ID : MRU_ 442568 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

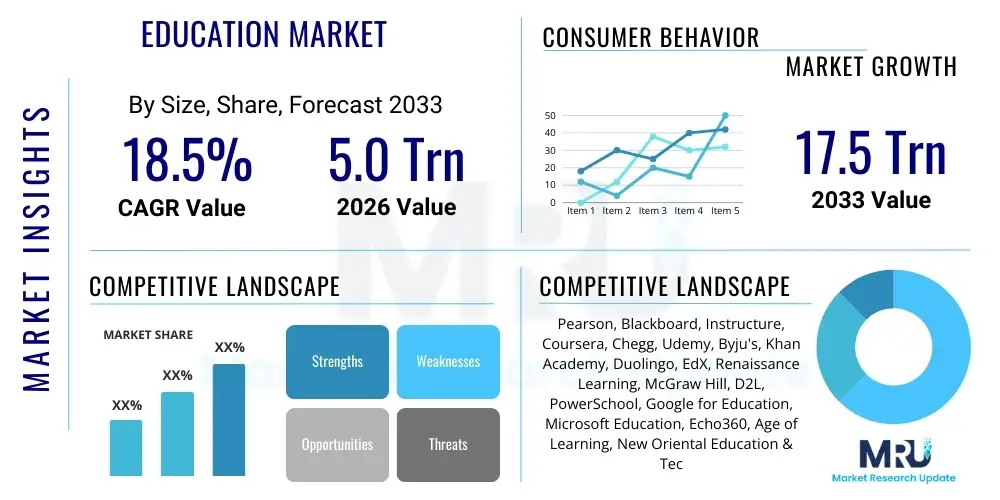

The Education Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 4.5 Trillion in 2026 and is projected to reach USD 10.2 Trillion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating global demand for flexible, personalized, and technology-integrated learning solutions, coupled with increased government and private sector investment in skill development initiatives across emerging economies. The market scope encompasses traditional educational institutions, corporate training platforms, and the rapidly growing segment of EdTech platforms focusing on lifelong learning and professional certification.

The Education Market encompasses all services, products, and technologies utilized for teaching, learning, and administrative functions across academic and professional settings globally. Products range from physical infrastructure and curriculum content to advanced digital learning management systems (LMS), massive open online courses (MOOCs), and immersive reality tools. Major applications span K-12 schooling, higher education, vocational training, and corporate upskilling programs. The primary benefit derived is the enhanced accessibility and personalization of educational content, leading to improved learning outcomes and career readiness. Key driving factors include widespread internet penetration, favorable demographic shifts in developing nations, and continuous technological advancements, particularly in artificial intelligence and cloud computing, which are reshaping instructional delivery models and administrative efficiencies. Furthermore, the increasing necessity for continuous professional development due to rapid industrial transformation mandates robust educational infrastructure, thereby fueling market growth across all demographic segments.

The global Education Market is characterized by vigorous digital transformation and shifting consumption patterns, favoring hybrid and fully online models. Key business trends indicate a strong move toward platform consolidation, where large EdTech providers acquire smaller, specialized solution developers to offer integrated ecosystem services, creating comprehensive learning environments that cater to diverse stakeholder needs, from institutional administration to individualized student tutoring. Regionally, the Asia Pacific (APAC) region stands out as the primary growth engine, propelled by enormous demographic size, rising disposable incomes, and intensive governmental focus on improving educational quality and accessibility in large economies such as India and China. Conversely, mature markets in North America and Europe are concentrating on advanced technological integration, focusing on data analytics and adaptive learning solutions to optimize institutional resource allocation and student performance metrics. Segment-wise, the corporate training segment is exhibiting the highest growth CAGR, driven by the imperative for workforce reskilling and upskilling in response to automation and the adoption of advanced technologies across nearly all industrial sectors, establishing continuous learning as a critical component of modern organizational strategy.

User queries regarding the impact of Artificial Intelligence (AI) in the Education Market overwhelmingly center on personalized learning pathways, the automation of administrative tasks, and the ethical implications concerning data privacy and algorithmic bias in student assessment. Common expectations highlight AI's ability to create highly individualized educational experiences that adapt content pace and style based on real-time student performance data, addressing the long-standing challenge of heterogeneous classroom learning speeds. Conversely, concerns frequently revolve around the potential displacement of human educators, the necessary investment in robust data infrastructure to support AI models, and ensuring equitable access to these sophisticated technologies across different socio-economic strata. The primary thematic convergence suggests that stakeholders are keen on AI's role in augmenting human teaching capacity—handling repetitive tasks and diagnostics—rather than replacing the essential human element of mentorship and critical thinking development. This dual focus on efficiency gains and pedagogical transformation underpins the current innovation trajectory in EdTech, necessitating careful policy formulation to maximize benefits while mitigating inherent technological risks.

The Education Market growth trajectory is fundamentally propelled by powerful drivers, including the globalization of educational standards and the imperative for continuous workforce retraining, catalyzed by rapid technological obsolescence. These growth forces, however, are moderated by significant restraints, primarily the high initial implementation cost associated with advanced digital infrastructure and security concerns related to massive collections of sensitive student data, particularly in regions with fragmented regulatory frameworks. Opportunities abound in the burgeoning demand for specialized vocational and professional certification programs that bypass traditional degrees, offering faster entry into high-demand careers, alongside the expansion of affordable, accessible EdTech solutions targeting low-income and rural populations. The key impact forces driving immediate market shifts include the post-pandemic acceleration of digital adoption across all educational tiers, necessitating robust cloud infrastructure and sophisticated cybersecurity protocols, and the increasing competitive intensity from non-traditional education providers who leverage technology to disrupt conventional academic models through micro-credentials and skill-focused bootcamps, placing persistent pressure on established institutions to innovate rapidly and effectively.

The Education Market is highly fragmented, necessitating detailed analysis across several critical dimensions to accurately capture its evolving dynamics and consumption patterns. Segmentation by Component includes hardware, software, and services, reflecting the shift toward integrated technology solutions. By Sector, the market is divided into academic (K-12, Higher Education) and non-academic (Corporate, Professional Development, Vocational). The deployment model distinction between on-premise and cloud-based solutions is increasingly favoring cloud infrastructure due to its scalability and accessibility, while geographical segmentation reveals distinct maturity levels and investment priorities across major global regions. Understanding these structural subdivisions is essential for strategic planning, enabling market participants to focus resources on the highest-growth areas, such as cloud-native learning management systems and specialized corporate upskilling platforms tailored for high-tech industries.

The value chain of the Education Market starts with upstream activities dominated by content creators and foundational technology providers, including textbook publishers, curriculum developers, and core software infrastructure firms specializing in cloud services and advanced AI/ML algorithms. These entities are responsible for generating the intellectual property and technical frameworks that underpin modern educational delivery. Midstream, the primary focus shifts to aggregation and distribution, encompassing Learning Management System (LMS) providers, digital platform operators, and educational technology integrators who package core content and software into deployable solutions for institutions or direct consumers. This middle layer plays a crucial role in ensuring interoperability and ease of access across diverse device types and regulatory environments, often involving complex partnerships between content holders and platform builders.

Downstream activities center on the delivery and consumption of educational services, involving traditional schools, universities, corporate training departments, and direct-to-consumer tutoring services. The final stage of the value chain involves feedback and assessment loops, where data collected on learning outcomes and system usage informs upstream content refinement and technology upgrades. Distribution channels are highly varied, ranging from direct sales models to institutional procurement frameworks, supplemented significantly by indirect channels such as educational resellers, global system integrators, and independent consulting firms specializing in EdTech implementation, all contributing to the pervasive adoption of new learning tools and methodologies.

The integration of technology has drastically streamlined the distribution process; for digital content and services, indirect channels like online marketplaces and global cloud vendor platforms are increasingly dominant, allowing smaller specialized providers to reach vast global audiences without requiring extensive physical infrastructure. Conversely, infrastructure components and customized institutional solutions still rely heavily on direct sales engagements and long-term service contracts. Understanding the power dynamics between upstream content providers, who often hold proprietary knowledge, and downstream service providers, who own the critical relationship with the end-user, is vital for predicting market shifts and identifying strategic partnership opportunities within this highly interconnected ecosystem.

Potential customers within the Education Market are segmented into three primary categories: Institutional Buyers, Corporate Entities, and Individual Learners, each with distinct needs and procurement requirements. Institutional Buyers constitute the largest traditional segment, encompassing public and private K-12 schools, higher education universities, and vocational colleges, primarily seeking comprehensive solutions such as Student Information Systems (SIS), Learning Management Systems (LMS), and large-scale digital content licenses. Their procurement cycles are often long and bureaucratic, heavily influenced by government funding, accreditation standards, and demonstrated return on investment (ROI) in terms of improved student outcomes and administrative efficiency. Corporate Entities, including large multinational corporations and small-to-medium enterprises (SMEs), form the rapidly growing non-academic segment, focused on continuous professional development, compliance training, and strategic upskilling programs to maintain competitive advantage in evolving technological landscapes. These buyers prioritize scalable, modular, and measurable learning solutions, often favoring custom content and micro-credential certifications linked directly to performance metrics and business goals, driving high demand for specialized B2B EdTech platforms.

Individual Learners represent the final, yet increasingly influential, segment, driven by the personal desire for lifelong learning, career transitions, or supplementary academic support. This segment interacts directly with platforms offering Massive Open Online Courses (MOOCs), subscription-based language learning apps, private tutoring services, and certification courses provided by non-institutional entities. Their purchasing decisions are highly sensitive to pricing, user experience (UX), brand reputation, and the perceived value of the credential or skill acquired. The rise of direct-to-consumer EdTech models, leveraging social media and personalized marketing, has made this segment critical for companies focusing on niche skills and non-traditional credentials. The convergence of these segments means that successful market players must offer adaptable products that can satisfy the rigorous demands of institutional procurement while maintaining the intuitive, high-value experience expected by individual consumers seeking immediate skill application and career advancement.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Trillion |

| Market Forecast in 2033 | USD 10.2 Trillion |

| Growth Rate | 12.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Pearson plc, BlackBoard Inc., Instructure Holdings, Coursera, Udemy, Microsoft (Education Division), Google for Education, BYJU'S, Chegg, 2U Inc., Duolingo, D2L Corporation, McGraw Hill, PowerSchool, SAP (LMS Solutions), Renaissance Learning, Skillsoft, Stride, K12 International, EdX (part of 2U). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Education Market is undergoing a rapid technological convergence, centered around cloud computing, artificial intelligence, and immersive technologies, fundamentally altering how content is delivered and consumed. Cloud computing serves as the indispensable backbone, providing scalable infrastructure necessary for hosting large Learning Management Systems (LMS), enabling real-time collaboration tools, and facilitating access to extensive digital libraries, ensuring seamless connectivity and operational resilience for global educational ecosystems. The adoption of Software as a Service (SaaS) models for educational software has minimized capital expenditure for institutions while guaranteeing continuous updates and robust security, making complex tools accessible even to resource-constrained environments, thereby democratizing access to high-quality administrative and instructional technology across diverse geographic locations.

Artificial Intelligence (AI) and Machine Learning (ML) are the primary drivers of personalized learning, utilizing sophisticated algorithms to analyze student performance data, identify knowledge gaps, and dynamically adjust curriculum presentation and difficulty. This ranges from intelligent tutoring systems that provide immediate, individualized feedback to predictive analytics used by institutions to manage student retention and optimize resource allocation based on anticipated enrollment trends and academic risk factors. Furthermore, the integration of these technologies into assessment tools is moving testing away from standardized, summative evaluations toward continuous, formative assessments, offering deeper insights into cognitive processes and subject mastery, thereby ensuring that educational interventions are timely and highly targeted.

Immersive technologies, specifically Virtual Reality (VR) and Augmented Reality (AR), are transforming experiential learning, particularly in fields requiring high-fidelity simulations such as medicine, engineering, and vocational trades. VR allows students to practice complex procedures in a risk-free environment, while AR overlays digital information onto real-world settings, enhancing classroom instruction and field research. Blockchain technology is also emerging as a critical component for ensuring the security, verifiability, and immutability of academic records and professional credentials, addressing the growing need for trust in global talent acquisition. The collective integration of these advanced technologies is defining the competitive landscape, rewarding providers who can successfully weave together data analytics, personalized delivery, and immersive experiences into coherent, impactful learning platforms that deliver demonstrable value for both institutional and individual end-users.

The primary driver is the necessity for scalable, personalized learning experiences, accelerated by the global shift to hybrid models following the pandemic. Furthermore, technological advancements in AI, coupled with increased accessibility via mobile devices and widespread internet penetration, enable cost-effective content delivery beyond traditional geographic boundaries, fueling both academic and corporate adoption.

AI is transforming assessment by moving from summative grading to continuous, formative evaluation. Intelligent tutoring systems provide immediate, constructive feedback personalized to the student’s learning style, automating the scoring of complex assignments, identifying learning deficiencies in real-time, and significantly enhancing instructional efficiency for educators.

The Asia Pacific (APAC) region is projected to exhibit the highest growth potential, primarily due to its vast, underserved student population, aggressive governmental policies supporting digitalization of schools, and the high demand for supplemental learning and test preparation resources fueled by rising middle-class disposable incomes, particularly in countries like India and China.

Major restraints include the substantial initial capital investment required for robust digital infrastructure and high-speed connectivity, particularly in developing economies. Additionally, significant concerns remain regarding data privacy and the security of sensitive student information, alongside institutional resistance to pedagogical change and the necessity for comprehensive digital literacy training for faculty and administrative staff.

The shift is highly significant, reflecting a growing market demand for immediate, job-relevant skills over lengthy degree programs. Micro-credentials, often provided by corporate or non-traditional platforms, offer flexible, measurable pathways for rapid upskilling and reskilling, directly addressing the dynamic workforce needs caused by technological disruption and ensuring lifelong employability for individual learners worldwide.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.