ID : MRU_ 439694 | Date : Jan, 2026 | Pages : 257 | Region : Global | Publisher : MRU

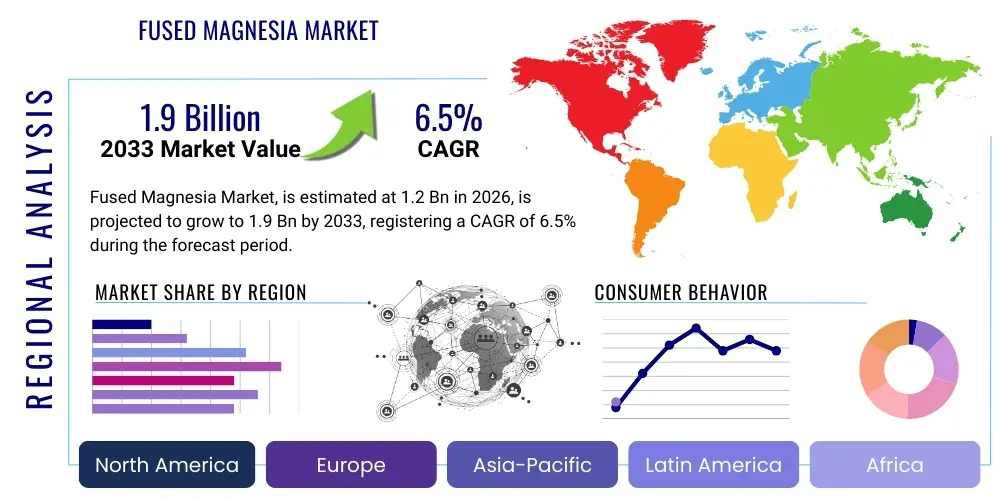

The Fused Magnesia Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 1.2 Billion in 2026 and is projected to reach USD 1.9 Billion by the end of the forecast period in 2033. This growth trajectory is underpinned by consistent demand from key industrial sectors, primarily refractories, coupled with an increasing emphasis on high-performance materials capable of withstanding extreme conditions.

The market's expansion is not only quantitative but also qualitative, driven by technological advancements aimed at enhancing the purity, density, and application-specific properties of fused magnesia. Innovations in manufacturing processes, including improvements in electric arc furnace technology and raw material beneficiation, are contributing to the availability of superior quality fused magnesia, which in turn fuels its adoption in specialized and high-value applications across various industries. The global industrial landscape's shift towards higher efficiency and longer-lasting materials plays a crucial role in this upward trend.

Fused magnesia (FM) is a high-purity, dense, and chemically stable refractory material produced by melting caustic calcined magnesia or natural magnesite in an electric arc furnace at extremely high temperatures, typically above 2800°C. This fusion process results in large, well-formed periclase crystals, which are responsible for its exceptional properties. The material exhibits a very high melting point, superior thermal shock resistance, excellent chemical stability against slag corrosion, and good electrical insulating properties at high temperatures. These characteristics make it indispensable in demanding industrial environments where extreme heat and chemical aggression are common.

The major applications of fused magnesia primarily lie within the refractory industry, where it is used in the production of high-performance refractory bricks, monolithic refractories, and tundish boards for critical applications in steelmaking, cement kilns, and glass furnaces. Beyond refractories, fused magnesia finds significant utility as an electrical insulating material in heating elements, thermocouples, and specialized ceramics due to its high dielectric strength and thermal conductivity. It also plays a role in the production of specific chemicals and advanced materials where its unique properties are leveraged for process optimization and product enhancement.

The benefits derived from using fused magnesia are multifaceted, encompassing enhanced material performance, extended product lifespan in high-temperature applications, and improved energy efficiency in industrial processes. Its exceptional resistance to thermal cycling and chemical attack significantly reduces maintenance costs and operational downtime for end-users. Key driving factors for the market include the continuous growth of global steel production, the increasing demand for high-performance refractories that offer longer service life, the expansion of the cement and glass industries, and technological advancements that enable new applications and improved material properties. Furthermore, industrialization and infrastructure development in emerging economies are creating robust demand for high-quality refractory solutions, solidifying fused magnesia's market position.

The Fused Magnesia Market is currently undergoing significant transformations, marked by several overarching business trends. These include a strategic focus by manufacturers on product differentiation through advanced purification techniques and customized formulations to meet specific application requirements, particularly in high-end refractory and electrical insulation sectors. There is a discernible trend towards consolidation among key players aiming to achieve economies of scale and expand their global footprint, alongside an increasing emphasis on sustainable production practices to mitigate environmental impact and comply with stringent regulatory frameworks. Furthermore, market participants are investing in research and development to explore new applications and improve the energy efficiency of production processes, addressing both cost pressures and environmental concerns.

From a regional perspective, the market exhibits dynamic growth patterns. Asia Pacific continues to dominate the global landscape, primarily driven by robust industrial expansion in countries like China and India, where steel, cement, and glass production capacity is steadily increasing. This region benefits from significant infrastructure development projects and a large manufacturing base. Europe and North America represent mature markets, characterized by stable demand for high-performance and specialty fused magnesia products, with a focus on technological innovation and adherence to strict quality standards. Emerging economies in Latin America, the Middle East, and Africa are showing promising growth, fueled by industrialization efforts and urbanization, which are increasing the need for refractory materials in their developing heavy industries.

Segmentation trends within the fused magnesia market highlight the enduring prominence of the refractories segment, which accounts for the largest share due to its critical role in steelmaking and other high-temperature industries. Within refractories, demand for both shaped (bricks) and unshaped (monolithic) products remains strong, with a growing preference for advanced monolithic solutions that offer flexibility and ease of installation. The electrical insulation segment is also experiencing steady growth, propelled by the expanding electronics and heating element industries, which require materials with excellent dielectric properties and thermal stability. Moreover, the market is witnessing an increased demand for high-purity fused magnesia, a premium product type crucial for advanced ceramic applications and niche electrical insulation components where purity directly correlates with performance and reliability.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Fused Magnesia Market frequently revolve around improvements in manufacturing efficiency, quality control, and supply chain optimization. Users are particularly interested in how AI can reduce energy consumption in the high-energy intensive production process of fused magnesia, enhance the consistency and purity of the final product, and provide better foresight into demand and raw material sourcing. Concerns also include the cost of AI implementation, the need for specialized skills, and the potential disruption to traditional manufacturing practices. Based on this analysis, the key themes, concerns, and expectations users have about AI's influence in this domain center on leveraging AI for operational excellence, predictive capabilities, and material innovation to achieve cost savings, superior product quality, and greater market responsiveness, while navigating implementation challenges.

The Fused Magnesia Market is significantly influenced by a dynamic interplay of drivers, restraints, opportunities, and various impact forces that shape its growth trajectory and competitive landscape. Key drivers propelling market expansion include the sustained growth in global steel production, which remains the primary consumer of fused magnesia for its critical refractory applications, alongside the robust expansion of the cement and glass industries. Furthermore, the increasing demand for high-performance refractories that offer extended service life and improved efficiency in extreme industrial environments is a significant catalyst. The ongoing industrialization and infrastructure development projects in emerging economies across Asia Pacific, Latin America, and Africa also contribute substantially to market growth by driving demand for basic industrial materials, including refractories.

Conversely, several restraints pose challenges to the market. The production of fused magnesia is an energy-intensive process, making it susceptible to volatile energy prices, which can significantly impact production costs and overall profitability for manufacturers. Stringent environmental regulations related to carbon emissions and waste disposal from industrial processes also exert pressure on producers to adopt more sustainable and costly manufacturing practices. Moreover, the market faces potential limitations from the volatile prices and availability of high-quality raw materials, primarily magnesite, which can fluctuate due to geopolitical factors, mining regulations, and extraction costs. The availability of alternative refractory materials, while not always offering the same performance profile, can also pose a competitive threat in certain applications.

Despite these restraints, ample opportunities exist for market players to foster growth and innovation. Significant potential lies in research and development activities aimed at exploring advanced applications for fused magnesia in novel industrial sectors, such as high-temperature energy storage or advanced electronics, beyond its traditional refractory uses. There is also an opportunity to develop and implement more energy-efficient production methods and technologies that can mitigate the impact of high energy costs and environmental concerns, thereby improving the market's sustainability profile. Furthermore, the growing emphasis on the circular economy and recycling initiatives for spent refractories presents an opportunity to develop processes for recycling fused magnesia, which could reduce raw material dependence and operational costs. The impact forces within the market, including the bargaining power of buyers and suppliers, the threat of new entrants, the intensity of rivalry, and the threat of substitutes, consistently shape pricing strategies, product innovation, and market consolidation trends.

The Fused Magnesia Market is comprehensively segmented to provide a detailed understanding of its diverse landscape, considering various product forms, application areas, and end-use industries. This segmentation analysis offers granular insights into demand patterns, technological preferences, and regional consumption trends, enabling stakeholders to identify key growth pockets and strategic opportunities. The market's structure reflects the specialized requirements of different industrial processes, highlighting the versatility and essential nature of fused magnesia across a broad spectrum of high-temperature and electrical applications. Understanding these segments is crucial for market participants to tailor product offerings, optimize distribution strategies, and conduct targeted marketing efforts.

The value chain of the Fused Magnesia Market begins with the upstream activities, primarily involving the extraction and initial processing of raw materials. The key raw material is natural magnesite, sourced from mines globally, which then undergoes crushing, grinding, beneficiation, and calcination to produce caustic calcined magnesia (CCM) or dead burned magnesia (DBM). These purified forms of magnesia are critical inputs for the fusion process. Upstream suppliers include mining companies, mineral processing plants, and producers of specialized equipment used in calcination and beneficiation. The quality and purity of these upstream materials significantly impact the final properties and cost of fused magnesia, making strong supplier relationships and quality control paramount.

The midstream segment of the value chain is where the actual production of fused magnesia occurs. This involves melting the calcined magnesia in high-temperature electric arc furnaces, followed by controlled cooling, crushing, and sizing to produce various grades of fused magnesia aggregates and powders. Manufacturers in this stage invest heavily in advanced furnace technologies, energy management systems, and quality assurance processes to ensure the production of consistent, high-purity fused magnesia that meets stringent industry specifications. The operational efficiency and technological sophistication of these manufacturing facilities are key determinants of a company's competitive advantage in the market.

Downstream activities involve the distribution and application of fused magnesia in various end-use industries. Fused magnesia is primarily supplied to refractory manufacturers, who then process it into shaped (bricks) or unshaped (monolithic) refractory products. It is also supplied to producers of electrical heating elements, specialty ceramics, and other industrial components. The distribution channel typically involves a mix of direct sales from large manufacturers to key industrial clients and indirect sales through a network of distributors, agents, and traders who provide warehousing, logistics, and technical support to a broader customer base. Direct channels are often preferred for large-volume, customized orders, while indirect channels serve to reach smaller clients and provide regional market access. The effectiveness of the distribution network directly influences market penetration and customer reach for fused magnesia producers.

Potential customers for fused magnesia are diverse and span a wide array of heavy industries and specialized manufacturing sectors, all of whom require materials capable of performing under extreme thermal, chemical, and electrical conditions. The primary end-users, or buyers of fused magnesia products, are predominantly large-scale industrial entities whose operational success hinges on the reliability and longevity of their high-temperature linings and components. These customers are constantly seeking materials that offer enhanced performance, reduce operational downtime, and contribute to energy efficiency, thereby driving their demand for high-quality fused magnesia that can meet increasingly stringent technical specifications.

Foremost among these potential customers are steel manufacturers, who extensively use fused magnesia in the production of refractory bricks and monolithic linings for electric arc furnaces, basic oxygen furnaces, steel ladles, and tundishes. The material's exceptional resistance to molten metal and slag corrosion is critical for maintaining the integrity of these vessels during steelmaking. Similarly, cement producers represent a significant customer segment, relying on fused magnesia-based refractories for the lining of their rotary kilns, where intense heat and abrasive conditions are prevalent. The glass manufacturing industry also heavily consumes fused magnesia for its melting furnaces due to its excellent resistance to molten glass corrosion and high-temperature stability, ensuring consistent glass quality and prolonging furnace life.

Beyond the core heavy industries, potential customers include manufacturers of electrical heating elements and components, who utilize high-purity fused magnesia for its superior electrical insulation properties at high temperatures. Companies specializing in advanced ceramics and specialty chemicals also form a crucial customer base, requiring fused magnesia for its high purity, thermal stability, and chemical inertness in their high-performance product formulations and processing equipment. Furthermore, non-ferrous metal producers, involved in the smelting and refining of metals like aluminum and copper, constitute another segment of buyers, utilizing fused magnesia for lining their furnaces and crucibles. These diverse customer profiles underscore the broad utility and indispensable nature of fused magnesia in the global industrial economy.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 1.9 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Magnezit Group, RHI Magnesita, Vesuvius plc, Imerys Refractory Minerals, Kumas Manyezit Sanayi A.S., Grecian Magnesite S.A., Jiachen Group, Dandong Jinyuan Refractories Co., Ltd., Liaoning Jinding Magnesite Group, Haicheng Houying Group, Qinghua Refractories, Liaoning Minmetals, SMW-BOF (Shanghai Minmetals Wuzhou Refractories Co., Ltd.), Magnesia GmbH, Refratechnik Group, Possehl Erzkontor GmbH, Xinyang Refractories Group, Wancheng Magnesite. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Fused Magnesia Market is continuously evolving with significant advancements in its key technology landscape, primarily focused on enhancing production efficiency, improving material purity, and expanding application capabilities. Central to this technological progress are innovations in electric arc furnace (EAF) technologies, which are the heart of fused magnesia production. Modern EAFs incorporate advanced automation, precise temperature control systems, and energy recovery mechanisms designed to reduce the exceptionally high power consumption inherent in the fusion process. These improvements aim to lower operational costs and minimize the environmental footprint by optimizing energy utilization and reducing greenhouse gas emissions, reflecting a broader industry push towards more sustainable manufacturing.

Beyond the fusion process itself, significant technological developments are observed in raw material beneficiation and purification techniques. These include advanced flotation processes, heavy media separation, and chemical purification methods that effectively remove impurities such as silica, lime, and iron oxides from raw magnesite. The goal is to achieve extremely high purity levels, which are critical for the performance of fused magnesia in demanding applications like high-end refractories, electrical insulation for heating elements, and specialized ceramics. Furthermore, sophisticated particle size distribution control technologies are being employed to customize the physical properties of fused magnesia grains, ensuring optimal packing density, reactivity, and performance characteristics for specific end-use formulations.

The technology landscape also encompasses advanced analytical and quality control methodologies that ensure product consistency and meet stringent customer specifications. Techniques such as X-ray diffraction (XRD) for phase analysis, scanning electron microscopy (SEM) for microstructural examination, and atomic absorption spectroscopy (AAS) for chemical composition analysis are routinely used. Automation and digitalization are increasingly integrated into production lines, enabling real-time monitoring, data-driven process optimization, and predictive maintenance. These technological advancements collectively contribute to the production of superior quality fused magnesia, driving its adoption in high-value applications and strengthening the market's overall competitiveness and innovation capacity.

The Fused Magnesia Market exhibits distinct regional dynamics driven by varying industrial capacities, economic development, and regulatory environments. Asia Pacific stands as the dominant force in the global market, primarily propelled by the immense manufacturing and industrial growth in countries such as China and India. These nations are characterized by burgeoning steel, cement, and glass industries that are the largest consumers of fused magnesia-based refractories. Rapid urbanization, extensive infrastructure development projects, and a favorable policy landscape for industrial expansion have significantly boosted demand for high-performance refractory materials in this region. Furthermore, local availability of raw materials and competitive production costs contribute to Asia Pacific's leading market share, making it a critical hub for both production and consumption.

Europe represents a mature yet robust market for fused magnesia, characterized by stable demand for high-quality and specialized products. Countries like Germany, Russia, and the UK are key consumers, particularly in their advanced steel, non-ferrous metals, and ceramics sectors. The European market places a strong emphasis on technological innovation, environmental compliance, and the development of energy-efficient refractory solutions. Manufacturers in this region often focus on high-purity and tailor-made fused magnesia grades to cater to niche applications and meet stringent performance standards. While growth rates might be lower compared to Asia Pacific, the consistent demand for high-performance materials and the focus on value-added products ensure a steady market presence.

North America also maintains a significant share in the fused magnesia market, driven by its established industrial base, particularly in the automotive, aerospace, and construction sectors which rely on advanced materials. The demand in the United States and Canada is stable, with a strong preference for durable and high-performance refractories that contribute to operational efficiency and reduced downtime. Latin America, along with the Middle East and Africa (MEA), are emerging markets showcasing promising growth potential. Industrialization initiatives, investments in mining and metallurgy, and infrastructure development projects in countries like Brazil, Saudi Arabia, and South Africa are gradually increasing the demand for fused magnesia, albeit from a lower base. These regions are increasingly becoming attractive for market players seeking new growth opportunities and expanding their global footprint through strategic partnerships and localized supply chains.

Fused magnesia is a high-purity, dense, and chemically stable refractory material produced by melting calcined magnesia in an electric arc furnace. Its primary use is in the manufacturing of high-performance refractories for extreme temperature applications in industries such as steel, cement, and glass, due to its exceptional resistance to heat, thermal shock, and chemical attack.

The market's growth is primarily driven by the expanding global steel, cement, and glass industries, increasing demand for high-performance refractories that offer longer service life, and significant industrialization coupled with infrastructure development in emerging economies. Technological advancements in production and application also contribute to its sustained demand.

The iron & steel industry is the largest consumer of fused magnesia, utilizing it extensively in furnace linings, ladles, and tundishes. Other major consuming sectors include the cement industry for rotary kiln linings, the glass industry for melting furnaces, and manufacturers of electrical heating elements and special ceramics for high-temperature electrical insulation.

The market offers several types of fused magnesia, mainly categorized by crystal size and purity. Key types include Large Crystalline Fused Magnesia, Medium Crystalline Fused Magnesia, Small Crystalline Fused Magnesia, and High Purity Fused Magnesia, each tailored for specific performance requirements and applications.

Environmental regulations significantly impact fused magnesia production by imposing strict limits on carbon emissions and waste disposal, necessitating substantial investments in cleaner technologies and sustainable practices. These regulations can increase production costs but also drive opportunities for developing energy-efficient processes and promoting the recycling of spent refractory materials, influencing market dynamics towards more eco-friendly solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.