ID : MRU_ 444449 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

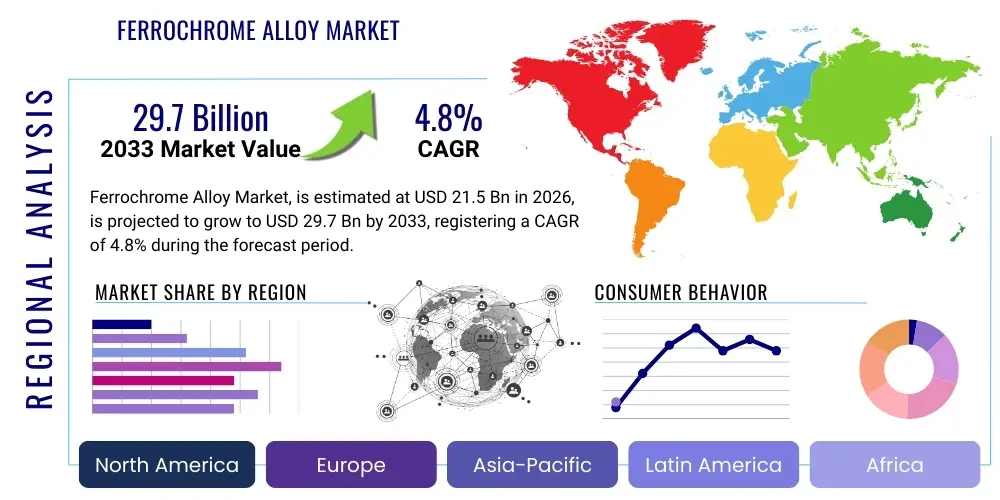

The Ferrochrome Alloy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.9% between 2026 and 2033. The market is estimated at USD 25.8 Billion in 2026 and is projected to reach USD 36.3 Billion by the end of the forecast period in 2033. This growth is primarily driven by the escalating demand from the stainless steel industry, which relies heavily on ferrochrome for its corrosion resistance and strength properties. Global industrialization, particularly in emerging economies, alongside significant investments in infrastructure and the automotive sector, continues to fuel the expansion of this essential alloy market. The market's trajectory is also influenced by advancements in smelting technologies and an increasing focus on sustainable production practices, aiming to enhance efficiency and reduce environmental impact across the value chain. As global manufacturing scales up, the indispensable role of ferrochrome in high-performance applications ensures its sustained market growth.

The Ferrochrome Alloy Market encompasses the global production, distribution, and consumption of ferrochrome, an alloy of chromium and iron, characterized by its high melting point, exceptional hardness, and superior corrosion resistance. This critical material is primarily utilized as a key ingredient in the production of stainless steel, imparting its distinctive properties and enabling a wide range of applications. Beyond stainless steel, ferrochrome finds significant use in the manufacturing of various specialized alloys, including tool steels, high-strength low-alloy steels, and some cast iron varieties, contributing to the durability and performance of numerous industrial products. The primary benefits of ferrochrome include enhancing steel's hardenability, wear resistance, and high-temperature strength, making it indispensable in industries requiring robust and resilient materials. Major applications span across construction, automotive manufacturing, machinery, consumer goods, and the burgeoning renewable energy sector. Key driving factors for the market's expansion include the escalating global demand for stainless steel, driven by rapid urbanization and infrastructure development, particularly in Asia-Pacific economies, coupled with increasing production volumes in the automotive and industrial machinery sectors. Additionally, technological advancements in ferrochrome production, focusing on energy efficiency and environmental sustainability, further support market growth by optimizing operational costs and meeting stringent regulatory standards.

The Ferrochrome Alloy Market is experiencing robust expansion, propelled by sustained demand from its primary end-use sectors, particularly stainless steel manufacturing. Current business trends indicate a strategic focus on consolidation among key players, aiming to enhance economies of scale and optimize resource utilization, alongside increasing investments in advanced smelting technologies to improve efficiency and reduce carbon footprint. The market is witnessing a shift towards more sustainable production methods, including the exploration of ferrochrome recycling and the adoption of cleaner energy sources, driven by stringent environmental regulations and corporate social responsibility initiatives. From a regional perspective, Asia-Pacific, led by China and India, remains the dominant force, accounting for the largest share of both production and consumption dueorapid industrialization, extensive infrastructure projects, and a booming manufacturing sector. Europe and North America exhibit stable demand, with a greater emphasis on high-quality and specialty ferrochrome grades for advanced applications, while emerging markets in Latin America and Africa present significant untapped potential for future growth. Segmentation trends highlight a consistent demand for high carbon ferrochrome, the most widely used grade in stainless steel, though there is a growing interest in low and medium carbon ferrochrome for specialty alloys requiring precise metallurgical properties. The interplay of raw material price volatility, energy costs, and evolving trade policies significantly influences market dynamics, necessitating adaptive strategies from market participants to maintain competitive advantage and secure supply chains globally.

The integration of Artificial Intelligence (AI) across the ferrochrome alloy market is generating significant interest and expectations, primarily centered around enhancing operational efficiency, improving product quality, and optimizing complex supply chain logistics. Users are keen to understand how AI can revolutionize traditional smelting processes, moving towards predictive maintenance to minimize downtime, optimizing energy consumption to reduce high operational costs, and improving raw material utilization for greater sustainability. There is a strong expectation that AI will provide advanced analytics for market forecasting, enabling better inventory management and more agile response to demand fluctuations and raw material price volatility. Furthermore, concerns are often raised regarding the initial investment costs for AI implementation, the need for skilled personnel to manage these advanced systems, and data security, alongside the potential for job displacement in traditional roles. Nevertheless, the overarching sentiment is that AI holds immense potential to drive unprecedented levels of productivity, precision, and environmental stewardship within the ferrochrome industry, transforming it into a more resilient and technologically advanced sector, capable of addressing future challenges more effectively.

The Ferrochrome Alloy Market is significantly shaped by a dynamic interplay of Drivers, Restraints, and Opportunities, which collectively constitute its Impact Forces. Primary drivers for market growth include the relentless expansion of the global stainless steel industry, which consumes the vast majority of ferrochrome, propelled by increasing urbanization, infrastructure development, and industrialization across emerging economies. Additionally, the automotive and construction sectors' persistent demand for high-strength, corrosion-resistant materials further stimulates ferrochrome consumption. Conversely, the market faces notable restraints such as the inherent volatility in raw material prices, particularly chrome ore and electricity, which are major cost components in ferrochrome production. Stringent environmental regulations aimed at curbing carbon emissions and promoting sustainable mining practices also pose challenges, requiring substantial investments in cleaner technologies. Opportunities for market players arise from the burgeoning demand in developing nations, advancements in smelting technologies that promise greater efficiency and reduced environmental impact, and the potential for recycling ferrochrome to establish a more circular economy. The impact forces are thus a complex web of economic growth influencing demand, regulatory pressures dictating operational parameters, and technological innovations opening new avenues for sustainable and efficient production methods. Geopolitical events and trade policies also exert considerable influence, shaping global supply chains and market accessibility, demanding robust risk management strategies from industry stakeholders to navigate these evolving landscapes.

The Ferrochrome Alloy Market is meticulously segmented across various parameters, offering a granular view of its diverse dynamics and demand patterns. These segmentations are crucial for understanding market specificities, identifying lucrative niches, and formulating targeted strategies. The market is primarily bifurcated by type of ferrochrome, application in end-use industries, and geographical region, each revealing distinct growth trajectories and competitive landscapes. Different grades of ferrochrome, categorized by their carbon content, cater to specific metallurgical requirements, with high carbon ferrochrome dominating due to its widespread use in stainless steel, while low and medium carbon grades serve more specialized applications requiring precise control over carbon levels. The application segment details the consumption patterns across key industries, highlighting the overwhelming reliance of the stainless steel sector but also recognizing the significant contributions from the automotive, construction, and machinery industries. Regional segmentation underscores the geographical distribution of both production capabilities and consumption centers, reflecting global economic shifts and industrial development.

A comprehensive Value Chain Analysis for the Ferrochrome Alloy Market highlights the intricate series of activities from raw material extraction to final product consumption, revealing key operational dependencies and value-addition points. The upstream segment of the value chain is dominated by the mining and beneficiation of chromite ore, the primary raw material for ferrochrome. This stage involves exploration, extraction, crushing, grinding, and concentration of chromite to produce a marketable ore concentrate. Key players in this segment are typically large mining corporations located in chromite-rich regions like South Africa, Kazakhstan, and India. Following chromite ore, the midstream phase involves the smelting of chromite ore with reductants (such as coke or anthracite) in electric arc furnaces to produce ferrochrome. This energy-intensive process requires significant capital investment and technological expertise, with major producers often integrating backward into mining or having long-term supply agreements. The downstream segment encompasses the distribution and sales of ferrochrome alloys to various end-user industries, predominantly stainless steel manufacturers, foundries, and specialized alloy producers. Distribution channels for ferrochrome are multifaceted, involving both direct sales from producers to large industrial consumers through long-term contracts and indirect sales via a network of traders, distributors, and agents who cater to smaller or regional buyers. Direct sales often characterize relationships with major stainless steel mills, ensuring stable supply and customized product specifications. Indirect channels, on the other hand, provide market reach and flexibility, particularly for serving diverse customers and managing logistical complexities across different geographical regions, playing a vital role in connecting producers to a broad spectrum of end-users worldwide and enabling market fluidity.

The Ferrochrome Alloy Market serves a diverse yet concentrated base of potential customers, primarily comprised of industries that require materials with enhanced properties like corrosion resistance, high strength, and excellent heat resistance. The predominant end-users are large-scale stainless steel manufacturers, who consume over 80% of global ferrochrome production as a crucial alloying element to achieve specific metallurgical characteristics required for various stainless steel grades. These manufacturers range from integrated steel plants to specialized stainless steel producers, demanding consistent quality and reliable supply volumes. Beyond stainless steel, major consumers include foundries and specialized alloy producers that manufacture high-performance alloys such as tool steels, wear-resistant cast irons, and superalloys for niche applications in the aerospace, power generation, and chemical processing industries. These customers often have stringent specifications and require particular grades of ferrochrome, such as low carbon or medium carbon varieties, for their highly specialized production processes. Furthermore, the automotive sector, through its demand for lightweight and corrosion-resistant components, and the construction industry, with its increasing use of stainless steel in modern infrastructure and architectural designs, represent significant indirect purchasers. The growing renewable energy sector, particularly in components for wind turbines and solar power infrastructure requiring durable materials, also emerges as a high-potential customer segment. The buying decisions of these customers are typically influenced by factors such as product quality, price competitiveness, supply reliability, technical support, and the adherence to environmental and sustainability standards, making long-term partnerships and value-added services critical for suppliers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 25.8 Billion |

| Market Forecast in 2033 | USD 36.3 Billion |

| Growth Rate | 4.9% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Glencore PLC, Samancor Chrome, Eurasian Resources Group (ERG), Outokumpu Oyj, Tata Steel Ltd., IFM-Ferroalloys, VISA Steel Limited, IMFA (Indian Metals & Ferro Alloys Ltd.), Mintal Group, Dongfang Resources, Nava Bharat Ventures Limited, South32 Ltd., Alloys India International, OM Holdings Ltd., Anglo American plc, Merafe Resources, Balasore Alloys Limited, Jindal Stainless Limited, Metda Mining Company, Shanxi Taigang Stainless Steel Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Ferrochrome Alloy Market's technological landscape is continuously evolving, driven by the imperative to enhance production efficiency, reduce operational costs, and meet increasingly stringent environmental standards. A central focus remains on advancements in smelting technologies, particularly improvements in electric arc furnaces (EAFs) and submerged arc furnaces (SAFs), which are the workhorses of ferrochrome production. Innovations include the development of larger, more energy-efficient furnaces capable of higher throughputs and better energy utilization, often incorporating advanced process control systems for real-time monitoring and optimization of smelting parameters. Significant research and development efforts are directed towards pre-reduction technologies, such as the use of rotary kilns or plasma furnaces, to reduce the energy demand in the main smelting process by partially reducing chromite ore before it enters the EAF or SAF. Furthermore, the industry is heavily investing in technologies aimed at reducing carbon emissions, including carbon capture and utilization (CCU) systems, and exploring alternative reductants like biomass or hydrogen to move away from fossil fuel-based reducing agents. Automation and digitalization, leveraging IoT sensors and data analytics, are transforming plant operations by enabling predictive maintenance, optimizing raw material blending, and improving overall yield and product consistency. These technological strides are not only crucial for maintaining competitiveness but also for ensuring the long-term sustainability and environmental viability of ferrochrome production globally, pushing the industry towards cleaner and more resource-efficient manufacturing paradigms that align with global climate goals and circular economy principles.

Ferrochrome alloy is an alloy of chromium and iron, with chromium content typically ranging from 50% to 70%. Its primary use is in the production of stainless steel, where it imparts essential properties such as corrosion resistance, high strength, and hardness. It is also used in other specialty alloys and cast irons to enhance their performance characteristics.

The Asia Pacific (APAC) region currently dominates the global ferrochrome alloy market in terms of both production and consumption. This dominance is primarily driven by the significant stainless steel manufacturing output and rapid industrialization in countries such as China and India, coupled with extensive infrastructure development across the region.

Key drivers for market growth include the escalating global demand for stainless steel, fueled by urbanization and infrastructure projects, particularly in emerging economies. Additionally, the expansion of the automotive and construction sectors, along with technological advancements in ferrochrome production processes aimed at efficiency and sustainability, significantly contribute to market expansion.

The ferrochrome alloy market faces several challenges, including the volatility of raw material prices, particularly for chromite ore and electricity, which are major cost components. Stringent environmental regulations aimed at reducing carbon emissions and high energy consumption costs also pose significant restraints on market growth and operational profitability for producers globally.

AI is increasingly impacting the ferrochrome alloy market by enabling process optimization, leading to improved yields and reduced energy consumption in smelting operations. It also facilitates predictive maintenance for machinery, enhances real-time quality control, and optimizes complex supply chain logistics, ultimately boosting efficiency, sustainability, and market responsiveness across the industry.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.