ID : MRU_ 441221 | Date : Feb, 2026 | Pages : 243 | Region : Global | Publisher : MRU

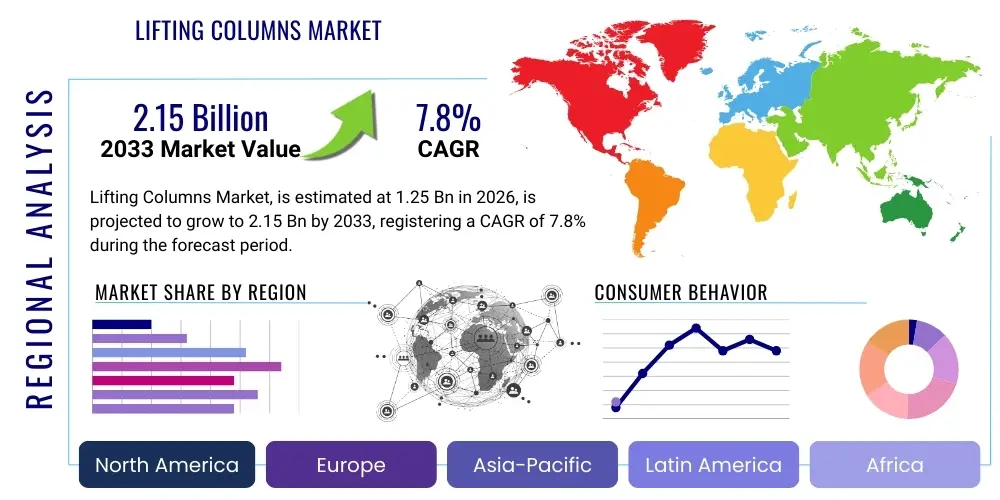

The Lifting Columns Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 1.25 Billion in 2026 and is projected to reach USD 2.15 Billion by the end of the forecast period in 2033.

The Lifting Columns Market encompasses electrically actuated linear motion systems designed for stable, synchronized vertical movement, primarily utilized in applications requiring adjustable height and robust load support. These systems, characterized by their telescopic structure and integrated motor drives, offer precise control over positioning, making them indispensable in modern ergonomic, industrial, and medical environments. Key market drivers include the global proliferation of ergonomic office furniture, stringent regulatory standards mandating safe material handling practices in manufacturing, and the increasing complexity of automated medical equipment, such as surgical tables and patient handling devices. Lifting columns provide a superior alternative to hydraulic and pneumatic systems in scenarios demanding clean operation, low noise levels, and repeatable accuracy, positioning them as fundamental components in advanced automation solutions across various sectors.

Product sophistication within the market is rapidly increasing, driven by demand for greater load capacity combined with sleeker design profiles. Modern lifting columns integrate advanced features such as Hall sensors for enhanced positional feedback, sophisticated controller units for synchronized movement across multiple columns, and battery backup systems for mobility in medical carts. Major applications span industrial workstations, where they facilitate height adjustments for optimal operator safety and efficiency; medical imaging equipment, ensuring precise patient positioning; and advanced home and office environments, supporting sit-stand desks and adjustable kitchen systems. The core benefit of these columns lies in their ability to improve ergonomics, increase productivity, and comply with evolving health and safety standards by enabling dynamic adjustments to working heights and positions, directly influencing user wellbeing and operational output across diverse end-user industries.

Furthermore, the inherent robustness and customizable nature of lifting columns allow manufacturers to cater to highly specialized needs, ranging from heavy-duty industrial machinery lift platforms to highly precise laboratory automation tools. The driving factors propelling sustained market expansion include technological advancements leading to higher duty cycles and smaller installation footprints, the rising awareness regarding the long-term health implications of sedentary work environments, and the overarching trend towards smart factories and automated warehouses where flexible and adjustable infrastructure is paramount. As industries continue to invest heavily in digitalization and ergonomic design, the demand for reliable, intelligent lifting column solutions capable of seamlessly integrating with Internet of Things (IoT) ecosystems and sophisticated control networks is expected to intensify throughout the forecast period, underpinning the projected growth trajectory of the global market.

The global Lifting Columns Market is undergoing substantial expansion, propelled primarily by robust business trends centered on automation, ergonomics, and healthcare infrastructure modernization. Key business indicators suggest a sustained shift toward three-stage and multi-stage columns offering extended stroke lengths and higher stability under load, catering specifically to the sophisticated demands of automated industrial assembly lines and advanced surgical robotics platforms. Strategic mergers, acquisitions, and collaborative partnerships focused on integrating sensor technology and sophisticated control algorithms are defining the competitive landscape, with major players emphasizing vertical integration to control component quality and intellectual property surrounding actuation technology. The transition from purely mechanical to digitally interconnected columns that provide real-time diagnostic feedback and predictive maintenance capabilities represents a defining trend influencing purchasing decisions across enterprise sectors seeking improved uptime and operational efficiency.

Regionally, Asia Pacific (APAC) stands out as the fastest-growing market, driven by massive investments in smart manufacturing infrastructure, the rapid expansion of the medical device manufacturing hub in countries like China and India, and increasing disposable income leading to higher adoption rates of ergonomic furniture in commercial and residential settings. North America and Europe, while mature, maintain dominant market shares due to stringent ergonomic regulations, high adoption rates of advanced automation in industries such as automotive and aerospace, and substantial expenditure on healthcare technology upgrades. The regulatory environment in Europe, specifically concerning workplace safety and comfort (e.g., EU Directive 90/270/EEC), continues to stimulate demand for height-adjustable solutions, creating a stable growth foundation for specialized lifting column providers across the continent.

Segment trends reveal that the Application segment dominated by the Industrial Automation sector due to the ubiquitous need for height-adjustable workstations, conveyor systems, and assembly jigs that must adapt to different tasks and operator heights. However, the Medical & Rehabilitation segment is projected to exhibit the highest CAGR, spurred by the aging global population, the increasing complexity of patient care equipment, and the necessity for precise, quiet, and reliable movement in operating rooms and diagnostic centers. Within the Product Type segment, high-precision, low-noise multi-stage columns are gaining traction over traditional two-stage columns, indicating a preference for compactness and enhanced vertical range without compromising load-bearing capacity. These shifts highlight a market moving towards premium, technologically dense products that justify higher price points based on superior performance and integration capabilities within sophisticated technological ecosystems.

User inquiries regarding AI's influence on the Lifting Columns Market predominantly revolve around themes of predictive maintenance, optimized motion control, and enhanced system integration capabilities. Users frequently ask how AI algorithms can predict mechanical failure, optimize energy consumption during cyclical operations, and facilitate dynamic adaptation of lifting column movements based on real-time environmental or user input data. Concerns are often raised about the complexity of integrating AI modules into existing infrastructure and the cybersecurity risks associated with networked, smart lifting systems. Overall user expectation is that AI integration will lead to a new generation of "intelligent columns" capable of autonomous operation, highly accurate diagnostics, and seamless synchronization within broader robotic and automated workflows, transforming them from simple actuators into crucial, data-generating nodes within the industrial Internet of Things (IIoT).

The market for lifting columns is significantly influenced by a confluence of driving forces, inherent limitations, and emergent opportunities that collectively shape its growth trajectory and competitive dynamics. Primary drivers include the global mandate for improved workplace ergonomics, particularly the massive adoption rate of height-adjustable desks in commercial and home offices, coupled with stringent occupational safety regulations that necessitate adjustable machinery in industrial settings. Restraints often center around the relatively higher initial capital expenditure compared to manual or purely pneumatic systems, particularly for specialized, heavy-duty, or high-precision columns. Opportunities arise primarily from technological miniaturization, allowing columns to be integrated into smaller, mobile devices (like diagnostic carts), and the growing intersection between medical technology and rehabilitation, where highly customizable and reliable vertical positioning is essential for patient care and surgical precision. The interplay of these forces dictates market velocity, compelling manufacturers to innovate constantly to mitigate cost restraints while maximizing technological appeal and compliance with evolving global standards.

The impact forces within the market are predominantly technological and regulatory. Technological momentum favors high-efficiency, low-noise linear actuators capable of integrating seamlessly into smart ecosystems, pushing manufacturers to invest heavily in integrated control systems and brushless motor technology. Regulatory impact forces, particularly those driven by ISO standards concerning cleanroom compliance (in medical and pharmaceutical manufacturing) and international safety standards (e.g., UL certifications), influence product design and market entry strategies. Furthermore, the strong influence of the global supply chain, marked by price volatility in raw materials like steel and specialized electronics, acts as a significant external force impacting profitability and pricing strategies across the industry. Firms capable of navigating these supply chain complexities while rapidly incorporating next-generation sensor and control technology are best positioned to capitalize on sustained market demand.

Specific examples of restraints include the performance gap between linear actuators and traditional hydraulic lifts in extreme high-load applications, although linear technology is rapidly closing this gap. Opportunities are vast in emerging markets where rapid urbanization and industrialization are creating virgin demand for modern, ergonomic infrastructure in new office towers and industrial parks. Addressing the environmental concern associated with material extraction and disposal through the adoption of sustainable manufacturing practices and materials also presents a crucial opportunity for market differentiation and compliance with ESG (Environmental, Social, and Governance) investment criteria. Successfully leveraging these opportunities requires agile product development cycles and targeted marketing that emphasizes total cost of ownership (TCO) benefits over initial purchase price, thereby mitigating the perceived restraint of high upfront investment costs for end-users seeking long-term operational advantages.

The Lifting Columns Market is comprehensively segmented based on three critical parameters: Product Type, Load Capacity, and End-Use Application, providing a granular view of demand dynamics across varied industry landscapes. Analyzing these segments is essential for stakeholders to identify high-growth niches and tailor product development strategies. The market exhibits distinct preferences based on performance requirements; for instance, the medical sector demands precision, quiet operation, and specialized hygiene compliance, contrasting sharply with the industrial sector's focus on sheer load-bearing capacity, durability, and duty cycle performance. This differentiation ensures that manufacturers must maintain a versatile portfolio addressing the unique operational constraints and regulatory compliance requirements inherent to each major segment, necessitating specific design choices regarding materials, motor specifications, and electronic controls, ultimately influencing pricing and competitive positioning across the board.

The segmentation by Product Type (Two-Stage, Three-Stage, Multi-Stage) highlights the ongoing technological migration towards solutions offering better stroke-to-retracted-height ratios, crucial for maximizing workspace utility and minimizing visual intrusion. Three-stage columns, offering superior stability and extension compared to two-stage variants, dominate high-end ergonomic and medical device applications. Meanwhile, the segmentation by Load Capacity (Light Duty, Medium Duty, Heavy Duty) directly correlates with the primary purchasing industry; heavy-duty columns are indispensable in automotive manufacturing platforms and large-scale material handling systems, while light-duty columns saturate the mass-market sit-stand desk segment, representing the largest volume driver in terms of units sold globally due to high consumer adoption rates in modern workplaces.

The End-Use Application segmentation offers the most direct insight into current and future demand hubs. While Office Furniture has historically been a foundational segment, the Industrial Automation and Medical & Rehabilitation segments are exhibiting accelerated growth due to increased capital expenditure in advanced machinery and specialized patient care devices. The integration of lifting columns into sophisticated medical equipment, such as MRI tables, C-arm systems, and automated laboratory equipment, requires exceptionally high reliability and low electromagnetic interference (EMI), leading to premium market valuations within this segment. Successful market penetration therefore depends heavily on segment-specific certifications and establishing trust based on long-term performance data in mission-critical environments.

The value chain for the Lifting Columns Market is characterized by a complex structure starting with specialized raw material procurement and culminating in highly customized integration services at the end-user stage. The upstream segment involves the acquisition of high-quality metals (aluminum alloys, stainless steel for column profiles), precision gears, and sophisticated electronic components (DC motors, microprocessors, Hall sensors). Key challenges upstream include ensuring reliable sourcing of specialized magnetic materials for motors and maintaining cost efficiency amidst volatile metal prices. High vertical integration among leading manufacturers often dictates the quality and cost control in this phase, as companies seek to internalize the production of critical components like control boards and motor assemblies to ensure optimal performance and proprietary intellectual property protection.

The midstream phase focuses on core manufacturing, assembly, and testing. This includes the high-precision machining of telescopic profiles, injection molding of necessary plastic components, motor assembly, and the complex integration of electronic control systems for synchronization and safety features. Stringent quality control is essential here, particularly testing for durability, noise levels, load capacity, and compliance with certifications (e.g., CE, UL). Distribution channels play a vital role in reaching end-users efficiently. Direct channels are commonly used for large Original Equipment Manufacturers (OEMs) in the medical and industrial sectors, where technical consultation and customized solutions are prerequisites. Indirect channels, involving specialized distributors and furniture component suppliers, cater primarily to the mass-market office furniture segment, requiring robust logistics and efficient inventory management.

Downstream analysis highlights the role of systems integrators and furniture manufacturers who incorporate the lifting columns into final products. This phase involves providing specialized installation support, software integration (especially for smart furniture and IIoT applications), and post-sale technical service. The proximity of the lifting column manufacturer to these downstream integrators is often a competitive advantage, facilitating rapid prototyping and custom dimensioning. The end-user purchase decision is highly dependent on factors such as reliability, quiet operation, aesthetic design, and the manufacturer's warranty and service network, reinforcing the importance of maintaining strong, collaborative relationships across the entire value chain from component sourcing to final product deployment and lifecycle support.

The potential customers for lifting columns are highly diverse, spanning sectors that prioritize ergonomic adjustment, precise positioning, and automation capability. The largest and fastest-growing customer base resides within Original Equipment Manufacturers (OEMs) specializing in sit-stand office furniture, where lifting columns are the core functional component. These furniture OEMs demand high volume, standardized products that offer cost efficiency, aesthetic integration, and dependable performance suitable for commercial environments. Furthermore, architectural and interior design firms frequently specify lifting columns for use in integrated smart homes, adjustable kitchen installations, and customized architectural features requiring dynamic vertical movement, often necessitating bespoke designs and quiet operational characteristics to meet high-end residential standards.

Another major customer segment consists of industrial machinery builders and systems integrators who utilize heavy-duty columns for complex automation projects. These industrial customers include automotive manufacturers requiring height-adjustable assembly fixtures, logistics companies integrating adjustable conveyor systems, and specialized machinery builders needing precision lift mechanisms for CNC machines or inspection equipment. Their purchasing criteria emphasize high load capacity, stringent duty cycles, robustness against environmental contaminants (dust, liquids), and seamless communication with industrial control systems (PLCs). Reliability and long-term maintenance support are paramount for these industrial applications due to the high costs associated with production downtime, making technical specifications and certification history crucial factors in procurement.

Critically, the Medical Device Manufacturing sector represents a premium customer segment, demanding columns for use in surgical tables, specialized patient lifts, C-arm imaging systems, and diagnostic workstations. These customers require highly specialized columns characterized by low noise output, smooth transition capabilities (vital for patient comfort), resistance to cleaning agents (IP rating compliance), and strict adherence to medical standards such as IEC 60601-1. The purchase cycle in this segment is lengthy, involving rigorous validation and regulatory compliance checks, emphasizing precision, safety redundancy, and documented material traceability. Ultimately, the market is defined by a dichotomy: high-volume, standardized needs from the office sector, and low-volume, high-specification needs from the medical and advanced industrial sectors, each requiring tailored product offerings and customer service strategies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.15 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | LINAK A/S, Thomson Industries Inc., SKF Group, Progressive Automations Inc., TiMOTION Technology Co. Ltd., Phoenix Mecano Group, DEWERT Okin GmbH, Ewellix (formerly SKF Motion Technologies), Kesseböhmer GmbH, Hettich Holding GmbH & Co. oHG, Accuride International, Ltd., LogicData Electronic & Software GmbH, Concens A/S, Venture Mfg. Co., Hiwin Technologies Corp., T-Slot Engineering, Actuator Solutions GmbH, ZIMM Group, Rollon S.p.A., Ketterer GMBH. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Lifting Columns Market is rapidly evolving, driven by advancements in integrated electromechanical components and sophisticated control systems designed for enhanced performance, connectivity, and user safety. Core technology relies on precision DC or EC (Electronically Commutated) motors, coupled with high-efficiency gear drives, typically worm or screw gear mechanisms, housed within telescopic aluminum or steel profiles. A key technological trend is the transition towards advanced sensor integration, utilizing Hall effect sensors not merely for limit switches but for continuous, high-resolution positional feedback. This sensory data is critical for achieving the perfect synchronization required when two or more columns operate in parallel, particularly under varying load conditions, which is essential for maintaining stability in medical tables and large industrial workstations where uneven loads are common.

Furthermore, significant technological development is focused on optimizing the control unit (CU) architecture. Modern CUs incorporate advanced microprocessors capable of running complex proprietary algorithms for soft start/stop functions, which minimize mechanical stress and noise, thereby extending the column’s lifespan and improving the user experience, particularly in noise-sensitive environments like offices and hospitals. Wireless control, often leveraging Bluetooth or proprietary RF protocols, is becoming standard, facilitating seamless integration with smart home and office ecosystems and reducing cable clutter. The standardization of digital communication protocols, enabling columns to interface directly with external PLCs or industrial networks (e.g., Ethernet/IP, PROFINET), is transforming these components into active, addressable nodes within the Industrial Internet of Things (IIoT), allowing for remote monitoring and diagnostics.

Material science innovation also plays a critical role, particularly concerning the internal gliding mechanisms. The use of advanced polymer guides and precision ball screw technology minimizes friction, reduces heat generation, and significantly lowers operational noise, directly addressing key customer pain points related to durability and acoustic signature. In specialized segments, such as medical applications, the technology focuses on achieving high Ingress Protection (IP) ratings to withstand stringent cleaning procedures and fluid spills, often requiring specialized sealing techniques and corrosion-resistant materials. The future trajectory of technology involves further miniaturization of high-torque motors, increased power density, and the wider adoption of self-locking mechanisms that ensure load retention without continuous power consumption, thereby improving energy efficiency and overall safety compliance across diverse application environments.

Regional dynamics are critical to understanding the global distribution and growth drivers of the Lifting Columns Market, with distinct patterns emerging across established and developing economies. North America, particularly the United States, holds a significant market share, characterized by high adoption rates in the medical sector—driven by advanced healthcare infrastructure and substantial R&D investment in diagnostic equipment—and a mature ergonomic office furniture market. Stringent OSHA regulations concerning worker safety and ergonomic standards provide a foundational baseline for sustained demand. The region exhibits a strong preference for high-quality, customized, and technologically integrated columns, often paying a premium for features like network connectivity and complex multi-axis control systems required for sophisticated industrial automation solutions.

Europe represents another core market, highly influenced by proactive government mandates emphasizing workplace health and wellness (e.g., European Agency for Safety and Health at Work guidelines). Germany and Scandinavia are leaders in adopting ergonomic solutions, fueling steady demand for height-adjustable tables and industrial assembly jigs. European manufacturers are often pioneers in developing highly efficient, aesthetically refined, and exceptionally quiet lifting columns, catering to the continent's strong focus on minimalist design and strict acoustic regulations in commercial spaces. Furthermore, the strong presence of the automotive and precision engineering industries in Central Europe ensures continuous demand for heavy-duty, highly reliable lifting platforms for manufacturing and assembly operations, supporting robust regional market stability.

Asia Pacific (APAC) is projected to be the fastest-growing region, primarily fueled by the rapid industrialization of nations like China, India, and South Korea, coupled with massive government investments in smart city infrastructure and modern office spaces. The surge in electronics manufacturing and the relocation of global production lines to APAC drive immense demand for flexible and automated industrial workstations. Simultaneously, rising standards of living and growing awareness of ergonomic benefits among the rapidly expanding middle class are translating into explosive growth for the office furniture segment. While price sensitivity remains higher in some APAC countries compared to the West, there is a distinct and accelerating shift towards quality, reliability, and imported technology, positioning the region as the key engine for global volume growth in the forecast period.

The primary difference lies in the number of telescopic profiles and stroke length. Three-stage columns offer a significantly longer extension (stroke) relative to their retracted height, providing superior flexibility and stability. This makes three-stage columns ideal for applications requiring a greater vertical range, such as surgical tables or complex height-adjustable industrial work cells.

Currently, the Industrial Automation segment contributes substantial revenue due to the high load capacity and specialized demands of assembly lines, material handling systems, and automated machinery. However, the Office Furniture and Ergonomics segment drives the highest volume of unit sales globally, reflecting the widespread corporate and residential adoption of sit-stand desks, positioning it as a key long-term revenue driver.

AI significantly enhances operational efficiency by enabling predictive maintenance, which reduces unexpected downtime by forecasting component failure. Additionally, AI optimizes power consumption through adaptive motion control and improves precision and synchronization in multi-column systems, critical for maintaining stability and extending the service life of industrial equipment.

Medical applications generally require medium to heavy-duty capacity (1,500 N to 4,000 N or higher), depending on the specific equipment like surgical tables or patient lifts. Crucially, medical columns must also meet strict criteria for low noise, smooth movement (for patient comfort), high IP ratings for cleaning resistance, and certified safety redundancy (IEC 60601-1 compliance).

The Asia Pacific (APAC) region, driven primarily by China and India, offers the fastest growth potential. This rapid expansion is supported by substantial ongoing industrial infrastructure development, massive investment in smart manufacturing, and the accelerating commercial adoption of ergonomic workplace solutions across newly established business centers.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.