ID : MRU_ 443071 | Date : Feb, 2026 | Pages : 248 | Region : Global | Publisher : MRU

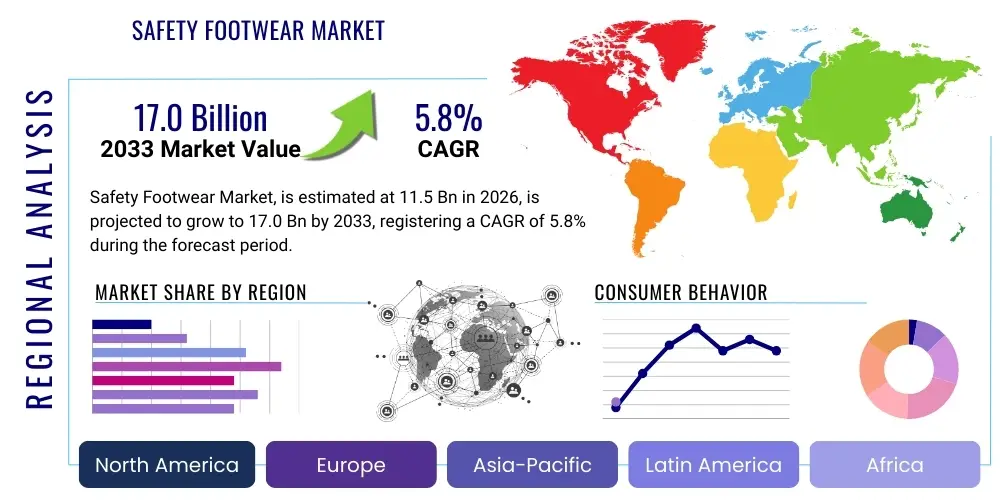

The Safety Footwear Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 11.5 Billion in 2026 and is projected to reach USD 17.0 Billion by the end of the forecast period in 2033.

Safety footwear, an essential component of Personal Protective Equipment (PPE), is specifically engineered to protect the wearer's feet from various workplace hazards, including impact, compression, puncture, electrical risks, and slips. These specialized products are mandated across rigorous industrial environments where occupational risks are inherent. The global market is characterized by stringent regulatory oversight, primarily driven by international standards such as ASTM International (U.S.) and EN ISO 20345 (European Union), which dictate the minimum requirements for protective features like steel toe caps, composite materials, metatarsal guards, and slip-resistant outsoles. The primary function of safety footwear transcends simple protection; modern designs incorporate ergonomic features, advanced cushioning, and breathability to ensure worker comfort during long shifts, directly influencing adherence to safety protocols and overall productivity.

The product portfolio within the safety footwear industry is diverse, encompassing safety boots, shoes, and specialized forms such as dielectric and chemical-resistant models. Major applications span high-risk sectors including construction, manufacturing, oil and gas, mining, and logistics, where heavy machinery, sharp objects, and hazardous substances pose constant threats. Driving factors for market expansion include accelerating global industrialization, especially in developing economies, coupled with heightened awareness regarding occupational health and safety (OHS) legislation enforcement worldwide. Benefits derived from utilizing compliant safety footwear are manifold, including reduced workplace injuries, minimized lost workdays, lower liability costs for employers, and, fundamentally, enhanced worker well-being, solidifying the market's critical role in the industrial landscape.

Furthermore, technological advancements are continually shaping the landscape of safety footwear. Manufacturers are increasingly utilizing lightweight materials, such as non-metallic composite toes, which offer comparable protection to traditional steel without the added weight or thermal conductivity issues. The integration of smart features, including embedded sensors for monitoring temperature, impact levels, and worker fatigue, represents a key growth trajectory. These innovations not only improve performance and comfort but also align with the broader shift towards preventative and proactive safety management systems, ensuring that protective equipment remains a dynamic rather than static defense mechanism against industrial risks.

The global Safety Footwear Market demonstrates resilient growth driven by mandatory safety regulations and robust industrial activity across diverse sectors. Current business trends highlight a significant pivot towards sustainability, with manufacturers exploring recycled, bio-based, and responsibly sourced materials to meet growing corporate social responsibility (CSR) demands from large industrial buyers. The competitive landscape is characterized by both established global PPE giants and specialized regional manufacturers focusing on niche applications and custom fitting solutions. Consolidation activities, particularly mergers and acquisitions, are common strategies employed to expand geographical reach and integrate advanced material science capabilities, specifically concerning impact absorption technologies and superior traction systems designed for diverse working surfaces.

Regionally, the Asia Pacific (APAC) continues its dominance, fueled by massive infrastructure projects, burgeoning manufacturing sectors in China and India, and the gradual adoption of stricter OHS standards mirroring Western protocols. North America and Europe, while mature, remain crucial high-value markets, emphasizing premium features, enhanced durability, and advanced material innovation, particularly in sectors like petrochemicals and precision engineering. Segment trends indicate accelerated adoption of composite toe footwear over traditional steel toe, owing to weight reduction and suitability for environments sensitive to metal detection or extreme temperatures. Moreover, the utility segment, encompassing logistics and warehousing, is experiencing rapid growth, necessitating specialized, lighter footwear designed for high mobility and anti-fatigue properties, differing significantly from the heavy-duty requirements of mining or construction applications.

The market faces operational challenges related to fluctuating raw material prices, particularly for specialized rubber, plastics, and high-performance textiles. However, opportunities abound in developing smart safety solutions. Integrating technologies like RFID tracking for inventory management and wear-life monitoring is gaining traction. The retail distribution channel is expanding rapidly, moving beyond traditional industrial suppliers to encompass e-commerce platforms and specialized retail outlets, enhancing accessibility for small and medium-sized enterprises (SMEs) and individual contractors seeking specialized protective gear. Overall, the market trajectory remains positive, underpinned by an unwavering global commitment to mitigating workplace injuries through high-quality protective gear.

Common user questions regarding AI's impact on safety footwear typically revolve around predictive maintenance, customization capabilities, and compliance monitoring efficiency. Key concerns focus on whether AI can improve the longevity and specific fit of protective gear without substantially increasing costs, and how data generated by smart footwear will be secured and utilized for proactive safety management. Users are highly interested in AI’s potential to analyze operational data—such as step count, pressure distribution, and micro-impacts—to predict when a shoe is compromised or needs replacement, thereby optimizing inventory and reducing risk exposure. The consensus expectation is that AI integration will shift safety management from reactive incident reporting to preventative, data-driven safety optimization, particularly through personalized product recommendations based on individual gait analysis and work environment profiles.

AI is beginning to revolutionize manufacturing processes in the safety footwear sector. In the design and prototyping phases, machine learning algorithms analyze vast datasets related to material stress tests, impact resilience, and ergonomic performance under different industrial conditions. This analytical capability allows manufacturers to simulate failure points and optimize material combinations—such as combining lightweight polymer shells with energy-absorbing midsoles—resulting in products that offer superior protection-to-weight ratios. Furthermore, AI-driven systems are being deployed in quality control, utilizing high-speed cameras and image recognition software to detect minute defects in stitching, sole bonding, and material consistency with far greater accuracy and speed than manual inspection, ensuring compliance with strict global safety certifications before products reach the market.

In the application phase, smart safety footwear integrated with IoT sensors generates continuous real-time data regarding worker behavior and environmental exposure. AI models process this complex telemetry to provide actionable insights. For instance, analyzing subtle changes in the wearer's gait pattern can flag early signs of fatigue or musculoskeletal stress, prompting timely intervention. Moreover, the optimization of the supply chain benefits significantly from AI, enabling predictive forecasting of demand based on regional industrial activity, climate patterns, and regulatory changes, allowing manufacturers and distributors to manage inventory levels more efficiently, reducing both waste and lead times for specialized protective gear.

The dynamics of the Safety Footwear Market are fundamentally shaped by the interplay of stringent regulatory Drivers, operational Restraints, transformative Opportunities, and various Impact Forces originating from technological advancements and economic shifts. The primary driver remains the enforcement of occupational safety laws globally, mandating the use of certified PPE, particularly in high-risk industries like construction and mining, where non-compliance results in severe penalties and significant liability exposure for employers. However, the market faces restraints rooted in the higher manufacturing cost of technologically advanced and specialized footwear, often leading to slower adoption in cost-sensitive emerging markets, coupled with the persistent challenge of balancing robust protection requirements with demands for high comfort and aesthetic appeal, which can sometimes be perceived as mutually exclusive.

Opportunities in this sector are strongly linked to material science and connectivity. The development of advanced, lightweight protective materials, such as carbon fiber and advanced polymers, allows for the creation of durable, comfortable, and metal-free safety options, appealing to a broader industrial base. The burgeoning trend of smart safety footwear, integrating IoT sensors for continuous health and environment monitoring, presents a substantial revenue stream and facilitates preventative safety strategies. Impact forces driving the market include rapid urbanization and associated infrastructure development worldwide, particularly in APAC, which necessitates large labor forces equipped with appropriate safety gear. Furthermore, the increasing global focus on worker wellness and corporate commitment to zero-incident policies exerts continuous upward pressure on the quality and adoption rates of premium safety footwear.

Conversely, macroeconomic volatility, including inflation and supply chain disruptions, acts as a significant restraint, increasing the cost of raw materials like specialized rubbers and durable textiles, affecting overall profitability. The impact forces also involve the shift in labor demographics; with an aging workforce in many developed nations, there is a heightened demand for ergonomic and anti-fatigue safety footwear designed to mitigate age-related physical stress. Successfully navigating these forces requires manufacturers to invest heavily in R&D to deliver cost-effective, multi-hazard protective solutions that meet evolving regulatory landscapes and address the practical comfort concerns of end-users.

The Safety Footwear Market is extensively segmented based on key criteria including Material, Type, Application, and Distribution Channel, reflecting the diverse needs and hazard profiles across different industries. This granular segmentation is crucial for manufacturers to tailor their product development efforts, focusing on specific performance characteristics, such as electrical hazard protection or resistance to chemicals, which are vital for particular end-user sectors like petrochemicals or pharmaceuticals. The complexity of industrial requirements necessitates a deep understanding of these segments to ensure compliance and maximized protective efficacy. Analysis reveals that the material segment is rapidly evolving, moving away from reliance solely on traditional leather toward synthetic materials and high-performance composites, which offer superior weight reduction and specialized environmental resistance properties.

The segmentation by Type, encompassing safety shoes and boots, reveals distinct market demand patterns. While safety boots dominate applications in rugged environments such as construction, mining, and forestry due to enhanced ankle support and higher water resistance, safety shoes are increasingly preferred in sectors requiring high mobility and lighter duty protection, such as logistics, manufacturing assembly lines, and light industrial settings. Furthermore, segmentation by Application highlights the dominance of the construction and manufacturing industries, which are the largest consumers due to the high occupational hazard frequency and workforce density. Emerging application areas, such as the utility sector and maintenance services, are showing accelerated growth, demanding flexible and often custom-designed footwear.

Lastly, the distribution channel segmentation illustrates the shift in purchasing dynamics. While offline channels (industrial distributors and specialized PPE retail stores) remain the primary avenue for large corporate bulk purchases, the online channel is experiencing exponential growth. E-commerce platforms provide greater product transparency, competitive pricing, and accessibility, particularly to smaller contractors and individual professionals seeking highly specialized protective gear. Strategic market growth will depend on optimizing the supply chain to effectively service both large-scale B2B industrial clients and the fragmented B2C demand via digital platforms.

The Value Chain for the Safety Footwear Market begins with upstream activities involving the sourcing and processing of core raw materials, predominantly specialized leathers, high-grade rubbers for outsoles, and advanced materials such as composite plastics, Kevlar, and specialized puncture-resistant fabrics for midsoles and protective plates. Key upstream analyses focus on securing stable supplies of these raw materials, which often face price volatility due to global commodity markets. Manufacturers must establish robust relationships with specialized polymer and textile suppliers to ensure material quality meets stringent certification standards (e.g., slip resistance, electrical resistance, and impact rating). Efficient material transformation, including tanning, molding, and cutting, significantly impacts the final product cost and performance, emphasizing technological investment in precision manufacturing equipment.

The midstream stage involves the core manufacturing, assembly, and quality assurance processes, where design integrity and compliance testing are paramount. Downstream analysis focuses on product distribution, marketing, and post-sale services. Distribution channels are bifurcated into direct sales to large industrial enterprises (often via tenders and long-term contracts) and indirect sales through a network of specialized safety equipment distributors, industrial wholesalers, and increasingly, e-commerce platforms. The choice of channel depends heavily on the scale of the customer and the regional regulatory requirements. Indirect channels allow for wider market penetration and localized inventory management, while direct channels facilitate customization and closer relationship management with key institutional clients. Effective logistics, ensuring timely delivery of certified products to remote industrial sites, is a critical success factor in the downstream operation.

Optimizing the value chain requires synergistic collaboration between material innovation suppliers and end-product manufacturers. The growing complexity of protective requirements necessitates continuous feedback loops from the end-users (the workers) back through the distribution and manufacturing stages to refine design and comfort features. Furthermore, sustainable practices, such as waste reduction in material processing and end-of-life recycling programs for durable footwear components, are increasingly integrated into the value chain as large corporations demand greener procurement options. This integrated approach ensures both compliance and market relevance while optimizing cost structures across the entire lifecycle of the safety product.

The potential customer base for the Safety Footwear Market is vast and highly diversified, spanning virtually every industry where manual labor, heavy machinery, or hazardous environments are present. The primary end-users, or buyers of the product, are large industrial organizations, government agencies responsible for public works and infrastructure, and construction companies that purchase safety footwear in bulk to comply with mandated PPE requirements for their entire workforce. Procurement decisions within these large entities are typically centralized, driven by factors such as compliance with specific safety standards (e.g., electrical hazard ratings, metatarsal protection), durability metrics, and the supplier's ability to handle large-volume customization and regular resupply contracts.

Beyond bulk procurement by large enterprises, the market includes a significant segment comprising Small and Medium-sized Enterprises (SMEs) and individual contractors. SMEs often rely on general industrial distributors or online channels for their smaller, more fragmented purchasing needs, valuing immediate availability and cost-effectiveness. Individual professionals, such as specialized welders, electricians, and tradespeople, often seek premium, customized safety footwear that offers enhanced comfort and specialized features relevant to their specific craft, demonstrating a higher willingness to pay for superior performance and ergonomic design that reduces fatigue over extended working hours. This B2C component, particularly driven by individual preference for non-traditional designs, is growing rapidly.

Furthermore, an emerging customer segment includes institutions involved in logistics, warehousing, and parcel delivery, sectors experiencing exponential growth globally. These environments require lighter, slip-resistant footwear with anti-fatigue properties rather than heavy-duty impact protection, shifting the demand profile towards specialized athletic-style safety shoes. Understanding the specific risk matrix for each customer segment—from the severe crushing hazards in mining to the slip-and-fall risks in food processing—is essential for manufacturers to effectively target and supply appropriate certified protective solutions across this broad spectrum of potential buyers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 11.5 Billion |

| Market Forecast in 2033 | USD 17.0 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Honeywell International Inc., VF Corporation (Timberland PRO, Dickies), Bata Corporation, Wolverine World Wide Inc. (CAT Footwear, Harley-Davidson Footwear), Safety Jogger, Blackrock Expert Safetywear, Jallatte Group, Rahman Group, Sika Footwear A/S, UVEX Safety Group GmbH & Co. KG, Elten GmbH, Dunlop Protective Footwear, KEEN Utility, Red Wing Shoe Company, Rock Fall (UK) Ltd., Cofra S.p.A., Dr. Martens (AirWair International Ltd.), Ergodyne, Garmont International Srl, Liberty Shoes Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Safety Footwear Market is rapidly transitioning from traditional, passive protective gear to integrated, high-performance systems utilizing advanced material science and digital connectivity. A primary technological focus involves the development and application of composite materials, such as carbon fiber and fiberglass, for toe caps and puncture-resistant midsoles. These technologies offer equivalent or superior protection to steel components while drastically reducing the weight of the footwear, improving thermal insulation, and eliminating metal content, which is crucial for environments with metal detectors or magnetic interference. Innovations in outsole technology are also paramount, utilizing specialized rubber compounds and geometric tread patterns derived from biomechanical analysis to achieve unparalleled levels of slip and oil resistance, addressing one of the most common causes of industrial accidents.

A significant disruptive technology is the integration of Smart Safety components. This includes embedding IoT sensors, RFID chips, and Bluetooth beacons directly into the footwear structure. These sensors monitor key parameters such as impact force, temperature exposure, worker localization, and biomechanical data (e.g., gait analysis and fatigue indicators). Data collected is transmitted wirelessly to central safety platforms, enabling real-time monitoring of workplace conditions and worker health. This shift allows employers to move towards preventative maintenance protocols and personalized safety management. Furthermore, additive manufacturing (3D printing) is gaining ground, particularly for prototyping and the customization of components like orthotic insoles and specialized sole units, allowing manufacturers to create complex geometries that enhance cushioning and ergonomic performance tailored to specific industrial tasks.

Another area of concentrated R&D investment is centered on sustainable manufacturing and material circularity. Companies are exploring bio-based polymers, recycled rubber, and durable textile technologies that minimize environmental impact without compromising safety ratings. Technologies that enhance breathability and moisture management—such as advanced membrane linings (akin to Gore-Tex) and highly engineered ventilation systems—are critical for comfort in diverse climates, reducing the risk of skin infections and increasing the overall acceptability and usage compliance of the protective footwear among the workforce. These integrated technological advancements are defining the next generation of highly ergonomic and connected protective gear.

The global Safety Footwear Market exhibits significant regional variations driven by differing industrialization rates, regulatory stringency, and climate conditions. North America, led by the stringent OSHA regulations in the United States and Canada, represents a highly mature and high-value market. Demand here is characterized by a strong preference for durable, brand-name safety boots and shoes incorporating advanced anti-fatigue technology and specialized protection (e.g., EH-rated for electrical hazards). Key industry consumers include major construction, oil & gas, and manufacturing giants, demanding high compliance standards and premium material performance. The market growth is stable, primarily fueled by replacement cycles and continuous investment in infrastructure and energy production.

Europe mirrors North America in its maturity but is driven by the pan-European EN ISO standards, which dictate minimum performance levels. Western European countries emphasize sustainability, ergonomic design, and specialized protective features tailored for high-precision manufacturing, chemicals, and aviation sectors. Germany, the UK, and France are critical markets, with strong consumer demand for certified, comfortable safety shoes suitable for indoor industrial environments. Regulatory bodies across the EU ensure consistent application of safety standards, propelling demand for certified protective equipment and favoring manufacturers with strong R&D capabilities in lightweight and sustainable protective solutions.

Asia Pacific (APAC) stands out as the fastest-growing region, contributing the largest volume to the global market. This rapid expansion is propelled by massive industrial growth in nations like China, India, and Southeast Asian countries, coupled with substantial infrastructure and urbanization projects. While price sensitivity remains a factor, increasing governmental enforcement of local occupational safety laws, influenced by global protocols, is shifting demand from basic, uncertified protective wear to compliant safety footwear. The sheer scale of the manufacturing and construction workforce in APAC ensures sustained high demand, though regional manufacturing dominance also leads to intense price competition. Latin America and the Middle East & Africa (MEA) are emerging markets, with growth concentrated in mining, energy extraction, and developing infrastructure sectors, where demand for heavy-duty protective boots is particularly strong, albeit often subject to regional economic instability and varied regulatory enforcement.

Steel toe footwear uses steel caps for maximum impact and compression resistance, providing robust protection that meets stringent industrial standards. However, steel is heavy and conductive. Composite toe footwear utilizes non-metallic materials, such as carbon fiber or specialized plastic, offering similar safety ratings while being significantly lighter, non-conductive (beneficial for electrical environments), and non-magnetic. Demand for composite materials is increasing due to enhanced comfort and suitability across diverse temperature ranges, making them highly desirable for roles requiring prolonged standing or high mobility.

Globally, the quality and certification of safety footwear are primarily governed by two major standards: EN ISO 20345, prevalent across Europe and widely recognized internationally, and ASTM F2413, mandatory in the United States. These standards dictate minimum requirements for features such as impact resistance (I), compression resistance (C), metatarsal protection (Mt), electrical hazard protection (EH), and puncture resistance (PR). Compliance with these standards is critical for manufacturers, as end-user procurement decisions are often contingent on certified adherence to regional safety laws and liability reduction protocols. The increasing globalization of supply chains necessitates manufacturers to seek dual or multi-standard certifications to access various international markets effectively.

Smart technology is fundamentally transforming safety footwear design by embedding sensors (IoT) and connectivity features into the product. This allows for real-time monitoring of workplace risks and worker health. Future designs will focus on sophisticated biomechanical analysis (e.g., gait, posture) to prevent fatigue and musculoskeletal injuries, integration of GPS/RFID for precise worker localization and asset tracking, and predictive maintenance alerts. This shift enables preventative safety measures rather than purely reactive incident management, leading to the development of highly customized, data-driven protective equipment that improves overall OHS performance.

The largest market share for safety footwear is consistently held by the Construction and Manufacturing industries globally. The construction sector, due to high physical hazards, heavy machinery use, and stringent site regulations, necessitates robust protective boots with features like puncture resistance and metatarsal guards. The manufacturing sector, encompassing heavy industry, automotive, and general assembly lines, also drives significant demand for durable, non-slip safety shoes. Additionally, the rapid expansion of the Logistics, Warehousing, and Transportation sectors, fueled by e-commerce growth, is rapidly increasing the demand for lightweight, anti-fatigue safety shoes designed for high mobility environments.

Sustainability trends are increasingly critical, driven by corporate social responsibility (CSR) mandates from large buyers. Manufacturers are focusing on material circularity, utilizing recycled rubber for outsoles and bio-based polymers for other components. Furthermore, efforts are concentrated on reducing manufacturing waste, minimizing the use of hazardous chemicals in processes like leather tanning, and improving the longevity and recyclability of the final product. The market is witnessing a rise in products certified for sustainable sourcing and ethical labor practices, positioning sustainability as a key competitive differentiator alongside performance and protection features.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.