ID : MRU_ 441495 | Date : Feb, 2026 | Pages : 241 | Region : Global | Publisher : MRU

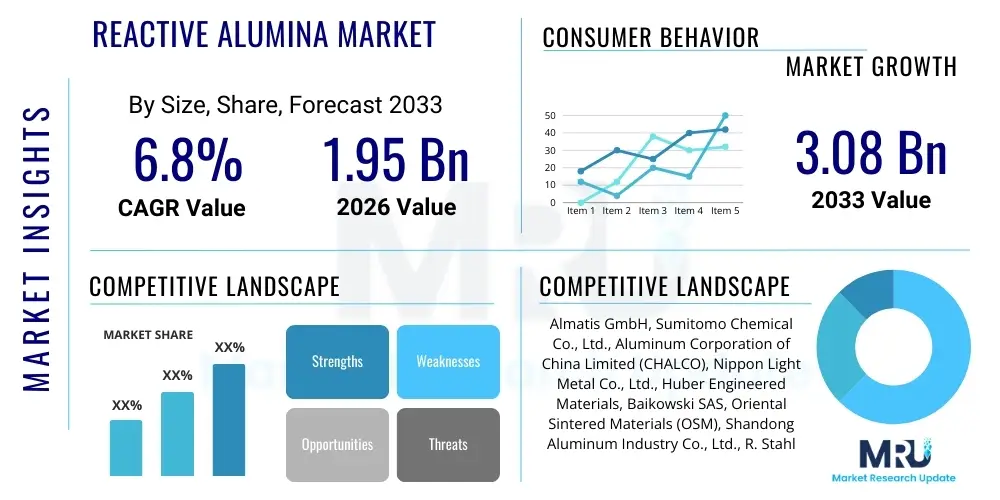

The Reactive Alumina Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 1.8 Billion in 2026 and is projected to reach USD 2.8 Billion by the end of the forecast period in 2033.

The Reactive Alumina Market encompasses the production and distribution of high-purity, fine-particle aluminum oxide (Al2O3) characterized by exceptional chemical reactivity, surface area, and controlled particle size distribution. Reactive alumina is distinct from standard calcined or fused alumina due to its specialized manufacturing process, often involving complex thermal treatments or precipitation methods, which enhance its densification properties and mechanical strength when integrated into advanced material systems. This specialized form of alumina serves as a critical raw material in demanding applications where high density, exceptional wear resistance, thermal stability, and low-temperature firing are paramount. The market is fundamentally driven by the escalating demand for high-performance ceramics, specialized refractories, and precision polishing compounds used across highly sophisticated industrial sectors.

Major applications of reactive alumina span across refractory materials for steel and glass industries, technical ceramics for electronics and automotive parts, and as an essential component in abrasive tools and polishing slurries due to its hardness and controlled morphology. Its benefits include improved sintering behavior, allowing manufacturers to achieve higher material density and superior mechanical properties at lower firing temperatures compared to traditional aluminas, thereby reducing energy consumption and manufacturing costs. Furthermore, its inherent chemical inertness makes it indispensable in catalytic supports and filtration media, where stability under extreme conditions is required. The robust performance profile of reactive alumina positions it as a cornerstone material for industrial modernization and technological advancement globally.

Driving factors propelling the expansion of the reactive alumina market include the rapid growth in the automotive sector, particularly the increased adoption of electric vehicles requiring lightweight, durable, and thermally stable components. Additionally, the flourishing electronics industry demands high-purity alumina substrates and encapsulation materials for semiconductor manufacturing and LED applications. Significant infrastructural investment in emerging economies, necessitating high-grade refractory lining for furnaces and kilns, further fuels market demand. Technological advancements in powder metallurgy and advanced ceramics processing continually open new high-value applications, reinforcing the essential nature of reactive alumina as a functional ingredient for next-generation products.

The Reactive Alumina Market demonstrates robust growth, primarily fueled by the accelerating shift toward high-performance materials in critical infrastructure and manufacturing sectors, globally. Business trends highlight intense competition centered on product purity levels and customized particle size distribution, where manufacturers leveraging advanced calcination technologies and effective supply chain management gain a competitive advantage. Strategic mergers, acquisitions, and long-term supply agreements with major end-users, especially in the technical ceramics and advanced refractories space, are defining current market strategies. Furthermore, sustainability initiatives are influencing product development, pushing for energy-efficient production processes and the exploration of recycled or secondary alumina sources to meet environmental compliance standards and reduce operational carbon footprints.

Regional trends indicate that the Asia Pacific (APAC) region remains the dominant market shareholder and the fastest-growing geographical segment, primarily driven by massive industrial expansion, particularly in China, India, and Southeast Asian nations heavily investing in steel production, electronics, and automotive manufacturing bases. North America and Europe, while mature markets, exhibit consistent growth driven by stringent quality requirements and a high concentration of specialized technical ceramic manufacturers focused on aerospace, defense, and high-end medical applications. These developed regions emphasize innovation in ultrafine and nanosized reactive alumina grades, demanding superior quality control and compliance with strict industrial standards, pushing technological boundaries.

Segmentation trends reveal that the Refractories segment currently holds the largest volume share, reflecting its foundational role in high-temperature industrial processes. However, the Technical Ceramics and Polishing and Grinding Media segments are exhibiting the highest Compound Annual Growth Rates (CAGRs). Demand for high-purity reactive alumina (99.9%+) is escalating rapidly, reflecting the increasing sophistication of end-user requirements, particularly in LED substrates, battery components, and electronic packaging. Product form segmentation shows a distinct preference for powder and granular forms, optimized for efficient processing in downstream manufacturing, ensuring consistent material flow and achieving uniform product density across various critical applications.

User queries regarding the impact of Artificial Intelligence (AI) on the Reactive Alumina Market commonly revolve around themes of manufacturing optimization, predictive quality control, supply chain resilience, and the development of novel material formulations. Users are keenly interested in how AI can enhance the consistency and purity of reactive alumina production, a process notoriously sensitive to temperature and raw material variability. Key themes include the use of machine learning for defect detection in sintered ceramics, optimizing furnace energy consumption during the calcination process, and employing predictive analytics to manage complex global supply logistics, particularly concerning bauxite and energy inputs. Expectations are high that AI will lead to significant cost reductions and unprecedented improvements in material performance characteristics.

The Reactive Alumina Market is primarily driven by persistent demand from high-growth industries such as specialized refractories, advanced ceramics, and abrasives, underpinned by the material's superior strength and thermal properties. Restraints include the high capital expenditure required for setting up high-purity production facilities, volatility in energy costs necessary for the calcination process, and the dependency on reliable sourcing of bauxite and intermediate aluminum hydroxide. Opportunities are emerging through the development of highly specialized nano-reactive alumina grades tailored for additive manufacturing and bio-ceramic applications, alongside strategic efforts to expand production capacity in APAC. The cumulative impact forces indicate a positive trajectory, driven by technological necessity and ongoing industrial modernization, though tempered by supply chain vulnerabilities and pricing pressures from large-volume purchasers.

The primary driving force remains the increasing global adoption of technical ceramics in mission-critical applications, including semiconductor processing equipment, industrial pump seals, and advanced weaponry components, where only high-density, highly resistant materials suffice. Furthermore, environmental regulations demanding increased efficiency in industrial furnaces accelerate the adoption of high-performance reactive alumina-based refractories, which offer longer service life and better insulation. The shift towards lightweight materials in aerospace and automotive industries continues to push demand, as reactive alumina composites offer optimal strength-to-weight ratios compared to traditional metal alloys, solidifying its essential role in modern engineering design and construction globally.

However, the market faces significant restraints. The complexity and energy intensity of producing high-purity reactive alumina grades lead to high manufacturing costs, limiting market entry for smaller players. Furthermore, the global supply chain for precursor materials, particularly bauxite, is concentrated and subject to geopolitical risks and trade tariffs, introducing supply volatility. Another considerable restraint is the availability of substitutes, such as silicon carbide or zirconia, which may offer comparable performance in specific niche applications, forcing reactive alumina producers to continuously innovate and justify the cost-premium associated with their product’s superior thermal and electrical insulating properties. Successfully navigating these restraints requires robust R&D investment and geopolitical risk mitigation strategies by major market participants.

The Reactive Alumina Market segmentation provides a detailed framework for understanding market dynamics across different product attributes, applications, and regional consumption patterns. This segmentation is crucial for stakeholders to identify high-growth niches, allocate resources effectively, and tailor product offerings to specific industry requirements. The primary segmentation dimensions include Product Type (High Purity vs. Standard Purity), Application (Refractories, Ceramics, Abrasives), and End-Use Industry. The refinement of processing techniques has allowed manufacturers to offer highly customized reactive alumina grades, optimized for specific performance metrics such as surface area, porosity, and crystallite size, further defining market subsets.

The segmentation by purity is particularly important, as higher purity grades (typically 99.8% Al2O3 and above) command a significant price premium and are exclusively used in sensitive applications like electronics, medical implants, and high-end grinding media, where even minor impurities can compromise performance. Conversely, standard purity reactive alumina is widely used in high-volume applications such as general industrial refractories and structural ceramics. Analyzing the growth rate across these segments reveals a disproportionate increase in demand for high-purity materials, reflecting the global trend towards miniaturization and enhanced material performance in technological devices. This necessitates continuous investment in separation and purification technologies.

Application-based segmentation confirms the refractories sector as the largest consumer base, utilizing reactive alumina to enhance the density, thermal shock resistance, and corrosion resistance of monolithic and shaped refractory products. The growth in the technical ceramics segment, encompassing wear-resistant components, seals, and insulators, is projected to accelerate the fastest, driven by the increasing need for durable components in severe operating environments across chemical processing, power generation, and specialized machinery manufacturing. Understanding the intertwined nature of these segments—where technological breakthroughs in one area often drive requirements in another—is essential for accurate market forecasting and strategic planning.

The value chain for the Reactive Alumina Market is complex and capital-intensive, starting with the mining and refining of bauxite ore, followed by the production of aluminum hydroxide (the precursor). Upstream analysis focuses heavily on secure, long-term sourcing of high-quality bauxite, energy costs associated with the Bayer process (for alumina production), and the subsequent, highly energy-intensive calcination process necessary to achieve the desired reactivity and particle characteristics. Efficiency and control over these upstream steps are crucial determinants of the final product's quality and cost structure, often leading to vertical integration strategies among major market players to ensure supply stability and consistent quality control from mine to finished powder.

Midstream activities involve the specialized chemical processing and milling of calcined alumina to achieve the required ultra-fine particle sizes and narrow distribution ranges characteristic of reactive alumina. This stage utilizes advanced grinding and classification technologies, often unique to individual producers, representing significant intellectual property and technological barriers to entry. Direct distribution channels, where manufacturers supply large-volume users (like major refractory or ceramic producers) directly, are common for customized or high-purity grades, allowing for technical collaboration and quick feedback loops. Indirect channels, involving specialized chemical distributors, handle smaller volumes and cater to diversified end-users, ensuring wider market reach and localized technical support.

Downstream analysis centers on the integration of reactive alumina into final products across diverse end-use sectors, including refractory brick manufacturing, plasma spraying, and ceramic sintering processes. The performance of reactive alumina critically affects the mechanical strength, thermal properties, and longevity of the final product, positioning the manufacturer as a critical supplier. End-users often require stringent technical specifications and batch-to-batch consistency, making quality assurance a paramount factor throughout the entire value chain. Strategic partnerships between reactive alumina suppliers and major end-product manufacturers are increasingly vital to co-develop optimized material solutions for emerging applications such as high-density armor and advanced thermal management systems.

The primary end-users and buyers of reactive alumina are large-scale industrial consumers demanding materials with superior wear resistance and thermal stability. These encompass the global refractory industry, which purchases substantial volumes for lining high-temperature furnaces and kilns used in steel, cement, and glass production, seeking to extend furnace life and improve energy efficiency. Another major segment includes technical ceramics manufacturers, who utilize reactive alumina powders to produce high-specification components like ballistics armor, electronic packaging, cutting tools, and prosthetic joints, requiring ultra-high purity and controlled microstructure for optimal performance under extreme operational conditions.

Furthermore, the abrasive and polishing industry constitutes a significant customer base, where reactive alumina is formulated into high-performance grinding media, lapping compounds, and precision polishing slurries essential for finishing sensitive surfaces, particularly in the semiconductor and optical components manufacturing sectors. The petrochemical and chemical processing industries are also increasing consumers, using reactive alumina as an inert filler or catalyst support material due to its chemical stability and high surface area properties. The diversity of these end-user segments ensures market resilience, as demand drivers are spread across cyclical industrial sectors, stabilizing overall market growth and sustaining the need for continuous supply of high-quality reactive alumina materials worldwide.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 2.8 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Almatis GmbH, Baikowski SAS, Nippon Light Metal Co. Ltd., Sumitomo Chemical Co. Ltd., Chalco (Aluminum Corporation of China Limited), Huber Engineered Materials, KC Corporation, Nabaltec AG, Rusal, Shandong Aluminum Corporation, Xingran Materials Co., Ltd., Zibo Honghe Chemical Co., Ltd., Vesuvius plc, Possehl Erzkontor GmbH, Washington Mills. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technology landscape in the Reactive Alumina Market revolves around optimizing the synthesis and processing of aluminum hydroxide precursors to achieve highly specific crystallographic structures and ultrafine particle sizes, which define reactivity. The dominant technology is high-temperature calcination, which uses rotary kilns or shaft furnaces, but modern advancements focus on flash calcination and controlled atmosphere sintering to minimize grain growth and maximize surface area. Innovations in wet chemistry routes, such as sol-gel and co-precipitation methods, are gaining traction for producing ultra-high purity and nano-sized reactive alumina required for highly sensitive electronic and biomedical applications, offering superior control over phase transformation and particle morphology compared to traditional dry processes.

Advanced milling and classification technologies are equally critical, utilizing jet mills, ball mills, and sophisticated air separators to ensure extremely tight particle size distributions (PSD) below 10 micrometers, often reaching sub-micron levels. Consistency in PSD is essential for achieving high green density and minimizing shrinkage during the final sintering stage of ceramic manufacturing, directly influencing the performance and structural integrity of the final component. Furthermore, surface modification technologies, including specialized coatings or chemical treatments, are employed to enhance the dispersibility of reactive alumina powders in solvent systems or polymer matrices, improving handling and integration into composite materials, thereby addressing challenges related to powder agglomeration.

The technological evolution is intensely focused on reducing the environmental impact and energy footprint of production. Producers are investing heavily in technologies that allow for lower calcination temperatures or utilize alternative energy sources, responding to increasing global regulatory pressure and the necessity to reduce operational costs. Automation, coupled with sensor technology and Big Data analytics, is increasingly implemented across the entire production line—from raw material inspection to final packaging—to maintain zero-defect standards and ensure batch traceability. These technological advances not only improve material quality but also significantly enhance operational efficiency, solidifying the market’s reliance on capital-intensive, high-precision manufacturing processes to meet demanding customer specifications across diverse industrial segments.

Regional dynamics play a crucial role in shaping the Reactive Alumina Market, reflecting varying levels of industrialization, technological maturity, and infrastructural investment worldwide. Asia Pacific (APAC) leads the market, primarily due to the massive scale of its manufacturing base, particularly in key consumer countries like China, India, Japan, and South Korea. These nations host vast steel, cement, automotive, and electronics industries, all requiring high volumes of reactive alumina for refractories and technical ceramics. APAC’s growth is further fueled by lower production costs and substantial government investments in industrial infrastructure, making it both the largest producer and consumer globally, driving continuous demand for standard and high-purity grades.

North America and Europe represent mature yet highly specialized markets characterized by stringent quality standards and a high concentration of sophisticated end-users in aerospace, defense, and medical sectors. Demand in these regions is primarily for ultra-high purity and specialty-grade reactive alumina used in advanced ceramics, requiring complex certifications and precise technical specifications. Although volume growth is slower compared to APAC, the value realized per unit is higher due to the premium nature of the applications. European focus on sustainable industrial practices is also driving innovation in energy-efficient production technologies within the region.

Latin America (LATAM) and the Middle East and Africa (MEA) are emerging regions that show promising growth, particularly in countries with developing metallurgical and petrochemical sectors. LATAM’s demand is driven by mining and infrastructure projects, while MEA benefits from significant investments in oil and gas processing facilities, necessitating high-performance refractory linings. Market penetration in these regions often involves navigating logistical challenges and establishing reliable distribution networks, but the underlying industrial growth promises steady expansion for key reactive alumina providers who successfully establish local presence or strong distribution partnerships.

Reactive alumina is defined by its exceptionally small, uniform particle size (often sub-micron) and high surface area, coupled with low soda content and high purity, which allows for significantly lower sintering temperatures and achieves higher density and mechanical strength in the final ceramic product compared to standard calcined alumina used for general abrasives or fillers. This enhanced reactivity is crucial for advanced technical applications.

The Technical Ceramics segment, particularly applications within the electronics and semiconductor industries (e.g., LED substrates, electronic packaging, and high-performance insulators), drives the highest growth rate for high-purity reactive alumina. This demand is fueled by the need for materials with impeccable dielectric properties and thermal management capabilities to support increasing miniaturization and complexity in electronic devices.

Volatile energy prices significantly impact profitability because the production process, especially the high-temperature calcination required to achieve high reactivity and purity, is extremely energy-intensive. Fluctuations in natural gas or electricity costs directly translate into higher operational expenditures. Producers mitigate this through long-term energy contracts, investing in energy-efficient technologies, or hedging strategies to stabilize manufacturing costs.

APAC is the dominant region in the global Reactive Alumina Market, acting as both the largest consumer and the largest production base. Its market leadership is attributed to rapid industrialization, massive investments in metallurgy and construction, and a booming electronics manufacturing sector in countries like China and India, creating immense, sustained demand for both refractory and high-performance ceramic grades of reactive alumina.

Key technical specifications sought by customers include precise Particle Size Distribution (PSD), typically measured in micrometers or nanometers, which dictates sintering behavior; high chemical purity (especially low soda content); specific surface area (measured in m2/g) influencing reactivity; and controlled phase composition, often focusing on achieving specific alpha alumina crystal structures for optimal performance in high-wear and high-temperature environments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.