ID : MRU_ 432328 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

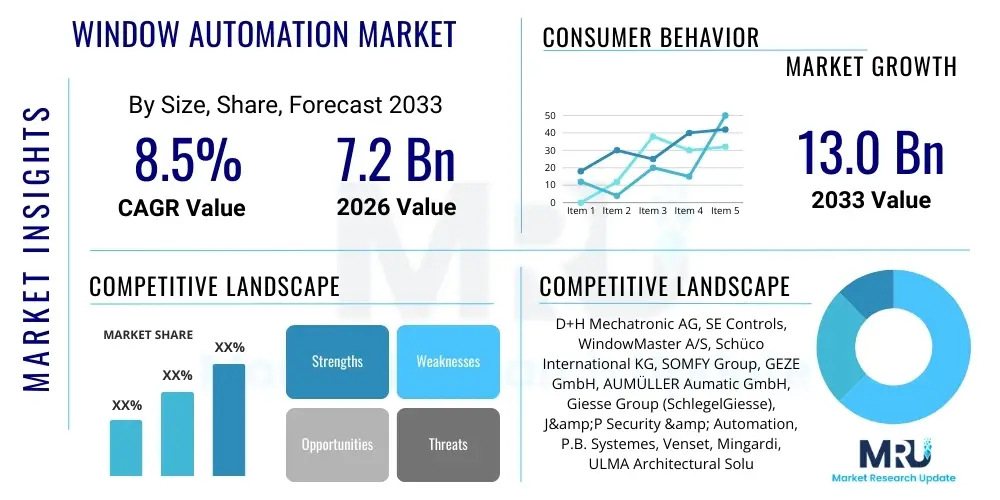

The Window Automation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 7.2 Billion in 2026 and is projected to reach USD 13.0 Billion by the end of the forecast period in 2033.

The Window Automation Market encompasses the design, manufacture, and deployment of motorized systems and control interfaces used to automatically open, close, and adjust windows, skylights, louvers, and facade elements. These systems integrate mechanical components such as actuators (chain, spindle, rack and pinion), sensors (rain, wind, temperature, CO2), and advanced control units, often connected via wired or wireless networks, forming integral parts of Building Management Systems (BMS) and smart home ecosystems. The fundamental value proposition of window automation lies in optimizing building performance concerning energy efficiency, occupant comfort, natural ventilation, and safety, particularly in smoke and heat extraction scenarios.

Products within this market range from simple remote-controlled systems for hard-to-reach windows to highly complex, integrated environmental control solutions driven by artificial intelligence and IoT platforms. Major applications span across diverse sectors, including high-end residential complexes seeking enhanced comfort and security, expansive commercial structures requiring precise climate control and compliance with green building standards, and industrial facilities where controlled ventilation is crucial for operational safety and air quality management. The increasing global focus on sustainable construction practices and the stringent enforcement of building codes related to emergency ventilation and egress are fundamentally driving the adoption rates across mature and developing economies.

The primary benefits realized through automated window systems include significant reductions in heating, ventilation, and air conditioning (HVAC) energy consumption by leveraging natural ventilation (stack effect cooling) and modulating solar heat gain dynamically. Furthermore, these systems enhance indoor air quality (IAQ) by intelligently purging stale air or excess carbon dioxide, thereby improving occupant productivity and well-being. Driving factors for market expansion include the proliferation of smart building technology, rising consumer demand for sophisticated home automation features, rapid urbanization leading to dense residential and commercial constructions, and technological advancements in brushless DC motors and miniature sensing technologies, enabling more discreet and efficient installations.

The Window Automation Market is experiencing robust growth fueled primarily by mandatory energy efficiency regulations and the accelerating integration of IoT and AI into commercial and residential infrastructure. Key business trends indicate a shift towards unified, platform-agnostic control systems that allow seamless integration with existing building infrastructure, prioritizing interoperability and cybersecurity. Manufacturers are increasingly focusing on modular design and wireless communication protocols to reduce installation complexity and costs, making automation accessible to a broader range of construction projects, including retrofits. Strategic alliances between actuator manufacturers and Building Management System providers are defining the competitive landscape, pushing innovation in predictive maintenance and enhanced user interfaces.

Regional trends highlight that Europe maintains market dominance due to early adoption driven by comprehensive environmental and safety standards, particularly concerning mandatory natural smoke and heat exhaust ventilation systems (SHEV). North America exhibits rapid expansion, primarily propelled by the burgeoning smart home market and significant investment in sustainable commercial real estate development aimed at LEED certification. The Asia Pacific region, characterized by rapid urbanization, high population density, and significant infrastructural spending in countries like China and India, is poised to demonstrate the highest Compound Annual Growth Rate, driven by demand for energy-efficient solutions in massive new building construction projects.

Segmentation trends reveal that the Control Systems segment, particularly wireless and cloud-based controls, is capturing a disproportionately high share of the market value, emphasizing the shift from mechanical components to sophisticated software and connectivity solutions. Within application segments, the commercial sector remains the largest revenue generator, demanding robust, high-cycle durability and sophisticated networked control for complex façade management. However, the residential segment is showing the fastest growth trajectory, largely attributed to increasing affordability and accessibility of DIY (Do-It-Yourself) and professionally installed smart window kits that leverage standardized protocols like Z-Wave and Zigbee, integrating automated windows into the broader smart home ecosystem for enhanced convenience, security, and climate control.

User inquiries regarding AI's impact on Window Automation predominantly center on "How AI enhances energy savings," "The role of predictive analytics in maintenance," and "If AI-driven windows truly improve occupant comfort." There is significant user expectation that AI should move automated systems beyond simple reactive adjustments (e.g., closing when it rains) to highly sophisticated predictive and proactive management. Key concerns often revolve around data privacy when utilizing cloud-based AI algorithms and the complexity of integrating these advanced systems into legacy Building Management Systems (BMS). Users expect AI to optimize ventilation schedules based not just on external weather but also on internal factors like CO2 concentration, occupancy patterns, and thermal mass inertia, ultimately delivering a seamless, invisible layer of climate control.

AI's influence is fundamentally transforming the window automation market from a mechanistic function to an intelligent, adaptive environmental response system. By processing vast amounts of real-time data from internal sensors (occupancy, temperature, air quality) and external data streams (weather forecasts, solar radiation indices), AI algorithms can determine the optimal precise degree and duration for window adjustments. This predictive capability minimizes energy wastage associated with unnecessary heating or cooling by accurately anticipating changes in environmental conditions, thereby maximizing reliance on passive strategies like natural light harvesting and cross-ventilation before mechanical systems are activated. The deployment of machine learning is enhancing system reliability by detecting anomalies and predicting mechanical failures in actuators, significantly reducing downtime and maintenance costs.

Furthermore, AI facilitates superior personalization and responsiveness crucial for occupant satisfaction in smart buildings. Instead of fixed operational schedules, AI models learn individual user preferences and seasonal behavioral patterns, adjusting window positioning to optimize daylight penetration, minimize glare, and maintain specific microclimates within different zones of a building. This shift towards personalized climate zones, managed autonomously by AI, positions automated windows as a core element of truly intelligent, human-centric buildings. This advanced functionality is paving the way for certified 'wellness' buildings, where IAQ and thermal comfort are dynamically managed through proactive façade control rather than merely reactive system overrides.

The dynamics of the Window Automation Market are heavily influenced by a confluence of structural drivers and persistent restraints, creating powerful impact forces that shape market trajectory. The dominant drivers include the global push for green building certifications (such as LEED and BREEAM), which necessitate dynamic façade management for optimal energy performance, and the rapid expansion of the Internet of Things (IoT) infrastructure, which allows for robust, scalable networked control systems. These drivers create a compelling economic and regulatory necessity for automation, pushing building developers towards integrated solutions. Conversely, significant restraints include the high initial capital investment required for comprehensive automated systems compared to traditional manual windows, the perceived complexity of installation and commissioning, and the lack of standardization across different communication protocols (a lingering barrier to seamless integration). These forces result in a high-impact environment where technological innovation in cost reduction and standardization represents the key to unlocking broader market potential.

Opportunities within the market primarily lie in the retrofitting of existing commercial building stock, which constitutes a vast, untapped market demanding energy-efficient upgrades without requiring full structural overhauls. The development of wireless, battery-powered actuator technologies is addressing the installation complexity restraint, enabling easier integration into older structures. Another major opportunity exists in the development of specialized, low-power sensor arrays designed for specific regional requirements, such as high-wind resistance automation in coastal areas or enhanced fire safety compliance in dense urban settings. Furthermore, the convergence of window automation with renewable energy solutions, such as solar-powered actuators, provides a niche for sustainable product differentiation.

The impact forces exerted on the market are highly concentrated in regulatory enforcement and technological maturity. Regulatory mandates regarding natural smoke ventilation and energy performance standards compel the commercial sector to adopt complex automation systems, acting as a powerful, non-negotiable pull factor. Simultaneously, the maturity of IoT platforms and the increasing affordability of microcontrollers and motor components are lowering the technological barrier to entry, fostering competition and accelerating product development cycles, particularly in wireless communication and enhanced sensing capabilities. The market demonstrates a moderate bargaining power among buyers, especially in the commercial sector, where large procurement contracts incentivize customization and competitive pricing among vendors, while the threat of new entrants remains moderate due to the necessity of specialized engineering expertise and high reliability standards required for building components.

The Window Automation Market is systematically analyzed based on product type, application (end-user), technology, and operation type to accurately gauge demand patterns and identify high-growth sub-markets. This granular segmentation provides stakeholders with targeted insights into technological preferences and regional adoption rates. The Product Type segmentation distinguishes between the mechanical components (actuators and mechanisms) and the intelligence layer (control systems and sensors), highlighting the growing market value contribution of sophisticated control interfaces and IoT integration. Analyzing the market through the lens of Application clearly delineates the differing reliability, cycle life, and complexity requirements between the residential, commercial, and industrial sectors, revealing the commercial segment's dominance due to regulatory mandates and scale requirements.

Further analysis by Technology emphasizes the ongoing transition towards smart, interconnected solutions, focusing on the rapid uptake of wireless protocols and AI-driven cloud-based systems over traditional wired solutions. This segmentation is crucial for understanding R&D investment trends. The Operation Type segmentation clarifies market preference regarding the degree of automation, differentiating between fully automated systems (BMS-integrated, weather-responsive) and simpler semi-automated systems (remote control operation with manual override). Each segmentation criterion underscores the market's evolution from simple mechanization to complex, integrated building intelligence, confirming the prioritization of connectivity, efficiency, and seamless user experience as primary differentiating factors across all segments and geographical regions.

The value chain for the Window Automation Market commences with upstream analysis, focusing on the sourcing and manufacturing of critical raw materials and specialized components. This stage involves the procurement of highly durable plastics, specialized metals (aluminum, stainless steel), and, most critically, high-precision electric motors and microcontrollers necessary for actuator function and control unit intelligence. Key upstream suppliers include manufacturers of permanent magnet DC motors, embedded systems, and sophisticated sensor technology, where quality control and miniaturization capabilities are paramount. Stability and cost effectiveness in the supply of these specialized electronic and mechanical components directly influence the final product price and reliability, creating significant upstream dependency for major automation system providers.

The midstream section of the value chain is characterized by the manufacturing, assembly, and integration processes. This involves the specialized engineering required to convert raw components into robust actuators, control units, and customized façade solutions. Integration complexity is high, as manufacturers must ensure compatibility between mechanical components, electronic controls, and various communication protocols. Manufacturers often specialize, with some focusing on high-volume standardized residential systems while others concentrate on highly customized, high-cycle commercial building façade solutions. Rigorous testing for weather resistance, durability, and compliance with specific safety standards (like EN 12101-2 for smoke ventilation) is a critical value-add at this stage.

Downstream analysis covers the distribution channels, system integration, installation, and after-market services. Distribution is bifurcated into direct sales channels, typically utilized for large commercial or institutional projects where complex integration and project management are required, and indirect channels, predominantly serving the residential and small commercial segments through distributors, wholesale electrical suppliers, and specialized smart home integrators. Professional system installers and certified integrators play a crucial role in the value delivery, ensuring correct commissioning and integration with the building's central management system (BMS). After-market services, including maintenance contracts and remote diagnostics, represent a significant and growing revenue stream, essential for maintaining the continuous operational integrity and compliance of automated window systems.

Potential customers for window automation systems are broadly categorized based on their primary motivation for adoption: energy efficiency, safety/compliance, and enhanced comfort/luxury. The largest volume buyers currently reside in the Commercial Building sector, particularly developers and owners of Class A office spaces, large retail complexes, and healthcare facilities. These end-users are driven primarily by the need to achieve stringent green building certifications (reducing operational costs) and complying with life safety regulations requiring automated smoke and heat extraction systems. Investment in automation for these customers is typically viewed as a necessity for modern building operation and long-term asset value enhancement.

Another significant customer segment is the High-End Residential Market, encompassing luxury apartment complexes, custom-built homes, and modern villas. For this segment, the primary motivators are convenience, security, and integration into comprehensive smart home ecosystems. These buyers demand aesthetically pleasing, quiet, and seamlessly integrated systems that enhance the quality of life, often including sophisticated weather-responsive functions and remote control capabilities via mobile applications. While volume is lower than the commercial sector, the value per installation is often higher due to the customization and premium components required.

Emerging but increasingly important customers include Industrial Facilities, such as large manufacturing plants and warehouses, where automation is crucial for controlling internal air quality, managing excessive heat buildup, and ensuring OSHA compliance regarding workplace ventilation. Government and Institutional Buildings, including schools and universities, are also key buyers, driven by public mandates for energy conservation and improving air quality for occupant health (e.g., CO2 monitoring in classrooms). These buyers prioritize reliability, longevity, and ease of centralized management across multiple buildings or campuses.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 7.2 Billion |

| Market Forecast in 2033 | USD 13.0 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | D+H Mechatronic AG, SE Controls, WindowMaster A/S, Schüco International KG, SOMFY Group, GEZE GmbH, AUMÜLLER Aumatic GmbH, Giesse Group (SchlegelGiesse), J&P Security & Automation, P.B. Systemes, Venset, Mingardi, ULMA Architectural Solutions, Alutec Group, FAKRO Group, Colt International, UAB Automatikos Sistemos, TiMOTION Technology, Rockwell Automation, Siemens AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Window Automation Market is rapidly evolving, driven by the shift towards connectivity and enhanced intelligence, moving away from purely mechanical systems. A cornerstone of current innovation is the deployment of robust Internet of Things (IoT) technologies, which enable centralized, real-time monitoring and control of façade elements. IoT platforms facilitate the collection of massive datasets from embedded environmental sensors, allowing the system to make adaptive, contextual decisions regarding ventilation and solar shading. The reliance on standardized wireless communication protocols like Zigbee, Z-Wave, and Bluetooth Low Energy (BLE) is mitigating the complexity and cost associated with traditional hardwired Bus systems (like KNX), making installations quicker, more flexible, and highly scalable, especially for residential and small commercial applications.

Another crucial technological development involves the continuous improvement in actuator technology, primarily focusing on increasing efficiency, reducing noise levels, and ensuring long-term durability. Brushless DC (BLDC) motors are becoming standard, offering superior torque density, longer life cycles, and quieter operation compared to older brushed motors, meeting the stringent requirements of residential and high-end commercial spaces. Parallel to this, advancements in miniaturization allow actuators to be concealed within the window frame or architectural façade, preserving aesthetic integrity, which is a major purchase criterion for architects and interior designers. Furthermore, specialized materials are being developed to improve fire resistance and thermal performance of the actuator casings, crucial for life safety applications.

The most sophisticated technological driver is the integration of cloud-based services and Artificial Intelligence (AI) for control optimization. Cloud platforms enable remote diagnostics, over-the-air firmware updates, and the centralized management of multiple buildings or sites. AI and Machine Learning (ML) algorithms utilize the sensor data to perform predictive control—for instance, learning building occupancy patterns and local climate variability to pre-adjust windows hours before an expected temperature peak or air quality dip. This level of predictive intelligence transforms the automated window from a simple closure device into a proactive climate moderator, significantly enhancing energy savings and ensuring regulatory compliance without direct human intervention, defining the next generation of smart façade management systems.

Regional dynamics play a significant role in shaping the demand for window automation, driven by varying climate conditions, regulatory environments, and construction standards. Europe currently dominates the global market, largely due to its rigorous enforcement of energy performance in buildings directives (EPBD) and mandatory standards for Natural Smoke and Heat Exhaust Ventilation Systems (SHEV), governed by EN 12101-2. Countries such as Germany, the UK, and Scandinavia are mature markets where automated windows are a prerequisite for most new commercial builds and essential for achieving high BREEAM or Passive House ratings. This regulatory framework ensures consistent, high-volume demand for reliable, compliant actuators and complex networked control systems designed for life safety applications.

North America, particularly the United States, is experiencing accelerated growth, fueled by strong consumer adoption of smart home technology and increasing governmental focus on sustainability and energy resilience in commercial real estate. While historically slower on mandatory SHEV standards compared to Europe, the adoption of automation is now being driven by architects specifying sophisticated façade systems to maximize natural light and air quality, supporting certifications like LEED and WELL Building Standard. Key growth areas include high-rise residential buildings in major metropolitan areas and the retrofit market in older commercial offices seeking substantial operational cost reductions through intelligent climate management. The competition here is intensely focused on seamless integration with established smart home ecosystems (e.g., Google Home, Amazon Alexa).

The Asia Pacific (APAC) region is projected to be the fastest-growing market globally, driven by unprecedented rates of urbanization and massive investments in infrastructure across countries like China, India, and Southeast Asia. The demand is segmented: in developed parts (Japan, South Korea), the focus is on energy efficiency and luxury residential automation; in emerging markets, demand is driven by the need for enhanced air quality control in densely polluted urban centers and large-scale industrial ventilation systems. While price sensitivity remains a factor in parts of APAC, the sheer volume of new construction projects ensures substantial market opportunity, particularly for wireless, modular systems that can be rapidly deployed in high-density residential towers and large-scale mixed-use developments.

The primary driver is regulatory compliance, specifically the need to meet stringent energy performance mandates and mandatory life safety standards such as Natural Smoke and Heat Exhaust Ventilation Systems (SHEV). Automation ensures precise climate control and rapid emergency response, essential for modern building operations.

Automated windows maximize energy efficiency by utilizing natural ventilation (stack effect) and dynamic solar shading. By intelligently opening and closing based on real-time temperature, wind, and solar load data, the systems minimize reliance on energy-intensive mechanical HVAC systems, leading to substantial energy cost savings.

The future is defined by integration of Artificial Intelligence (AI) for predictive control, leveraging IoT platforms for centralized management, and the widespread adoption of wireless communication protocols (Zigbee, Z-Wave) to enhance ease of installation and system scalability across both new builds and retrofit projects.

Yes, for large commercial and institutional buildings, the high initial cost is often justified by the long-term ROI derived from significantly reduced operational energy costs, minimized maintenance downtime due to predictive diagnostics, and enhanced building asset valuation resulting from green building certifications.

Europe holds the dominant market share, driven by its well-established, strict regulatory environment, particularly concerning mandatory safety standards (SHEV) and comprehensive directives on building energy performance (EPBD), which have standardized the requirement for sophisticated automated façade management systems.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.