ID : MRU_ 443867 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

The Amorphous Polyolefin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.8 Billion in 2026 and is projected to reach USD 2.9 Billion by the end of the forecast period in 2033.

The Amorphous Polyolefin (APO) market encompasses a specialized segment within the broader polymer industry, focusing on synthetic polymers characterized by their non-crystalline molecular structure. These polymers, typically derived from propylene, ethylene, or combinations thereof, exhibit unique properties that make them invaluable across a diverse range of industrial applications. APOs are distinguished by their low molecular weight, excellent adhesion characteristics, superior flexibility, and thermal stability, which collectively contribute to their functionality in demanding environments. Unlike their crystalline counterparts, amorphous polyolefins lack a defined melting point, instead softening over a temperature range, a characteristic that is particularly advantageous in applications requiring specific rheological properties or a broad operating window. The market for amorphous polyolefins is driven by their versatile applications and the constant demand for high-performance materials in key end-use sectors.

The product description of Amorphous Polyolefins highlights their elastomeric behavior at room temperature and their ability to form strong bonds with various substrates, including metals, plastics, and cellulosic materials. This intrinsic adhesive quality is a primary reason for their widespread adoption. Major applications of APOs include hot-melt adhesives, where they provide rapid bonding, high tack, and good substrate wetting, making them ideal for packaging, bookbinding, and hygiene products. They are also extensively utilized in sealants for construction and automotive industries, offering waterproofing and durable sealing solutions due to their flexibility and environmental resistance. Furthermore, APOs serve as effective polymer modifiers, enhancing the impact resistance, processability, and overall performance of other plastics. Their benefits extend to improved product longevity, reduced manufacturing costs through efficient application, and enhanced aesthetic appeal in finished goods.

Several critical factors are driving the expansion of the Amorphous Polyolefin market. The accelerating demand from the packaging industry, spurred by e-commerce growth and the need for efficient, secure packaging solutions, significantly propels APO consumption. The automotive sector's continuous innovation, particularly in lightweighting and improving vehicle interior aesthetics, also fuels demand for APOs in adhesives and sealants. Additionally, the construction industry's reliance on high-performance sealants and roofing materials contributes to market growth. The inherent benefits of APOs, such as their excellent moisture resistance, good dielectric properties, and chemical inertness, ensure their sustained relevance and adoption across these diverse and dynamic industrial landscapes. Moreover, ongoing research and development efforts aimed at creating more sustainable and bio-based amorphous polyolefins are expected to open new avenues for market expansion, addressing environmental concerns and catering to evolving regulatory frameworks.

The Amorphous Polyolefin market is currently experiencing robust growth, primarily fueled by significant advancements and increasing adoption across several key industrial sectors. Business trends indicate a strong emphasis on product innovation, particularly in developing APOs with enhanced thermal stability, improved adhesion to challenging substrates, and lower application temperatures to increase energy efficiency. Manufacturers are also focusing on optimizing supply chains and production processes to meet escalating demand from the packaging, automotive, and construction industries, which are the primary consumers of these versatile polymers. Strategic partnerships and collaborations between raw material suppliers and end-product manufacturers are becoming more prevalent, aimed at fostering innovation, ensuring consistent material quality, and expanding market reach. There is a discernible trend towards custom formulations that cater to specific application requirements, underscoring the market's shift towards value-added offerings rather than commodity products. Sustainability initiatives are also emerging as a critical business driver, with research into recyclable and bio-based APOs gaining momentum, reflecting a broader industry commitment to environmental stewardship and circular economy principles.

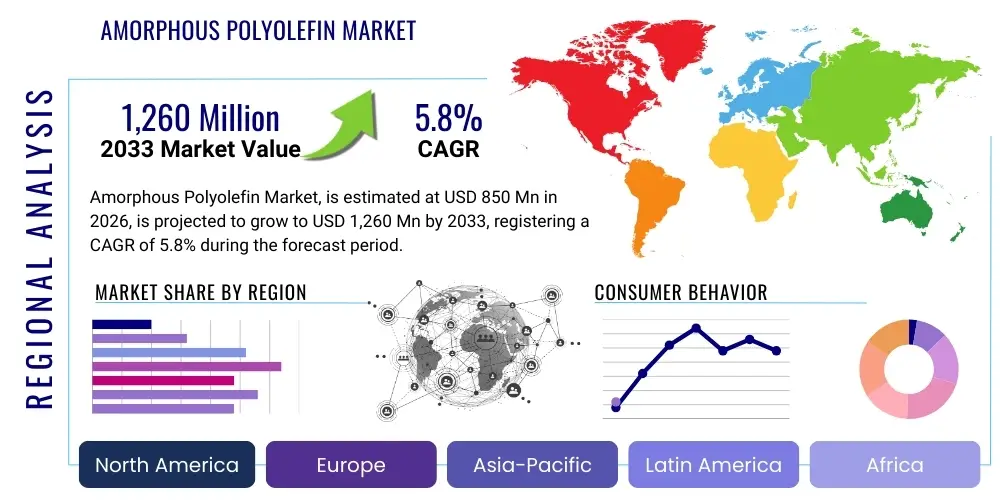

Regional trends play a pivotal role in shaping the Amorphous Polyolefin market landscape. Asia Pacific, particularly countries like China, India, and Southeast Asian nations, stands out as the largest and fastest-growing market. This growth is attributable to rapid industrialization, burgeoning manufacturing sectors, significant infrastructure development, and increasing disposable incomes driving consumer goods demand, especially in packaging and automotive. North America and Europe represent mature markets characterized by stringent regulatory environments and a strong focus on high-performance and specialty APO formulations. In these regions, demand is primarily driven by technological advancements, the adoption of sustainable materials, and innovation in niche applications such as medical devices and advanced electronics. Latin America and the Middle East & Africa are emerging as promising markets, driven by improving economic conditions, expanding industrial bases, and investments in construction and manufacturing. These regions offer substantial untapped potential for APO manufacturers looking to diversify their geographic footprint.

Segmentation trends within the Amorphous Polyolefin market reveal distinct patterns of growth and evolution across various categories. By type, propylene-based APOs continue to dominate due to their balanced properties and cost-effectiveness, though ethylene-based and co-polymer APOs are gaining traction for specific high-performance applications. In terms of applications, hot-melt adhesives remain the largest segment, driven by their indispensable role in packaging and hygiene products. However, significant growth is also observed in sealants for construction and automotive, and in polymer modification, where APOs enhance the performance and durability of other plastic materials. The end-use industries segment highlights the pervasive influence of APOs, with packaging holding the largest share, followed by automotive, construction, and increasingly, electrical and electronics, and personal care. The trend points towards a diversification of applications and a growing demand for tailor-made APO solutions that address the unique challenges and requirements of these specialized industries, pushing manufacturers to invest in research and development to maintain a competitive edge and capture emerging market opportunities. The demand for APOs in flexible packaging and durable goods continues to underpin steady growth, while nascent markets like medical adhesives present new, high-value prospects.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Amorphous Polyolefin market frequently revolve around themes of manufacturing efficiency, product development, quality control, and supply chain optimization. Key concerns include the initial investment required for AI integration, data privacy, and the need for skilled personnel to manage AI-driven systems. Users express expectations for AI to revolutionize process optimization, leading to reduced waste, lower energy consumption, and faster material characterization. There is also a strong interest in AI's potential to accelerate the discovery of novel APO formulations, predict market trends more accurately, and enable predictive maintenance in production facilities, thereby minimizing downtime and improving overall operational efficiency.

The Amorphous Polyolefin (APO) market is shaped by a complex interplay of Drivers, Restraints, Opportunities, and broader Impact Forces that dictate its growth trajectory and competitive landscape. A significant driver is the escalating demand from the packaging industry, particularly for hot-melt adhesives, fueled by the expansion of e-commerce and the need for secure, efficient, and aesthetic packaging solutions. The automotive sector's continuous innovation in lightweight materials and interior assemblies also propels APO adoption due to their superior bonding and sealing properties. Furthermore, the construction industry's reliance on high-performance sealants and roofing membranes contributes substantially to market expansion. The inherent benefits of APOs, such as excellent adhesion, flexibility, thermal stability, and moisture resistance, consistently drive their preference over traditional alternatives. Additionally, the increasing demand for polymer modification, where APOs improve the impact strength and processability of other plastics, underscores their versatile utility and market growth.

However, the market faces several restraints that could impede its growth. Volatility in the prices of raw materials, primarily crude oil and natural gas derivatives (propylene and ethylene), significantly impacts production costs and profit margins for APO manufacturers. This fluctuation makes long-term planning challenging and can lead to price instability for end-users. Intense competition from alternative polymer types, such as styrene-butadiene-styrene (SBS) and ethylene vinyl acetate (EVA) in adhesive and sealant applications, poses a constant challenge, forcing APO producers to differentiate their products through performance and cost-effectiveness. Furthermore, stringent environmental regulations regarding the use of petrochemical-based products and concerns about plastic waste can create barriers to market entry and growth, pushing manufacturers towards more sustainable, yet often more expensive, alternatives. The need for specialized processing equipment and technical expertise for APO application can also act as a restraint, particularly for smaller enterprises.

Despite these challenges, numerous opportunities are poised to drive the Amorphous Polyolefin market forward. The emergence of new applications in niche sectors, such as medical devices, electronics encapsulation, and specialized industrial tapes, presents significant growth avenues for high-performance APO grades. The ongoing development of bio-based or partially bio-based amorphous polyolefins addresses environmental concerns and aligns with global sustainability trends, potentially unlocking new markets and customer segments seeking eco-friendly solutions. Growth in developing economies, particularly in Asia Pacific and Latin America, characterized by rapid industrialization, infrastructure development, and rising consumer spending, offers vast untapped market potential. Technological advancements in polymerization techniques leading to novel APO structures with enhanced properties, such as improved clarity, higher service temperatures, or better chemical resistance, will also create new market demands. Beyond these, broader impact forces such as technological advancements, geopolitical stability, and evolving consumer preferences for durable and high-quality products continuously shape the market. Supply chain disruptions, often caused by global events, can temporarily impact raw material availability and logistics, highlighting the need for resilient supply networks. The increasing emphasis on circular economy principles and product lifecycle management is also becoming an influential force, encouraging innovation in material recovery and recycling solutions for APOs.

The Amorphous Polyolefin market is comprehensively segmented to provide a detailed understanding of its diverse applications, product types, and end-use industries. This segmentation is crucial for market participants to identify lucrative niches, develop targeted strategies, and address specific customer needs effectively. The primary categories for segmentation typically include product type, application, and end-use industry, each offering unique insights into the market's structure and growth dynamics. Understanding these distinct segments allows for a granular analysis of competitive landscapes, regional consumption patterns, and technological advancements tailored to specific market demands. The versatility of amorphous polyolefins enables their penetration across a wide array of sectors, driving the need for such detailed categorization.

The value chain for the Amorphous Polyolefin market begins with the upstream segment, primarily involving the extraction and processing of petrochemical feedstocks. This stage is dominated by large chemical companies and oil & gas corporations that produce monomers such as propylene, ethylene, and butene from crude oil and natural gas. These basic chemical building blocks are then supplied to polymer manufacturers. The quality, availability, and price stability of these raw materials are critical determinants of profitability and production efficiency for APO manufacturers. Upstream suppliers invest heavily in refining and petrochemical cracking technologies to produce high-purity monomers, often operating at a global scale to leverage economies of scale and optimize logistics. Any disruption in this segment, such as geopolitical events affecting oil prices or natural disasters impacting production facilities, can have cascading effects throughout the entire value chain, leading to price volatility and supply shortages for downstream players. Moreover, the environmental impact of feedstock extraction and processing is under increasing scrutiny, driving efforts towards more sustainable sourcing and production methods among upstream participants.

Moving downstream, the value chain encompasses the polymerization process where these monomers are converted into amorphous polyolefins. This stage involves specialized chemical manufacturing facilities equipped with advanced reactors and catalysis technologies to control the molecular structure and properties of the APOs. Key manufacturers in this segment differentiate themselves through proprietary polymerization technologies, unique product formulations, and the ability to produce a wide range of APO grades tailored to specific application requirements. Post-production, APOs are processed into various forms such as pellets, crumbs, or hot-melt sticks, which are then packaged and prepared for distribution. This segment focuses on quality control, ensuring that the physical and chemical properties of the APOs meet stringent industry standards for consistency and performance. Investments in research and development are crucial at this stage to innovate new APO products with improved performance characteristics, sustainability profiles, and cost-effectiveness, thereby meeting evolving customer demands and expanding market applications. The technical expertise required for this stage often creates significant barriers to entry for new market players.

The distribution channel for Amorphous Polyolefins is a complex network involving both direct and indirect sales. Direct distribution typically involves APO manufacturers selling directly to large-volume end-users, such as major packaging companies, automotive manufacturers, or construction firms, who have established procurement relationships and require customized technical support. This channel allows for closer customer relationships, direct feedback loops for product improvement, and often results in larger, long-term contracts. In contrast, indirect distribution involves a network of distributors, agents, and specialty chemical suppliers who cater to smaller and medium-sized enterprises (SMEs) or those requiring smaller quantities. These intermediaries provide local stockholding, logistics services, and technical assistance, bridging the gap between manufacturers and diverse end-users. They play a vital role in market penetration, especially in regions with fragmented demand or complex regulatory landscapes. The choice between direct and indirect channels often depends on market size, geographic reach, customer type, and the level of technical support required. Both channels are critical for ensuring widespread market access and efficient delivery of APO products to their diverse range of end-users across various industries globally.

The potential customers for Amorphous Polyolefins are incredibly diverse, spanning numerous industries due to the versatile properties and applications of these polymers. At the forefront are major players in the packaging industry, including manufacturers of corrugated boxes, flexible packaging, labels, and tapes. These companies rely heavily on APO-based hot-melt adhesives for efficient, high-speed assembly lines, ensuring secure sealing and robust product integrity for everything from food and beverage containers to consumer goods and e-commerce parcels. The need for rapid setting times, strong adhesion to various substrates, and cost-effectiveness makes APOs an indispensable component for these end-users. Furthermore, the hygiene product sector, comprising manufacturers of disposable diapers, sanitary napkins, and adult incontinence products, represents a significant customer base, leveraging APOs for their excellent non-toxic adhesion and flexibility, which are critical for comfort and performance in personal care items. These customers often require specialized APO formulations that can withstand various environmental conditions and provide consistent performance throughout the product's lifecycle.

Another substantial segment of potential customers is found within the automotive industry. Vehicle manufacturers and their tier-1 suppliers utilize amorphous polyolefins extensively in various applications, including interior trim assembly, headliner bonding, carpet lamination, and exterior body panel sealing. The demand for lightweighting in vehicles to improve fuel efficiency and reduce emissions drives the adoption of advanced adhesives and sealants, where APOs excel due to their strong bonding capabilities, vibration dampening properties, and resistance to environmental factors like temperature extremes and moisture. Furthermore, APOs are employed in sound insulation and anti-flutter applications, contributing to overall vehicle quality and passenger comfort. Manufacturers in the construction industry also form a critical customer group, using APO-based sealants for roofing membranes, window and door insulation, pipe wrapping, and flooring adhesives. The demand for durable, weather-resistant, and flexible sealing solutions in building and infrastructure projects ensures a steady demand for these polymers. These customers prioritize long-term performance, ease of application, and compliance with stringent building codes and environmental standards.

Beyond these major sectors, a wide array of other industries represent significant potential customers for amorphous polyolefins. Companies involved in polymer modification, seeking to enhance the properties of other plastics such as polypropylene or polyethylene, frequently utilize APOs to improve impact strength, flexibility, and overall processing characteristics. This includes manufacturers of automotive components, consumer electronics casings, and durable goods. The electrical and electronics sector uses APOs for cable filling compounds, encapsulation of sensitive components, and as protective coatings where excellent dielectric properties and moisture resistance are paramount. Additionally, manufacturers of furniture, footwear, textiles, and various industrial assembly products also form a diverse customer base, leveraging APOs for their versatile bonding, sealing, and coating capabilities. As industries continue to innovate and demand high-performance, cost-effective, and increasingly sustainable material solutions, the customer base for amorphous polyolefins is expected to expand into new and specialized applications, driven by ongoing research and development efforts to tailor APO properties for specific niche requirements.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 2.9 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Eastman Chemical Company, Sasol Limited, Evonik Industries AG, Renkert Oil, Inc., Borealis AG, Chevron Phillips Chemical Company LLC, ExxonMobil Chemical Company, LyondellBasell Industries N.V., SABIC, Versalis S.p.A., Braskem S.A., TotalEnergies, Reliance Industries Limited, PTT Global Chemical Public Company Limited, LG Chem, Formosa Plastics Corporation, INEOS, Sinopec Corp., China National Petroleum Corporation (CNPC) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Amorphous Polyolefin market is characterized by a dynamic technology landscape, driven by continuous innovation aimed at enhancing product performance, improving manufacturing efficiency, and addressing sustainability concerns. A foundational technology involves advanced polymerization techniques, primarily utilizing Ziegler-Natta or metallocene catalysts. Metallocene catalysts, in particular, enable more precise control over polymer architecture, leading to APOs with narrower molecular weight distributions, improved thermal stability, and enhanced adhesive properties. This catalytic precision allows manufacturers to tailor APOs for specific application requirements, such as high-temperature resistance in automotive adhesives or improved low-temperature flexibility in packaging sealants. Ongoing research in catalyst development is focused on achieving even greater selectivity and activity, reducing catalyst residues, and enabling the use of a wider range of monomers, which ultimately expands the functional scope of APOs and reduces production costs. The ability to fine-tune crystallinity and molecular weight through these advanced polymerization methods is crucial for meeting the diverse demands of end-use industries.

Beyond polymerization, processing technologies play a critical role in optimizing the application and performance of amorphous polyolefins. Hot-melt adhesive formulation technology is particularly advanced, involving the precise blending of APOs with tackifiers, waxes, antioxidants, and other additives to achieve desired adhesion characteristics, open times, set times, and viscosity profiles. Innovations in this area include the development of reactive hot-melt systems that offer even stronger bonds and improved environmental resistance, as well as formulations designed for lower application temperatures to reduce energy consumption and improve worker safety. Furthermore, extrusion and compounding technologies are essential for converting raw APO pellets into various forms suitable for end-use, such as films, sheets, or specific adhesive sticks. These technologies focus on efficient melting, mixing, and shaping while preserving the desired properties of the APOs. Automation and process control systems are increasingly integrated into these manufacturing steps to ensure consistent quality, minimize waste, and enhance overall operational efficiency, directly impacting the market's competitiveness and growth potential.

The technological landscape also reflects a growing emphasis on sustainability and product lifecycle management. Research and development efforts are increasingly directed towards developing bio-based or partially bio-based amorphous polyolefins, leveraging renewable feedstocks to reduce reliance on petrochemicals and lower the carbon footprint of APO products. This involves exploring new monomer sources derived from biomass or waste streams, as well as developing green polymerization techniques. Additionally, technologies related to recycling and circularity are gaining prominence. This includes innovations in material recovery processes for APO-containing products, as well as designing APO formulations that are compatible with existing recycling streams or are inherently biodegradable under specific conditions. Furthermore, advanced analytical techniques such as spectroscopy, chromatography, and rheology are continually evolving to provide deeper insights into APO structure-property relationships, enabling faster characterization, quality control, and the development of next-generation materials. These technological advancements collectively contribute to making amorphous polyolefins more versatile, sustainable, and capable of addressing complex industrial challenges, thereby maintaining their relevance and fostering future market expansion.

Amorphous Polyolefins (APOs) are non-crystalline synthetic polymers derived from propylene, ethylene, or their co-polymers. Key characteristics include excellent adhesion, superior flexibility, thermal stability, and low molecular weight. Unlike crystalline polymers, APOs soften over a temperature range rather than exhibiting a sharp melting point, making them highly versatile in various applications.

The largest consumers of Amorphous Polyolefins are the packaging industry, primarily for hot-melt adhesives in sectors like e-commerce and consumer goods, and the automotive industry, where APOs are crucial for bonding, sealing, and lightweighting components. The construction sector also represents a significant end-user for sealants and roofing materials.

Market growth for Amorphous Polyolefins is primarily driven by increasing demand from the packaging and automotive sectors due to their superior adhesive and sealing properties, the continuous need for polymer modification, and the rising adoption in emerging applications. The inherent benefits like flexibility, thermal stability, and moisture resistance further fuel their demand.

Key challenges for APO manufacturers include the volatility in raw material prices (propylene, ethylene), intense competition from alternative polymers such as EVA and SBS, and stringent environmental regulations that necessitate investments in sustainable production methods and bio-based alternatives. Specialized processing requirements also pose a barrier.

Asia Pacific is the largest and fastest-growing market for Amorphous Polyolefins, driven by rapid industrialization, burgeoning manufacturing sectors, significant infrastructure development, and increasing consumer demand in countries like China and India. Its robust economic growth and expanding middle-class populations fuel widespread adoption across packaging, automotive, and construction industries.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.