ID : MRU_ 437188 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

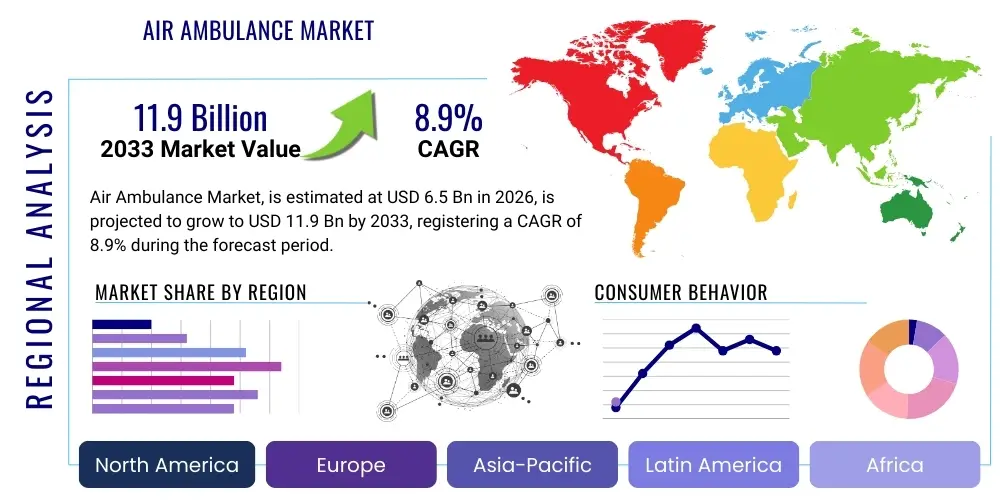

The Air Ambulance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2026 and 2033. This robust growth is attributed to increasing healthcare spending, advancements in aviation technology, and a rising prevalence of critical medical emergencies requiring rapid transportation. The market is estimated at USD 6.5 Billion in 2026 and is projected to reach USD 11.9 Billion by the end of the forecast period in 2033. The continuous expansion of public and private insurance coverage for air medical transport, alongside infrastructural improvements in remote and underserved areas, acts as a primary catalyst for market value appreciation.

Market expansion is particularly noticeable in developing economies where road infrastructure may be poor, making air transport the most viable, or sometimes the only, option for swift patient transfer to tertiary care centers. Furthermore, the increasing complexity of medical procedures, coupled with the centralization of specialized medical services (such as trauma care and organ transplants), necessitates efficient inter-facility transfers, thus bolstering demand for air ambulance services. This projected financial trajectory underscores the essential role air medical services play in modern emergency healthcare systems globally.

The Air Ambulance Market encompasses specialized aviation services dedicated to the emergency and non-emergency transportation of patients, medical personnel, and critical medical equipment. These services are typically deployed using fixed-wing aircraft (like jets) for long-distance inter-facility transfers and rotary-wing aircraft (helicopters) for rapid scene calls and short-distance transport, especially in congested urban areas or difficult terrains. The primary objective is to significantly reduce the time taken to deliver specialized medical care, often referred to as minimizing the "golden hour" for trauma patients, thereby improving patient outcomes and survival rates. The air ambulance product is essentially a comprehensive medical ecosystem integrated within an aircraft, featuring advanced life support systems, specialized medical staff, and communication technologies designed to maintain and stabilize patients during transit.

Major applications of air ambulance services span across various critical healthcare domains. These include trauma and accident response, cardiac emergencies, neurological incidents (such as stroke), neonatal and pediatric critical care transfers, and high-risk obstetric transport. Furthermore, a substantial segment of the market is dedicated to inter-facility transfers, particularly involving the transport of patients requiring specialized equipment like ECMO (Extracorporeal Membrane Oxygenation) or those awaiting organ transplants. The benefits are multifaceted, encompassing quicker access to specialized definitive care, enhanced operational flexibility compared to ground ambulances, and the capability to traverse geographical barriers rapidly.

Driving factors propelling market growth include the globalization of medical tourism, demanding high standards of international medical transport; increasing investments by governments and private entities in emergency medical services (EMS) infrastructure; and technological innovations in aircraft design focused on improving safety, speed, and capacity for advanced medical equipment. Moreover, the aging global population, which is more susceptible to chronic illnesses requiring specialized emergency care, consistently drives the demand curve upwards. The crucial awareness among medical professionals and the public regarding the time-critical nature of certain medical conditions further solidifies the essential nature of air ambulance operations.

The Air Ambulance Market is characterized by robust growth driven by accelerating demand for immediate critical care and inter-facility patient transfers across high-income and rapidly developing regions. Business trends indicate a strong move towards fleet modernization, incorporating technologically advanced helicopters and jets that offer greater range, speed, and superior cabin space for complex medical procedures en route. Strategic partnerships between air ambulance operators and hospital networks, as well as cross-border collaborations, are defining market consolidation strategies, aimed at improving operational efficiency and expanding service coverage, particularly into historically underserved rural areas. Furthermore, the emphasis on value-based care and the negotiation of favorable reimbursement policies with private insurers and governmental bodies remain critical for sustained profitability in this capital-intensive sector.

Regionally, North America maintains the dominant market share, primarily due to established reimbursement models, a high concentration of sophisticated trauma centers, and significant penetration of Helicopter Emergency Medical Services (HEMS). However, the Asia Pacific region is anticipated to register the highest Compound Annual Growth Rate (CAGR), fueled by expanding healthcare infrastructure in countries like China and India, increased public health spending, and a growing recognition of the necessity for standardized emergency response systems. Europe exhibits steady growth, focusing on consolidating fragmented national services into more efficient pan-European air medical networks, often integrated tightly with national healthcare systems. Regulatory harmonization and standardization of training across regions are emerging trends impacting global market operations.

In terms of segmentation trends, the rotary-wing segment (helicopters) continues to dominate in short-haul and accident scene response due to its vertical take-off and landing capabilities, crucial in urban and mountainous settings. Concurrently, the fixed-wing segment is gaining traction, particularly for long-distance and international patient repatriation, benefiting from increasing travel and medical globalization. The service type segment shows a clear tilt toward scene response operations, but the inter-facility transfer segment is rapidly expanding due to the increasing specialization and centralization of critical medical expertise in large urban tertiary centers, necessitating efficient transfers from smaller regional hospitals. Payor segmentation highlights the increasing role of private insurance and out-of-pocket payments, though government funding remains foundational in many national markets.

User queries regarding AI's influence in the Air Ambulance Market predominantly revolve around optimizing response times, enhancing flight safety, improving operational logistics, and the reliability of AI in critical decision-making during patient stabilization. Users are seeking to understand how AI can move beyond simple data logging to provide predictive analytics for emergency routing, crew deployment, and maintenance scheduling. Key concerns often focus on data privacy (HIPAA compliance, GDPR) and the regulatory framework surrounding autonomous or semi-autonomous flight capabilities, especially in sensitive environments. There is high expectation that AI will dramatically reduce operational costs while simultaneously increasing the efficiency and reach of services, particularly in anticipating high-demand periods and managing complex cross-border transfers.

Artificial Intelligence and Machine Learning (ML) are set to revolutionize air ambulance operations by transforming logistical planning and clinical decision support. AI algorithms can process real-time variables—including weather conditions, air traffic, hospital bed availability, physician specialization, and patient vitals—to calculate the optimal flight path and destination hospital within milliseconds. This predictive routing capability significantly cuts down the crucial response time, directly impacting patient prognosis. Furthermore, AI-powered predictive maintenance models analyze telemetry data from aircraft systems to foresee potential mechanical failures, allowing for proactive servicing and minimizing costly, mission-critical downtime, thus enhancing overall operational safety and reliability.

Beyond logistics, AI is proving invaluable in clinical support within the confines of the aircraft cabin. AI-driven diagnostic tools can assist flight paramedics and nurses in interpreting complex patient data collected from monitoring devices, offering real-time recommendations for treatment adjustments based on established clinical guidelines. This is particularly beneficial in scenarios involving rare or rapidly evolving conditions where on-board personnel may need immediate, sophisticated secondary clinical consultation. As data aggregation from past missions informs these AI models, the sophistication and accuracy of clinical recommendations will continuously improve, standardizing high-quality care delivery regardless of the geographical location or specific medical personnel on board.

The Air Ambulance Market is influenced by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO), which collectively shape its growth trajectory and operational environment. Key drivers include the escalating global incidence of trauma cases and cardiovascular diseases, requiring immediate, specialized transport; the increasing efficiency and standardization of global air medical infrastructure; and favorable regulatory environments, particularly concerning safety standards and cross-border operations. However, significant restraints impede growth, primarily the high initial capital investment required for purchasing and equipping specialized aircraft, coupled with the exorbitant operational costs (fuel, highly trained personnel, and specialized maintenance). The critical nature of these services means that operational reliability and safety mandates exert immense pressure on providers.

Opportunities for market growth lie predominantly in geographical expansion, particularly leveraging emerging economies in APAC and MEA where EMS systems are underdeveloped, offering a substantial need for rapid medical access. Furthermore, technological opportunities, such as the adoption of Unmanned Aerial Vehicles (UAVs) for transporting medical supplies or less critical patients, and advancements in telemedicine integrated into air transport, present avenues for cost reduction and service expansion. Addressing the restraint of high cost through innovative service models, such as shared service agreements between smaller regional hospitals, or public-private partnerships, can unlock untapped market potential.

Impact forces govern the market’s responsiveness to external changes. Political and legal impact forces are high, as air ambulance operations are heavily dependent on air traffic control regulations, cross-border flight permissions, and standardized medical licensing. Economic forces exert a strong influence, given that service demand is often inelastic (critical emergencies), but affordability and reimbursement mechanisms dictate profitability. Social forces, particularly public awareness regarding the benefits of rapid medical transport and cultural acceptance of air medical services, are gradually shifting positively, encouraging utilization. Technology acts as a pivotal force, continually enabling faster, safer, and more capable air assets, thereby reducing operational limitations and increasing the overall impact potential of air medical services globally.

The Air Ambulance Market is extensively segmented based on service type, aircraft type, and end-user, providing a granular view of demand patterns and strategic areas for investment. Segmentation by service type distinguishes between critical scene response (transporting patients directly from accident sites) and inter-facility transfers (moving patients between hospitals for specialized care), with both segments demonstrating strong growth but driven by different geographical and infrastructural factors. The segmentation by aircraft type, separating fixed-wing and rotary-wing aircraft, reflects differences in mission profile, range, and cost structures, crucial for operators planning fleet composition. Understanding these segments is vital for stakeholders to tailor services, manage costs effectively, and comply with varied regional regulatory standards, optimizing resource allocation based on specific demand characteristics.

The air ambulance value chain is complex, starting with upstream activities involving aircraft manufacturing, highly specialized avionics and medical equipment production, and the rigorous training of aviation and medical personnel. Key upstream suppliers include established aerospace companies providing highly reliable, airworthy platforms suitable for medical modifications, as well as specialized medical device companies supplying portable ventilators, advanced monitoring systems, and infusion pumps optimized for flight conditions. The ability to secure aircraft meeting stringent operational criteria, coupled with efficient parts and maintenance supply logistics, is paramount to maintaining high service availability, which is a key performance indicator in this market.

Midstream activities involve the core air ambulance service operation, including flight logistics, scheduling, dispatch, maintenance, and the direct provision of clinical care during transport. This stage is heavily influenced by regulatory compliance (e.g., FAA/EASA regulations, medical licensing) and the strategic positioning of aircraft. Distribution channels are generally direct, relying on sophisticated communication networks to connect accident scenes or referring hospitals directly to the air ambulance operator's dispatch center. This immediacy in communication is critical; thus, robust IT and telecommunication infrastructure forms an integral part of the service delivery mechanism.

Downstream analysis focuses on the end-users—hospitals, governmental agencies, and insurance companies—and the reimbursement mechanisms. Hospitals act as major referrers and often partners, integrating air ambulance services into their overall trauma and transfer protocols. Indirect distribution involves partnerships with insurance providers or third-party administrators who manage the payment and coordination logistics for patients. Operational efficiency, defined by rapid turnaround times, flawless safety records, and successful clinical outcomes, ultimately determines the value captured downstream, affecting contract renewals and reimbursement rates. Effective management of this integrated chain, from procuring advanced aircraft to securing prompt final payment, is crucial for sustained market leadership.

The primary customers and end-users of air ambulance services are diverse, spanning the entire healthcare ecosystem and involving various governmental and private entities. Hospital networks, particularly those designated as Level I trauma centers or highly specialized tertiary care facilities (e.g., cardiology, neurosurgery, organ transplantation centers), constitute the most frequent and crucial end-users. These institutions rely on air ambulances for efficient inter-facility transfers of critically ill or injured patients who require capabilities beyond what the referring facility can provide, ensuring continuity of high-level care.

Another significant customer base includes governmental agencies, military forces, and public safety organizations. These entities require air medical evacuation services for disaster relief, search and rescue operations, and transporting service members, often through long-term contracts guaranteeing service readiness and adherence to specific military or governmental operational standards. The third major segment encompasses private insurance companies, health maintenance organizations (HMOs), and medical assistance providers, which contract air ambulance services to manage patient transport logistics for their insured members, aiming to control costs while ensuring high-quality, rapid access to necessary medical facilities.

Finally, a growing segment involves private individuals and medical tourists, often utilizing air ambulance services for international patient repatriation or non-emergency transfers over significant distances. While often highly price-sensitive, this segment demands exceptional customer service, sophisticated logistics planning, and transparency regarding medical and aviation credentials. The convergence of these customer groups mandates a flexible, highly reliable, and medically comprehensive service offering tailored to distinct contractual requirements and operational expectations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 11.9 Billion |

| Growth Rate | 8.9% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Global Medical Response (GMR), Air Methods Corporation, PHI Air Medical, Metro Aviation Inc., Babcock International Group, STARS, REGA, AirLink/VitaLink, Acadian Companies, Scandinavian Air Ambulance, AMR Air Ambulance, CareFlight, Express Aviation Services, Blackcomb Aviation, London Air Ambulance, Era Group Inc., Ornge, Air Charter Service, European Air Ambulance, FAI rent-a-jet. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Air Ambulance Market is rapidly evolving, driven by the need for increased safety, efficiency, and advanced in-flight medical capabilities. A primary focus lies in integrating sophisticated avionics, including state-of-the-art navigation systems like GPS/GLONASS and Synthetic Vision Systems (SVS), which enhance situational awareness, especially during low-visibility conditions or complex landings, directly improving operational safety. Furthermore, advanced communication systems, such as satellite communication links and high-speed data transmission, ensure seamless connectivity between the aircraft, ground control, and the receiving hospital, enabling real-time transmission of patient data and remote consultation with specialist physicians on the ground.

On the medical front, technology centers on creating miniaturized, ruggedized, and portable versions of equipment traditionally found in intensive care units (ICUs). This includes advanced cardiac monitors, compact blood gas analyzers, high-frequency ventilators, and mobile ECMO units specifically engineered to withstand the vibrations, altitude changes, and space constraints inherent in air travel. The trend toward integration also means that all monitoring devices are networked, feeding real-time vital signs directly into electronic patient records (EPRs), facilitating faster and more accurate handover upon arrival at the trauma center. The goal is to provide an ICU environment in the sky.

Emerging technologies, especially in automation, are set to redefine operations. This includes the testing and potential deployment of Unmanned Aerial Vehicles (UAVs) for autonomous delivery of blood, pharmaceuticals, or automated external defibrillators (AEDs) to remote scenes, and potentially, in the long term, for transporting patients themselves. Furthermore, advanced simulator training using Virtual Reality (VR) and Augmented Reality (AR) allows flight crews to practice complex, high-stress medical procedures and mission profiles in a risk-free environment, significantly elevating the standard of care provided during transport and minimizing human error during actual operations.

Regional analysis reveals significant disparities in market maturity, regulatory frameworks, and service demand across the globe, defining strategic focus areas for air ambulance providers. North America, comprising the United States and Canada, represents the most mature and lucrative market. This dominance is sustained by highly developed trauma systems, established Helicopter Emergency Medical Services (HEMS) networks, and robust, though complex, governmental and private insurance reimbursement structures that support high utilization rates. The sheer volume of critical care transport, coupled with continuous technological investment in the fleet, ensures North America remains a cornerstone of the global market, setting the benchmark for operational standards and clinical excellence.

Europe presents a strong but often fragmented market, characterized by nationally managed, often publicly funded, air ambulance services (e.g., NHS in the UK, national agencies in Scandinavian countries). While utilization is high, regulatory harmonization remains a key challenge, particularly for cross-border operations. Central and Western European nations drive growth through sophisticated inter-facility transfers, especially for highly specialized care. Conversely, the Asia Pacific (APAC) region is poised for explosive growth, driven by rapid urbanization, increasing per capita income leading to greater demand for premium healthcare services, and vast geographical challenges requiring fixed-wing transport. Governments in countries like India, China, and Australia are making substantial investments to integrate air medical services into their national disaster response and public health frameworks.

The Middle East and Africa (MEA) and Latin America (LATAM) markets offer substantial long-term growth opportunities, although they currently face hurdles related to economic volatility, lower penetration of private insurance, and underdeveloped aviation infrastructure outside major metropolitan hubs. In the Middle East, high oil revenues support significant investment in state-of-the-art air medical fleets, focusing on complex inter-country transfers and high-net-worth individual transport. In LATAM, growth is often concentrated around large metropolitan areas and driven by private sector investment filling gaps left by often inadequate public emergency services. These regions require tailored solutions, often leaning towards long-range fixed-wing aircraft for significant geographical coverage.

The high cost of air ambulance services is primarily driven by substantial operational expenses, including the massive capital investment in purchasing and medically equipping specialized aircraft (rotary and fixed-wing), continuous fuel and maintenance costs, and the need for highly specialized, certified medical and aviation crews who require rigorous, ongoing training and certifications.

Rotary-wing aircraft (helicopters) are optimized for short-distance, critical scene response missions due to their vertical takeoff/landing capability and agility in complex terrain or urban environments. Fixed-wing aircraft are utilized for long-distance inter-facility transfers and international patient repatriation, offering greater speed, range, and cabin capacity for extended complex care.

AI significantly enhances safety and efficiency by providing predictive maintenance scheduling to prevent mechanical failures, optimizing flight routing in real-time based on weather and air traffic, and assisting on-board medical crews with clinical decision support systems, thereby streamlining operations and reducing critical response times.

North America (primarily the US) holds the largest market share due to its established infrastructure of specialized trauma centers, widespread acceptance and integration of Helicopter Emergency Medical Services (HEMS), high prevalence of private insurance coverage, and sophisticated, though often challenging, reimbursement models supporting service utilization.

Air ambulance services are utilized for both, but the market shows strong growth in inter-facility transfers. While scene response remains critical for trauma, the centralization of highly specialized medical services (e.g., organ transplant, severe burns, complex neurosurgery) increasingly necessitates rapid, safe transport between regional and tertiary care centers, driving the inter-facility segment.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.