ID : MRU_ 433894 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

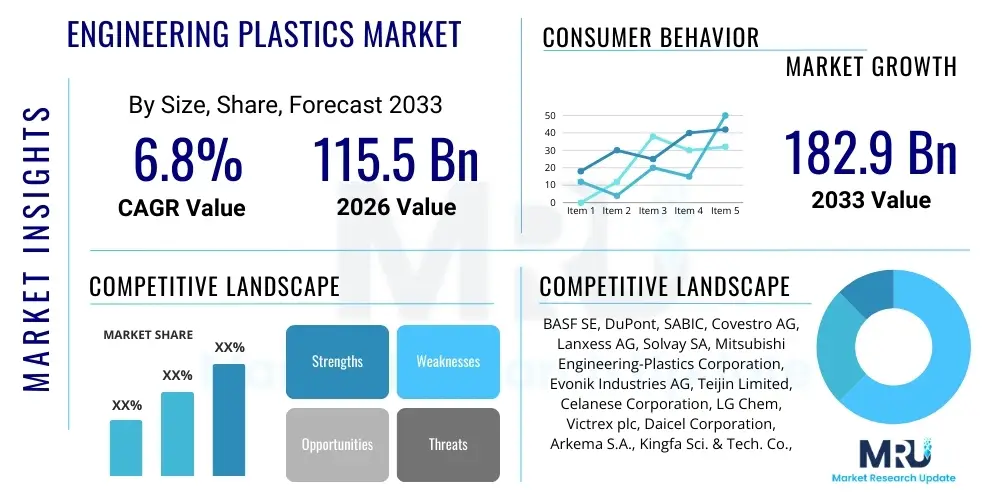

The Engineering Plastics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 115.5 Billion in 2026 and is projected to reach USD 182.9 Billion by the end of the forecast period in 2033. This substantial expansion is primarily driven by the escalating demand for lightweight, high-performance materials across critical end-use industries, particularly automotive and electronics, where conventional materials are often insufficient in meeting modern regulatory and operational requirements.

Engineering plastics are a class of polymeric materials that exhibit superior mechanical and thermal properties compared to commodity plastics, allowing them to be utilized in demanding applications requiring high stability, impact resistance, and durability. These advanced materials, including key polymers such as Polyamides (PA), Polycarbonates (PC), Acetal (POM), and Polybutylene Terephthalate (PBT), are essential components in the ongoing industrial shift towards material optimization. The inherent strength-to-weight ratio and excellent processability of engineering plastics make them indispensable for replacing heavier, traditional materials like metals and ceramics, thereby contributing significantly to efficiency gains and sustainability initiatives across numerous sectors.

Major applications of engineering plastics span several high-value sectors. In the automotive industry, they are crucial for reducing vehicle weight, enhancing fuel efficiency, and improving safety through components like under-the-hood parts, interior trim, and structural elements. The electrical and electronics sector relies heavily on these materials for housing, connectors, switches, and insulating components, due to their superior dielectric properties and fire retardancy. Furthermore, their application is expanding rapidly within the medical industry for sterilized instruments, disposable devices, and drug delivery systems, leveraging their biocompatibility and chemical resistance profiles.

The primary benefits driving market adoption include enhanced thermal stability, excellent mechanical strength, superior dimensional stability, and resistance to harsh chemical environments. These factors, combined with the continuous innovation in polymer blend technologies and compounding techniques, are sustaining high demand. Driving factors include the global focus on vehicle electrification and autonomous driving systems, which require complex, durable, and lightweight sensor housings and battery components, alongside the miniaturization trend in consumer electronics demanding materials with precise tolerance and high heat dissipation capabilities.

The Engineering Plastics Market is characterized by robust growth, fueled predominantly by technological advancements in the automotive and electrical and electronics (E&E) sectors. Key business trends indicate a strong industry focus on sustainability, leading to increased investment in bio-based and recycled engineering plastics. Manufacturers are intensely competing on performance characteristics such as flame retardancy, thermal conductivity, and enhanced mechanical properties for niche applications, particularly in advanced mobility solutions. Strategic mergers, acquisitions, and collaborations focused on supply chain stability and localized production capacity are defining the competitive landscape, aimed at optimizing cost structures and ensuring material availability amid fluctuating raw material prices.

Regionally, the Asia Pacific (APAC) region stands out as the dominant growth engine, attributed to the rapid expansion of manufacturing capabilities, particularly in China, Japan, and South Korea, which host major automotive and E&E manufacturing hubs. North America and Europe demonstrate mature market characteristics, focusing on high-value, specialized segments like aerospace, medical devices, and advanced compounding. These established regions are pioneering the transition toward circular economy models for plastics, influencing global regulatory standards and driving innovation in material recycling and recovery processes. Emerging markets in Latin America and the Middle East & Africa are showing promising potential, driven by infrastructure development and increasing domestic manufacturing output.

Segment trends reveal that the Polyamide (PA) and Polycarbonate (PC) segments remain critical contributors to market revenue, owing to their versatility and extensive use in structural applications and glazing/housing, respectively. The specialty polymers segment, encompassing Fluoropolymers and PEEK, is experiencing accelerated growth due to demand from extreme-performance environments such as aerospace and offshore energy. Application-wise, the automotive sector continues to command the largest market share, with significant growth projected in applications related to electric vehicle (EV) battery casings, thermal management systems, and interior lightweighting initiatives. This segment's growth trajectory is intrinsically linked to global mandates for CO2 emission reduction and energy efficiency.

Common user inquiries regarding AI's influence on the Engineering Plastics Market center around three key themes: optimization of manufacturing processes, acceleration of material discovery and formulation, and improvement in quality control and predictive maintenance. Users frequently ask how AI can reduce the variability in complex polymerization reactions, how machine learning algorithms can rapidly screen new filler combinations for custom polymer compounds, and what role AI plays in optimizing injection molding parameters to minimize defects. These concerns highlight a collective expectation that AI will transition plastics manufacturing from an empirically driven process to a highly data-driven, predictive, and efficient operation, ultimately leading to cost reductions and the faster introduction of novel, high-performance materials.

The application of Artificial Intelligence (AI) and machine learning (ML) models is poised to revolutionize the entire lifecycle of engineering plastics, beginning with material science research and extending through manufacturing and recycling. In research and development, AI algorithms can analyze vast chemical databases to predict the properties of untested polymer compositions, significantly accelerating the discovery of new blends optimized for specific end-use requirements, such as enhanced heat resistance or tailored mechanical resilience. This capability dramatically reduces the time and cost associated with traditional experimental trial-and-error methodologies, allowing companies to respond more swiftly to evolving market demands for specialized engineering materials.

Within the manufacturing sphere, AI is being deployed for advanced process optimization and control. ML models analyze real-time data streams from extruders, reactors, and injection molding machines—monitoring variables like temperature, pressure, flow rate, and energy consumption—to identify subtle correlations that human operators might miss. This predictive capability enables manufacturers to adjust process parameters dynamically, ensuring consistent product quality, minimizing material waste, and maximizing throughput efficiency. Furthermore, AI-driven visual inspection systems provide highly accurate, automated quality assurance, detecting microscopic defects that are critical for high-reliability components used in aerospace or medical applications, thus elevating the overall integrity of the final plastic products.

The Engineering Plastics Market is driven primarily by the sustained need for lightweighting in the transportation sector and the increasing sophistication of electrical and electronic devices. Restraints include the volatility and high cost of raw materials derived from crude oil, which often necessitates significant investment in captive polymerization facilities to maintain stable profitability. Opportunities emerge from the rapid development of bio-based engineering plastics and the implementation of advanced recycling technologies, addressing growing consumer and regulatory pressures for environmental sustainability. The key impact forces are regulatory shifts favoring stricter emission standards (pushing lightweighting) and global macroeconomic factors influencing industrial production capacity and commodity prices.

The primary drivers are foundational to the market's high growth trajectory. The push for weight reduction in vehicles—a critical requirement for improving fuel economy in Internal Combustion Engine (ICE) vehicles and extending range in Electric Vehicles (EVs)—mandates the substitution of heavy metallic parts with high-performance engineering plastics. Simultaneously, the proliferation of 5G technology, the Internet of Things (IoT), and high-density computing requires plastics that offer superior thermal management, electrical insulation, and electromagnetic interference (EMI) shielding capabilities, driving demand for specialized grades like high-performance polyamides and advanced polycarbonates. These technological requirements ensure a continuous, high-volume demand stream for advanced polymeric materials.

However, the market faces significant restraints. The dependence on petrochemical feedstocks exposes manufacturers to sharp price fluctuations, impacting production costs and profitability margins. Furthermore, the inherent complexity in processing certain high-performance engineering plastics (such as PEEK or specific PBT grades) requires specialized machinery and highly skilled labor, leading to increased capital expenditure for new entrants. Opportunities present a path for long-term strategic advantage, specifically in the realm of sustainable materials. The development of Polylactic Acid (PLA) and other bio-derived polymers, engineered to match the performance profile of traditional plastics, opens up new market avenues, especially in packaging and consumer goods where green credentials are highly valued. Advanced chemical recycling processes also offer a critical opportunity to mitigate environmental impact and secure raw material sources.

The Engineering Plastics Market segmentation provides a granular view of material utilization across various industries, categorized primarily by Material Type and End-Use Application. Analysis by material type reveals distinct performance niches, with Polyamide (PA) dominating due to its excellent balance of mechanical strength, temperature resistance, and chemical compatibility, making it a foundational material across transportation and consumer goods. Polycarbonate (PC) is essential in applications demanding high clarity, impact resistance, and optical properties, particularly in the E&E sector for display screens and housings. The application-based segmentation clearly indicates the automotive industry's continuous reliance on these materials for achieving weight reduction and enhancing component durability, making it the most critical revenue-generating sector.

Within the material segmentation, key differentiations exist based on thermal performance and cost profiles. Standard engineering plastics like PA, PC, and PBT capture the majority of the volume market, serving mass-produced components. Conversely, high-performance engineering plastics (HPEPs), including Polyphenylene Sulfide (PPS) and Polyether Ether Ketone (PEEK), occupy specialized niches requiring continuous operation at extreme temperatures (above 150°C) and resistance to highly corrosive media, critical for aerospace, energy, and medical implants. The strategic focus for manufacturers is increasingly on compounding these base resins with fillers such as glass fiber, carbon fiber, or mineral additives to create customized, highly optimized grades that meet specific dimensional and mechanical requirements for advanced applications like structural parts in aircraft or medical diagnostics equipment.

The end-use application landscape demonstrates deep penetration of engineering plastics into core industrial economies. While Automotive and E&E maintain leadership, the Construction sector is witnessing rising adoption for durable, weather-resistant structural and non-structural components, replacing wood and metal in window frames, pipes, and insulation systems. The Medical and Healthcare sector demands ultra-pure, sterilizable plastics for equipment housings and precision surgical tools, often driving innovation in high-end, low-volume materials. Understanding these segment dynamics is crucial for suppliers, as it dictates research priorities, regulatory compliance focus (especially in medical), and overall distribution strategies tailored to the unique supply chain demands of each industry.

The value chain for the Engineering Plastics Market is complex and extends from the upstream procurement of petrochemical feedstocks (e.g., benzene, propylene, ethylene) to the downstream fabrication of finished components by processors and end-users. The upstream stage involves specialized chemical producers converting basic raw materials into monomers (like caprolactam for PA or bisphenol A for PC). Midstream, the polymerization and compounding stage is critical, where major engineering plastics manufacturers synthesize the base resins and often add reinforcements, stabilizers, and colorants to create application-specific grades. The efficiency and reliability of this midstream compounding process are crucial determinants of product performance and market competitiveness.

Downstream analysis focuses on the transformation of plastic pellets into final products. This stage is dominated by specialized processors utilizing advanced techniques such as injection molding, extrusion, and blow molding, often requiring high precision and stringent quality control, especially for materials with narrow processing windows like PEEK or high-glass content composites. Distribution channels are highly structured; direct sales are common for large-volume orders to major automotive Original Equipment Manufacturers (OEMs) and Tier 1 suppliers, ensuring technical support and customized material specifications. Indirect distribution, leveraging a network of specialized plastic distributors and regional agents, serves smaller processors and specialized industrial clients, providing localized inventory and technical service for diverse application requirements.

The integrated nature of the value chain means disruptions at the feedstock level can rapidly propagate through to end-user prices and component availability. Manufacturers increasingly seek backward integration into monomer production or secure long-term, fixed-price contracts to mitigate raw material price volatility. The forward integration strategy focuses on providing pre-compounded materials or semi-finished goods, adding value before the final processing step. Successful value chain participants emphasize strong technological partnerships with processors and end-users, facilitating the co-development of new material grades optimized for cutting-edge applications, such as high-voltage insulation in EV charging infrastructure or sterile housing for next-generation medical scanners.

The primary consumers and end-users of engineering plastics are large-scale manufacturing entities across the Automotive, Electrical & Electronics, and Industrial sectors, which require materials offering high mechanical, thermal, and electrical performance beyond the capabilities of commodity polymers. Within the automotive segment, key buyers include global OEMs (such as Volkswagen, Toyota, and General Motors) and their Tier 1 suppliers (like Bosch or Continental) who purchase high volumes of PA, PBT, and PC for engine components, vehicle interiors, exterior body panels, and increasingly, battery modules and power electronics cooling systems. The shift towards sustainable mobility is fundamentally reshaping the procurement criteria for these customers, placing an emphasis on materials with verified low-carbon footprints or certified recycled content.

In the Electrical and Electronics (E&E) market, major consumers include global technology companies (e.g., Samsung, Apple, and Schneider Electric) and contract manufacturers. These customers prioritize engineering plastics based on dielectric strength, flame retardancy (meeting strict UL standards), and dimensional stability for precision parts like connectors, switches, circuit boards, and device enclosures. The continuous trend of miniaturization and increased power density necessitates materials capable of handling higher operating temperatures without degradation, driving demand for high-performance specialty polymers like PPS and PEI in critical components for 5G infrastructure and data centers.

Beyond the high-volume industrial sectors, specialized markets represent significant potential customer bases focused on niche, high-margin applications. The Medical device industry represents a customer segment demanding ultra-high purity, biocompatibility (ISO 10993 compliance), and resistance to harsh sterilization methods (like autoclaving or gamma radiation). Similarly, the Aerospace industry acts as a crucial customer for high-performance materials (such as PEEK and carbon fiber-reinforced composites) used in lightweight, flame-resistant interior parts and structural elements, where performance and safety regulations supersede cost considerations. These buyers require materials with full traceability and highly stringent quality certifications, leading to long-term supply relationships with specialized polymer manufacturers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 115.5 Billion |

| Market Forecast in 2033 | USD 182.9 Billion |

| Growth Rate | CAGR 6.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, DuPont, SABIC, Covestro AG, Lanxess AG, Solvay SA, Mitsubishi Engineering-Plastics Corporation, Evonik Industries AG, Teijin Limited, Celanese Corporation, LG Chem, Victrex plc, Daicel Corporation, Arkema S.A., Kingfa Sci. & Tech. Co., Ltd., Polyplastics Co., Ltd., Sumitomo Chemical Co., Ltd., Kuraray Co., Ltd., Asahi Kasei Corporation, RTP Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Engineering Plastics Market is focused on three main areas: advanced compounding techniques, additive manufacturing (3D printing) compatibility, and the development of sustainable, circular economy solutions. Compounding technology involves sophisticated twin-screw extrusion processes to incorporate high levels of reinforcement materials, such as long glass fiber or carbon nanotubes, into the polymer matrix. This precise control over filler dispersion is crucial for achieving the ultra-high strength and stiffness required for metal replacement applications in structural automotive parts. Manufacturers are continually refining surface treatments and coupling agents to ensure optimal adhesion between the polymer resin and the reinforcement, maximizing composite performance and durability under dynamic stress conditions.

A second crucial technological advancement lies in enhancing the processability of engineering plastics for additive manufacturing (AM). Historically, high-performance polymers like PEEK and certain polyamides were difficult to 3D print due to high melting temperatures and warping issues. Current R&D efforts are yielding specialized filament and powder forms optimized for selective laser sintering (SLS) and fused deposition modeling (FDM), enabling the creation of complex, customized tools, prototypes, and low-volume end-use parts with properties closely matching injection-molded counterparts. This technological convergence allows end-users, particularly in aerospace and medical sectors, to rapidly iterate designs and produce components with geometric complexities unattainable via traditional manufacturing methods.

Finally, technology is driving the transition towards sustainability through innovative depolymerization and purification technologies. Chemical recycling techniques, such as pyrolysis and solvent-based dissolution, are being refined to efficiently recover high-value monomers or pure polymers from mixed plastic waste streams, including challenging materials like multi-layer packaging or complex electronic housings containing engineering plastics. These technologies are crucial for closing the loop on materials like Polyamide 6 (Nylon 6) and Polyethylene Terephthalate (PET), reducing reliance on virgin feedstocks and adhering to increasingly strict regulatory mandates regarding minimum recycled content in new products. Furthermore, advancements in catalyst chemistry are vital for improving the commercial viability of bio-based monomers for sustainable PA and PC production.

The global Engineering Plastics Market exhibits significant regional variations in growth momentum, technology adoption, and end-use demand patterns. The Asia Pacific (APAC) region currently holds the largest market share and is projected to maintain the fastest growth rate throughout the forecast period. This dominance is intrinsically linked to the immense industrial output emanating from countries like China, India, and ASEAN nations, driven by colossal manufacturing bases for consumer electronics, white goods, and light vehicles. Investment in infrastructure and localized production capacity by global polymer suppliers continues to solidify APAC's position as the global hub for engineering plastics consumption and processing, focusing heavily on cost-effective, high-volume production for global supply chains.

North America and Europe represent mature yet highly specialized markets characterized by high technology integration and stringent regulatory environments. In North America, demand is concentrated in the high-performance segments, particularly aerospace, defense, and specialized medical device manufacturing, prioritizing highly engineered plastics like PEEK and PEI for mission-critical applications. European market growth is heavily influenced by the European Green Deal and associated directives, which prioritize circular economy models. Consequently, the focus in Europe is less on volume growth and more on the development and adoption of recycled and bio-based engineering plastics (rEP and bio-PA), often supported by robust legislative frameworks mandating minimum sustainable content in products.

Latin America (LATAM) and the Middle East & Africa (MEA) are emerging regions offering substantial long-term growth prospects. LATAM's market expansion is tied to the recovery and development of its automotive assembly and construction sectors, particularly in Brazil and Mexico. The MEA region, particularly the Gulf Cooperation Council (GCC) countries, benefits from significant upstream investments in petrochemical complexes, aiming to move beyond basic commodity plastics and into specialized material production. These regions are increasingly attracting foreign direct investment (FDI) into localized manufacturing, which necessitates a parallel growth in the consumption of durable, high-specification engineering materials for domestic industrialization and export markets. These emerging markets often serve as high-volume centers once localized demand justifies the establishment of regional compounding and processing facilities.

The primary driver is the global imperative for lightweighting in the transportation sector, particularly the rapid expansion of Electric Vehicles (EVs). Engineering plastics replace heavier metals, reducing vehicle weight, which directly improves energy efficiency and extends EV battery range, meeting increasingly strict global emission standards.

Engineering plastics exhibit superior performance characteristics compared to commodity plastics (like PE or PP). They offer higher mechanical strength, better thermal stability (ability to operate at higher continuous use temperatures), improved dimensional stability, and enhanced chemical resistance, making them suitable for high-stress industrial and structural applications.

The high-performance engineering plastics (HPEPs) segment, including materials like PEEK (Polyether Ether Ketone) and PEI (Polyetherimide), is projected for the highest growth. This acceleration is due to rising demand from highly regulated industries such as aerospace, medical implants, and advanced thermal management systems in electronics, which require materials operating reliably under extreme conditions.

Sustainability is a critical strategic focus. The market is increasingly prioritizing the development and adoption of bio-based engineering plastics (e.g., bio-Polyamides) and improving chemical recycling technologies to recover monomers from complex plastic waste. This shift is driven by stringent regulatory pressures, corporate sustainability targets, and consumer demand for circular materials.

Additive manufacturing (3D printing) is expanding the application scope of engineering plastics by enabling the production of highly complex, customized, and lightweight parts. Specialized PEEK and PA powders and filaments allow manufacturers to rapidly prototype and produce low-volume, high-value end-use components, accelerating product development cycles, particularly in tooling and functional prototyping.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.