ID : MRU_ 433655 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

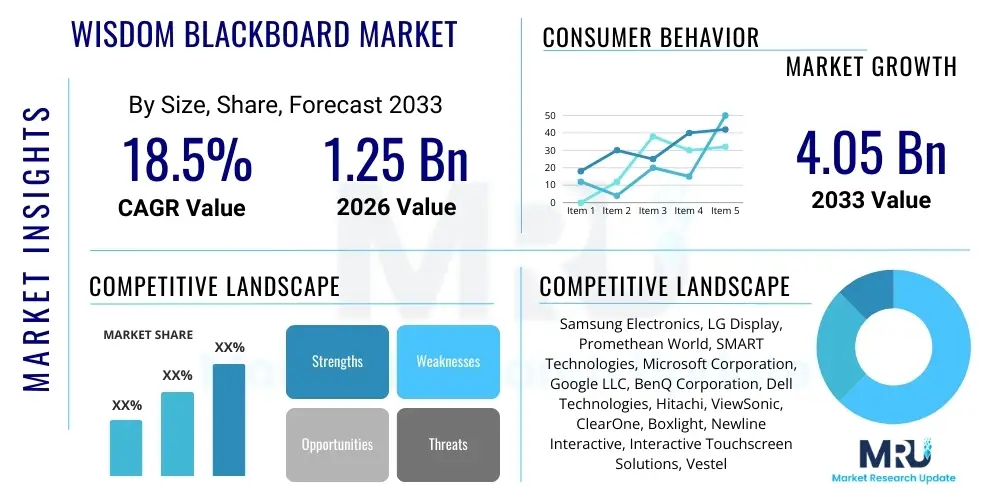

The Wisdom Blackboard Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at $1.25 Billion in 2026 and is projected to reach $4.05 Billion by the end of the forecast period in 2033. This robust expansion is primarily fueled by the accelerating integration of interactive display technologies and sophisticated learning management systems (LMS) within educational institutions globally, alongside increasing government investments aimed at digital transformation in pedagogy. The shift from traditional static blackboards to dynamic, multi-functional smart displays, often referred to as Wisdom Blackboards due to their integrated computational and adaptive capabilities, signifies a fundamental paradigm change in classroom engagement and instructional delivery, making it a high-growth sector within EdTech.

Market valuation growth is strongly correlated with technological advancements, particularly in areas like high-resolution display clarity, multi-touch capabilities, and seamless cloud connectivity. Developing nations, specifically those in the Asia Pacific and Latin American regions, are emerging as significant growth catalysts, driven by ambitious public education modernization programs. Furthermore, the rising adoption of hybrid learning models, which necessitate integrated physical and digital teaching tools, substantially enhances the demand curve for these advanced blackboard systems. The competitive landscape is characterized by continuous innovation in software ecosystems that enhance the blackboard’s utility beyond simple display, incorporating features such as real-time feedback, assessment tools, and access to vast digital content libraries, thereby solidifying its position as a central component of the modern classroom infrastructure.

The Wisdom Blackboard Market encompasses high-technology interactive display solutions designed for educational and professional training environments, moving significantly beyond conventional chalkboards or standard whiteboards. These products typically integrate large-format touchscreens, embedded computing power, network connectivity, and specialized pedagogical software, acting as a central hub for collaborative learning and digital content delivery. Major applications span K-12 education, higher education institutions, and corporate training centers, where they facilitate interactive presentations, real-time annotation, video conferencing integration, and access to cloud-based resources. Key benefits include enhanced student engagement, improved data visualization, streamlined lesson preparation for educators, and support for diverse learning styles. The market growth is fundamentally driven by the global imperative to digitize education, the increasing proliferation of Bring Your Own Device (BYOD) policies requiring central interactive displays, and robust governmental funding focused on educational technology infrastructure upgrades, ensuring the Wisdom Blackboard remains a critical investment area for modernization efforts.

Product descriptions of these systems often highlight features like 4K resolution, anti-glare coatings, low latency touch responses (supporting 20 or more simultaneous touch points), and integrated operating systems (such as Android or proprietary EdTech platforms) optimized for educational use cases. The integration of specialized software for features like optical character recognition (OCR), instant translation, and adaptive testing further defines these devices, differentiating them from general-purpose commercial displays. In higher education, their application extends to complex simulations and hybrid lecture halls, connecting remote participants with the physical classroom effectively. For corporate training, they serve as sophisticated collaboration tools for workshops and high-level strategy sessions, emphasizing interoperability and robust security protocols necessary for proprietary information handling. The continuous evolution of these features maintains the high demand trajectory for these integrated learning solutions.

The Wisdom Blackboard Market is witnessing substantial expansion, characterized by a rapid transition toward highly integrated, software-centric interactive display solutions, driven primarily by favorable business trends focused on educational digitalization and remote learning infrastructure enhancement. Key business trends include aggressive mergers and acquisitions among display manufacturers and EdTech software developers, aimed at offering bundled, comprehensive classroom solutions. Furthermore, the market structure is shifting from hardware-centric sales to subscription-based models for proprietary learning software and cloud services, ensuring recurring revenue streams and deeper integration into institutional ecosystems. This strategic pivot ensures that hardware longevity is paired with continuous software innovation, enhancing the overall value proposition of the installed base.

Regionally, the Asia Pacific (APAC) region stands out as the primary growth engine, fueled by massive public sector investments in countries like China, India, and South Korea, targeting universal digital literacy and classroom infrastructure modernization. North America and Europe, while representing mature markets, maintain high demand due to constant technological refresh cycles, focusing on sophisticated features like advanced data analytics capabilities and AI integration for adaptive learning environments. Segment trends indicate a major proliferation of cloud-connected 65-inch and 75-inch models, favored for their optimal balance between classroom size suitability and visual clarity. The K-12 segment continues to be the dominant end-user category, although corporate training and vocational education segments are demonstrating accelerated adoption rates, underscoring the versatility and applicability of the Wisdom Blackboard technology across diverse learning contexts and professional development needs.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Wisdom Blackboard Market typically revolve around how AI can transition these displays from passive presentation tools to truly intelligent, adaptive learning platforms. Users frequently ask: "How can AI personalize content delivery through the blackboard?" and "Will AI integration automate routine teaching tasks?" Other core concerns relate to data privacy, specifically, "How is student data collected and protected when the blackboard uses AI for analytics?" and expectations regarding the immediate utility, "What specific AI tools (like real-time translation or automated assessment) are ready for current classroom deployment?" These questions collectively point to a strong user expectation that AI integration must translate directly into enhanced pedagogical outcomes, reduced teacher workload, and secure, ethical data handling practices, moving the product beyond basic interactivity toward true 'wisdom' capabilities.

The impact of AI is fundamentally transformative, enabling the Wisdom Blackboard to operate as an intelligent teaching assistant rather than merely a display screen. AI algorithms can analyze student interaction patterns, annotation styles, and response times captured directly on the board interface. This behavioral data is then processed to generate real-time feedback for the teacher regarding class engagement levels and areas where students are struggling, allowing for immediate pedagogical adjustment. For instance, if multiple students struggle with a specific annotated diagram, the AI can automatically suggest supplementary resources, pull up relevant video tutorials, or adjust the complexity of the displayed material dynamically. This adaptive capacity is crucial for accommodating diverse classroom needs and ensuring personalized learning pathways, a significant market differentiator.

Furthermore, AI significantly enhances content management and accessibility. AI-powered tools integrated into the blackboard can automatically categorize, tag, and search vast libraries of educational content, making lesson preparation dramatically faster and more efficient for educators. Features such as instant voice-to-text transcription, translation services for multilingual classrooms, and automated grading of handwriting or digitally submitted assignments are becoming standard expectations. However, successful market adoption hinges on manufacturers addressing critical ethical concerns regarding bias in AI models and ensuring stringent compliance with global data privacy regulations (like GDPR and FERPA), requiring robust security frameworks embedded directly into the blackboard operating system and cloud services.

The dynamics of the Wisdom Blackboard Market are governed by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively constituting the market's Impact Forces. Key drivers include accelerating government initiatives worldwide focused on modernizing educational infrastructure, recognizing digital literacy as a national competitive advantage. Complementing this is the proven pedagogical benefit of interactive learning, which demonstrably boosts student engagement and retention rates, pushing institutional adoption. However, market expansion faces significant restraints, primarily high initial capital expenditure (CAPEX) required for deployment, especially in budget-constrained public school districts, coupled with the need for continuous, specialized training for educators to effectively leverage the sophisticated features of these systems, which remains a logistical challenge globally. Despite these hurdles, substantial opportunities exist in the expansion into niche markets like corporate skill development and vocational training, and the integration of emerging technologies like Augmented Reality (AR) and Internet of Things (IoT) sensors to create truly immersive and connected learning environments.

The primary driving force remains technological maturation, making the systems more robust, intuitive, and feature-rich. Advances in screen technology (e.g., micro-LED, improved touch sensitivity) reduce maintenance costs and improve user experience, making the investment more palatable. The shift toward cloud-based lesson storage and resource access is also a strong driver, facilitating seamless transition between classrooms and remote settings. Conversely, a major restraining impact force is the lifecycle management challenge; the rapid obsolescence cycle of consumer electronics hardware necessitates frequent and costly upgrades for educational institutions, which often operate on fixed, multi-year budgets. Moreover, resistance to change from long-tenured educators unfamiliar with advanced digital tools acts as a significant human-factor restraint, necessitating substantial investment in professional development programs by both vendors and educational authorities.

Opportunities center on strategic market penetration. Developing nations present untapped potential, especially as manufacturing efficiencies reduce hardware costs, making the technology accessible to a wider demographic. The post-pandemic sustained necessity of robust hybrid learning solutions further solidifies the market opportunity, requiring integrated systems that bridge the gap between physical and virtual instruction seamlessly. Impact forces such as competitive intensity are high, pushing companies toward product differentiation through proprietary software ecosystems rather than just hardware specifications. Government subsidies and procurement mandates, particularly in large centralized education systems, act as powerful accelerators, dictating rapid regional market growth and setting de facto technical standards for new deployments over the forecast period.

The Wisdom Blackboard Market is highly diversified, segmented primarily based on screen size, end-user type, component type, and deployment model, reflecting the varied needs across the educational and professional spectrum. Analyzing these segments provides crucial insight into consumer spending patterns and technological preferences. The screen size segment remains the most crucial differentiator, with displays ranging from 55-inch models suitable for small group collaboration rooms to expansive 86-inch or larger units designed for large lecture halls and auditoriums. Component-wise, the market is split between hardware (the display and embedded PC module) and software/services (operating system, proprietary learning apps, and cloud services), with the latter segment increasingly dominating value creation and driving long-term revenue growth through subscription models. The proliferation of various screen resolutions and touch technologies also creates sub-segments within the hardware category, addressing specific requirements for graphic intensity or precision in annotation.

The end-user segmentation clearly indicates K-12 institutions as the historical and current revenue mainstay, driven by large volume procurement cycles and universal classroom installation mandates. However, the higher education segment is showing faster growth due to the need for advanced features supporting research, distance learning integration, and complex simulation visualization, demanding higher-specification processors and sophisticated integration capabilities with campus IT infrastructure. Deployment model analysis reveals a gradual shift from purely on-premise solutions towards hybrid and cloud-managed systems. Cloud deployment offers scalability, centralized management of devices across multiple campuses, and easy software updates, which are vital for maintaining technological parity and ensuring system reliability across large educational networks, ultimately reducing total cost of ownership (TCO) for institutional buyers who prefer operational expenditure (OPEX) models.

The Value Chain for the Wisdom Blackboard Market begins with upstream activities, centered around the sourcing and manufacturing of critical high-technology components, primarily large-format display panels (LCD/LED/OLED), touch sensors, and specialized high-performance embedded processors. Key upstream players include panel manufacturers (often based in Asia) and semiconductor suppliers. Efficiency and cost optimization at this stage are critical, as the display panel cost represents the largest single element of the final product price. Integration activities involve system assemblers and original equipment manufacturers (OEMs) who combine these raw components with proprietary chassis designs, power management units, and integrated audio systems, ensuring compliance with strict educational safety and durability standards. Technological partnerships between display makers and software developers are increasingly common upstream to ensure hardware-software optimization from the initial design phase.

The midstream focuses on the software development, which adds the primary intellectual value to the product. This includes creating the customized operating system interface, developing specific educational applications (e.g., collaborative annotation tools, assessment engines), and establishing secure cloud infrastructure for content storage and device management. Effective distribution is a downstream activity predominantly reliant on specialized EdTech distributors and system integrators who possess the necessary expertise to handle large-scale institutional installations, network configuration, and ongoing technical support. These integrators play a vital role in providing end-to-end solutions, including classroom connectivity and professional development training for teachers, moving beyond simple box sales.

Distribution channels are categorized into direct and indirect models. Direct sales are often utilized for large, high-value contracts with major university systems or national government tenders, allowing manufacturers to maintain tight control over pricing and customized solution delivery. Conversely, the vast majority of K-12 sales and smaller institutional purchases are executed through an indirect network of certified value-added resellers (VARs) and local EdTech channel partners. These indirect channels provide necessary geographic coverage, localized technical support, and essential financing options tailored to educational procurement cycles. The profitability throughout the chain is increasingly shifting towards the services and software end, emphasizing recurring revenue from cloud subscription models rather than relying solely on the single transaction profit derived from hardware manufacturing and initial distribution.

The primary potential customers and end-users of Wisdom Blackboard technology are institutions dedicated to organized instruction and skill transfer, spanning academic, vocational, and corporate domains. K-12 school districts represent the largest volume segment, driven by governmental mandates to equip every classroom with interactive technology capable of supporting curriculum delivery, centralized testing, and collaborative project work. These buyers prioritize ease of use, durability, standardized fleet management features, and robust integration with existing Student Information Systems (SIS). Purchasing decisions in K-12 often involve lengthy procurement processes managed by district technology officers, balancing pedagogical requirements with strict budgetary constraints and long-term maintenance costs, favoring vendors who offer comprehensive support packages and strong professional development programs for their teaching staff.

Higher education institutions, including large research universities and community colleges, constitute another critical customer base. Their purchasing drivers differ, focusing on advanced features necessary for hybrid lecture delivery, complex data visualization for specialized courses (e.g., engineering, medicine), and seamless integration with high-end conferencing solutions. University administrators prioritize sophisticated network security, high processing power to handle demanding software applications, and interoperability across diverse operating systems and personal devices used by both faculty and students. This segment often seeks custom software solutions and integration services, necessitating a close vendor-institution partnership for successful deployment and sustained utilization within a complex technological ecosystem.

Furthermore, the rapidly expanding corporate training and vocational sectors represent a high-growth opportunity. Potential customers here include large multinational corporations requiring centralized, standardized platforms for employee onboarding, skill refreshment, and remote global team collaboration. Unlike academic buyers, corporate end-users emphasize ROI metrics, rapid deployment capabilities, advanced security features for proprietary information sharing, and specialized software tailored for business use cases like design review and agile project management. This segment values systems that promote dynamic, actionable decision-making during workshops, often favoring features like integrated whiteboarding software that links directly to project management tools, ensuring the Wisdom Blackboard serves not just as a teaching tool but as a crucial business asset for productivity enhancement.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.25 Billion |

| Market Forecast in 2033 | $4.05 Billion |

| Growth Rate | CAGR 18.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Samsung Electronics, LG Display, Promethean World, SMART Technologies, Microsoft Corporation, Google LLC, BenQ Corporation, Dell Technologies, Hitachi, ViewSonic, ClearOne, Boxlight, Newline Interactive, Interactive Touchscreen Solutions, Vestel, Sharp Corporation, Panasonic Corporation, Horizon Education, Jupiter Systems, Genee World |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Wisdom Blackboard Market is characterized by the convergence of advanced display manufacturing, specialized pedagogical software development, and robust cloud infrastructure. Core technologies revolve around high-definition display panels, primarily based on LCD and LED technologies, increasingly moving towards 4K resolution standards to ensure clarity in large classroom settings. Crucially, the integration of ultra-responsive multi-touch technology, utilizing projected capacitive (PCAP) or infrared (IR) sensor arrays, allows for simultaneous input from multiple users with minimal latency, mimicking the natural feel of writing. The embedded computing unit, often running optimized Android or Windows operating systems, is essential for enabling standalone functionality without external PC reliance, facilitating quick boot times and seamless access to integrated learning applications, which is a major technological expectation in modern classrooms.

Software innovations represent the most significant area of differentiation. Key technologies include proprietary interactive whiteboarding applications (IWB software) that offer advanced annotation tools, geometry recognition, and content sharing protocols (e.g., Miracast, AirPlay for wireless device mirroring). Furthermore, cloud computing infrastructure (SaaS model) is foundational, enabling features like centralized management dashboards for IT administrators, secure cloud storage for student and teacher work, and facilitating over-the-air firmware and software updates across a fleet of devices. This cloud reliance ensures data security and scalability, moving the focus from hardware purchase to ecosystem management, thereby improving the operational efficiency of large educational networks and providing continuity across physical and remote learning environments.

Emerging technologies actively shaping the market include the incorporation of AI and Machine Learning (ML) for features such as adaptive testing, real-time handwriting recognition, and behavioral analytics. Furthermore, advancements in specialized peripherals, such as integrated high-quality cameras and beamforming microphones, are essential for enhancing the distance learning experience and facilitating high-quality virtual instruction directly through the blackboard. The adoption of IoT protocols allows the blackboard to seamlessly interact with other classroom devices, such as lighting systems, student tablets, and environmental sensors, establishing a truly connected and smart learning environment. Manufacturers are also heavily investing in incorporating enhanced cybersecurity protocols at the hardware and software level to protect sensitive educational data from increasing cyber threats, recognizing that data integrity is paramount for institutional trust and long-term viability in the EdTech sector.

Regional dynamics significantly influence the adoption and maturity level of the Wisdom Blackboard Market, reflecting varying levels of government investment, technological readiness, and population density across the globe. North America, driven primarily by the United States and Canada, represents a highly mature market characterized by frequent technology refresh cycles, high adoption rates of hybrid learning models, and significant demand for advanced integration with existing campus management systems. The emphasis in this region is less on initial installation volume and more on features such as integrated AI analytics, robust network security, and compliance with strict educational standards like FERPA. Competition is intense, forcing vendors to focus on software ecosystems and continuous service improvements to maintain market share against established local and international players.

The Asia Pacific (APAC) region is forecasted to exhibit the highest growth rate during the forecast period, making it the most critical region for future market expansion. This explosive growth is largely attributable to large-scale modernization projects spearheaded by governments in countries such as China, India, and Indonesia, which are rapidly transitioning hundreds of thousands of classrooms from traditional boards to interactive digital solutions. The sheer volume of potential deployments, often subsidized by national education budgets, makes APAC the primary focus for hardware manufacturing and supply chain expansion. While cost-sensitivity remains a factor, the long-term strategic goal of achieving universal digital literacy fuels sustained, large-scale investment, concentrating demand particularly in the mid-size (65-inch to 75-inch) segment which offers a balance of cost-effectiveness and functionality for standard classrooms.

Europe presents a strong, though segmented, market, with high disparity between Western and Eastern European countries. Western Europe (e.g., UK, Germany, France) demonstrates high quality demands, prioritizing environmental sustainability in manufacturing and adherence to strict data privacy regulations (GDPR). Educational buyers here focus on open, interoperable platforms that support diverse operating systems and curricula, ensuring pedagogical flexibility. Eastern European markets are primarily driven by EU funding and structural modernization funds, resulting in large, project-based tenders focused on volume deployment and competitive pricing. Latin America and the Middle East & Africa (MEA) are emerging markets, characterized by rapid urbanization and increasing government focus on leveraging technology to bridge educational disparities, presenting substantial untapped potential. Adoption in MEA is often concentrated in high-income urban centers and private schools, but governmental investment in Gulf Cooperation Council (GCC) countries is quickly accelerating market penetration through substantial state-backed education initiatives.

The Wisdom Blackboard Market is projected to experience a robust CAGR of 18.5% between 2026 and 2033, driven by increasing investment in global educational digitalization and the necessity for advanced hybrid learning tools.

Wisdom Blackboards are integrated systems featuring embedded computing power, cloud connectivity, and specialized AI-enhanced pedagogical software, differentiating them from older IWBs which typically required an external projector and PC to function.

The Asia Pacific (APAC) region is anticipated to dominate market growth, primarily due to large-scale, state-sponsored educational modernization programs and rapid adoption rates in high-population economies like China and India.

The primary restraint is the high initial capital expenditure (CAPEX) required for purchasing and installing the hardware, coupled with the ongoing need for substantial investment in specialized professional development training for educators.

AI integration focuses on features like adaptive content delivery, real-time student engagement analytics, automated assessment, and advanced handwriting recognition, enabling the system to act as an intelligent assistant to the teacher and personalize learning experiences.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.