ID : MRU_ 439373 | Date : Jan, 2026 | Pages : 257 | Region : Global | Publisher : MRU

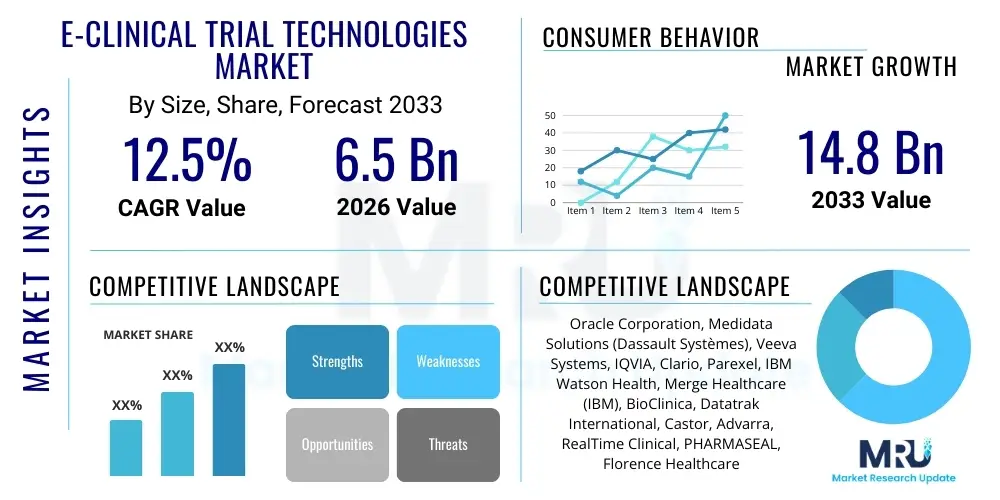

The E-Clinical Trial Technologies Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.5% between 2026 and 2033. The market is estimated at USD 2.8 Billion in 2026 and is projected to reach USD 7.1 Billion by the end of the forecast period in 2033.

The E-Clinical Trial Technologies Market encompasses a broad range of software solutions and services designed to streamline, optimize, and manage the complex processes involved in clinical research. These technologies are critical for enhancing the efficiency, accuracy, and compliance of clinical trials, which are fundamental to the development of new drugs, therapies, and medical devices. The core offerings within this market include Electronic Data Capture (EDC) systems, Clinical Trial Management Systems (CTMS), Electronic Clinical Outcome Assessment (eCOA) and Electronic Patient-Reported Outcome (ePRO) solutions, Randomization and Trial Supply Management (RTSM) platforms, and Electronic Trial Master File (eTMF) systems. These technologies collectively aim to digitalize traditionally manual processes, ensuring data integrity, accelerating study timelines, and reducing operational costs across all phases of clinical development.

The primary applications of e-clinical trial technologies span the entire clinical research lifecycle, from initial study design and patient recruitment to data collection, monitoring, analysis, and regulatory submission. Benefits derived from the adoption of these solutions are extensive, including improved data quality, reduced data entry errors, enhanced real-time access to clinical data, faster trial completion rates, and greater cost-effectiveness compared to paper-based methods. Furthermore, e-clinical technologies facilitate better collaboration among various stakeholders, including sponsors, contract research organizations (CROs), investigators, and regulatory bodies, by providing centralized platforms for information sharing and project management. The ability to conduct decentralized or hybrid trials, which gained significant traction during recent global health crises, is also largely dependent on robust e-clinical infrastructure.

Several driving factors are propelling the growth of the E-Clinical Trial Technologies Market. A primary driver is the increasing complexity and cost of clinical trials, necessitating more efficient and technologically advanced solutions to manage vast amounts of data and diverse regulatory requirements across multiple geographies. The rising demand for new drug discoveries, particularly in oncology, rare diseases, and personalized medicine, fuels greater investment in clinical research and, consequently, in the technologies that support it. Furthermore, stringent regulatory mandates from bodies like the FDA and EMA for data quality, traceability, and patient safety encourage the adoption of validated e-clinical systems. The growing trend towards remote monitoring, decentralized trials, and patient-centric approaches, alongside advancements in cloud computing and data analytics, also significantly contributes to market expansion by making these technologies more accessible and powerful for a wider range of clinical research stakeholders.

The E-Clinical Trial Technologies Market is experiencing robust growth driven by an imperative to enhance efficiency and reduce costs in drug development. Key business trends indicate a strong shift towards integrated platforms that offer end-to-end solutions, moving beyond standalone systems to provide comprehensive suites encompassing EDC, CTMS, eCOA/ePRO, and eTMF functionalities. This integration aims to minimize data silos, improve interoperability, and provide a holistic view of trial progress. Furthermore, there is a growing emphasis on user-friendly interfaces and mobile accessibility to facilitate greater adoption among site staff and patients, particularly as decentralized clinical trials (DCTs) become more prevalent. Companies are investing heavily in research and development to incorporate cutting-edge technologies like artificial intelligence (AI), machine learning (ML), and predictive analytics, which promise to revolutionize data processing, patient recruitment, and risk-based monitoring strategies. Consolidation through mergers and acquisitions is also a noticeable trend, as larger players seek to expand their product portfolios, geographic reach, and technological capabilities, thereby offering more comprehensive solutions to their client base and solidifying market share in a competitive landscape.

Regional trends reveal that North America continues to dominate the market, largely due to high R&D expenditures by pharmaceutical and biotechnology companies, the presence of major market players, and a well-established regulatory framework that encourages the adoption of advanced clinical technologies. Europe follows suit, driven by similar factors and increasing government initiatives to support clinical research innovation. However, the Asia Pacific (APAC) region is projected to exhibit the highest growth rate during the forecast period. This accelerated growth in APAC can be attributed to the rising number of clinical trials conducted in emerging economies, increasing investments in healthcare infrastructure, a large patient pool, and lower operational costs, making it an attractive hub for global clinical research. Latin America, the Middle East, and Africa (MEA) are also showing promising growth, albeit from a smaller base, as these regions progressively adopt digital solutions to improve their clinical research capabilities and adhere to international standards, further decentralizing global clinical trial efforts.

Segment trends highlight the Electronic Data Capture (EDC) segment as the largest revenue generator, given its foundational role in collecting and managing clinical trial data efficiently and accurately. However, the Electronic Clinical Outcome Assessment (eCOA) / Electronic Patient-Reported Outcome (ePRO) segment is poised for significant growth, driven by the increasing focus on patient-centricity and the demand for real-time, high-quality patient-reported data. Cloud-based deployment models are rapidly gaining traction over on-premise solutions due to their scalability, flexibility, cost-effectiveness, and ease of access, which are critical for multi-site and global trials. Among end-users, pharmaceutical and biopharmaceutical companies remain the largest adopters, but Contract Research Organizations (CROs) are emerging as pivotal clients, as they increasingly leverage e-clinical technologies to provide advanced services to their sponsors and streamline their own operational workflows. This diverse growth across segments underscores the comprehensive evolution of the e-clinical trial ecosystem, moving towards more integrated, patient-focused, and technologically advanced solutions to meet the demands of modern drug development.

Users frequently inquire about AI's potential to revolutionize various aspects of e-clinical trials, seeking to understand how it can enhance data accuracy, accelerate timelines, and reduce costs. Common questions revolve around AI's capabilities in patient recruitment, trial design optimization, real-time data analysis for risk-based monitoring, and the development of predictive models for drug discovery and safety. Concerns often include the reliability and interpretability of AI algorithms, data privacy and security implications, the need for regulatory guidance on AI use in clinical research, and the potential for job displacement or skill gaps within the industry. Expectations are high for AI to streamline complex processes, improve decision-making through advanced analytics, and ultimately lead to more efficient and successful clinical trials, paving the way for faster access to new therapies. The emphasis is on understanding both the transformative opportunities and the practical challenges associated with integrating AI into established e-clinical workflows, ensuring that its application meets ethical, scientific, and regulatory standards.

The E-Clinical Trial Technologies Market is significantly shaped by a dynamic interplay of drivers, restraints, and opportunities, collectively known as DRO & Impact Forces. A primary driver is the escalating cost and complexity of conducting traditional clinical trials, which often involve extensive manual processes, paper-based documentation, and geographically dispersed research sites. Pharmaceutical and biotechnology companies are under immense pressure to accelerate drug development timelines while simultaneously ensuring data accuracy and regulatory compliance. E-clinical technologies offer a compelling solution by automating data collection, centralizing information, and providing real-time insights, thereby drastically reducing operational overheads, minimizing human error, and expediting the overall trial lifecycle. Furthermore, the increasing global demand for new therapeutic interventions, particularly for chronic and rare diseases, fuels greater investment in R&D, which in turn necessitates more efficient and scalable clinical research tools. Stringent regulatory requirements for data quality, traceability, and patient safety from bodies such as the FDA, EMA, and other regional authorities also serve as a significant driver, as e-clinical systems are inherently designed to meet these rigorous standards through features like audit trails and validated data entry. The paradigm shift towards patient-centric clinical trials and decentralized models, amplified by recent global health events, further pushes the adoption of technologies that enable remote monitoring, electronic consent, and virtual patient engagement, expanding the market for these innovative solutions.

Despite the strong tailwinds, the market faces several notable restraints. One significant barrier to adoption is the substantial initial investment required to implement and integrate complex e-clinical platforms. Many smaller pharmaceutical companies, biotech startups, and academic research institutions may find the upfront costs, including software licenses, hardware infrastructure, and training, prohibitive. Data security and privacy concerns also pose a major restraint. Clinical trial data, often involving highly sensitive patient information, is a prime target for cyberattacks, and any breach can lead to severe financial penalties, reputational damage, and loss of public trust. Ensuring robust cybersecurity measures and compliance with data protection regulations like GDPR and HIPAA is a continuous challenge. Furthermore, the lack of universal standardization across different e-clinical platforms and a fragmented regulatory landscape across various countries can hinder seamless data exchange and interoperability, creating integration complexities for global trials. Resistance to change from traditionalists within clinical research organizations, coupled with the need for extensive training to transition staff from legacy systems to new digital platforms, also presents an adoption hurdle, requiring significant change management efforts to overcome entrenched practices.

Opportunities within the E-Clinical Trial Technologies Market are abundant and poised to drive future growth. The emergence of new therapeutic areas, such as cell and gene therapies, precision medicine, and advanced biologics, demands highly specialized and agile clinical trial designs that can be effectively managed by advanced e-clinical solutions. These complex trials, often involving smaller, highly specific patient populations, benefit immensely from the precision and efficiency offered by digital platforms. Geographically, emerging markets in Asia Pacific, Latin America, and the Middle East and Africa present vast untapped potential. As these regions expand their clinical research infrastructure and increase their participation in global trials, the demand for e-clinical technologies is expected to surge, driven by the need to harmonize with international standards and improve local research capabilities. Moreover, the continuous advancement and integration of disruptive technologies like Artificial Intelligence (AI), Machine Learning (ML), Blockchain, and the Internet of Medical Things (IoMT) within e-clinical platforms offer significant opportunities. AI/ML can enhance patient recruitment, optimize trial design, and improve data analysis, while Blockchain can bolster data integrity and security, and IoMT devices enable real-time, continuous patient monitoring. These technological synergies promise to unlock new levels of efficiency, data quality, and insights, transforming the future landscape of clinical research and creating novel revenue streams for technology providers.

The E-Clinical Trial Technologies Market is meticulously segmented to provide a granular understanding of its diverse components, offerings, and end-user adoption patterns. This segmentation allows for a detailed analysis of market dynamics, growth drivers, and competitive landscapes across various product types, deployment models, primary end-users, and specific phases of clinical trials. Understanding these segments is crucial for stakeholders to identify niche opportunities, tailor their offerings to specific client needs, and strategically position themselves within the evolving market. The market's structure reflects the specialized requirements of clinical research, where different technological solutions address distinct challenges in data collection, trial management, patient engagement, and regulatory compliance, ensuring a comprehensive digital infrastructure for modern drug and therapy development. Each segment contributes uniquely to the overall market growth, driven by specific technological advancements, regulatory pressures, and operational efficiencies sought by clinical research stakeholders.

The value chain for the E-Clinical Trial Technologies Market is characterized by a sequential flow of activities involving various stakeholders, from the initial development of software solutions to their ultimate deployment and utilization in clinical research. The upstream segment of this value chain primarily involves technology providers, including software developers, IT infrastructure companies, and data management tool creators. These entities are responsible for conceptualizing, designing, and building the core e-clinical platforms such as EDC, CTMS, ePRO, and eTMF systems. This phase also includes the development of supporting technologies like cloud computing infrastructure, cybersecurity solutions, and advanced analytics engines. Key activities here involve extensive research and development to incorporate the latest technological advancements like AI/ML, blockchain, and mobile capabilities, ensuring that the solutions are robust, scalable, compliant with regulatory standards, and interoperable with existing systems. Partnerships with data visualization and integration specialists are common in this stage to create comprehensive and user-friendly platforms that can handle the complexities of clinical data. Talent acquisition in software engineering, data science, and clinical domain expertise is crucial for innovation in this upstream segment.

Moving downstream, the value chain encompasses the distribution channels and the ultimate end-users of these e-clinical technologies. Distribution can occur through direct sales, where technology vendors engage directly with pharmaceutical companies, CROs, and medical device manufacturers. This often involves extensive consultation, customization, implementation support, and ongoing technical maintenance. Indirect distribution channels include partnerships with system integrators, value-added resellers (VARs), and strategic alliances with other healthcare IT providers who can bundle e-clinical solutions with their broader offerings. These intermediaries often provide localized support, training, and integration services, which are critical for smooth adoption, especially in geographically diverse markets. The effectiveness of the distribution channel is heavily reliant on the sales and marketing strategies employed by the technology providers, including participation in industry conferences, digital marketing, and building strong client relationships based on trust and demonstrated efficacy of their platforms. Customer support, post-implementation services, and continuous software updates form a crucial part of maintaining customer satisfaction and fostering long-term client relationships in this competitive market.

At the very end of the value chain are the direct and indirect end-users who leverage these e-clinical trial technologies to conduct their research. Direct end-users include pharmaceutical and biopharmaceutical companies that sponsor trials, Contract Research Organizations (CROs) that execute trials on behalf of sponsors, and medical device companies developing new products. Academic and research institutions also form a significant direct end-user group, utilizing these tools for investigator-initiated studies. These organizations benefit from the enhanced efficiency, data quality, cost savings, and accelerated timelines offered by e-clinical platforms. Indirect beneficiaries include patients participating in trials, who experience improved engagement through ePRO/eCOA tools and often benefit from decentralized trial models that reduce the burden of site visits. Regulatory bodies also benefit indirectly from the improved data quality and transparency facilitated by these technologies, which streamlines the review and approval processes for new drugs and devices. The successful adoption and utilization of e-clinical technologies by these end-users depend on factors such as ease of use, scalability, integration with existing systems, robust security features, and compliance with global regulatory standards, all of which reflect back on the quality and value offered by the upstream technology providers and their distribution networks.

The E-Clinical Trial Technologies Market serves a diverse yet highly specialized clientele, all united by the common goal of advancing medical science through rigorous clinical research. The primary potential customers are pharmaceutical and biopharmaceutical companies, ranging from large multinational corporations to small and mid-sized biotech firms. These entities are at the forefront of drug discovery and development, investing heavily in clinical trials to bring new therapies to market. They leverage e-clinical platforms to manage their extensive portfolios of studies, ensure regulatory compliance across various geographies, optimize data collection, and accelerate their product pipelines. The increasing complexity of drug development, the globalization of clinical trials, and the relentless pressure to reduce costs and timelines make these companies avid adopters of advanced e-clinical solutions. Their demand spans the full spectrum of products, from comprehensive EDC and CTMS systems to specialized eTMF and pharmacovigilance software, as they seek integrated solutions to streamline their entire research process and gain a competitive edge.

Another significant segment of potential customers comprises Contract Research Organizations (CROs). CROs play a pivotal role in the clinical research ecosystem, often managing trials on behalf of pharmaceutical, biotechnology, and medical device companies. As outsourced partners, CROs are constantly seeking ways to enhance their operational efficiency, deliver high-quality data, and demonstrate value to their clients. Adopting cutting-edge e-clinical technologies allows CROs to offer more advanced services, reduce their own internal costs, improve project management, and provide real-time insights to their sponsors. For CROs, the ability to seamlessly integrate various e-clinical tools and offer flexible, scalable solutions is crucial, as they handle a diverse range of studies across multiple therapeutic areas. Their adoption patterns often reflect the demands of their clients and the need to remain competitive in a rapidly evolving service market. CROs are increasingly investing in integrated platforms that facilitate global collaboration, enhance data interoperability, and support decentralized trial models, which are becoming standard expectations from their pharmaceutical partners.

Medical device companies represent another important customer segment within the E-Clinical Trial Technologies Market. Similar to pharmaceutical companies, they conduct clinical investigations to test the safety and efficacy of new medical devices before regulatory approval and market launch. While the regulatory pathways and data types might differ slightly from drug trials, the fundamental need for efficient data capture, robust trial management, and comprehensive documentation remains the same. E-clinical technologies help medical device companies navigate complex regulatory frameworks, manage post-market surveillance studies (Phase IV), and ensure meticulous data integrity for device performance and patient outcomes. Additionally, academic and research institutions, including university medical centers and government-funded research bodies, are increasingly adopting e-clinical solutions. These institutions conduct a vast number of investigator-initiated studies and often require cost-effective, user-friendly platforms to manage their research efficiently, comply with ethical guidelines, and facilitate data sharing for scientific advancement. Their demand is often driven by the need for accessible tools that can support a wide range of study types, from small pilot studies to large-scale epidemiological research, and accommodate limited budgets while maintaining scientific rigor.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 2.8 Billion |

| Market Forecast in 2033 | USD 7.1 Billion |

| Growth Rate | 13.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Oracle Corporation, Medidata Solutions (Dassault Systèmes), Veeva Systems, IQVIA, Parexel International, Clario (formerly ERT and Bioclinica), eClinicalWorks, Clinical Data Management (CDM), Laboratory Corporation of America Holdings (LabCorp), Bio-Optronics (Clinical Conductor CTMS), MaxisIT, Biomapas, IBM Watson Health, SAS Institute, ArisGlobal, Medpace, Syneos Health, Thermo Fisher Scientific (PPD), Forte Research Systems, Realtime Clinical Systems (RCS) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The E-Clinical Trial Technologies Market is characterized by a vibrant and rapidly evolving technology landscape, constantly integrating cutting-edge innovations to meet the complex demands of modern clinical research. At its core, the widespread adoption of cloud computing platforms (Software-as-a-Service or SaaS models) has been foundational. Cloud-based solutions offer unparalleled scalability, flexibility, and accessibility, enabling global collaboration across geographically dispersed teams and facilitating the rapid deployment of systems without extensive upfront IT infrastructure investments. This not only reduces operational costs but also ensures real-time data access and centralized management, critical for managing multi-site and international trials. Mobile technologies, including dedicated applications for smartphones and tablets, are also pivotal, facilitating electronic patient-reported outcomes (ePRO), electronic clinical outcome assessments (eCOA), and remote patient monitoring, thereby enhancing patient engagement and enabling decentralized clinical trial models. These technologies are making clinical trials more patient-centric and accessible, particularly for chronic disease management and long-term follow-up studies.

Beyond the foundational elements, the integration of Artificial Intelligence (AI) and Machine Learning (ML) is rapidly transforming various facets of e-clinical trial management. AI algorithms are being employed to optimize patient recruitment by analyzing vast datasets to identify suitable candidates, improve trial design through predictive modeling, and enhance data quality by detecting anomalies and patterns in real-time. ML capabilities are crucial for risk-based monitoring, allowing sponsors and CROs to identify potential issues proactively and allocate resources more efficiently, moving away from traditional, resource-intensive monitoring approaches. Big data analytics plays a complementary role, enabling the processing and interpretation of massive volumes of diverse clinical data generated from various sources, including electronic health records, genomic data, and wearable sensors. This analytical capability is instrumental in deriving actionable insights, supporting pharmacovigilance efforts by identifying adverse event trends, and accelerating the discovery of biomarkers for targeted therapies, thereby driving precision medicine initiatives.

Emerging technologies such as the Internet of Medical Things (IoMT) and blockchain are also gaining traction within the e-clinical space. IoMT devices, including smart sensors and wearables, facilitate continuous, passive data collection from patients in real-world settings, providing richer and more frequent data points than traditional sporadic site visits. This passive data collection can significantly reduce patient burden while enhancing the ecological validity of trial outcomes. Blockchain technology, with its inherent distributed ledger and cryptographic security features, is being explored for its potential to enhance data integrity, ensure auditability, and bolster the security of clinical trial data, creating an immutable record of all transactions and changes. This could address significant concerns around data authenticity and regulatory compliance, particularly in sensitive areas like data sharing and patient consent management. Furthermore, advancements in interoperability standards and application programming interfaces (APIs) are crucial for enabling seamless data exchange between disparate e-clinical systems and external healthcare platforms, fostering a more integrated and efficient clinical research ecosystem. The continuous evolution and convergence of these technologies are key drivers for innovation and growth within the E-Clinical Trial Technologies Market, pushing the boundaries of what is possible in clinical drug and device development.

E-Clinical Trial Technologies are software and service solutions that digitalize, automate, and manage various aspects of clinical research. These encompass systems like Electronic Data Capture (EDC), Clinical Trial Management Systems (CTMS), Electronic Patient-Reported Outcomes (ePRO), and Electronic Trial Master Files (eTMF), aiming to enhance efficiency, data quality, and compliance in drug and device development.

AI significantly impacts the market by optimizing patient recruitment, enhancing trial design through predictive analytics, automating complex data analysis, improving pharmacovigilance, and facilitating risk-based monitoring. It streamlines workflows, reduces costs, and accelerates timelines, leading to more efficient and successful clinical trials by leveraging advanced data insights.

Key drivers include the escalating costs and complexity of traditional clinical trials, increasing demand for new drug discoveries, stringent regulatory requirements for data quality and safety, and the growing shift towards patient-centric and decentralized clinical trial models. Technological advancements in cloud computing and data analytics also play a crucial role.

The market is segmented by Product/Solution (e.g., EDC, CTMS, ePRO, eTMF), Deployment Model (Cloud-based, On-premise), End-user (Pharmaceutical & Biopharmaceutical Companies, CROs, Medical Device Companies), and Clinical Trial Phase (Phase I, II, III, IV), each addressing specific needs within the clinical research lifecycle.

The market is projected for robust growth, with a Compound Annual Growth Rate (CAGR) of 13.5% between 2026 and 2033, reaching an estimated USD 7.1 Billion by 2033. This growth is driven by continuous innovation, increasing digitalization in healthcare, and the imperative for more efficient drug development processes globally.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.