ID : MRU_ 441262 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

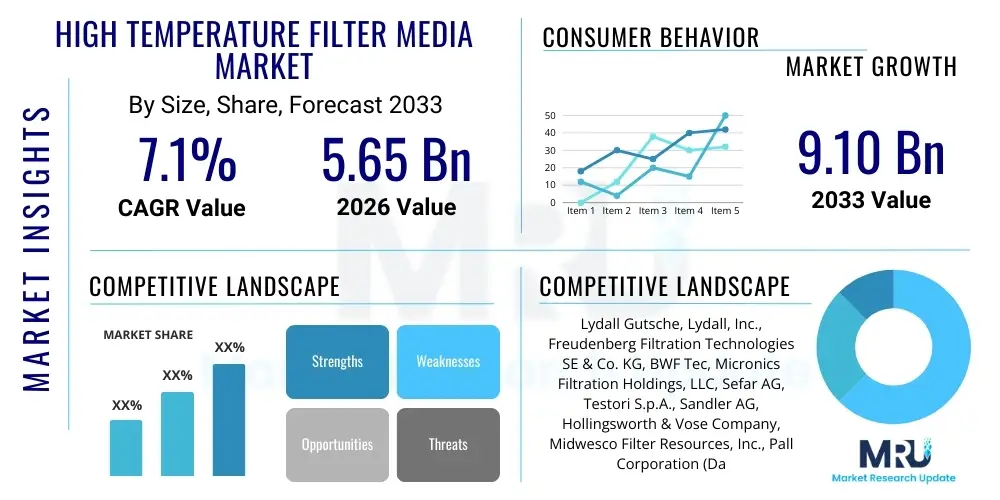

The High Temperature Filter Media Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 7.2 Billion by the end of the forecast period in 2033.

The High Temperature Filter Media Market encompasses specialized filtration materials designed to operate efficiently in industrial environments where gas streams or processes exceed standard operating temperatures, typically above 260°C (500°F). These specialized media, which include materials like ceramic fibers, high-performance synthetic fibers (such as P84, PTFE, and certain aramids), and metal alloys, are crucial for effective particulate matter (PM) control, ensuring compliance with increasingly stringent air quality regulations globally. The primary function is to remove dust and pollutants from hot gas streams before they are released into the atmosphere, thereby protecting downstream equipment and public health.

Major applications of high temperature filter media are concentrated within heavy industries characterized by combustion processes and thermal treatment, including cement manufacturing, coal-fired power generation, waste incineration, metals production (especially non-ferrous), and specialized chemical processing. These materials offer significant benefits over conventional filter media, such as exceptional thermal stability, chemical resistance, and superior particulate capture efficiency, leading to reduced operational downtime and lower maintenance costs. The demand is intrinsically linked to industrial activity expansion, especially in emerging economies undergoing rapid industrialization and modernization of existing production facilities.

Key driving factors accelerating market growth include global mandates for sustainable industrial practices and environmental protection, particularly the enforcement of Maximum Achievable Control Technology (MACT) standards and similar legislation across North America and Europe. Furthermore, technological advancements in material science, leading to the development of filter media with enhanced mechanical strength and reduced permeability at elevated temperatures, are expanding the functional scope and lifespan of filtration systems. The transition towards more energy-efficient and cleaner industrial processes necessitates robust and reliable high-temperature filtration solutions.

The High Temperature Filter Media Market is poised for stable and robust growth, primarily driven by escalating global environmental regulatory pressures concerning industrial air pollution and the necessary modernization of aging infrastructure in established industrial sectors. Business trends indicate a strong focus on research and development, particularly in ceramic and metal-based filtration systems, offering superior longevity and chemical resilience compared to traditional textile-based materials. Strategic mergers, acquisitions, and collaborations between material scientists and system integrators are prevalent, aiming to create integrated dust collection solutions optimized for extreme heat environments. The market profitability is increasingly linked to providing tailored solutions for industry-specific challenges, such as handling corrosive gas mixtures or managing cyclical temperature fluctuations within processes like cement clinker cooling and flue gas desulfurization (FGD).

Regional trends highlight Asia Pacific (APAC) as the fastest-growing market, propelled by massive investments in new coal-fired power plants (despite global decarbonization efforts), accelerated growth in cement and steel production, and the subsequent need for rigorous emission control mandated by governments in China and India. North America and Europe, characterized by highly mature regulatory frameworks, exhibit growth driven by the replacement and upgrading of existing filtration systems with advanced, high-efficiency media to comply with stricter pollution limits. Europe, in particular, shows strong adoption rates for filter media used in biomass energy and waste-to-energy facilities, emphasizing circular economy initiatives and sustainable energy generation.

Segment trends underscore the dominance of the non-woven segment (felt) due to its cost-effectiveness and adaptability, though the technical textile (woven) segment is favored in highly abrasive environments requiring superior mechanical strength. Based on material type, ceramic filters are gaining substantial traction in ultra-high temperature applications (above 800°C), while high-performance polymer fibers like PTFE and P84 remain staples in the 260°C to 400°C range. End-user segmentation confirms the power generation and cement industries as the primary consumers, although robust growth is expected from the niche markets of hazardous waste incineration and specialized glass manufacturing, reflecting the diversification of industrial requirements.

User queries regarding AI's influence typically revolve around predictive maintenance capabilities, optimizing filtration cycles, improving media lifespan estimation, and enhancing compliance monitoring efficiency. Users are particularly concerned about how AI-driven sensor data fusion can reduce unexpected shutdowns caused by filter failure in harsh, high-temperature environments. Key expectations center on AI algorithms capable of analyzing real-time gas flow rates, temperature spikes, particulate loading, and differential pressure across the filter media to predict degradation patterns. This analytical capability is anticipated to transform filter replacement schedules from reactive or time-based maintenance to highly precise condition-based maintenance, minimizing material wastage and maximizing operational uptime, critical factors in capital-intensive industries.

The integration of AI, machine learning (ML), and Industrial Internet of Things (IIoT) is rapidly shifting the operational paradigm of industrial air pollution control. AI systems analyze vast datasets collected from sensors embedded within baghouses and dust collectors, allowing for instantaneous adjustment of cleaning cycles (e.g., pulse-jet timing and intensity) based on actual dust load and permeability characteristics, preventing premature blinding or mechanical stress on the high-temperature media. Furthermore, ML models are being developed to assist material scientists in simulating the performance and degradation of novel filter materials under various extreme conditions, significantly accelerating the R&D cycle for next-generation, high-performance filter media designed to withstand temperatures previously considered infeasible for fabric filters.

While AI does not directly alter the chemical composition or physical structure of the filter media itself, its indirect impact lies in optimizing the utilization and performance verification of these specialized materials. By offering continuous performance auditing and flagging minor deviations that might indicate early structural compromise—such as localized hot spots or chemical attack—AI serves as a powerful diagnostic tool. This precision extends to regulatory compliance, where AI platforms can generate comprehensive, tamper-proof operational reports required by environmental agencies, automating the complex task of demonstrating continuous compliance with stringent high-temperature emission standards, particularly in highly regulated zones like the EU.

The High Temperature Filter Media Market is fundamentally shaped by powerful environmental regulatory drivers, technological restraints concerning material survivability, and significant growth opportunities presented by industrial expansion and the green energy transition. The primary driver is the global tightening of emission standards, forcing heavy industries to adopt best available technology (BAT) for particulate matter control, necessitating high-performance media capable of handling flue gas temperatures. Restraints often revolve around the high initial capital investment required for specialized baghouse systems and the high replacement cost of advanced materials like ceramic monoliths or highly specialized PTFE membranes. Opportunities are abundant in the burgeoning waste-to-energy sector and in hydrogen production, which require robust filtration solutions for off-gases, particularly in regions actively divesting from conventional power sources.

The primary driver accelerating the market is the irreversible trend toward decarbonization and cleaner industrial output. Governments worldwide, particularly in the developed economies of North America and Europe, are imposing stricter limits on PM2.5 and PM10 emissions from stationary sources, especially for industries operating high-temperature processes such as incineration and metal refining. This regulatory impetus ensures a continuous demand for replacement media and motivates facilities to upgrade from low-efficiency electrostatic precipitators (ESPs) to modern high-temperature fabric filters (baghouses). Furthermore, the extended lifespan and superior filtration efficiency offered by premium high-temperature media ultimately justify the higher upfront cost, making them a necessity rather than an optional expense for large industrial operators focused on long-term sustainability and compliance.

Key restraining factors include the complex material science challenges associated with developing filter media that maintain mechanical integrity and chemical resistance simultaneously under continuous high heat and exposure to corrosive compounds (like sulfuric acid mist or alkali salts). Manufacturing specialized materials, such as sintered metal fibers or novel ceramic compositions, involves high production costs and relatively low throughput, contributing to higher market prices compared to conventional media. Additionally, the long product qualification cycles required by major industrial operators act as a market barrier for newer, less-proven filtration technologies. The inherent challenge of disposing of spent high-temperature filter media also presents a logistical and environmental restraint, prompting research into recyclable or biodegradable high-temperature materials.

Opportunities are strongly present in emerging industrial applications and geographical areas. The rapid expansion of specialized metallurgical processes, particularly in high-purity material production and advanced ceramics, creates niche demand for filtration media operating in exceptionally harsh environments. Geographically, Southeast Asia and Latin America represent high-growth potential, driven by infrastructure development projects and new power plant construction where regulatory oversight, though currently less stringent than in OECD nations, is rapidly evolving. The transition toward high-efficiency gasification and pyrolysis technologies in the energy sector also mandates high-temperature filtration at crucial stages, further diversifying the application landscape for advanced filter media providers who can offer customized solutions tailored to these complex processes.

The High Temperature Filter Media Market is comprehensively segmented based on material type, product type, end-use application, and geographical region, reflecting the diverse and demanding requirements of various industrial sectors. Segmentation by material type—including ceramic fibers, high-performance polymers (PTFE, P84, PEEK), glass fiber, and specialized metal alloys—is crucial as the operating temperature and chemical environment dictate the material choice, directly influencing the product's performance and cost structure. Product type segmentation typically divides the market into woven fabrics, non-woven felts (the most common type for bag filters), and rigid media (cartridges and ceramic elements), each tailored for specific dust loads and mechanical stress conditions. The dynamic nature of industrial processes necessitates continuous refinement within these segments, focusing on improving material resilience and optimizing the filter structure to enhance dust cake release and reduce energy consumption.

The end-use application segment forms the most critical determinant of market demand, reflecting the concentration of sales within heavy industry. Key sectors driving consumption include thermal power generation (coal, gas, biomass), cement production (kiln and cooler exhaust), waste incineration (municipal solid waste and hazardous waste), metallurgical processing (smelters and foundries), and chemical manufacturing. Each application presents a unique set of challenges, ranging from high alkali exposure in cement kilns to extreme thermal cycling in waste incinerators, requiring specialized media properties. The chemical resistance and operational longevity under continuous stress are paramount considerations for end-users when selecting appropriate filter media, leading manufacturers to specialize their product lines for specific industry verticals.

Geographical segmentation highlights regional market maturity, regulatory rigor, and industrial capacity. Regions like North America and Europe emphasize replacement cycles and advanced technology adoption due to strict emissions control, while APAC drives volume growth through new installations associated with rapid industrialization. Understanding these segment dynamics is essential for market players to effectively allocate resources, tailor R&D efforts toward materials optimized for specific regional climatic and regulatory requirements, and develop strategic partnerships that leverage local manufacturing expertise and distribution channels to maintain a competitive advantage in this technically challenging and highly specialized market landscape.

The value chain for the High Temperature Filter Media Market begins with upstream raw material suppliers, predominantly specializing in high-purity inorganic chemicals and specialized monomers or polymers essential for creating heat-resistant fibers. This phase involves complex processes like polymerization for synthetics (e.g., PTFE, P84) or advanced ceramic manufacturing techniques for rigid media components. Quality control at this stage is paramount, as the purity and consistency of the raw materials directly determine the thermal stability and mechanical performance of the final filter media. Key activities include research into novel fiber structures, optimizing chemical precursors, and securing stable supply agreements for relatively scarce high-performance polymers and specialized metal powders used in sintering processes.

Midstream activities involve the specialized manufacturing and processing of the filter media. This includes needle punching for non-woven felts, weaving for fabrics, and complex lamination or finishing treatments (such as PTFE membrane application or specialized surface coatings) to enhance chemical resistance and dust cake release properties. Manufacturers in this segment operate capital-intensive plants requiring specialized machinery capable of handling delicate yet high-performance materials. The finished media—often in the form of large rolls—is then converted into final products, such as customized filter bags, cartridges, or elements, tailored to fit specific industrial baghouse designs. Differentiation at this stage often relies on proprietary coating technologies and precision sewing techniques that ensure the structural integrity of the filter element under intense operating conditions.

Downstream activities center on distribution, installation, and post-sales maintenance within the diverse end-user base. The distribution channel typically involves direct sales to major engineering, procurement, and construction (EPC) firms building new facilities, as well as sales through specialized industrial distributors who maintain inventory and provide technical support to existing facilities undergoing routine filter replacements. Direct sales are common for high-value, customized rigid media solutions, while indirect distribution handles the high-volume supply of standard filter bags. Aftermarket services, including system auditing, filter installation, and waste disposal advice, constitute a significant portion of the downstream value, ensuring the optimal performance and longevity of the high-temperature filtration system, thereby maximizing customer retention and brand loyalty within this highly technical market.

The primary customer base for High Temperature Filter Media consists of operators and owners of large-scale industrial facilities that generate hot flue gases and are subject to strict air emission regulations. These facilities operate continuous high-temperature processes and include major international utilities and independent power producers running coal-fired power plants, increasingly integrated with pollution control technologies like Selective Catalytic Reduction (SCR) and Flue Gas Desulfurization (FGD), both of which often require robust high-temperature dust filtration. Additionally, major multinational and regional cement manufacturers are crucial buyers, as filtration is essential for controlling particulate emissions from the kiln and cooler exhaust streams, environments characterized by extremely high temperatures, abrasive dust loads, and alkaline chemical attacks.

A rapidly expanding segment of potential customers includes operators of Waste-to-Energy (W-t-E) and municipal solid waste (MSW) incineration plants. These facilities inherently produce highly corrosive and high-temperature flue gases containing various pollutants, necessitating premium filter media like PTFE or specialized glass fibers for reliable operation. The increasing global focus on sustainable waste management and the construction of new W-t-E facilities, particularly across Europe and APAC, drive consistent demand for high-performance filter bags capable of maintaining integrity under cycling thermal loads and chemical exposure, ensuring regulatory compliance and minimizing the release of hazardous pollutants like dioxins and furans.

Furthermore, specialized metallurgical processing plants, particularly steel mills, aluminum smelters, and non-ferrous metal foundries, represent significant and lucrative potential customers. These operations utilize high-temperature furnaces and refining processes that generate high volumes of fine particulate matter, often requiring sintered metal filters or ceramic elements due to the extremely abrasive and high-heat nature of the dust. Chemical and petrochemical manufacturers, especially those involved in specialized catalyst production or high-temperature reaction processes, also require custom filtration solutions. The purchasing decision in these industries is heavily influenced by total cost of ownership (TCO), material longevity, and the supplier's proven track record in meeting stringent, often customized, performance specifications rather than solely by initial purchase price.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.2 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lydall Gutsche GmbH & Co. KG, Filtration Group Corporation, TenCate Industrial Fabrics, Testori S.p.A, Sefar AG, Micronics Engineered Filtration Group, Clear Edge Filtration, GKD Group, 3M Company, Pall Corporation, AAF International (Daikin), W. L. Gore & Associates, Inc., Parker Hannifin Corporation, Fibertex Nonwovens, Sinoma Science & Technology Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The High Temperature Filter Media technological landscape is continuously evolving, driven by the need for materials that can withstand increasingly demanding operational parameters, specifically higher temperatures and more aggressive chemical compositions in flue gases. A critical technological focus involves advanced polymer synthesis, particularly the development of high-performance polymer fibers like PTFE (Polytetrafluoroethylene), P84 (Polyimide), and PPS (Polyphenylene Sulfide). While PTFE offers excellent chemical resistance and high continuous operating temperature (up to 260°C), manufacturers are concentrating on blending and laminating these fibers with membrane materials to achieve superior surface filtration (dust cake forms on the surface rather than penetrating the depth), significantly enhancing filtration efficiency and pulse-cleaning effectiveness, thereby reducing mechanical stress and extending filter life. New surface treatment chemistries are also being employed to improve hydrophobicity and oleophobicity, crucial for mitigating filter blinding in moist or oily exhaust streams.

Another major technological frontier lies in the domain of inorganic media, specifically ceramic and sintered metal filters, which are essential for applications exceeding 400°C, where polymer fibers fail. Ceramic filters, often constructed from materials such as alumina or silicon carbide, are fabricated using advanced sintering processes or filament winding techniques to create rigid, porous structures (candle filters or barrier filters). Recent innovations focus on optimizing the pore size distribution and enhancing the mechanical fracture toughness of these brittle materials to prevent failure during thermal shocks or physical handling. Sintered metal filters, typically made from stainless steel or nickel alloys, leverage powder metallurgy to produce highly uniform, robust elements capable of operation up to 900°C. Technology advancements here include developing gradient pore structures within the metal matrix to optimize filtration depth and flow dynamics while maximizing structural strength.

Furthermore, composite filter media represent a significant trend, combining the best attributes of various materials to overcome single-material limitations. This often involves laminating an ultra-thin, highly efficient expanded PTFE (ePTFE) membrane onto a robust, temperature-resistant substrate (like fiberglass or P84 felt). This composite approach ensures high collection efficiency (approaching HEPA levels) while maintaining the thermal and mechanical stability required for baghouse operation. The integration of real-time monitoring technologies, including acoustic sensors and advanced differential pressure transducers linked to AI systems, is also part of the technology landscape, moving the focus beyond the material itself to the performance management ecosystem surrounding the media, ensuring precise operation and maximizing the return on investment in these advanced filtration solutions.

The global High Temperature Filter Media Market exhibits distinct regional dynamics, dictated primarily by varying levels of industrial maturity, regulatory enforcement, and energy generation strategies. North America and Europe are considered mature markets characterized by stringent environmental regulations, particularly concerning PM2.5 emissions, driving demand for premium, high-efficiency media used primarily in replacement cycles and infrastructure modernization projects. In these regions, growth is steady and focused on high-value segments such as specialized waste incineration, advanced metallurgy, and the use of biomass and natural gas in power generation, necessitating highly reliable filter materials to meet strict continuous emission monitoring requirements.

The Asia Pacific (APAC) region stands out as the primary engine of volume growth, accounting for the largest market share and the highest CAGR globally. This intense growth is fueled by rapid industrialization, massive investments in coal-fired power plants (despite global shift away from coal), burgeoning cement and steel production, and expanding manufacturing sectors, particularly in China and India. Although regulatory compliance historically lagged, governments across APAC are rapidly adopting stricter emission standards, forcing the large-scale installation of advanced filtration systems in new facilities and mandating upgrades in older plants, thereby creating immense, sustained demand for high-temperature filter media.

Latin America (LATAM) and the Middle East and Africa (MEA) represent emerging markets with high future potential. LATAM's market growth is tied to investments in mineral processing and power generation infrastructure, where imported technologies necessitate compliance with international standards. MEA, particularly the Gulf Cooperation Council (GCC) countries, shows strong demand driven by rapid construction, cement production, and expanding petrochemical and refining sectors, which require robust filtration solutions to handle extremely dusty and often corrosive environments. While these regions may experience greater market volatility than developed economies, the long-term industrialization trajectory ensures increasing uptake of high-temperature filtration solutions.

The market growth is fundamentally driven by increasingly stringent global environmental regulations, particularly concerning industrial particulate matter (PM) emissions. Secondary drivers include the rapid expansion and modernization of heavy industries (power, cement, metallurgy) in developing economies and the necessity for industrial operators to reduce downtime and ensure continuous regulatory compliance.

For ultra-high temperature applications, typically exceeding 400°C (750°F), specialized inorganic media are employed, primarily ceramic filters (such as alumina or silicon carbide candles) and sintered metal alloys (like stainless steel or nickel-based elements), as traditional polymer or glass fibers cannot maintain structural integrity under such extreme thermal stress.

While advanced, high-temperature media (e.g., PTFE or ceramic) have a higher initial purchase price, they significantly reduce the Total Cost of Ownership (TCO) by offering superior chemical resistance, extended operational lifespan, reduced pressure drop for energy savings, and minimized unplanned downtime associated with frequent replacements or system failures.

The cement industry is one of the largest end-users, requiring robust filtration media for kiln and cooler exhausts. These processes generate high volumes of abrasive, high-temperature, and chemically alkaline dust, making reliable, high-performance media essential for both product recovery and mandatory compliance with air pollution control limits.

The Asia Pacific region is the fastest-growing market globally, primarily due to massive infrastructure development, rapid industrialization, and subsequent regulatory catch-up efforts. The high volume of new construction and facility upgrades across power, steel, and cement sectors in countries like China and India fuels a massive demand for filtration media.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.