ID : MRU_ 435994 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

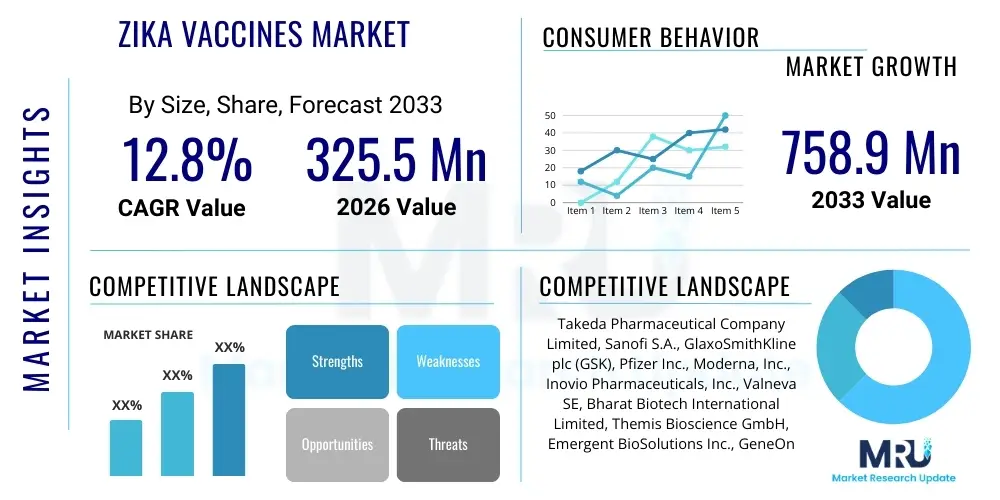

The Zika Vaccines Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2026 and 2033. The market is estimated at USD 325.5 Million in 2026 and is projected to reach USD 758.9 Million by the end of the forecast period in 2033.

The Zika Vaccines Market encompasses the development, production, and distribution of prophylactic and therapeutic agents designed to prevent or treat infection by the Zika virus (ZIKV). ZIKV, primarily transmitted by Aedes mosquitoes and occasionally sexually, gained global prominence due to its association with severe neurological disorders, particularly microcephaly in newborns and Guillain-Barré syndrome in adults. The market introduction phase has been characterized by intense research and development efforts across various technological platforms, including inactivated virus, subunit, nucleic acid (mRNA/DNA), and viral vector approaches, driven by the critical unmet need for effective preventative measures in endemic regions.

The primary applications of Zika vaccines center on mass immunization programs targeted at vulnerable populations, particularly women of childbearing age and residents of areas with active ZIKV transmission. The benefits derived from successful vaccination include the direct prevention of viremia and associated acute symptoms, but crucially, the reduction of ZIKV-related congenital syndrome (CZS) and its devastating lifelong impact on children and their families. Furthermore, widespread vaccination minimizes the risk of local outbreaks and alleviates the substantial healthcare burden placed on public health infrastructure in affected low- and middle-income countries.

Major driving factors fueling market expansion include sustained funding from international public health organizations such as the World Health Organization (WHO) and the Coalition for Epidemic Preparedness Innovations (CEPI), coupled with governmental initiatives to enhance pandemic preparedness. The increasing frequency and geographic expansion of ZIKV outbreaks, influenced by climate change, urbanization, and global travel, necessitate preemptive vaccine development. Technological advancements, particularly in rapid response platforms like mRNA technology, have significantly accelerated the pace of preclinical and clinical trials, ensuring that viable candidates can potentially reach regulatory approval within the forecast timeframe, thereby transitioning the market from a research focus to a commercialized product landscape.

The Zika Vaccines market is poised for significant growth, marked by robust business trends focusing on strategic partnerships between pharmaceutical majors, biotechnology startups, and academic institutions to share risk and expedite clinical development timelines. Key business dynamics include the transition of several promising vaccine candidates into late-stage clinical trials and the optimization of manufacturing processes to ensure scalability for global demand, especially given the sporadic nature of outbreaks requiring rapid stock mobilization. Financial investments are heavily skewed toward platforms offering high efficacy, rapid deployment, and thermostability suitable for deployment in resource-limited tropical settings, driving specialization in advanced delivery systems.

Regionally, the market dynamics are governed by disease endemicity and governmental capacity for vaccine procurement. Latin America and Southeast Asia remain critical focus areas due to historical ZIKV prevalence and the immediate necessity for preventative healthcare solutions. North America and Europe, while having lower indigenous transmission rates, play a pivotal role in research funding, clinical trial execution, and commercial production capabilities. Emerging regional trends indicate increased focus on establishing regional manufacturing hubs in Asia Pacific and Latin America to ensure equitable access and reduce reliance on centralized production, thereby stabilizing supply chains in anticipation of future epidemics.

Segment trends reveal a pronounced shift towards Nucleic Acid-Based Vaccines (DNA and mRNA) due to their inherent advantages in rapid design, manufacturing speed, and dose-sparing capabilities, making them highly responsive to epidemic threats. While traditional Inactivated and Live-Attenuated vaccines offer proven safety profiles, the agility and potential effectiveness of novel platforms are attracting the majority of R&D investment. End-user segmentation emphasizes governmental procurement and international organizational tenders as the primary revenue streams, reinforcing the public health focus of the market over conventional commercial sales channels, thus tying market success closely to global political will and public health policy implementation.

Users frequently inquire how Artificial Intelligence (AI) can accelerate the identification of optimal antigen targets and adjuvant combinations, streamline the complex and often resource-intensive processes of preclinical research, and enhance clinical trial efficiency for Zika vaccines. Key concerns revolve around the ethical deployment of AI in patient selection and the reliability of machine learning models in predicting viral evolution or outbreak severity, which directly impacts development prioritization. Expectations are high regarding AI's ability to minimize translational failure rates by identifying potential toxicity early in the drug discovery phase, allowing developers to pivot quickly and focus resources on the most viable vaccine candidates, thus fundamentally changing the traditional linear development pipeline into a more agile, data-driven approach.

The application of advanced computational biology and machine learning algorithms is profoundly influencing the initial stages of Zika vaccine development by accelerating hit-to-lead identification. AI-powered platforms analyze vast genomic and proteomic datasets of ZIKV strains to precisely model protein structures and predict immunogenic epitopes, dramatically reducing the time required for rational vaccine design compared to traditional empirical methods. Furthermore, machine learning models are being utilized to analyze high-throughput screening data, ensuring that only the most promising candidates—those exhibiting the optimal balance of immunogenicity and safety—are advanced into expensive and time-consuming in vivo studies, leading to significant cost savings and faster progression.

Beyond discovery, AI is optimizing clinical development and logistical planning. Predictive modeling leverages epidemiological data and environmental factors to forecast potential outbreak hotspots and timeline severity, allowing for strategic planning of Phase II/III trials in geographically appropriate locations, minimizing risks of enrollment failure. In manufacturing, AI algorithms optimize fermentation and purification parameters for novel vaccines, ensuring consistent quality and maximizing yield. This holistic integration of AI, from target identification through logistical supply chain optimization, is crucial for developing a rapid-response capability essential for combating unpredictable emerging infectious diseases like ZIKV.

The dynamics of the Zika Vaccines Market are driven by the persistent threat of congenital defects associated with ZIKV and significant financial support from global health bodies, which act as primary market drivers. These drivers are somewhat counteracted by restraints, including the complex regulatory pathways required for novel vaccine technologies and the logistical challenges inherent in conducting clinical trials in geographically diverse, often remote, outbreak zones. Opportunities exist in leveraging platform technologies, such as mRNA, for faster deployment and in developing combination vaccines that address other co-circulating arboviruses like Dengue and Chikungunya. These internal forces—Drivers, Restraints, and Opportunities—are constantly shaped and amplified by powerful external impact forces, primarily political stability in endemic regions and the fluctuating intensity of public health crises.

Key drivers include substantial investment in R&D from governments and non-profit organizations focused on neglected tropical diseases, alongside the proven correlation between ZIKV infection during pregnancy and severe birth defects, which creates an urgent public health mandate. However, the sporadic nature of ZIKV outbreaks poses a significant restraint; if transmission rates fall between outbreaks, maintaining momentum for large-scale, long-term clinical trials becomes challenging, potentially leading to trial discontinuation or slow enrollment. Another major restraint is the lack of a dedicated, reliable commercial market outside of emergency public health procurement, making sustained private investment difficult without guaranteed advanced market commitments.

Opportunities center on developing second-generation thermostable vaccines that do not require ultra-cold storage, greatly expanding usability in tropical settings with poor infrastructure. Furthermore, the established success of novel platforms (e.g., mRNA technology during the COVID-19 pandemic) has validated these rapid response methods for ZIKV, reducing perceived developmental risk. The most significant impact forces are regulatory harmonization across continents, which could speed up approval processes, and the sustained political commitment to global health security, ensuring continued funding and prioritization of ZIKV prevention despite competing public health crises, solidifying the transition of candidates from research benches to commercialization pipelines.

The Zika Vaccines market is extensively segmented based on the technological platform utilized, reflecting the diverse approaches being explored in the clinical landscape, as well as the target end-users and geographical distribution. The segmentation by vaccine type is critical, illustrating the developmental risk profile, manufacturing scalability, and anticipated efficacy associated with traditional versus cutting-edge methods. Nucleic acid-based platforms and viral vectors represent high-growth potential segments due to their speed of development and relative ease of manufacturing adaptation, whereas inactivated vaccines offer established safety precedents that appeal to cautious regulatory bodies and public health officials prioritizing safety above all else.

Analysis by End-User primarily differentiates between Governmental Agencies and International Organizations (such as WHO, PAHO, UNICEF), which are the main purchasers for large-scale immunization campaigns, and smaller segments such as Research Institutes and commercial hospitals/clinics. This segmentation highlights that procurement in this market is highly centralized and policy-driven, emphasizing the necessity for manufacturers to engage robustly with public health stakeholders rather than focusing on direct-to-consumer sales strategies. The success of a vaccine candidate often hinges not just on its clinical efficacy but on its suitability for large, multi-country procurement tenders, requiring competitive pricing and proven logistical viability.

Geographical segmentation, while based on traditional market definitions, must also account for endemicity, showing high demand and clinical activity in Latin America (especially Brazil, Colombia) and Asia Pacific (Southeast Asian nations). The segmentation provides critical insight for commercial strategy, dictating where manufacturing scale-up, distribution network development, and localized clinical efforts should be concentrated to achieve maximum public health impact and return on investment. The complexity of the supply chain due to varying regional regulatory requirements further necessitates segment-specific planning.

The value chain for the Zika Vaccines Market begins with intensive upstream research and development, involving academic institutions and specialized biotech firms focused on antigen identification, sequence analysis, and basic immunology studies. This initial phase requires substantial investment in highly skilled human capital, advanced genomic sequencing capabilities, and access to proprietary platform technologies, such as novel adjuvants or specialized lipid nanoparticle (LNP) delivery systems essential for nucleic acid vaccines. Key upstream suppliers include providers of high-purity raw materials, bioreactor components, and specialized laboratory reagents necessary for initial preclinical synthesis and formulation. Control over proprietary viral vector systems or mRNA production methodologies grants significant leverage in this initial stage.

Midstream activities center on manufacturing and quality assurance, where clinical-grade production is scaled up, often under strict Good Manufacturing Practice (GMP) guidelines. Manufacturers must navigate complexities related to biosafety levels (particularly for live-attenuated or viral vector products) and ensure batch-to-batch consistency. The selection of distribution channels is critical; direct channels often involve selling in bulk to governmental health ministries or global organizations like PAHO or Gavi, the Vaccine Alliance. Indirect channels rely on established third-party logistics (3PL) providers specialized in cold-chain management, which is essential given the thermal sensitivity of many vaccine candidates, particularly those based on nucleic acids, demanding highly specialized transportation networks.

Downstream activities focus on logistics, immunization delivery, and post-market surveillance. Since Zika vaccines are primarily public health tools, the final distribution is often managed by national public health infrastructure, utilizing existing immunization programs. This final stage involves educating healthcare providers and the public, securing necessary governmental authorizations for emergency use or widespread campaigns, and rigorously monitoring for adverse events, especially given the historical context of concerns regarding antibody-dependent enhancement (ADE) observed in related flavivirus vaccines. Effective downstream performance requires robust cold-chain monitoring (often 2-8°C, or lower for specific novel vaccines) up to the point of injection.

The primary customers and end-users in the Zika Vaccines Market are centralized public health entities with substantial purchasing power, rather than individual patients or private clinics. Governmental Agencies, specifically Ministries of Health in countries within endemic zones (e.g., Brazil, Colombia, India, Thailand), represent the largest segment of potential customers. These agencies are responsible for executing national immunization schedules, managing outbreak responses, and establishing local stockpiles, driving demand through long-term procurement contracts and tenders designed to stabilize pricing and guarantee supply for large populations, particularly pregnant women and women of reproductive age.

International Organizations constitute the second crucial customer segment. This includes major global health alliances such as the World Health Organization (WHO), the Pan American Health Organization (PAHO), and non-governmental entities like the Bill & Melinda Gates Foundation, Gavi, and CEPI. These organizations play a vital role by providing funding mechanisms, facilitating advanced market commitments (AMCs), and coordinating large-scale humanitarian distribution in low-resource settings where ZIKV poses the greatest threat. Their procurement decisions are based on efficacy, cost-effectiveness, suitability for tropical climates (thermostability), and ethical considerations regarding equitable access.

Furthermore, research institutes and academic centers, while not mass consumers, serve as significant early-stage buyers of initial vaccine batches for investigator-led trials, comparative studies, and ongoing surveillance research. Hospitals and clinics act as the final point of care delivery, administering the vaccines procured by governmental or international bodies. Their role is logistical, focusing on storage, professional administration, and accurate reporting of vaccine deployment and any associated monitoring data required for pharmacovigilance, although they typically do not initiate the primary commercial transaction for procurement.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 325.5 Million |

| Market Forecast in 2033 | USD 758.9 Million |

| Growth Rate | 12.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Takeda Pharmaceutical Company Limited, Sanofi S.A., GlaxoSmithKline plc (GSK), Pfizer Inc., Moderna, Inc., Inovio Pharmaceuticals, Inc., Valneva SE, Bharat Biotech International Limited, Themis Bioscience GmbH, Emergent BioSolutions Inc., GeneOne Life Science Inc., GeoVax Labs, Inc., Janssen Pharmaceuticals (Johnson & Johnson), Bavarian Nordic, Novavax, Merck & Co., Inc., Serum Institute of India Pvt. Ltd., CureVac NV, Vaxart, Inc., Osaka University |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Zika Vaccines Market is highly dynamic, characterized by parallel development tracks utilizing both traditional and highly innovative vaccine platforms. Historically, efforts focused on proven methods such as Inactivated and Live-Attenuated vaccines, which leverage whole virus particles to elicit immune responses, offering strong immunogenicity but requiring extensive safety testing to eliminate residual pathogenicity or potential for unexpected side effects. While these methods are robust and manufacturing processes are well-established, they typically require longer development timelines and less flexibility in responding to evolving viral strains, thus presenting a trade-off between speed and historical regulatory acceptance.

The market has seen a rapid acceleration in the adoption of next-generation platform technologies, specifically Nucleic Acid-Based Vaccines (DNA and mRNA) and Viral Vector Vaccines. mRNA technology, validated during the recent global pandemic, represents a paradigm shift due to its ability to be designed and manufactured extremely rapidly, bypassing the need for cell culture or fermentation of the antigen. This speed is critical for ZIKV, which poses an unpredictable epidemic threat. Similarly, Viral Vector vaccines, often using modified Adenovirus or Measles virus vectors to deliver the ZIKV antigen sequence, provide excellent cellular immunity and benefit from scalable manufacturing platforms already in use for other vaccines.

Future technology advancements are concentrating on enhancing delivery systems, particularly improving the thermostability of nucleic acid vaccines to remove the reliance on complex ultra-cold chains, which is prohibitive in many endemic regions. Research is also heavily invested in developing universal flavivirus vaccines—including Zika, Dengue, and West Nile—that offer broad protection, thereby simplifying immunization strategies and providing better preparedness against unexpected cross-reactivity risks. The integration of structural vaccinology and synthetic biology techniques continues to optimize antigen presentation, aiming for high protective efficacy with minimal required dosage and enhanced duration of immunity.

Several Zika vaccine candidates are in various stages of clinical development, with the most advanced technologies including nucleic acid (DNA/mRNA) and viral vector platforms. These candidates are currently undergoing Phase I/II trials, focusing on assessing safety, immunogenicity, and optimal dosing regimens, often with significant backing from global non-profit funding agencies like CEPI.

The pipeline is increasingly dominated by next-generation platforms, particularly mRNA vaccines (due to speed and scalability) and purified inactivated virus (PIV) vaccines, which utilize established manufacturing safety protocols. These rapid-response technologies are favored over traditional live-attenuated approaches due to concerns about potential complications in pregnant women.

The main challenges are the sporadic nature of ZIKV outbreaks, which complicates the execution of large-scale efficacy trials (Phase III), and the absence of a stable commercial market. Furthermore, manufacturers must overcome complex cold-chain requirements for novel vaccines to ensure feasibility in endemic, resource-limited tropical regions.

ADE, where pre-existing antibodies from related flaviviruses (like Dengue) can worsen ZIKV infection, is a major safety concern. Developers are utilizing rational design—especially with subunit and nucleic acid approaches—to target specific, non-cross-reactive epitopes to minimize ADE risk, rigorously monitoring this potential complication throughout clinical trials and post-market surveillance.

Latin America, particularly countries that experienced severe ZIKV outbreaks such as Brazil and Colombia, represents the largest potential customer base due to high endemicity and urgent public health needs. Demand is channeled almost exclusively through Governmental Agencies and international public health organizations in this region.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.