) and repowering specialists constitute a growing customer base for replacement and upgraded components. These buyers require specialized inventory, focusing on components compatible with various turbine models, emphasizing the after-sales market importance for component manufacturers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 45.8 Billion |

| Market Forecast in 2033 | USD 86.5 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Vestas Wind Systems A/S, Siemens Gamesa Renewable Energy, GE Renewable Energy, Enercon GmbH, Nordex SE, Goldwind Science & Technology Co., Ltd., Suzlon Energy Limited, Ming Yang Smart Energy Group Limited, TPI Composites, Inc., Acciona S.A., ZF Wind Power, Xinjiang Goldwind Science & Technology Co., Ltd., CSIC Haizhuang Windpower Co., Ltd., United Power, ENVISION Group, Hexcel Corporation, Toray Industries, Inc., DNV GL, SGS SA, SKF Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Wind Turbine Components Market is characterized by a relentless drive towards maximizing efficiency, durability, and scalability, primarily in response to the massive requirements of offshore wind farms. A key area of innovation is in rotor blade technology, specifically the integration of advanced composites like carbon fiber spars and structural elements. These materials allow for the production of extremely long blades (often exceeding 100 meters) without prohibitive increases in weight, thereby enabling higher energy capture and increased turbine ratings. Furthermore, segmented or modular blade designs are emerging to overcome logistical bottlenecks associated with transporting ultra-large components, facilitating deployment in previously inaccessible locations.

In the field of power conversion and transmission, the technology shift is palpable. There is a marked transition from traditional geared drivetrains utilizing Doubly Fed Induction Generators (DFIGs) towards direct-drive systems employing Permanent Magnet Synchronous Generators (PMSGs). Direct-drive systems eliminate the complex, high-maintenance gearbox, significantly boosting reliability, particularly in harsh offshore environments where scheduled maintenance is costly and weather-dependent. While PMSGs require rare earth elements, the operational benefits—including better low-wind performance and simplified O&M—often outweigh the material cost considerations, driving widespread adoption in next-generation high-capacity turbines (8 MW and above).

Another crucial technological focus involves smart components integrating advanced monitoring and control systems. Pitch and yaw systems now employ highly sophisticated sensory arrays and computational fluid dynamics (CFD) modeling capabilities to adjust blade angles and nacelle orientation dynamically and instantaneously, optimizing power output and minimizing damaging structural loads, especially during turbulent weather events. Furthermore, non-destructive testing (NDT) technologies, including ultrasonic and thermal imaging inspection tools, are becoming standard for quality assurance in high-stress components like rotor shafts and main bearings, ensuring structural integrity throughout the component lifespan and proactively preventing costly failures, enhancing the overall resilience of the wind energy infrastructure.

The primary driver is the declining Levelized Cost of Energy (LCOE) for wind power, which makes it economically competitive with conventional power sources, coupled with aggressive global governmental policies and renewable energy targets stimulating rapid new installation capacity, particularly in offshore wind projects requiring specialized, high-capacity components.

The Rotor Blades segment is projected to show the highest growth, driven by the increasing size of new turbines, necessitating advanced materials like carbon fiber for manufacturing ultra-long blades (80+ meters) that maximize the swept area and enhance energy capture efficiency across large-scale projects.

The adoption of Permanent Magnet Synchronous Generators (PMSGs) and direct-drive technology is reducing reliance on traditional gearboxes, thereby decreasing the complexity and maintenance requirements of the drivetrain. This shift is particularly pronounced in the offshore sector due to the high costs associated with remote maintenance activities.

Logistical constraints, specifically the challenge of transporting increasingly massive and oversized components (blades, nacelles, tower sections) from manufacturing facilities to remote project sites, significantly impacts project timelines and costs, requiring localized manufacturing or substantial infrastructure investment.

The Asia Pacific (APAC) region currently holds the largest market share, predominantly led by China's extensive manufacturing capabilities and massive domestic wind energy installation volume, encompassing both onshore and rapidly expanding offshore projects.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.