ID : MRU_ 431867 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

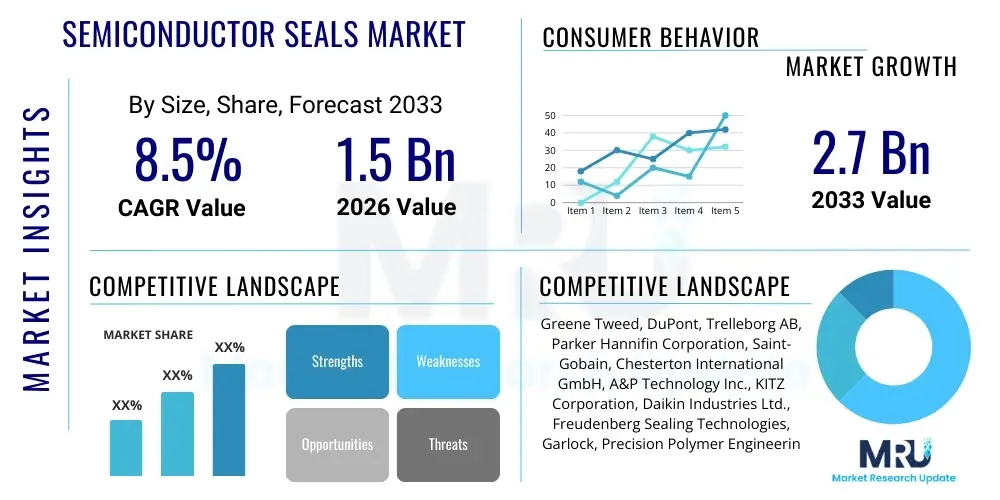

The Semiconductor Seals Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 1.5 Billion in 2026 and is projected to reach USD 2.7 Billion by the end of the forecast period in 2033.

The Semiconductor Seals Market encompasses specialized sealing solutions critical for maintaining the ultra-pure, high-vacuum, and corrosive environments necessary within semiconductor manufacturing equipment. These seals, primarily made from advanced polymers like Perfluoroelastomers (FFKM), PTFE, and highly durable metals, ensure process integrity during crucial fabrication steps such as etching, chemical vapor deposition (CVD), and physical vapor deposition (PVD). The core function of these seals is to prevent contamination, minimize downtime, and withstand extreme temperature and aggressive chemical exposure, directly impacting chip yield and operational efficiency. The demand for these high-performance seals is intrinsically linked to the increasing complexity and miniaturization of semiconductor devices, driving the need for materials capable of zero particle generation and superior plasma resistance.

Product descriptions vary widely, ranging from standard O-rings, custom-molded seals, and bonded seals to sophisticated gate valve seals and slit valve seals, each optimized for specific applications within the wafer fabrication process. The choice of seal material is paramount and dependent on the process gas used; for instance, FFKM materials are favored in plasma etching tools due to their superior chemical inertness and temperature stability, ensuring longevity and reducing the total cost of ownership for fabrication plants. The primary applications include reaction chambers, fluid handling systems for slurries and chemicals, and vacuum interfaces across various toolsets used in front-end-of-line (FEOL) and back-end-of-line (BEOL) processes.

The principal benefit of high-quality semiconductor seals is enhanced yield and reduced operational expenditure, achieved by extending the mean time between failure (MTBF) of critical components and preventing costly contamination events. Key driving factors fueling market expansion include the massive global investment in new fabrication facilities (fabs), fueled by government incentives and geopolitical strategies, coupled with the relentless demand for advanced microchips used in 5G, automotive electronics, data centers, and artificial intelligence infrastructure. This structural increase in global wafer starts and the transition to smaller node geometries necessitates seals with tighter tolerances and even greater material purity, pushing innovation across the supply chain.

The Semiconductor Seals Market is experiencing robust growth driven by significant investments in cutting-edge fabrication technologies, particularly those related to 3nm and 5nm node production, which necessitate higher purity and plasma resistance in sealing components. Business trends indicate a strong move toward proprietary and highly customized sealing solutions, with major equipment manufacturers (OEMs) increasingly partnering with material science specialists to co-develop seals optimized for new generation process tools. There is a clear market shift towards FFKM materials, which command a premium due to their superior performance characteristics in aggressive environments, reinforcing the value proposition of high-performance elastomers over traditional sealing options. Furthermore, sustainability is becoming a key business focus, with manufacturers exploring alternatives to perfluorinated compounds (PFAS) where possible, although the substitution in extreme plasma environments remains challenging, driving innovation in advanced materials that balance performance with environmental responsibility.

Regional trends are dominated by Asia Pacific (APAC), particularly China, Taiwan, South Korea, and Japan, which collectively account for the vast majority of global semiconductor manufacturing capacity and ongoing fab expansions. China’s aggressive investment strategy in self-sufficiency within semiconductor manufacturing is creating a substantial localized demand for high-end seals, although the reliance on specialized materials often sourced from North America and Europe remains a crucial supply chain dependency. North America and Europe, while having smaller manufacturing footprints, remain critical hubs for research, development, and the production of ultra-high-purity FFKM and PTFE materials, positioning them strongly in the high-value segment of the market. Geopolitical dynamics and trade tensions are increasingly influencing regional supply chain decisions, pushing foundries to diversify sourcing and increasing the strategic importance of localized manufacturing capabilities for essential components like seals.

Segment trends underscore the criticality of the Etching application segment, which utilizes the harshest plasma chemistries and therefore requires the most sophisticated seals, driving demand for materials like Kalrez and specialized PTFE variants. By material, FFKM remains the fastest-growing segment due to its unparalleled thermal and chemical stability, directly correlating with the complexity of modern deposition and etching processes. Within end-use industries, Integrated Device Manufacturers (IDMs) and pure-play Foundries represent the largest customer base, characterized by high-volume procurement and stringent qualification requirements, while Original Equipment Manufacturers (OEMs) serve as vital intermediaries, often dictating the seal specifications embedded within newly designed process tools. The move towards advanced packaging techniques is also opening new avenues for specialized seals designed for lower vacuum and milder chemical environments compared to front-end processing, signaling diversification in product requirements.

User queries regarding the impact of Artificial Intelligence on the Semiconductor Seals Market frequently revolve around two primary areas: first, how AI-driven demand for advanced chips (like GPUs and specialized accelerators) translates into increased requirements for sealing materials, and second, how AI itself can be used to optimize seal manufacturing, predictive maintenance, and quality control. Users are keen to understand if AI's influence necessitates entirely new seal designs for extreme power density chips or simply intensifies the current demand for higher yield and cleaner processes. The key themes emerging include the potential for AI algorithms to analyze material performance data in real-time within highly corrosive environments, predicting the point of failure (MTBF) of seals more accurately than traditional methods, thereby minimizing unplanned downtime in multi-billion-dollar fabrication facilities. Furthermore, interest exists in how AI can optimize inventory management for diverse seal SKUs required across a fab's multitude of processing tools, ensuring resilience against supply chain volatility while minimizing the holding cost of high-value components.

The market dynamics of the Semiconductor Seals sector are governed by powerful forces derived directly from the underlying volatility and technological intensity of the chip industry. Drivers are dominated by the continuous trend toward device miniaturization, which forces semiconductor manufacturers to adopt increasingly aggressive plasma chemistries and higher vacuum levels, thereby demanding seals with exceptional thermal stability and superior resistance to chemical attack, pushing the material performance envelope beyond traditional elastomer capabilities. Secondly, the massive global investment wave in new fabrication capacity, stimulated by government subsidies (such as the US CHIPS Act and similar European and Asian initiatives) and the underlying structural demand from end-use markets like 5G, high-performance computing, and automotive electrification, guarantees sustained high volume demand for critical consumables like seals. These drivers create a persistent need for suppliers capable of scaling production while maintaining ultra-high quality and cleanliness standards.

Restraints primarily center around the extremely high cost and long lead times associated with high-purity materials, particularly Perfluoroelastomer (FFKM), which is often proprietary and requires highly specialized manufacturing environments, limiting competition and increasing price sensitivity among end-users. Furthermore, the qualification process for seals in new fabrication equipment is notoriously rigorous, lengthy, and expensive; any change in material composition or supplier requires extensive testing to confirm zero impact on wafer yield, creating significant barriers to entry for new innovations or suppliers. Supply chain vulnerability, particularly the concentrated sourcing of specialty fluoropolymers and elastomers, represents another critical restraint, as geopolitical tensions or production disruptions at key material science companies can severely impact the global availability of essential sealing components, threatening fab operational continuity.

Opportunities are largely tied to emerging technological shifts, notably the transition to advanced packaging and heterogeneous integration, which require novel sealing solutions for specialized bonding and inspection tools, often operating under different pressure and temperature profiles than front-end tools. The push for sustainable manufacturing also presents an opportunity, driving research into next-generation seal materials that offer the performance of current FFKM but with improved environmental profiles or enhanced recyclability. Impact forces are currently high, primarily driven by rapid technological advancements (smaller nodes) and significant capital expenditure volatility. The reliance on advanced polymers means that material science innovation is the dominant impact force shaping competitive advantage; only those manufacturers capable of continuous R&D into plasma-resistant and high-purity compounds will capture premium market share. Furthermore, the necessity for robust supplier qualification ensures that once a seal is qualified within a major foundry's process, switching costs are high, reinforcing the market positions of incumbent, trusted suppliers.

The interplay of these factors suggests a market characterized by strong volume growth but intensely contested technological differentiation, where material purity and component reliability are non-negotiable prerequisites for participation.

The Semiconductor Seals Market is primarily segmented based on the critical characteristics that define seal performance and application within the fabrication ecosystem. Segmentation by Material differentiates products based on their chemical and thermal resistance capabilities, crucial for matching the seal to the severity of the process environment—with highly advanced elastomers dominating the revenue landscape. Segmentation by Application highlights the specific process steps in semiconductor manufacturing where the seals are deployed, such as the aggressive etching stage or the high-temperature deposition phases. Finally, segmentation by End-Use Industry distinguishes between direct purchasers like semiconductor foundries and the equipment manufacturers who integrate the seals into their tools. This multi-layered segmentation allows suppliers to focus R&D efforts on the most demanding and highest-growth segments, ensuring product offerings align with the precise needs of next-generation chip production.

The value chain for the Semiconductor Seals Market is highly specialized and spans from the upstream production of exotic raw materials to the stringent downstream qualification and installation in multi-million-dollar fabrication equipment. Upstream activities are dominated by a select group of global chemical companies specializing in high-performance fluoropolymers. These companies, such as DuPont and Daikin, synthesize the proprietary monomer precursors necessary for manufacturing high-purity Perfluoroelastomers (FFKM). This stage is characterized by high capital investment in synthesis facilities, stringent quality control protocols to ensure ultra-low impurity levels, and significant intellectual property surrounding the compounding and vulcanization processes. The scarcity and complexity of producing these specialty chemicals create a crucial bottleneck, making raw material pricing and supply security a central challenge for midstream seal manufacturers.

Midstream activities involve the specialized manufacturing and processing of the raw polymer into the final sealing components. This phase includes compounding the elastomers with specific fillers for plasma resistance, precision molding (injection, compression, or transfer molding) to achieve micron-level tolerances, and meticulous post-molding processes such as cleaning, curing, and packaging in certified cleanroom environments (ISO Class 1 to Class 100). Distribution channels for semiconductor seals are typically bifurcated. Direct sales are common for large, qualified seal manufacturers supplying Tier 1 Foundries (e.g., TSMC, Samsung, Intel) or major Original Equipment Manufacturers (OEMs) like Applied Materials or Lam Research, often under long-term supply agreements. This direct model emphasizes technical support, co-development, and rapid response to material performance issues. The relationship here is characterized by deep trust and shared technical data regarding process chemistries.

Indirect distribution often involves regional distributors or specialized material suppliers who provide inventory management and just-in-time delivery services for replacement seals (MRO market) to smaller fabs or localized manufacturing operations. Downstream, the key activities are focused on integration, validation, and maintenance. OEMs integrate these seals into their complex deposition and etching tools, where the seal performance is a critical factor in tool reliability guarantees. The ultimate end-users—the Foundries and IDMs—conduct rigorous qualification tests before approving any seal material for production use. The feedback loop from the downstream (seal failure analysis and process yield data) back to the upstream material science firms is vital for continuous product improvement and adapting to new semiconductor manufacturing nodes. This tightly coupled value chain underscores the strategic importance of reliable, high-purity sealing solutions, where failure at the lowest cost component can halt the production of the highest value finished product.

The primary consumers of high-performance semiconductor seals are entities involved in the active fabrication and maintenance of integrated circuits, predominantly falling into the categories of Integrated Device Manufacturers (IDMs), Pure-Play Foundries, and Original Equipment Manufacturers (OEMs). IDMs, such as Intel and Samsung, which design, manufacture, and sell their own chips, require vast quantities of seals for their internal fabrication facilities. These customers prioritize long-term reliability and standardization across their global fabs, often demanding custom seals tailored to their specific proprietary processes. Their buying criteria are heavily weighted towards Total Cost of Ownership (TCO), material purity, and documented success in minimizing particle contamination and maximizing Mean Time Between Failure (MTBF), making the technical qualification process a critical barrier to entry for potential suppliers.

Pure-Play Foundries, including industry giants like TSMC and GlobalFoundries, represent the largest and fastest-growing segment of the end-user market. As contract manufacturers for virtually all fabless semiconductor companies, their investment cycles and demand volumes are immense and directly linked to the global capacity utilization rate. These foundries utilize seals across thousands of etching, CVD, and PVD chambers, consuming seals both for initial equipment installation and for ongoing maintenance, creating a constant, high-volume replacement market. The seals used here must be compliant with the latest process nodes (e.g., 5nm, 3nm), where the operating environments are most extreme in terms of corrosive plasma and temperature fluctuation, demanding the absolute best performance from Perfluoroelastomer (FFKM) and advanced polymer seals.

Original Equipment Manufacturers (OEMs) of semiconductor processing tools—such as Applied Materials, Lam Research, KLA, and Tokyo Electron—are crucial intermediary customers. OEMs purchase seals for integration into the new equipment they sell to foundries worldwide. While they are not the final users, their purchasing decisions dictate component specifications and supplier qualification. OEMs require seals that guarantee tool performance and uptime metrics stipulated in their contracts with foundries. Their focus is on innovation integration, sourcing seals that enable breakthrough processes (e.g., new High Aspect Ratio (HAR) etch steps) and seals that are engineered to last the expected service life of the tool, minimizing warranty claims and enhancing their reputation for reliability in the fiercely competitive equipment market.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 2.7 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Greene Tweed, DuPont, Trelleborg AB, Parker Hannifin Corporation, Saint-Gobain, Chesterton International GmbH, A&P Technology Inc., KITZ Corporation, Daikin Industries Ltd., Freudenberg Sealing Technologies, Garlock, Precision Polymer Engineering (PPE), C. Otto Gehrckens GmbH & Co. KG, Nippon Valqua Industries Ltd., Flowserve Corporation, John Crane, Advanced Polymer Technology (APT), ERIKS NV, M Barnwell Services, Technetics Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Semiconductor Seals Market is primarily defined by continuous innovation in material science, advanced manufacturing processes, and surface engineering, all aimed at achieving zero contamination and maximum resistance to highly aggressive process environments. The most critical technological advancement is the development of next-generation Perfluoroelastomers (FFKM). While standard FFKM offers excellent chemical resistance, newer grades are engineered with enhanced plasma resistance, specifically targeting highly reactive fluorinated and chlorinated plasma chemistries used in advanced dry etching processes. These advanced FFKM formulations incorporate specialized proprietary fillers and curing agents that minimize mass loss and particle generation when exposed to plasma, extending the seal life dramatically and directly contributing to higher wafer yields. Furthermore, material purity is constantly being pushed, with manufacturers employing advanced analytical techniques to ensure trace metal and organic extractables are kept at parts-per-trillion levels, a non-negotiable requirement for sub-5nm fabrication.

Manufacturing precision represents another vital technological frontier. Given the extremely tight tolerances required for seals operating in high vacuum and critical valve applications, such as slit valves and gate valves, advanced precision molding techniques are employed. Technology includes ultra-low flash compression and injection molding systems, followed by highly specialized post-processing steps like super-critical fluid (SCF) cleaning. SCF cleaning, utilizing carbon dioxide, is crucial for removing organic contaminants that standard aqueous cleaning processes cannot eliminate effectively, ensuring the seals meet the rigorous cleanliness standards required for use inside the process chamber. The trend toward bonded seals—where an elastomer is chemically bonded to a metal retainer—is also growing, improving robustness and simplifying installation in complex equipment, relying on sophisticated adhesive and curing technologies that maintain integrity under thermal cycling and vacuum conditions.

Finally, the shift toward inert and high-purity PTFE solutions and chemically stable PEEK components is diversifying the technological profile, particularly in chemical delivery and wet process applications where plasma resistance is less critical than chemical inertness and temperature resistance. PTFE seals, often chemically modified (e.g., TFM), utilize specialized fillers to improve creep resistance and mechanical strength under continuous load, mitigating deformation that could lead to leakage. Furthermore, the development of Metal C-seals and E-seals is accelerating for permanent, high-temperature, or extreme vacuum applications, leveraging advanced metal alloys and specialized surface coatings to ensure leak-tight performance. Overall, the technology landscape is highly responsive to the semiconductor process roadmap, requiring continuous, iterative material breakthroughs driven by close collaboration between seal manufacturers, chemical suppliers, and semiconductor equipment OEMs.

The most critical material is Perfluoroelastomer (FFKM), specifically ultra-high-purity grades engineered for plasma resistance. FFKM offers unparalleled chemical and thermal stability, crucial for surviving the highly corrosive, high-temperature plasma environments necessary for creating sub-5nm features without contaminating the wafer.

Miniaturization forces the use of more aggressive process chemistries and higher vacuum levels. This heightens the performance requirements for seals, increasing demand for specialty materials (like FFKM) with zero particle generation rates and improved longevity, thereby driving market value growth significantly.

The Etching application segment holds the largest market share. Etching processes (both dry plasma and wet) subject seals to the harshest operating conditions, leading to faster seal degradation and necessitating more frequent replacement or the use of higher-cost, high-performance materials, contributing significantly to revenue.

OEMs, such as Applied Materials and Lam Research, are vital intermediaries. They integrate and qualify specific seals into their process tools, effectively dictating the approved seal specifications and suppliers that foundries must use, especially for new equipment purchases and warranty maintenance.

The key restraints include the extremely high cost and long lead times associated with sourcing ultra-high-purity Perfluoroelastomer (FFKM) raw materials, coupled with the rigorous, time-consuming, and expensive qualification processes required by major foundries for new sealing component suppliers.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.