ID : MRU_ 433312 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

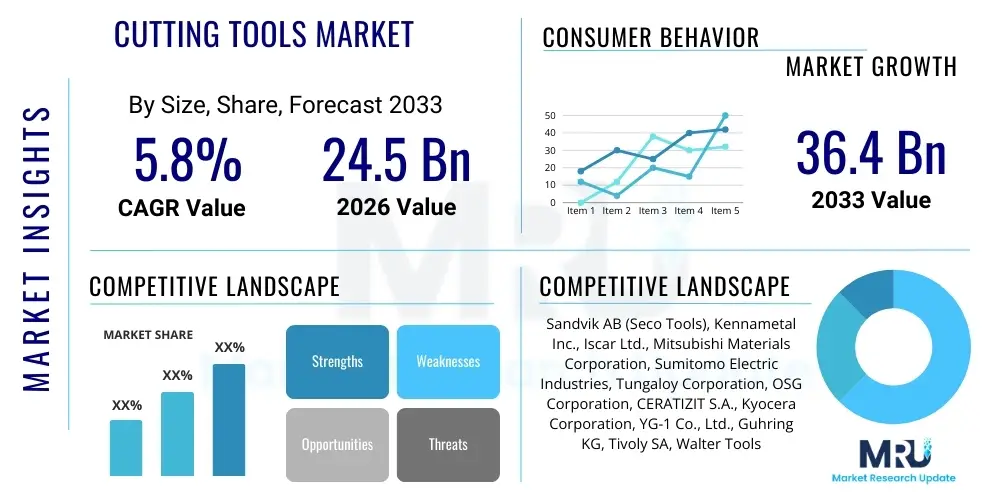

The Cutting Tools Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $24.5 Billion in 2026 and is projected to reach $36.4 Billion by the end of the forecast period in 2033.

The Cutting Tools Market encompasses a vast array of high-precision instruments essential for machining processes across virtually all manufacturing sectors. These tools, which include drills, mills, reamers, taps, and inserts, are critical for shaping, sizing, and finishing components to exacting specifications. Market growth is fundamentally driven by the expanding global demand for complex, high-tolerance components, particularly within the automotive, aerospace, medical device, and energy sectors, where material complexity (such as high-strength steels, titanium alloys, and composites) necessitates specialized tooling materials and sophisticated coating technologies like Physical Vapor Deposition (PVD) and Chemical Vapor Deposition (CVD). The continuous innovation in material science and tool geometries is a key enabler for productivity gains in modern manufacturing environments, allowing for faster processing speeds and extended tool life.

Major applications of cutting tools span high-volume production lines, specialized job shops, and integrated manufacturing systems. In the automotive industry, these tools are indispensable for powertrain components, chassis parts, and increasingly for battery enclosures in electric vehicles (EVs). The aerospace sector demands tools capable of handling superalloys with exceptional thermal stability and precision, vital for jet engine components and structural airframe parts. The inherent benefits of utilizing advanced cutting tools include improved surface finish quality, significant reduction in cycle times, enhanced machining accuracy, and crucial cost savings stemming from reduced downtime and optimized material removal rates. The performance of a cutting tool directly influences the overall efficiency and profitability of a manufacturing operation.

Driving factors propelling this market include the global trend toward industrial automation and the implementation of Industry 4.0 principles, which mandate higher performance and data integration capabilities from tooling. Furthermore, the increasing complexity of raw materials used in next-generation products, such as lightweighting initiatives in transportation, fuels continuous research and development into novel tool substrates (like specialized carbides and ceramics) and intelligent tooling systems equipped with embedded sensors for real-time monitoring. This focus on maximizing operational efficiency and adapting to new material challenges is the core catalyst for market expansion.

The Cutting Tools Market Executive Summary highlights a pronounced shift toward digitization and high-performance material applications. Current business trends indicate robust investment in hybrid manufacturing solutions that integrate subtractive processes with additive capabilities, fundamentally altering tool design requirements and usage patterns. The push for automated machining centers and unattended operation necessitates the adoption of highly reliable, long-life tools and sophisticated tool management software, reducing reliance on manual intervention and optimizing inventory control. Geographically, the Asia Pacific (APAC) region continues its dominance, fueled by massive industrial expansion in China, India, and Southeast Asia, driven by local and export-oriented manufacturing, particularly in consumer electronics and automotive parts. This regional growth is coupled with strategic investments in high-tech manufacturing centers in North America and Europe, focusing on advanced aerospace and medical device production.

Segment trends reveal a rapid adoption of Indexable Inserts due to their versatility and cost-efficiency in heavy-duty and roughing applications, allowing manufacturers to quickly swap out worn cutting edges without replacing the entire tool body. Concurrently, the demand for Solid Carbide tools is accelerating in high-precision and miniature machining applications, benefiting from superior rigidity and wear resistance crucial for intricate component features. Material innovation within these segments, focusing on advanced coatings such as aluminum chromium nitride (AlCrN) and diamond-like carbon (DLC), ensures tools can withstand extreme temperatures and pressures generated when machining difficult-to-cut materials like nickel-based superalloys and hardened steels.

The overall market trajectory is defined by consolidation among major players seeking to acquire specialized technology firms and expand their regional service capabilities, ensuring they can provide comprehensive tooling solutions alongside technical expertise. This consolidation, coupled with the rising imperative for sustainability in manufacturing, drives demand for reconditioning and recycling programs for expensive tools like carbide inserts. Successful market participation requires companies to excel not only in material science but also in delivering digital services, predictive analytics, and integrated tool management systems that align with the smart factory ecosystem, ensuring maximum tool performance and operational transparency across the customer base.

User queries regarding the impact of Artificial Intelligence (AI) on the Cutting Tools Market primarily center on three core areas: predictive maintenance, optimization of tool selection and path generation, and closed-loop quality control in autonomous machining environments. Users are keenly interested in how AI algorithms can leverage data from spindle loads, vibration sensors, and acoustic emissions to accurately predict tool wear and impending failure, thereby maximizing tool utilization and minimizing costly unplanned downtime. A significant concern revolves around the integration complexity—specifically, how to effectively merge proprietary tool data with machine tool control systems (CNC) and Manufacturing Execution Systems (MES) using cloud-based or edge computing solutions. Expectations are high that AI will lead to truly self-optimizing machining processes, moving beyond simple programmed parameters to dynamic, real-time adjustments of feed rates and speeds based on instantaneous machining conditions and material behavior, fundamentally transforming tooling life management and process stability.

AI’s influence extends profoundly into the design and performance validation phases of cutting tools. Generative design tools, powered by AI, are enabling manufacturers to iterate tool geometries faster, optimizing chip evacuation, thermal management, and vibration damping far beyond conventional simulation methods. This capability allows tool makers to rapidly respond to unique material challenges presented by industries like aerospace, where complex geometries and difficult materials are standard. Furthermore, AI assists in optimizing supply chain logistics and inventory management for end-users by forecasting demand for specific tool types based on production schedules and historical wear rates across disparate machine fleets, providing a robust solution to maintain lean inventories while ensuring tool availability.

In the context of generative manufacturing environments, AI facilitates the creation of digital twins for cutting tools, allowing operators and engineers to simulate the performance of a new tool or coating under various stress scenarios before it even reaches the physical production floor. This simulation capability dramatically reduces prototype costs and speeds up time-to-market for specialized tools. Ultimately, AI transforms the cutting tool from a passive consumable into an integral, intelligent component of the digital manufacturing ecosystem, providing actionable data that informs not only the immediate machining process but also future capital investment and tooling procurement strategies across the entire enterprise.

The Cutting Tools Market is shaped by significant Drivers, Restraints, Opportunities, and complex Impact Forces. Key drivers include the exponential growth in the global automotive industry, particularly the rapid transition toward Electric Vehicles (EVs), which requires specialized tooling for new materials like aluminum, composite battery housings, and intricate motor components, moving away from traditional internal combustion engine (ICE) tooling. Simultaneously, the persistent demand for lightweighting across aerospace and automotive sectors necessitates tooling capable of efficiently processing difficult-to-cut materials such as titanium alloys (Ti-6Al-4V) and nickel-based superalloys (Inconel), driving innovation in High-Performance Cutting (HPC) technologies. The ongoing global trend of industrial automation and the proliferation of advanced five-axis and multi-tasking CNC machines also fuels demand for specialized, high-rigidity tools designed for complex machining operations, emphasizing precision and minimizing operational variance across the supply chain.

Restraints in the market primarily involve the high volatility and increasing cost of raw materials, particularly tungsten carbide, which forms the foundation of most high-performance cutting tools. Fluctuations in geopolitical stability and supply chain disruptions can severely impact procurement costs and lead times, pressuring manufacturers to seek alternative materials or intensify recycling initiatives. Additionally, the shortage of highly skilled machinists and programmers capable of leveraging the full potential of advanced CNC machines and sophisticated tooling remains a structural restraint, slowing the adoption rate of some ultra-high-end tool systems that require specialized knowledge for optimal setup and operation. Economic downturns or regional trade disputes can temporarily suppress capital expenditure in manufacturing sectors, impacting tool consumption.

Opportunities are abundant, centered around the integration of Additive Manufacturing (AM) capabilities into the tooling production process, allowing for the creation of customized tools with intricate internal cooling channels that significantly enhance performance and thermal stability. The burgeoning medical device manufacturing sector, requiring micron-level precision for implants and surgical instruments, represents a high-value niche market demanding specialized micro-tooling solutions. Furthermore, the development of intelligent tooling—tools embedded with RFID tags or sensors for monitoring performance and identity—offers a compelling opportunity for market players to transition from being simple tool suppliers to providers of integrated manufacturing data services, aligning perfectly with the demands of Industry 4.0 environments. The combined impact forces result in a market where technical expertise, material innovation, and digital integration are the non-negotiable prerequisites for sustained competitive advantage.

The Cutting Tools Market is meticulously segmented based on product type, material composition, end-use application, and distribution channel, reflecting the diverse and highly specialized requirements of modern manufacturing. Segmentation analysis is critical for understanding market dynamics, as different segments exhibit varying growth rates influenced by technological advancements, regulatory environments, and regional industrial output. The primary product segmentation distinguishes between Indexable Tools, favored for large-scale, versatile, and heavy material removal tasks due to their replaceable inserts, and Solid Tools, preferred for high-precision finishing, small-part machining, and superior rigidity in intricate applications. The evolution of composite materials and high-strength alloys continues to drive investment specifically within the high-performance material and specialized application segments, creating lucrative niche markets.

Material composition segmentation highlights the dominance of cemented carbide, followed by High-Speed Steel (HSS), ceramics, and superhard materials like Polycrystalline Diamond (PCD) and Cubic Boron Nitride (CBN). Cemented carbide tools, often enhanced with advanced coatings (TiN, AlTiN, CVD Diamond), remain the industry standard, balancing cost, toughness, and wear resistance. However, the rapidly growing demand from the aerospace and medical sectors for machining superalloys is accelerating the utilization of specialized ceramics and CBN, which offer superior performance at elevated temperatures and hardness levels. Understanding this material shift is crucial for manufacturers developing next-generation tooling portfolios, ensuring compatibility with evolving manufacturing specifications.

Application segmentation reveals the automotive and general engineering sectors as the largest consumers, though aerospace and defense consistently drive demand for the highest performance and most expensive tools. The medical sector, demanding stringent traceability and micro-machining capabilities for implants and instruments, is becoming a key focus area for specialized tool makers. Regional analysis further refines these segment insights, showing that adoption rates of advanced tooling vary significantly, heavily influenced by local manufacturing maturity, labor costs, and governmental support for digitalization initiatives. The ongoing technological push towards higher throughput and precision across all these sectors underpins the stable long-term growth of the market.

The Value Chain for the Cutting Tools Market is characterized by highly specialized stages, beginning with upstream procurement of critical raw materials, principally Tungsten, Cobalt, and specialized powder metal alloys. The upstream segment is challenged by resource concentration and geopolitical risks associated with these strategic materials, necessitating robust sourcing and recycling strategies. Manufacturers engage in complex powder metallurgy and sintering processes to create the carbide blanks and substrates, requiring significant capital investment in high-precision equipment and specialized metallurgical expertise to control grain size and material purity, which directly influences the final tool performance. This foundational stage dictates the quality, cost, and availability of the core tool structure, making supply chain resilience a paramount operational concern for major tool producers globally.

The midstream component involves the core manufacturing process, including pressing, sintering, grinding, and, crucially, the application of advanced coatings (CVD/PVD). This phase is highly capital-intensive and technologically advanced, with market leaders investing heavily in proprietary grinding machines and coating technologies to achieve micron-level tolerances and superior wear resistance. Tool geometry design, often aided by computational fluid dynamics and advanced simulation software, is a critical value-add during this stage, differentiating premium tool providers. Standardization is prevalent in high-volume, general-purpose tools, while custom engineering dominates in niche sectors like aerospace or medical, where unique material compositions require bespoke tooling solutions and rapid prototyping capabilities.

Downstream activities focus on distribution, technical support, and end-user engagement. Distribution channels are typically a mix of direct sales to large Original Equipment Manufacturers (OEMs) for high-volume, standardized contracts, and an extensive network of specialized industrial distributors or third-party integrators who provide localized inventory, technical consultation, and regrinding/reconditioning services to small and medium enterprises (SMEs). The trend is moving towards integrating digital services, where tool manufacturers offer sophisticated tool management software (TMS), vending solutions, and performance monitoring as part of the overall offering. Technical support, including application engineering and process optimization advice, is a key differentiating factor, transforming the distributor relationship from transactional to strategic, ultimately enhancing overall customer productivity and loyalty in a highly competitive B2B market environment.

The primary customers (End-Users/Buyers) of cutting tools are diverse manufacturing entities that require precise material removal to create finished components. The largest segment remains the Automotive industry, encompassing both traditional internal combustion engine (ICE) component suppliers and the rapidly expanding Electric Vehicle (EV) supply chain, including battery enclosure manufacturers, motor housing suppliers, and structural component producers focused on lightweight materials like aluminum and composites. These customers require high volumes of reliable, standardized tools for long production runs, alongside specialized tools for complex machining of new EV components, driving demand for both indexable and solid carbide solutions optimized for high-speed machining environments.

The Aerospace and Defense sector represents a vital, high-value customer base, characterized by stringent quality control and the need to machine exotic materials (e.g., Inconel, Titanium alloys) that are extremely difficult to cut. Customers in this segment prioritize tool reliability, precision, and application-specific engineering support over absolute cost, driving demand for specialized superhard materials (CBN, PCD) and highly customized geometries capable of withstanding extreme thermal loads and minimizing material hardening during machining. These buyers often maintain direct relationships with tool manufacturers for technical consultancy and proprietary tool development programs, seeking strategic partnerships rather than simple transactional purchases.

Other significant potential customers include the General Engineering and Machine Shops segment, which comprises numerous small and medium enterprises (SMEs) requiring a versatile range of tools for job-shop environments, typically sourced through local industrial distributors. Furthermore, the Medical Device sector is a rapidly growing customer segment, demanding micro-machining capabilities for implants, surgical instruments, and prosthetic components, emphasizing materials like stainless steel, titanium, and specialized polymers. The Energy sector, including oil & gas drilling equipment and wind turbine component manufacturers (requiring large-diameter tooling for gearbox and hub machining), also constitutes a significant buyer base, particularly for robust tools designed for heavy-duty, demanding applications in specialized materials.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $24.5 Billion |

| Market Forecast in 2033 | $36.4 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Sandvik AB (Seco Tools), Kennametal Inc., Iscar Ltd., Mitsubishi Materials Corporation, Sumitomo Electric Industries, Tungaloy Corporation, OSG Corporation, CERATIZIT S.A., Kyocera Corporation, YG-1 Co., Ltd., Guhring KG, Tivoly SA, Walter Tools (Sandvik), Mapal Dr. Kress KG, LMT Tools, Emuge-Franken, HARVI, Nachi-Fujikoshi Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Cutting Tools Market is undergoing rapid transformation, largely driven by the demands of digital manufacturing and the processing of novel materials. A primary technological focus is on enhancing tool longevity and performance through advanced coating science. Multi-layer and nanocomposite coatings, utilizing techniques like High-Power Impulse Magnetron Sputtering (HiPIMS) for PVD applications, are becoming standard, offering superior hardness, reduced friction, and thermal stability compared to traditional mono-layer coatings. These advanced surface treatments are crucial for maintaining edge integrity when machining high-temperature alloys and hardened steels at aggressive speeds and feeds, extending the period between tool changes and supporting lights-out manufacturing operations.

Another pivotal technological development is the integration of embedded intelligence within the tools themselves, often referred to as 'Smart Tooling'. This involves incorporating micro-sensors, RFID chips, or data matrix codes that facilitate real-time performance monitoring, tool identification, and traceability throughout the entire lifecycle. These sensors can transmit data related to temperature, vibration, and cutting forces back to the machine control and cloud systems. This data, when analyzed by AI, enables adaptive control systems to dynamically adjust machining parameters, leading to optimal material removal rates, and providing crucial inputs for proactive maintenance scheduling. This shift towards data-driven tooling management is critical for operational excellence in Industry 4.0 facilities, moving beyond traditional, time-based maintenance models.

Furthermore, Additive Manufacturing (AM) is increasingly impacting tool production, particularly in creating specialized tool bodies (shanks and holders) with complex internal geometries impossible to achieve through conventional methods. Laser Powder Bed Fusion (LPBF) allows for the incorporation of intricate conformal cooling channels directly into the tool holder, enabling highly efficient dissipation of heat from the cutting zone. This significantly reduces thermal shock on the cutting edge, improving tool life and overall process stability, especially when deep-hole drilling or machining heat-sensitive materials. While the inserts themselves are still predominantly manufactured using sintering, the customization of the tool body using AM represents a significant technological leap toward optimized and application-specific cutting solutions, driving greater customization in the high-end market segment.

The market growth is fundamentally driven by the global transition towards electric vehicle (EV) manufacturing, necessitating new aluminum and composite machining tools, alongside the stringent demand for precision components in the expanding aerospace and medical device sectors. The adoption of advanced manufacturing techniques (Industry 4.0) and the increasing need to machine high-strength, lightweight materials also fuel demand.

The EV transition reduces demand for tooling used in traditional internal combustion engines (ICE) but significantly increases demand for specialized tools used to machine large aluminum battery enclosures, electric motor housings, and lightweight chassis components. This shifts focus toward high-speed machining (HSM) and robust tools optimized for non-ferrous and composite materials.

The Cemented Carbide segment dominates the market due to its superior balance of hardness, toughness, and wear resistance, making it suitable for a wide range of general and high-performance applications. Ongoing advancements in carbide coatings (PVD/CVD) further solidify its dominance, enabling higher productivity and longer tool life across diverse end-use industries.

AI plays a critical role in enabling predictive maintenance by analyzing sensor data to forecast tool wear, optimizing tool path and cutting parameters in real-time, and accelerating the design of new, high-performance tool geometries using generative design methodologies, enhancing overall machining efficiency.

The Asia Pacific (APAC) region offers the highest growth potential, attributed to sustained large-scale industrial expansion, governmental support for manufacturing bases in countries like China and India, and the rising consumer demand for locally produced goods across the automotive and electronics supply chains.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.