ID : MRU_ 443448 | Date : Feb, 2026 | Pages : 258 | Region : Global | Publisher : MRU

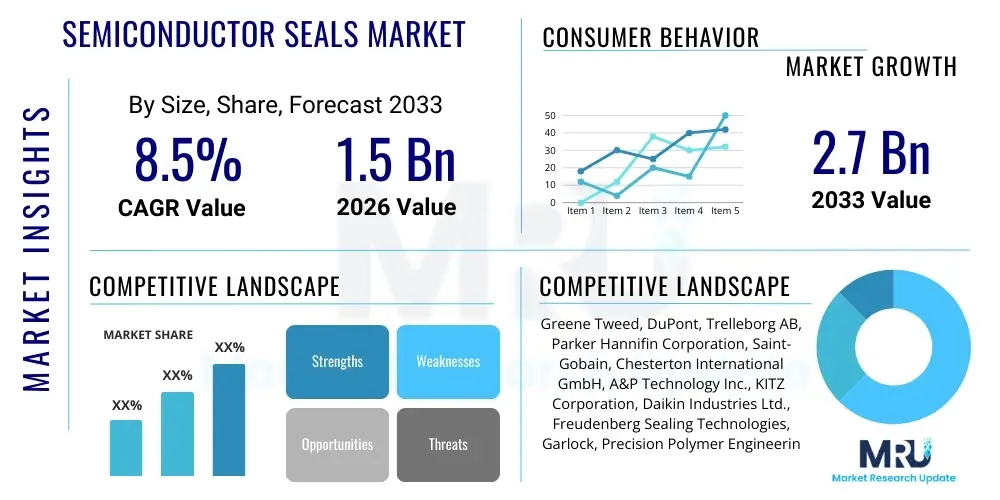

The Semiconductor Seals Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 8.6 Billion by the end of the forecast period in 2033.

The Semiconductor Seals Market encompasses specialized sealing solutions critical for maintaining the ultra-pure, high-vacuum, and chemically aggressive environments within semiconductor fabrication equipment. These components, primarily elastomeric O-rings, gaskets, and customized seals made from advanced polymers like Perfluoroelastomers (FFKM) and polytetrafluoroethylene (PTFE), are essential for equipment used in critical processes such as etching, chemical vapor deposition (CVD), physical vapor deposition (PVD), and atomic layer deposition (ALD). The performance of these seals directly impacts yield rates, process efficiency, and equipment uptime. Failure in seals can introduce contaminants, leading to expensive scrap and downtime, thus necessitating materials that offer unparalleled resistance to plasma, high temperatures, and corrosive process gases used in advanced manufacturing nodes.

The primary function of semiconductor seals is to prevent leakage and contamination in high-purity systems. They must exhibit superior chemical inertness, minimal outgassing, and excellent thermal stability to withstand extreme operating conditions. Modern semiconductor manufacturing, particularly the transition to sub-10nm architecture and the implementation of Extreme Ultraviolet (EUV) lithography, places increasingly severe demands on sealing technology. This trend mandates continuous material innovation, focusing on enhanced plasma resistance and reduced particle generation. Leading market players are heavily investing in proprietary compound development, often partnering directly with major Original Equipment Manufacturers (OEMs) like Applied Materials, Lam Research, and Tokyo Electron to ensure seals meet the rigorous specifications required for next-generation wafer processing tools.

Driving factors for this market expansion include robust global demand for advanced computing chips—driven by sectors such as artificial intelligence (AI), 5G infrastructure, and high-performance computing (HPC)—which necessitate increased global foundry capacity. Furthermore, the persistent trend toward miniaturization and complexity in chip design demands stricter process controls, thereby increasing the reliance on high-performance sealing materials capable of enduring harsher processing conditions. The market benefits derived from high-purity seals include prolonged Mean Time Between Failure (MTBF) for expensive equipment, improved wafer yield quality, and overall operational cost reduction through less frequent equipment maintenance and material replacement cycles.

The Semiconductor Seals Market is experiencing dynamic growth, primarily fueled by massive capital expenditure (CapEx) in leading semiconductor manufacturing regions, notably Taiwan, South Korea, the United States, and increasingly, China. Key business trends highlight a strong shift toward highly specialized, custom-engineered sealing solutions rather than standard off-the-shelf products. Manufacturers are prioritizing strategic supply chain resilience, moving away from single-source material dependencies, particularly following recent geopolitical and logistical disruptions. The integration of advanced diagnostics and predictive maintenance tools into sealing systems represents an emerging trend, allowing manufacturers to monitor seal integrity in real-time and predict failure points, thereby optimizing maintenance schedules and minimizing unscheduled downtime.

Regionally, the Asia Pacific (APAC) dominates the global semiconductor seals market, underpinned by the concentration of major Integrated Device Manufacturers (IDMs) and pure-play foundries like TSMC, Samsung, and SK Hynix. This dominance is expected to strengthen further as China aggressively pursues self-sufficiency in semiconductor production, driving significant investment in domestic fabrication plants (fabs). North America and Europe, while maintaining crucial roles in equipment manufacturing (OEMs) and advanced R&D, primarily contribute through the export of high-specification seal materials and cutting-edge sealing technologies. Expansion in Southeast Asia, specifically Malaysia and Vietnam, is also gaining traction as these nations attract backend assembly and testing operations, modestly increasing local demand for reliable sealing components.

Segment trends reveal that the Perfluoroelastomer (FFKM) material segment holds the largest market share due to its exceptional chemical resistance and thermal stability, making it the preferred choice for extreme plasma environments in etching and deposition chambers. However, advanced PTFE variants and specialized composites are seeing accelerated adoption where lower friction and specific mechanical properties are required. Application-wise, the etching and deposition processes remain the highest consumers of seals, given their harsh chemical environment and high replacement rates. Foundries and Integrated Device Manufacturers (IDMs) represent the primary end-users, driven by the necessity for flawless seals to protect their multimillion-dollar production lines and ensure the stringent quality standards required for complex logic and memory chips.

Common user questions regarding AI's influence on the Semiconductor Seals Market revolve around whether AI-driven chip design complexity will necessitate entirely new sealing materials, if predictive maintenance algorithms will reduce seal replacement frequency, and how AI might optimize the manufacturing process of the seals themselves. Users are keen to understand the balance between increased seal demand stemming from AI data center expansion and the potential decrease in replacement rates due to smarter monitoring systems. Furthermore, there is significant inquiry into whether AI-enhanced process control in fabs (e.g., plasma tuning optimization) could inadvertently make process conditions harsher or, conversely, more predictable, impacting seal longevity.

The rise of Artificial Intelligence (AI) serves as a primary macro-driver for the Semiconductor Seals Market, primarily through the massive surge in demand for high-performance computing (HPC) chips, AI accelerators, and specialized memory. The creation of these advanced processors requires state-of-the-art fabrication techniques (sub-5nm nodes), which rely heavily on highly aggressive processes like deep reactive ion etching (DRIE) and extreme deposition methods. These harsher manufacturing environments directly translate into a demand for seals with superior plasma and thermal resistance, pushing material scientists to rapidly innovate FFKM and PTFE compounds. AI’s indirect influence is seen in the need for increased global fab capacity to meet the unprecedented compute power requirements, ensuring sustained, long-term market growth for sealing solutions.

Beyond driving end-product demand, AI is also fundamentally changing the operational landscape within the semiconductor fabrication environment, which subsequently affects seal procurement and usage patterns. Predictive maintenance systems, often powered by machine learning algorithms analyzing vibration, temperature, and residual gas analysis data, are increasingly deployed on critical fab equipment. These systems allow equipment operators to forecast the degradation point of seals with high accuracy, shifting maintenance strategy from time-based replacements to condition-based replacements. While this optimization might slightly extend the operational lifespan of individual seals, the overall volume demand remains high due to accelerated global chip production schedules and the increasing density of sealing points within modern, complex processing chambers.

The Semiconductor Seals Market is shaped by a robust interplay of Drivers (D), Restraints (R), and Opportunities (O), exerting significant Impact Forces on strategic decisions and market trajectory. The foremost driver is the relentless pursuit of Moore's Law, pushing chip manufacturers toward smaller, more intricate geometries that require increasingly harsh processing chemicals and high-energy plasma treatments, necessitating continual upgrades in seal performance specifications. Simultaneously, geopolitical tensions and supply chain vulnerabilities act as major restraints, particularly concerning the sourcing of high-purity raw fluoropolymers and specialized curing agents, leading to volatility in pricing and lead times. Opportunities lie primarily in developing materials compatible with emerging fabrication techniques, such as advanced 3D stacking technologies and EUV lithography, which demand exceptional purity and vacuum integrity. These forces combine to create a highly specialized and technically demanding market environment where innovation is mandatory for competitive advantage.

Specific market drivers include massive government subsidies globally aimed at establishing domestic semiconductor supply chains (e.g., the U.S. CHIPS Act and EU Chips Act), leading to an unprecedented wave of new fab construction and equipment procurement. The escalating complexity of semiconductor processes, particularly multi-step etching and selective deposition, directly increases the number of critical sealing points per piece of equipment. Conversely, a significant restraint is the extremely high cost and long validation cycle required for new sealing materials in the semiconductor industry. Fabs require extensive qualification data, often taking 12 to 24 months, which slows the adoption of potentially superior, yet unproven, sealing technologies. Furthermore, the specialized skillset required for handling and installing ultra-high-purity seals poses a labor constraint, especially in rapidly expanding markets.

Market opportunities are centered on material science breakthroughs and strategic partnerships. The development of advanced thermoset perfluoroelastomer compounds that offer superior resistance to Fluorine radicals and other aggressive plasma species provides a pathway for seal manufacturers to capture premium segments. Furthermore, the push towards sustainability in manufacturing creates opportunities for developing non-PFAS (Per- and polyfluoroalkyl substances) based high-performance seal alternatives, although this remains a long-term challenge due to the current performance limitations of non-fluorinated materials under extreme conditions. The most powerful impact force remains technological obsolescence; seals that fail to meet the purity and plasma resistance demands of the next-generation fabrication nodes (e.g., 2nm and below) will rapidly lose market relevance, compelling continuous R&D investment.

The Semiconductor Seals Market is intricately segmented based on material type, application, and end-user, reflecting the highly specific requirements of various semiconductor manufacturing processes. Segmentation by material is crucial as the chosen compound dictates resistance to chemical corrosion, plasma erosion, and thermal cycling, with Perfluoroelastomer (FFKM) dominating due to its superior performance characteristics. Application segmentation identifies high-consumption areas like etching and deposition, where seals are exposed to the harshest environments and require frequent replacement, distinguishing them from less demanding applications like fluid handling or instrumentation. End-user segmentation categorizes demand based on the type of chip manufacturer, recognizing that Foundries typically have the highest volume requirements compared to Integrated Device Manufacturers (IDMs) or specialized Original Equipment Manufacturers (OEMs).

The value chain for the Semiconductor Seals Market begins with the upstream sourcing of specialized raw materials, primarily high-purity fluoropolymers, specialty elastomers, and proprietary fillers. This initial stage is highly consolidated, controlled by a few global chemical giants who produce the base compounds (e.g., DuPont, Daikin). The quality and purity of these raw materials are paramount, as even minute impurities can compromise the performance of the final seal in a plasma environment. Manufacturers in this stage must adhere to rigorous purity standards, investing heavily in cleanroom polymerization processes. The dependence on a specialized supply base introduces strategic vulnerability, prompting leading seal manufacturers to maintain dual-sourcing strategies and invest in purification technology to ensure material consistency and ultra-low outgassing properties.

The intermediate stage involves the specialized compounding, molding, and finishing of the seals. This conversion phase is complex, requiring high-precision injection molding, compression molding, or transfer molding techniques performed under ISO Class 1 to Class 7 cleanroom conditions. Customization is a key driver here, as different fab processes require specific seal geometries and material hardnesses (durometers). Seal manufacturers, such as Greene Tweed and Trelleborg, add significant value through proprietary compounding formulas designed for enhanced plasma resistance (e.g., lower erosion rates) and superior mechanical resilience. Advanced post-curing and cleaning processes, including plasma treatment and exhaustive cleaning with ultra-pure water and solvents, are necessary to achieve the ultra-cleanliness required by the downstream semiconductor fabrication facilities.

Distribution occurs through two primary channels: direct sales to Original Equipment Manufacturers (OEMs) and sales to end-users (Foundries/IDMs) either directly or via specialized, technically proficient distributors. Sales to OEMs (e.g., AMAT, TEL) represent the indirect channel; seals are integrated into new equipment packages, locking in seal providers for subsequent replacement cycles. The direct channel involves sales of replacement seals (aftermarket) to the fab operators themselves. Due to the critical nature and high purity requirements, a technical and consultative sales approach is mandatory, as distributors must possess deep knowledge of semiconductor processes and material compatibility. Effective supply chain management is crucial in the downstream, ensuring seals are delivered in appropriate, certified clean packaging to maintain integrity right up to installation.

The primary end-users and potential customers for high-performance semiconductor seals are broadly categorized into major global Foundries, Integrated Device Manufacturers (IDMs), and Original Equipment Manufacturers (OEMs). Foundries, such as TSMC, UMC, and GlobalFoundries, represent the largest volume segment, as their business model relies on maximizing wafer throughput and minimizing yield loss across multiple, high-volume production lines. These customers demand seals that offer extended operational lifetimes and absolute chemical inertness to ensure process stability in multi-billion-dollar fabrication facilities. Procurement decisions here are heavily influenced by proven MTBF (Mean Time Between Failure) statistics and total cost of ownership rather than initial unit price, reflecting the catastrophic financial consequences of process contamination.

Integrated Device Manufacturers (IDMs), which include giants like Samsung, Intel, and Micron, also represent significant potential customers. Unlike pure-play foundries, IDMs design, manufacture, and often package their own chips, necessitating sealing solutions across the entire value chain—from front-end fabrication (etching, deposition) to backend assembly and testing. The specific needs of IDMs are often tied to their internal technology roadmaps (e.g., advanced memory or specialized logic), requiring seal suppliers to collaborate closely on custom compounds and geometries compatible with proprietary process flows. The trend among both Foundries and IDMs to aggressively expand capacity globally, driven by technological mandates such as AI and autonomous vehicles, solidifies their position as the core target market.

Original Equipment Manufacturers (OEMs) constitute another critical customer segment. These are the companies that design and build the sophisticated tools used in the fab, such as etching tools, lithography systems, and PVD/CVD reactors (e.g., Applied Materials, ASML, Tokyo Electron, KLA). OEMs purchase seals for integration into new equipment shipped to Fabs worldwide. Securing OEM qualification is vital for seal manufacturers, as it provides a robust, long-term revenue stream through initial equipment installation and subsequent aftermarket replacement sales. OEMs demand stringent sealing performance certifications during the tool design phase, making them a high-barrier-to-entry, yet highly lucrative, segment for specialized seal providers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 8.6 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Greene Tweed, DuPont, Trelleborg AB, Parker Hannifin, Valqua, Freudenberg Sealing Technologies, Saint-Gobain, Entegris, Kureha Corporation, Techno-Visions, Precision Polymer Engineering (PPE), Pioneer Industrial, Seal & Design Inc., Fuji Industrial, Angst+Pfister. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Semiconductor Seals Market is dominated by advancements in material science focused on maximizing resistance to high-energy plasma and corrosive chemistries. A core technology involves developing ultra-high-purity Perfluoroelastomers (FFKM) with minimal leachables and extractables. Manufacturers utilize proprietary curing technologies, such as plasma curing or specialized cross-linking agents, to enhance the molecular structure of the material, making it denser and less susceptible to radical attack from process gases like NF3, C4F8, and Chlorine. This focus on material integrity is critical, as surface erosion or particle generation from seals can directly lead to defects on the semiconductor wafer, significantly lowering production yields. The relentless technological push is toward creating "zero-shedding" materials capable of surviving thousands of cycles in highly aggressive environments without degradation.

Another crucial technological development revolves around the manufacturing and post-processing techniques aimed at achieving and maintaining ultra-cleanliness. High-specification seals are now routinely manufactured in ISO Class 1 certified cleanrooms to eliminate external particle contamination. Post-molding processes include multi-stage cleaning protocols utilizing ultra-pure solvents, supercritical CO2 cleaning, and specialized UV treatments to remove volatile organic compounds (VOCs) and surface particles. Furthermore, advanced surface modification technologies, such as fluorination or specific coatings, are sometimes applied to seals used in critical vacuum environments to reduce friction, minimize particulate adhesion, and improve overall sealing effectiveness, particularly in dynamic applications like load locks.

The integration of sensing and monitoring technologies into sealing systems represents an emerging technological frontier, moving the market towards smart sealing solutions. This includes embedding or integrating micro-sensors (e.g., pressure or temperature gauges) or utilizing advanced materials that exhibit specific changes (e.g., color shift, electrical resistance change) upon exposure to certain contaminants or extreme wear. While still nascent, this technology aims to provide real-time data on seal health, enabling true predictive maintenance and significantly improving equipment uptime. Furthermore, computational modeling, specifically Finite Element Analysis (FEA), is widely used during the design phase to optimize seal geometry and compression force distribution, ensuring reliable sealing performance under fluctuating pressure and temperature conditions common in advanced deposition tools and increasingly crucial for maintaining the deep vacuum required for EUV lithography systems.

The primary material used in critical semiconductor applications, such as etching and deposition chambers, is Perfluoroelastomer (FFKM), often known by brand names like Kalrez or Chemraz. FFKM offers exceptional resistance to aggressive plasmas, high temperatures, and corrosive chemicals, ensuring ultra-low particle generation necessary for high-yield manufacturing.

EUV lithography requires extremely high vacuum levels (near perfect vacuum) and precise contamination control. This technology significantly elevates the demands on seal purity, outgassing characteristics, and long-term sealing integrity, necessitating the use of specialized, certified ultra-clean FFKM and modified PTFE seals to maintain system performance.

Asia Pacific (APAC) dominates the global market, accounting for the largest share of consumption. This dominance is driven by the massive production capacities of major Foundries and IDMs located in Taiwan, South Korea, and China, which are currently spearheading the transition to advanced logic and memory nodes.

The most significant challenge is the continuous necessity for advanced material innovation to combat increasing plasma aggressiveness. As chip geometries shrink, process conditions become harsher, requiring seal materials that can survive intense Fluorine radical attacks and maintain zero particle generation without lengthy and costly qualification periods.

Yes, seals, particularly those exposed to harsh plasma and chemical environments (e.g., in etching tools), are consumables subject to planned and unplanned replacement. Their replacement rate is a critical factor in equipment maintenance cost and is increasingly managed using advanced predictive maintenance algorithms to optimize uptime.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.