ID : MRU_ 433905 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

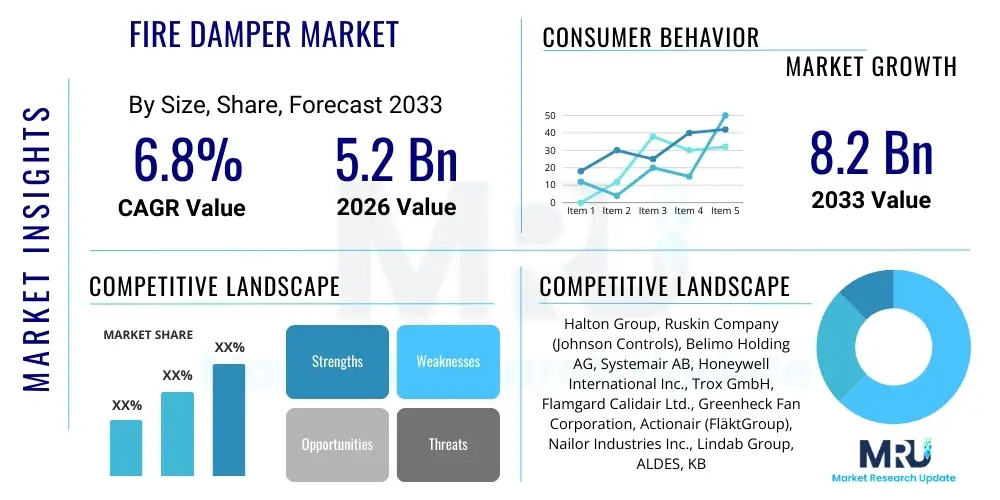

The Fire Damper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 5.2 Billion in 2026 and is projected to reach USD 8.2 Billion by the end of the forecast period in 2033.

The Fire Damper Market encompasses the manufacturing, distribution, and installation of critical passive fire protection components used primarily within Heating, Ventilation, and Air Conditioning (HVAC) systems. Fire dampers are safety devices installed in ducts and air transfer openings that penetrate fire-rated barriers, such as walls, floors, and ceilings. Their core function is to automatically close upon the detection of heat, thereby preventing the spread of fire and smoke through the ductwork system, maintaining the integrity of the fire separation, and safeguarding occupants and assets. The sophisticated engineering behind modern fire dampers allows them to operate reliably under extreme thermal conditions, utilizing mechanisms like fusible links or electromechanical actuation systems connected to building management systems (BMS).

The product landscape includes dynamic fire dampers, static fire dampers, and ceiling dampers, categorized further by their operational mechanism—namely, curtain (or guillotine) dampers and multiblade (or opposed blade) dampers. Major applications span across highly regulated sectors such as commercial infrastructure (office buildings, shopping centers), institutional facilities (hospitals, educational institutions), industrial complexes, and residential high-rises. These devices are indispensable for meeting rigorous building codes and safety standards mandated by international organizations like the National Fire Protection Association (NFPA) and the International Organization for Standardization (ISO). The increasing complexity of modern building designs, coupled with higher population densities in urban centers, continuously elevates the demand for robust and certified fire safety solutions, positioning fire dampers as a cornerstone of modern passive safety architecture.

Key market driving factors include stringent regulatory reforms enforcing mandatory fire safety installations in new construction and renovation projects globally, rapid urbanization, and significant infrastructural investment in emerging economies, particularly across the Asia Pacific region. Furthermore, heightened public awareness regarding workplace and residential safety standards, coupled with advancements in smart building technology integrating fire safety systems with centralized monitoring platforms, are contributing substantially to market expansion. The continuous development of specialized materials capable of withstanding prolonged exposure to high temperatures and improved actuation mechanisms also ensures market vitality and competitive differentiation among leading manufacturers.

The Fire Damper Market is characterized by robust growth, largely propelled by global regulatory convergence towards stricter fire safety standards and the ongoing boom in commercial and residential construction worldwide. Business trends indicate a strong move toward product differentiation through technological integration, particularly the adoption of intelligent, motorized dampers that offer remote testing, monitoring, and integration with advanced Building Management Systems (BMS). Key manufacturers are focusing on lightweight, high-performance materials and modular designs to simplify installation and reduce overall costs. Mergers and acquisitions remain a relevant strategy for established players seeking to quickly penetrate specialized regional markets or acquire niche technology capabilities, particularly in the smart safety segment, aiming for full compliance with increasingly complex certification requirements such as UL (Underwriters Laboratories) and EN (European Norms) standards.

Regionally, Asia Pacific (APAC) stands out as the primary growth engine due driven by unprecedented infrastructure development, specifically the construction of smart cities, data centers, and massive residential complexes in countries like China, India, and Southeast Asia. While North America and Europe represent mature markets, growth here is sustained by rigorous replacement cycles, continuous updates to existing building codes requiring upgrades to modern damper technology, and a high consumer propensity for premium, certified products. Market stability is underpinned by the essential nature of fire dampers—they are mandatory safety components, making demand relatively inelastic to minor economic fluctuations, though heavily dependent on the overall construction sector health.

Segment trends reveal that the motorized (electric) damper segment is achieving faster growth than traditional static/fusible link dampers due to the critical requirement for system integration and automated testing capabilities crucial for large-scale commercial structures and complex HVAC installations. By product type, the multiblade damper segment holds a significant market share due to its efficiency and applicability in high-velocity air systems. End-use demand is dominated by the commercial and institutional sectors, particularly the healthcare and hospitality industries, where continuous operation and occupant safety are paramount. Furthermore, the material segment shows a noticeable shift toward galvanized steel and stainless steel alloys engineered for enhanced corrosion resistance and higher fire rating endurance, reflecting industry focus on longevity and compliance in varied environmental conditions.

User inquiries regarding the integration of Artificial Intelligence (AI) and Machine Learning (ML) in the Fire Damper Market primarily center on predictive maintenance, smart testing automation, and enhanced real-time regulatory compliance verification. Users are keenly interested in how AI can move fire safety from a reactive measure to a proactive system, minimizing human error in inspection and guaranteeing the operational readiness of dampers. Key concerns include the initial cost of implementing AI-integrated smart dampers, the cybersecurity risks associated with networked safety systems, and the reliability of AI algorithms in complex, variable environments. Expectations focus heavily on AI-driven analytics that can detect subtle performance degradation long before failure, optimizing maintenance schedules and dramatically reducing the total cost of ownership (TCO) over the product lifecycle. The consensus anticipates that AI will not replace the core mechanical function of the damper but will revolutionize its monitoring, diagnostics, and regulatory reporting capabilities, ensuring continuous optimal safety performance.

AI is fundamentally transforming the maintenance and operational lifespan of fire dampers by enabling predictive analytics. Traditional fire damper inspection requires manual operation, which is costly, disruptive, and prone to human error. AI algorithms, fed by sensor data from smart dampers (e.g., motor current, temperature readings, cycle count, and position feedback), can establish a baseline of normal operation. Any deviation from this baseline triggers an alert, indicating potential mechanical wear or obstruction before the damper fails its next scheduled drop test. This proactive approach significantly enhances the reliability of the passive fire protection system, providing facility managers with actionable insights into necessary repairs, thus guaranteeing compliance with NFPA 80 and other critical safety standards throughout the building’s operational life.

Furthermore, AI facilitates advanced system integration within comprehensive smart building platforms. By communicating data on damper status, closure timings, and motor health to the BMS, AI systems can correlate fire damper operation with other safety assets like smoke detectors, sprinkler systems, and HVAC controls. This centralized, intelligent coordination ensures a synchronized response during a fire event, optimizing containment and evacuation protocols. The adoption of AI also streamlines the compliance process by automating the generation of mandatory inspection reports and maintaining a tamper-proof digital log of all performance tests, dramatically reducing the administrative burden and ensuring an auditable trail for regulatory bodies. This shift positions fire dampers as active, data-generating components rather than passive mechanical barriers.

The Fire Damper Market dynamics are driven primarily by stringent global safety regulations (Drivers) and the continuous expansion of the construction sector, particularly in emerging economies. Restraints include the high initial cost of advanced smart and motorized dampers, which can deter adoption in price-sensitive markets, alongside complexities related to installation and the need for highly specialized maintenance personnel. Significant Opportunities lie in the penetration of IoT and AI into the smart building segment, offering enhanced monitoring and predictive maintenance solutions, as well as exploiting the growing demand for retrofit and replacement projects in older infrastructure in developed regions. These forces collectively shape the market's trajectory, mandating constant innovation in materials and system integration while adhering to rigorous performance standards.

The primary driver is the pervasive enforcement of international and national fire safety codes, which mandates the installation of certified fire dampers in all ductwork penetrating fire barriers. Regulatory bodies worldwide are constantly updating these codes, often necessitating the replacement of older, less compliant units with advanced motorized or intumescent systems, thus fueling market demand even in mature regions. The accelerating rate of global urbanization, particularly the proliferation of complex high-rise commercial and residential buildings, further amplifies this demand, as modern structures require integrated, high-performance passive fire protection systems capable of protecting large populations over extended periods. Economic growth correlated with infrastructural spending in developing regions like Southeast Asia and the Middle East also serves as a strong market catalyst, driving new construction projects that inherently require fire damper installations.

However, market growth faces restraints, notably the intense price competition among manufacturers, which can compress profit margins, especially in the standardized product segments. Another significant hurdle is the lack of standardized installation and maintenance procedures across all regions, which can lead to compliance issues and premature system failures, discouraging investment in high-end systems. Moreover, the long lifespan of traditionally installed static fire dampers means that replacement cycles are lengthy, slowing the adoption rate of newer, smarter technologies in existing buildings unless mandated by updated legislation. Overcoming these restraints requires a combination of robust public safety education, global harmonization of installation standards, and technological innovation focused on reducing the total lifecycle cost of advanced damper systems.

The main opportunities revolve around developing and marketing smart fire dampers fully integrated with IoT technologies, offering remote diagnostics and automated testing capabilities. This segment caters directly to facility management companies seeking operational efficiency and verifiable compliance records. Furthermore, focusing on specialized applications, such as dampers designed for corrosive industrial environments (chemical plants, wastewater treatment) or high-temperature data center cooling systems, provides avenues for premium pricing and differentiation. The push for green building certifications (e.g., LEED) also presents an opportunity, as manufacturers can develop dampers utilizing sustainable materials or incorporating energy-efficient actuators, aligning safety with broader environmental responsibility goals.

The Fire Damper Market is extensively segmented based on criteria including product type, operational mechanism, material, and end-use application, providing a granular view of market dynamics and specialized demand pockets. Understanding these segments is crucial for strategic planning, allowing companies to tailor product development and marketing efforts towards specific regulatory requirements and end-user needs. The market’s segmentation reflects the variety of architectural requirements, HVAC system designs, and fire resistance durations demanded by different building classifications, ranging from simple residential installations to complex industrial complexes and high-security institutional environments.

By product type, the market distinguishes between motorized (automatic) dampers, which utilize actuators connected to fire alarm systems, and static dampers, which rely on localized temperature changes (fusible links). The operational mechanism splits the market into the ubiquitous curtain (guillotine) dampers and the more performance-oriented multiblade (or opposed blade) dampers, each suited for different airflow pressures and installation spaces. Material segmentation often differentiates between standard galvanized steel used in general commercial applications and specialty materials like stainless steel or aluminum used in corrosive environments or high-precision settings. Finally, the end-use segmentation provides insight into major revenue generators, where the commercial, institutional (healthcare, education), and industrial sectors consistently drive the largest volume and value demand, setting the pace for regulatory compliance requirements and technology adoption.

The Fire Damper market value chain begins with the upstream raw material suppliers, predominantly providers of high-grade steel (galvanized and stainless), aluminum, specialized coatings, and electrical components (actuators, sensors, fusible links). These suppliers face increasing pressure to provide materials that meet stricter thermal performance and corrosion resistance standards, which directly impacts the final product’s certification. Manufacturers then process these raw materials, engaging in precision sheet metal fabrication, assembly, and rigorous in-house testing to ensure compliance with international fire rating standards (e.g., 90 minutes, 120 minutes). This stage is capital-intensive and requires substantial investment in automated machinery and certification maintenance, distinguishing specialized fire damper manufacturers from general HVAC component producers.

The downstream segment involves complex distribution channels, encompassing direct sales, indirect sales through wholesalers, and specialized HVAC equipment distributors. Direct sales are common for large, customized infrastructure projects or governmental tenders, where manufacturers work closely with mechanical engineers and contractors. However, the bulk of sales flow through indirect channels, where distributors hold inventory and provide localized logistical support, often bundled with other HVAC safety components like smoke dampers and access doors. The final installation phase is executed by specialized mechanical contractors (M&E contractors), who are responsible for integrating the dampers into the ductwork and connecting motorized units to the Building Management System (BMS) or fire alarm control panel, a critical step that must adhere to stringent building codes and requires specialized labor.

A crucial element in the value chain is the role of certification and regulation bodies, which act as gatekeepers, ensuring product quality and safety compliance. Compliance costs are high but necessary, as an uncertified fire damper cannot be legally installed in most regulated structures. Key value addition is achieved through technological innovation (smart dampers with IoT capability) and efficient supply chain management that minimizes lead times, especially given the just-in-time nature of most construction projects. The end-users (building owners/developers) heavily rely on this chain to provide a certified product that minimizes fire risk and meets insurance requirements. Profit margins tend to be highest at the manufacturing and specialized installation stages due to the technical expertise and liability involved, compared to the distribution layer which operates on volume and efficiency.

The potential customer base for the Fire Damper Market is broad, primarily consisting of entities responsible for the design, construction, ownership, and maintenance of fire-rated buildings. These end-users are fundamentally driven by the dual mandates of regulatory compliance and the fiduciary responsibility of protecting occupants and assets. The largest volume buyers are General Contractors and Mechanical & Electrical (M&E) Engineering firms involved in large new construction projects (e.g., skyscraper office complexes, mega-malls, and university campuses), as these professionals integrate the dampers into the initial building design and installation plans.

Institutional clients, particularly healthcare systems (hospitals and clinics) and government agencies (military bases, administrative offices), represent highly reliable and often premium customers. These entities require the highest standards of fire safety, often preferring robust, highly certified, and complex motorized damper systems that integrate seamlessly with sophisticated Life Safety Systems (LSS) due to the critical nature of their operations and occupancy. The replacement and retrofit market, driven by facility managers of existing infrastructure, constitutes another significant customer segment, particularly in mature markets like North America and Europe, where older buildings require regular upgrades to meet contemporary fire codes, creating a steady, recurring demand stream for manufacturers.

Emerging consumers include operators of specialized, high-tech infrastructure such as large-scale Data Centers and Hyperscale Cloud facilities. Data centers, characterized by dense, complex cooling systems and continuous operation, require specialized fire dampers capable of isolating fire and smoke without compromising critical airflow integrity. Furthermore, the residential sector, specifically developers of multi-family high-rise housing, represents a massive volume driver, mandated by fire separation requirements on every floor and unit. These customers typically prioritize cost-effectiveness balanced with minimum regulatory compliance, driving demand for high-volume, standardized curtain-type dampers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 5.2 Billion |

| Market Forecast in 2033 | USD 8.2 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Halton Group, Ruskin Company (Johnson Controls), Belimo Holding AG, Systemair AB, Honeywell International Inc., Trox GmbH, Flamgard Calidair Ltd., Greenheck Fan Corporation, Actionair (FläktGroup), Nailor Industries Inc., Lindab Group, ALDES, KBE Fire Protection, MP3, Vostermans Ventilation, Flakt Woods Group, Elta Fans, Kruse, Fantech, Continental Fan Manufacturing Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Fire Damper Market is rapidly evolving beyond simple mechanical activation toward integrated smart safety solutions. The most significant advancement is the incorporation of Internet of Things (IoT) sensors and connectivity into motorized dampers, transforming them into "smart dampers." These devices incorporate microprocessors, position indicators, and network capabilities (often utilizing wireless protocols or BACnet/Modbus integration) that allow them to communicate their status—open, closed, or fault—in real-time to the central Building Management System (BMS) or a cloud-based maintenance platform. This enables facility managers to execute remote, automated drop tests required for mandatory inspections (NFPA 80), drastically reducing labor costs and ensuring continuous compliance without manual intervention. The precision of electronic actuation systems also allows for faster closure rates and more reliable performance compared to traditional fusible links.

Another critical area of technological focus is materials science, specifically the development of specialized alloys and intumescent coatings. Manufacturers are increasingly utilizing stainless steel and specialized galvanized coatings treated for extreme resistance to corrosion and high heat, making them suitable for harsh environments such as marine vessels, offshore platforms, and industrial processing facilities where standard steel would quickly degrade. Intumescent technology is being integrated into specific damper designs (especially for PVC or plastic ductwork systems), where the material expands exponentially upon heat exposure, sealing the gap and maintaining fire separation integrity even after the duct itself has failed. These material innovations ensure that dampers meet increasingly stringent fire resistance ratings (e.g., 2-hour, 4-hour ratings) required for critical infrastructure.

The convergence of advanced actuator technology and centralized monitoring platforms defines the modern competitive edge. Actuators are becoming smaller, more powerful, and significantly more energy efficient, reducing the overall power load on the HVAC system while increasing reliability. Furthermore, the software layer supporting these smart dampers includes sophisticated diagnostic algorithms capable of logging performance data, generating maintenance alerts based on operational wear (as discussed in the AI section), and providing detailed audit trails for regulatory compliance. This shift towards a digitally managed fire safety infrastructure is paving the way for full integration into broader smart city frameworks, where fire safety components contribute actively to the overall resilience and safety profile of urban environments, pushing the market toward higher-value, technology-enabled products.

The regional dynamics of the Fire Damper Market are heavily influenced by local construction activity, the maturity of building infrastructure, and the strictness of fire safety legislation.

A fire damper is designed primarily to block the passage of fire using fire-rated materials and automatically closes upon reaching a specific temperature (usually via a fusible link or motor). A smoke damper is engineered to restrict the passage of smoke, activated by smoke detectors, and is crucial for maintaining breathable air during evacuation. While distinct, many modern installations utilize Combination Fire/Smoke Dampers (CFSDs) which perform both functions, and local building codes, enforced globally (e.g., NFPA 90A), often mandate one or both depending on the duct penetration location and building type.

Regulatory bodies, such as the NFPA (NFPA 80 and 105), mandate specific inspection frequencies. Typically, all fire dampers must be inspected and tested (requiring them to be cycled closed and reset) one year after installation. Subsequently, inspections are required every four years for commercial buildings and every six years for hospitals and similar healthcare facilities. Documentation of these tests must be meticulously maintained and readily available for regulatory audit, a process often simplified by the adoption of smart, motorized dampers with automated logging capabilities.

The market is globally governed by two primary sets of standards: In North America, UL (Underwriters Laboratories) certification and NFPA (National Fire Protection Association) codes, particularly NFPA 80 (Fire Dampers) and NFPA 105 (Smoke Door Assemblies). In Europe, compliance relies on EN (European Norms) standards, specifically EN 1366-2 for fire resistance testing and CE marking for free trade within the European Economic Area. Adherence to these standards dictates market entry and product acceptability across major global construction markets, necessitating continuous testing and recertification by manufacturers.

Yes, motorized (dynamic) fire dampers generally offer a superior return on investment (ROI) over their lifecycle, particularly in large commercial or institutional buildings. While they have a higher upfront cost, motorized units allow for remote, automated testing and status monitoring, significantly reducing the labor and disruption associated with manual inspections. Furthermore, their integration with the Building Management System (BMS) provides immediate fault detection and verification of closure during an emergency, dramatically enhancing the overall reliability and compliance assurance of the passive fire protection system.

The Asia Pacific (APAC) region, specifically emerging economies like China, India, and Vietnam, is driving the highest growth due to unprecedented levels of urbanization and rapid infrastructure development, including high-rise commercial and massive residential construction projects. This growth is compounded by the increasing adoption and stricter enforcement of international fire safety standards, compelling new construction to integrate certified, robust fire damper solutions, thereby outpacing the steady replacement market growth observed in mature regions like North America and Europe.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.