ID : MRU_ 439028 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

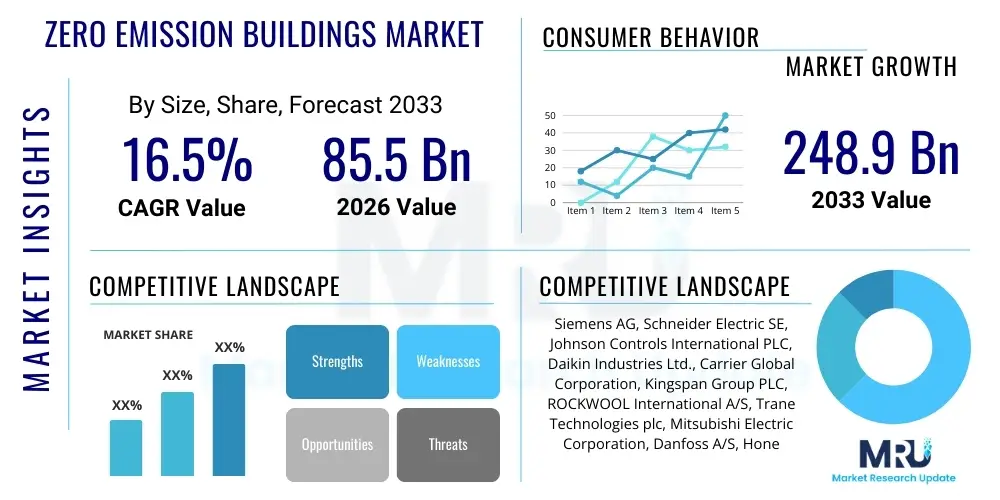

The Zero Emission Buildings Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 16.5% between 2026 and 2033. The market is estimated at USD 85.5 Billion in 2026 and is projected to reach USD 248.9 Billion by the end of the forecast period in 2033.

The Zero Emission Buildings (ZEB) Market encompasses the construction, retrofitting, and operation of structures that generate ultra-low or zero net greenhouse gas emissions over their entire lifecycle, often integrating high energy efficiency standards with on-site or off-site renewable energy generation. This approach goes beyond traditional net-zero energy concepts by considering embodied carbon from materials and construction processes, ensuring a comprehensive environmental footprint reduction. Key products facilitating this market include advanced insulation materials, high-performance windows, smart building management systems (BMS), and integrated photovoltaic (PV) and thermal solar technologies. The definition of ZEB is increasingly standardized by international bodies like the World Green Building Council, promoting holistic design practices focused on decarbonization.

Major applications of Zero Emission Buildings span both the residential and commercial sectors, including new construction projects, deep energy retrofits of existing building stock, and specialized facilities such as educational institutions and healthcare premises prioritizing sustainability. These buildings are designed to minimize heating and cooling demands through passive strategies, leading to significant reductions in operational energy consumption. The market is characterized by the complex integration of various architectural, engineering, and digital technologies, requiring specialized expertise in energy modeling and performance verification to meet stringent certification standards. The rising global urban population and the urgent need to mitigate climate change are fundamentally driving the adoption of these advanced building prototypes.

The primary benefits derived from ZEB adoption include substantial long-term operational cost savings due to minimized energy usage, improved indoor air quality and occupant comfort, and enhanced resilience against fluctuating energy prices and supply disruptions. Driving factors propelling market expansion include increasingly stringent government mandates and building codes focused on energy performance (e.g., the European Union’s Energy Performance of Buildings Directive), growing corporate commitments to Environmental, Social, and Governance (ESG) criteria, and consumer demand for sustainable and healthy living spaces. Furthermore, technological advancements in renewable energy storage and smart grid infrastructure are making ZEB implementation more feasible and economically viable across diverse climatic zones.

The Zero Emission Buildings market is experiencing robust expansion, driven primarily by favorable regulatory environments in developed economies and rapid technological maturation in energy management systems and renewable integration. Current business trends indicate a significant shift towards circular economy principles, where material selection and embodied carbon assessment are becoming integral components of ZEB project planning, moving beyond just operational energy performance. Key players are forming strategic partnerships across the construction supply chain—linking material manufacturers, architecture firms, and technology providers—to deliver integrated solutions and manage complex, multi-faceted ZEB projects efficiently. Investment is increasingly flowing into deep retrofit markets, recognizing the immense potential for decarbonization within the existing, aging building infrastructure, particularly in mature markets like Western Europe and North America.

Regionally, Europe maintains a dominant position due to ambitious, binding climate targets and strong governmental incentives for building renovation and efficiency, exemplified by national roadmaps for building stock decarbonization. North America follows closely, with state-level policies (particularly in California and the Northeast US) driving market activity, coupled with significant private sector investment in corporate sustainability portfolios. The Asia Pacific (APAC) region is poised for the highest growth trajectory, fueled by rapid urbanization, massive new construction volumes in countries like China and India, and a growing recognition among policymakers regarding the severe impact of fossil fuel dependence on air quality and energy security. The adoption rates vary, however, often depending on local grid stability and the availability of cost-effective renewable energy sources.

Segmentation trends highlight the increasing importance of the Residential segment, largely due to governmental focus on improving housing quality and reducing energy poverty, often through bulk financing mechanisms for household retrofits. Technology-wise, the Building Energy Management Systems (BEMS) and Energy Storage segments are witnessing exponential growth as sophisticated control mechanisms are crucial for maximizing the efficiency and grid interaction capabilities of ZEB. Furthermore, within the material segment, highly insulating, bio-based, and low-embodied carbon materials, such as cross-laminated timber (CLT) and recycled content insulation, are gaining substantial traction as stakeholders seek to address the full lifecycle emissions of buildings. This integrated approach ensures that the market growth is balanced across both technological innovation and sustainable material sourcing.

User inquiries regarding AI's impact on the Zero Emission Buildings market predominantly revolve around three key themes: predictive energy optimization, lifecycle carbon footprint management, and the feasibility of autonomous building operation. Users are keen to understand how AI-driven analytics can move ZEB from static efficiency to dynamic, real-time performance optimization, particularly in predicting and managing peak load demands and integrating intermittent renewable energy sources seamlessly. There are also significant concerns about the data infrastructure required, the interoperability of various smart building components, and the ethical implications of using large datasets of occupant behavior to maximize building efficiency. Users generally anticipate that AI will be the crucial enabling technology that allows ZEBs to operate reliably as interactive components of the smart grid, maximizing self-consumption and minimizing reliance on fossil fuels, thereby significantly improving the verification and reporting accuracy of their zero-emission status.

The Zero Emission Buildings market is fundamentally shaped by powerful synergistic forces: mandatory decarbonization targets (Drivers), high initial capital costs (Restraints), immense potential in renovation waves (Opportunities), and the irreversible trend towards sustainable infrastructure (Impact Forces). The growing regulatory pressure, particularly in major economic blocs, ensures sustained demand, while continuous innovation in building materials and system integration consistently addresses previous performance limitations. However, the specialized skill set required for ZEB design, construction, and commissioning remains a significant bottleneck, often limiting rapid scalability in emerging markets. The long-term economic and environmental imperatives, however, heavily outweigh these short-term constraints, setting the market on a decisive growth trajectory.

Drivers: Stricter Governmental Policies and Mandates for Deep Decarbonization. The primary driver is the global commitment to the Paris Agreement, translated into national and regional building codes demanding net-zero operational energy and, increasingly, net-zero lifecycle carbon. Financial incentives, such as green mortgages, tax credits, and public procurement mandates favoring ZEB construction, further accelerate adoption. Secondly, significant advancements in renewable energy technology, coupled with decreasing installation costs for solar PV and small-scale wind, make on-site generation economically viable, closing the gap between high efficiency and zero emissions. Finally, institutional investors and large corporations are integrating rigorous ESG reporting, prompting massive demand for green real estate assets that offer lower operational risks and align with corporate sustainability commitments.

Restraints: The most prominent restraint is the substantially higher upfront capital expenditure associated with ZEB construction, primarily due to specialized materials, advanced mechanical systems, and the necessary integration of distributed energy resources (DERs). This premium can deter cost-sensitive developers and homeowners, despite demonstrable long-term cost savings. Another critical restraint is the complexity and fragmentation of the construction supply chain; integrating passive design, active energy systems, and digital control technologies requires a high level of interdisciplinary coordination and technical proficiency, which is not uniformly available across all markets. Furthermore, the variability in performance measurement and certification standards across different jurisdictions can introduce uncertainty and potential risk for large-scale international development firms.

Opportunities: A monumental opportunity lies in the extensive deep energy retrofit market. Approximately 80% of the buildings that will exist in 2050 have already been constructed, making the decarbonization of the existing stock a massive and continuous market opportunity. Innovations in modular and prefabricated ZEB solutions offer the potential to significantly reduce construction timelines, improve quality control, and lower the cost premium associated with highly efficient construction. Furthermore, the integration of ZEBs into the emerging smart grid infrastructure presents opportunities for buildings to act as profit centers, selling stored or generated power back to the grid and accessing new revenue streams through sophisticated energy arbitrage and demand-side management services.

Impact Forces: The overarching Impact Force is Climate Mitigation Urgency; buildings account for nearly 40% of global energy-related CO2 emissions, making ZEB adoption an indispensable component of achieving global net-zero targets. Societal expectation and consumer preference are rapidly shifting towards healthier, sustainable, and high-performance buildings, compelling developers to prioritize ZEB standards to maintain market relevance and asset valuation. Economic forces, driven by the volatility of fossil fuel prices and the decreasing cost of renewables, solidify the long-term operational cost advantages of ZEBs, ensuring that investments in efficiency and generation provide superior returns compared to conventional buildings over the asset lifecycle. This combination of regulatory push, technological pull, and economic justification creates an unstoppable momentum for market transformation.

The Zero Emission Buildings market is comprehensively segmented based on the type of building asset, the operational status of the building (new construction versus retrofit), the specific system components utilized, and the materials deployed in construction. Analyzing these segments provides a clear view of where investment and regulatory attention are concentrated. The complexity of ZEB requirements necessitates a segmented approach, particularly for system integration, as performance relies equally on the physical envelope (materials) and the active energy management (systems). The dominance of the retrofitting segment in mature economies contrasts sharply with the high volume of new construction projects driving growth in rapidly urbanizing regions, influencing demand patterns for specialized components and expertise.

The ZEB value chain is highly integrated and complex, extending far beyond conventional construction processes, encompassing specialized upstream manufacturing, high-tech distribution channels, and highly specialized downstream services. Upstream analysis focuses on the sourcing and production of low-embodied carbon materials, such as bio-based composites, recycled steel, and high-performance insulation. This stage demands rigorous certification and tracking (e.g., Environmental Product Declarations - EPDs) to verify the sustainability claims critical to ZEB status. Manufacturers of advanced components, including high-efficiency heat pumps, integrated PV roofing systems, and smart sensors, play a vital role here, prioritizing interoperability and modularity to facilitate seamless integration at the construction site.

Downstream activities are dominated by specialized service providers: energy modelers, architects certified in passive house standards, ZEB commissioning agents, and technology integrators. Unlike standard construction, ZEB success hinges on the precise execution of the design and verification of performance post-occupancy. This requires ongoing monitoring and optimization services provided by BEMS and AI platform developers. The complexity inherent in balancing energy generation, storage, and consumption means that maintenance and operational phase services constitute a substantial and growing segment of the value chain, ensuring the building maintains its zero-emission target throughout its operational lifespan.

Distribution channels often bypass traditional construction supply methods for specialized components. Direct channels are prevalent for high-value, customized systems like large-scale battery storage or complex HVAC systems, involving direct sales from manufacturer to the specialized engineering firm or system integrator. Indirect channels, typically involving specialized distributors focused on sustainable building products (e.g., distributors specializing in Passive House components or certified low-VOC materials), handle standardized components like high-performance windows and advanced insulation. The increasing reliance on digital twin technology and Building Information Modeling (BIM) mandates strong collaboration and data sharing across all value chain participants, favoring firms capable of delivering integrated digital and physical solutions.

The primary customers for Zero Emission Buildings span both the public and private sectors, driven by different motivations yet converging on the need for sustainable, high-performing assets. Institutional investors and real estate investment trusts (REITs) represent a crucial customer segment, seeking to future-proof their portfolios against rising carbon taxes, regulatory obsolescence, and physical climate risks. These financial entities recognize that green-certified buildings command higher rents and valuations (the "Green Premium") and offer superior long-term stability, making ZEB adoption a core component of their fiduciary duty and risk management strategy.

Government entities at municipal, state, and federal levels are significant end-users, primarily driven by ambitious public sector mandates to lead by example in sustainability and climate action. This includes constructing new ZEB public schools, administrative offices, and affordable housing complexes, often utilizing public procurement processes to stimulate local market development for sustainable technologies. Furthermore, corporate customers, particularly those in the technology, finance, and consumer goods sectors, are increasingly demanding ZEB certification for their headquarters and data centers to meet stringent internal corporate sustainability pledges and satisfy shareholder pressure related to scope 3 emissions reduction.

Lastly, high-net-worth individuals and environmentally conscious homeowners constitute a vital segment, particularly in the residential market. These buyers are motivated by the desire for superior indoor air quality, reduced lifetime ownership costs, and personal alignment with environmental values. The growth in the residential segment is facilitated by accessible green financing options and greater public awareness regarding the long-term financial benefits of energy independence and resilience offered by fully integrated solar-plus-storage ZEB solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 85.5 Billion |

| Market Forecast in 2033 | USD 248.9 Billion |

| Growth Rate | 16.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, Schneider Electric SE, Johnson Controls International PLC, Daikin Industries Ltd., Carrier Global Corporation, Kingspan Group PLC, ROCKWOOL International A/S, Trane Technologies plc, Mitsubishi Electric Corporation, Danfoss A/S, Honeywell International Inc., ABB Ltd., Lendlease Corporation, Skanska AB, Saint-Gobain S.A., Tesla Inc., LG Electronics, SunPower Corporation, Enphase Energy, NREL (National Renewable Energy Laboratory - influencing technology). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological core of the Zero Emission Buildings market revolves around integrating high-performance passive design elements with highly efficient active systems and sophisticated digital controls. Key to passive design is the utilization of advanced thermal envelope components, including vacuum-insulated panels (VIPs) and high-density, low-lambda insulation materials that dramatically reduce heat transfer, minimizing the building's heating and cooling load. Complementing this is the pervasive adoption of triple or quadruple-pane glazing, often incorporating low-emissivity (Low-E) coatings and dynamic shading systems, which manage solar gain effectively across seasonal and daily cycles, ensuring optimal daylighting without thermal penalty. These technologies are foundational, reducing the demand side before any active systems are considered.

On the active side, highly efficient mechanical systems are standard, dominated by variable refrigerant flow (VRF) and geothermal heat pump (GHP) systems that provide heating and cooling using renewable electricity with exceptional coefficients of performance (COP). These systems replace conventional fossil fuel boilers entirely. Crucially, the integration of on-site renewable energy generation, predominantly solar photovoltaic (PV) systems, is mandatory. The technological trend here is moving toward building-integrated photovoltaics (BIPV), where solar cells are seamlessly incorporated into roofing, facades, and shading elements, maximizing architectural appeal while maintaining energy production capabilities essential for achieving the net-zero balance.

The enabling layer for all ZEB performance is the convergence of Building Energy Management Systems (BEMS) and Energy Storage Solutions (ESS). Modern BEMS leverage the Internet of Things (IoT) sensors and cloud computing, increasingly incorporating AI algorithms for predictive optimization of energy flows, coordinating HVAC operation, lighting control, and energy storage charge/discharge cycles based on real-time grid signals and predicted weather patterns. Battery ESS (typically Lithium-ion or flow batteries) provides the essential flexibility, allowing the ZEB to store excess renewable energy generated during the day and utilize it during peak evening hours or sell it back to the grid, transforming the building from a passive consumer to an active, distributed energy resource (DER). Furthermore, advanced metering infrastructure (AMI) ensures accurate, third-party verifiable tracking of the building's true zero-emission status.

While an NZEB balances annual operational energy consumption with on-site renewable generation, a ZEB adopts a more rigorous, holistic approach. A ZEB not only achieves net-zero operational energy but also considers and minimizes the embodied carbon (emissions associated with materials and construction) throughout the building's entire lifecycle, aiming for true decarbonization.

The primary constraints are the higher initial capital costs associated with specialized high-performance materials (e.g., advanced insulation and windows) and complex integrated systems (e.g., heat pumps and BEMS). Additionally, a shortage of highly skilled architects, engineers, and construction workers proficient in ZEB design and commissioning standards limits scalability.

Smart technology and AI are critical enablers. They transform static, highly efficient buildings into dynamic, performing assets. AI optimizes the Building Energy Management Systems (BEMS) in real-time, predicting energy demand and coordinating renewable generation and battery storage to maximize self-consumption, ensure grid responsiveness, and verify ongoing compliance with the zero-emission standard.

The Asia Pacific (APAC) region is projected to exhibit the highest Compound Annual Growth Rate (CAGR) due to rapid, large-scale urbanization, massive new construction volumes, and increasing governmental commitments in major economies like China and India to address severe environmental challenges and improve energy security through high-performance buildings.

Long-term financial benefits include significantly reduced operational expenses due to minimal or zero energy bills, increased asset valuation (the Green Premium), enhanced resilience against energy price volatility, and reduced risk of regulatory obsolescence (future-proofing assets against potential carbon taxes and stricter codes), making them attractive long-term investments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.