ID : MRU_ 436348 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

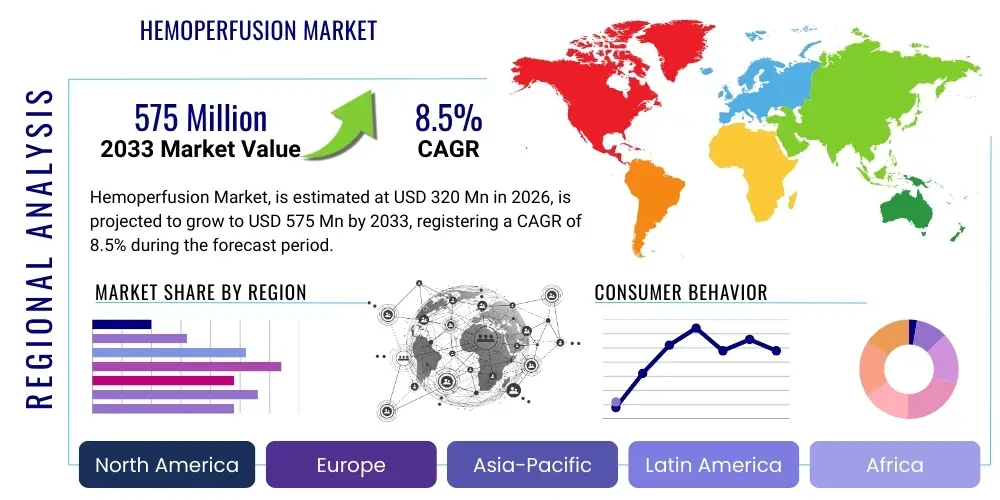

The Hemoperfusion Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at $320 million in 2026 and is projected to reach $575 million by the end of the forecast period in 2033. This growth trajectory is fundamentally driven by the rising global incidence of severe sepsis, acute poisoning, and specific autoimmune disorders requiring targeted removal of toxins, drugs, or inflammatory mediators from the blood circulation. The increasing emphasis on advanced critical care management and the ongoing development of novel, highly selective adsorbent materials are critical accelerators defining market valuation.

The valuation projection reflects significant investment in R&D aimed at developing specialized hemoperfusion cartridges. These advancements focus on improving biocompatibility, increasing adsorption capacity, and targeting specific molecular weight compounds relevant to conditions like hepatic failure (bilirubin, bile acids) and severe inflammation (cytokines). Furthermore, the integration of hemoperfusion systems into existing extracorporeal life support platforms, particularly in developed economies, contributes substantially to the overall market expansion, ensuring sustained growth across specialized hospital departments like toxicology and nephrology.

Hemoperfusion is an established extracorporeal blood purification technique used to remove toxins, drugs, and other harmful substances directly from the patient's blood by passing it over an adsorbent material. Unlike hemodialysis, which relies on diffusion and ultrafiltration across a semi-permeable membrane, hemoperfusion utilizes direct contact adsorption mechanisms. The product portfolio primarily consists of specialized adsorbent cartridges containing activated carbon, synthetic resins, or polymeric materials designed to selectively bind various endogenous or exogenous substances, ranging from small molecular poisons to mid-sized inflammatory cytokines and autoantibodies. This method is crucial in managing acute intoxication, refractory sepsis, drug overdose, and acute-on-chronic liver failure, where rapid detoxification is paramount for patient survival and recovery.

Major applications of hemoperfusion span several critical care domains. In toxicology, it is a life-saving procedure for severe drug overdose cases involving substances like paraquat, barbiturates, or tricyclic antidepressants that are poorly dialyzable. In critical care medicine, its use is expanding rapidly in treating sepsis and septic shock by mitigating the cytokine storm—a hyper-inflammatory response characterized by the excessive release of pro-inflammatory mediators. Beyond acute settings, emerging applications include the treatment of certain autoimmune diseases and specific metabolic disorders, leveraging the technology's ability to selectively remove pathogenic components from the circulatory system. The versatility and specificity of newer generation adsorbents have broadened the clinical utility significantly, moving beyond traditional poison control into complex immunomodulatory therapy.

The primary benefit of hemoperfusion lies in its high clearance rate for protein-bound or lipophilic substances that traditional hemodialysis struggles to remove effectively. Key driving factors include the rising global prevalence of drug abuse and accidental poisoning, coupled with better diagnostic capabilities leading to earlier intervention. Furthermore, substantial clinical evidence supporting the efficacy of cytokine adsorption in reducing mortality rates among critically ill septic patients is boosting procedural adoption. Technological progress focusing on developing high-flow, single-use, biocompatible cartridges with improved selectivity and minimal blood cell damage ensures the sustained positive trajectory of the global Hemoperfusion Market, supported by increasing infrastructure investments in critical care units worldwide.

The Hemoperfusion Market is characterized by robust business trends centered on technological innovation and clinical validation, particularly in the sepsis management domain. Companies are focusing heavily on developing next-generation polymeric resins and specialized carbon-based adsorbents engineered for targeted cytokine removal, responding directly to the high unmet need in critical care. Strategic collaborations between device manufacturers and large hospital networks are accelerating the integration of hemoperfusion units into standard Intensive Care Unit (ICU) protocols. Investment in manufacturing capacity expansion, particularly in the Asia Pacific region, reflects the burgeoning demand. A key business trend involves moving from broad-spectrum adsorption to highly specific cartridges, which commands premium pricing and drives increased revenue per procedure, reinforcing the market's high-value segment growth.

Regionally, North America and Europe currently dominate the market share due to advanced healthcare infrastructure, high awareness among critical care specialists, and supportive reimbursement policies for advanced blood purification therapies. However, Asia Pacific (APAC) is projected to exhibit the highest Compound Annual Growth Rate (CAGR) throughout the forecast period. This rapid regional expansion is fueled by increasing healthcare expenditure, rising incidence of poisoning and sepsis linked to dense populations, and the aggressive establishment of specialized critical care centers in countries like China and India. The regional landscape is further shaped by varying regulatory approval timelines, which influence the speed of adopting novel adsorbent technologies across different geographies, creating differential growth opportunities for market participants.

Segmentation trends indicate that the Product segment, specifically disposable cartridges, remains the largest revenue contributor due to the single-use nature and essential role in the procedure. Furthermore, the Application segment sees Sepsis and Septic Shock rapidly gaining prominence as the fastest-growing sub-segment, driven by global efforts to improve outcomes in critical illness and the robust introduction of specific cytokine adsorber products. Within the End-User segment, Hospitals are expected to retain maximum market share, primarily due to the necessity of specialized equipment, trained personnel, and the high volume of acute and emergency cases requiring immediate detoxification. These interconnected trends underscore a market pivot toward advanced, disease-specific extracorporeal treatments, optimizing efficacy and patient safety.

User queries regarding the impact of Artificial Intelligence (AI) on the Hemoperfusion Market frequently revolve around two core themes: optimizing treatment protocols and predicting patient responsiveness. Users are keen to understand if AI can personalize adsorption therapy by analyzing real-time patient data (e.g., cytokine levels, hemodynamics) to determine the optimal timing, duration, and flow rate for hemoperfusion, moving away from current standardized protocols. Concerns also focus on the potential for AI-driven diagnostic tools to accurately and rapidly identify patients in the hyper-inflammatory phase of sepsis who would benefit most from cytokine adsorption, addressing the critical time-sensitivity of the intervention. The consensus expectation is that AI integration will enhance precision medicine in critical care, making hemoperfusion interventions more timely and effective.

The integration of machine learning algorithms promises a paradigm shift in how hemoperfusion is utilized. By leveraging vast datasets collected from Electronic Health Records (EHRs) and continuous monitoring systems, AI models can identify subtle patterns indicative of impending organ failure or cytokine storm escalation. This predictive capability allows clinicians to initiate hemoperfusion preemptively rather than reactively, significantly improving therapeutic windows. Furthermore, AI can be employed to monitor the dynamic process of toxin clearance, providing feedback loops that adjust pump settings automatically, optimizing the saturation rate of the cartridge and ensuring maximum therapeutic efficiency throughout the procedure, thereby minimizing operational costs and maximizing blood purification efficacy.

In the research and development phase, AI is proving invaluable for material science innovation within the hemoperfusion sector. Advanced algorithms can simulate and predict the adsorption kinetics and biocompatibility of novel polymer structures and binding ligands, drastically speeding up the design and selection of new adsorbent materials tailored to specific targets, such as endotoxins or highly resistant bacterial metabolites. This AI-guided material engineering reduces the reliance on laborious empirical testing, accelerating the time-to-market for highly selective hemoperfusion cartridges. The overall impact of AI will be characterized by improved patient selection, procedural automation, and faster technological progression, solidifying hemoperfusion's role as a sophisticated critical care tool.

The Hemoperfusion Market is significantly influenced by a confluence of driving factors, restrictive elements, and substantial opportunities. The primary driver is the escalating global prevalence of critical illnesses, particularly severe sepsis, which necessitates rapid intervention to remove inflammatory mediators before irreversible organ damage occurs. Technological advances, especially the development of materials with high selectivity for target molecules (like bilirubin or specific cytokines), are continuously expanding the clinical applicability of hemoperfusion beyond traditional drug detoxification. Coupled with increasing awareness among critical care practitioners regarding the benefits of integrated blood purification techniques, these drivers sustain market momentum and encourage widespread procedural adoption across specialized clinical settings, ensuring a steady growth rate over the forecast period.

Restraints on market growth primarily stem from the high cost associated with hemoperfusion devices and disposable cartridges, which can limit adoption in resource-constrained healthcare environments, particularly in emerging economies. Furthermore, the requirement for highly specialized training for critical care nurses and technicians to manage the extracorporeal circulation apparatus safely and effectively poses a significant operational barrier. Regulatory hurdles and the complexity of securing favorable reimbursement status, especially for novel applications like immunomodulation in sepsis, also impede quicker market penetration. These restraining factors necessitate strategic pricing models and comprehensive training initiatives by market players to mitigate their impact on overall market access.

Opportunities for exponential market growth are abundant, chiefly revolving around expanding hemoperfusion into non-traditional areas, such as oncology for supportive care, autoimmune disease management (e.g., removing pathogenic autoantibodies), and prophylactic use in high-risk surgical settings. Crucially, the untapped potential in the Asia Pacific region, characterized by massive patient pools and improving healthcare infrastructure, represents a primary opportunity for geographical expansion. Impact forces, including stringent quality standards imposed by regulatory bodies and intensified competition leading to continuous product innovation, dictate the pace of technology adoption and standardization across global critical care units. The net effect of these DRO elements is a market moving towards greater specialization, clinical validation, and global accessibility.

The Hemoperfusion Market is comprehensively segmented based on product type, application, and end-user, providing a nuanced understanding of market dynamics and revenue generation streams. The Product segment primarily divides the market into devices (pumps, monitors) and consumables (adsorbent cartridges, tubing sets), with consumables dominating revenue due to their high volume, single-use nature. Analyzing these segments is critical for manufacturers to tailor their R&D investments, focusing resources on improving the longevity and selectivity of adsorbent materials, which are the core component driving therapeutic efficacy and patient outcomes in various clinical scenarios, including intoxication and septic shock management.

The Application segmentation reveals the diverse clinical utility of hemoperfusion, encompassing acute intoxication (drug overdose and poisoning), sepsis and septic shock, hepatic failure, and specific metabolic and autoimmune disorders. The rapid growth of the Sepsis segment highlights the increasing clinical evidence supporting targeted toxin and cytokine removal as a vital adjunctive therapy in managing life-threatening systemic inflammation. Conversely, the End-User analysis confirms that Hospitals, particularly those with advanced Intensive Care Units (ICUs) and Toxicology departments, represent the dominant purchasing segment. Specialized Clinics, focused on kidney or liver disease, constitute a smaller but growing segment demanding specialized extracorporeal treatment modalities.

The strategic value of this detailed segmentation lies in identifying high-growth pockets and areas of unmet clinical need. For instance, focusing on innovative cartridge designs for targeted removal of specific autoantibodies could unlock significant revenue in the autoimmune disease sub-segment, currently a niche area. Understanding the relative market shares of various adsorbent materials, such as activated charcoal versus synthetic resins, allows competitors to strategically position their offerings based on efficacy and cost-effectiveness. The overall market structure demonstrates a robust ecosystem where highly specialized, application-specific products are increasingly supplanting general detoxification solutions, driving premiumization within the consumable segment.

The value chain for the Hemoperfusion Market initiates with upstream activities focused heavily on specialized material procurement and R&D. This critical phase involves sourcing and refining raw materials, primarily medical-grade activated carbon and sophisticated synthetic polymeric resins. The competitiveness in the upstream segment hinges on securing materials with high adsorption efficiency, maximal biocompatibility, and minimal leaching characteristics. R&D is highly intensive here, as the development of novel ligands and surface modifications determines the clinical specificity and efficacy of the final product. Key players often invest substantial capital in proprietary adsorption technologies, creating high barriers to entry for new entrants focused solely on material provision, linking material quality directly to final therapeutic outcome and subsequent market acceptance.

Midstream activities involve the meticulous manufacturing, assembly, and quality control of hemoperfusion cartridges and associated machinery. Cartridge design requires precision engineering to ensure optimal blood flow dynamics and effective contact time between the blood and the adsorbent material without causing hemolysis or clotting. Manufacturing processes are subject to rigorous regulatory standards (e.g., FDA, CE marking), necessitating robust quality assurance systems. This stage also includes the integration of peripheral components, such as blood pumps and monitoring sensors, into unified Hemoperfusion Devices. Economies of scale play a role in device manufacturing, but the high-tech, low-volume nature of specialized cartridge production maintains significant production costs, which are ultimately reflected in the consumer price.

Downstream analysis focuses on distribution channels and end-user engagement. Distribution is primarily handled through a mix of direct sales forces, especially for large hospital systems and specialized ICU procurement, and indirect channels relying on medical equipment distributors. Due to the critical nature of the therapy, strong clinical support, installation, and ongoing maintenance training are essential components of the distribution strategy. Marketing and sales efforts are concentrated on educating critical care physicians, nephrologists, and toxicologists about clinical evidence and best practices. The efficacy of these distribution and support networks directly impacts market penetration and product adoption rates across global healthcare systems, emphasizing the need for robust, localized training programs to ensure safe and widespread use.

The primary segment of potential customers for the Hemoperfusion Market consists of advanced clinical facilities, predominantly large hospitals equipped with high-capacity Intensive Care Units (ICUs) and Emergency Departments (EDs). These institutions are the primary buyers due to the immediate, life-saving necessity of hemoperfusion in cases of acute poisoning, severe trauma, and refractory septic shock. Purchasing decisions within this segment are often driven by centralized procurement teams evaluating clinical efficacy data, total cost of ownership (including disposable costs), and compatibility with existing extracorporeal circulation equipment. Specialized care centers require robust, high-performance cartridges capable of rapid deployment and sustained performance in critical, time-sensitive environments, making them the cornerstone revenue generators for the market.

A rapidly expanding customer base includes specialized nephrology and toxicology centers, as well as standalone dialysis clinics. Nephrology centers utilize hemoperfusion for managing complications associated with chronic kidney disease, particularly where conventional dialysis proves insufficient for clearing specific uremic toxins. Toxicology centers are mandated to maintain stock of broad-spectrum hemoperfusion systems for immediate response to chemical or drug overdoses. This segment values reliability, ease of use, and a wide array of cartridge options targeting various toxins. As hemoperfusion techniques become more routine, the adoption rate among these specialized centers is rising, driven by improved patient referral pathways and standardization of acute care protocols across larger geographic regions.

The emerging potential customer segment involves research institutions and academic medical centers that integrate hemoperfusion technology into clinical trials focused on novel applications, such as targeting specific autoantibodies in autoimmune disorders (e.g., lupus, rheumatoid arthritis) or modulating the inflammatory response in complex surgical recovery. While these centers may not generate high volume sales, they play a crucial role in validating new technology, establishing clinical guidelines, and influencing future adoption rates among general hospitals. Engaging this segment requires providing specialized, adaptable systems and strong R&D collaboration support, ensuring that the next generation of hemoperfusion solutions aligns with cutting-edge medical research and addresses currently intractable clinical challenges.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $320 Million |

| Market Forecast in 2033 | $575 Million |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Jafron Biomedical, Baxter International (Gambro), Fresenius Medical Care, Kaneka Corporation, Asahi Kasei Medical, Toray Medical, CytoSorbents Corporation, Bioscience Inc., Health Light, Spectral Medical, Cerus Corporation, Aferesis Srl, Bioseparation Technology, SWS Medical Group, Beijing RZ Medical, Nikkiso Co. Ltd., Shandong Zhongbaokang Medical, Shanghai Runda Medical, HemaAdsorbents, Inc., Medica S.p.A. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The current technology landscape of the Hemoperfusion Market is dominated by advancements in adsorbent chemistry, primarily focusing on improving the selectivity and capacity of purification media. Traditional materials like activated charcoal, while effective for broad-spectrum poisoning, are being increasingly supplemented or replaced by specialized synthetic polymeric resins. These resins are chemically engineered to feature precise pore sizes and surface functionalities, allowing them to selectively capture specific target molecules, such as high molecular weight inflammatory cytokines (e.g., IL-6, TNF-alpha) or protein-bound toxins (e.g., bilirubin) while preserving essential blood components. This shift toward selective adsorption is a major technological driver, facilitating highly targeted therapies for complex conditions like sepsis and liver failure, and ensuring enhanced patient safety and reduced risk of adverse effects associated with non-selective clearance.

A significant technological innovation gaining traction is the development of immunoadsorption systems, which represent a highly specific form of hemoperfusion. These systems use ligands, such as antibodies or specific proteins immobilized onto the adsorbent matrix, to target and remove pathogenic autoantibodies or immune complexes responsible for autoimmune diseases. While more expensive and technically complex, immunoadsorption offers a precise therapeutic intervention for patients unresponsive to conventional immunosuppressive therapies. Furthermore, advancements in cartridge design are crucial; current R&D focuses on optimizing fluid dynamics within the cartridge to ensure high contact efficiency even at high blood flow rates, minimizing pressure drops and the potential for blood cell damage (hemolysis), thereby broadening the applicability of these systems in fragile critically ill patients.

Integration technology is another critical area, specifically the effort to combine hemoperfusion with other existing extracorporeal circuits, such as Continuous Renal Replacement Therapy (CRRT) or conventional hemodialysis machines. This integration allows for simultaneous removal of fluid, electrolytes, uremic toxins, and target adsorbable substances, streamlining critical care procedures and requiring less dedicated equipment. The development of next-generation devices also incorporates advanced monitoring technologies, including sensors that provide real-time data on the saturation status of the adsorbent cartridge or circulating levels of target toxins, enabling clinicians to make data-driven decisions regarding the timing of cartridge replacement or treatment cessation. These integrated, smarter systems represent the future standard for acute blood purification therapy, enhancing procedural control and therapeutic effectiveness.

North America holds a substantial share of the Hemoperfusion Market, primarily attributable to the presence of technologically advanced healthcare infrastructure, high awareness regarding advanced critical care technologies, and favorable reimbursement policies for extracorporeal blood purification therapies. The United States, in particular, drives market growth due to the high incidence of drug overdose cases requiring immediate detoxification, and significant research activity dedicated to utilizing hemoperfusion (especially cytokine adsorption systems) in treating severe sepsis. The region benefits from stringent regulatory standards that promote high-quality device manufacturing, coupled with robust clinical trial environments that swiftly validate and adopt novel technologies, maintaining its position as a key innovation hub in the global market landscape.

Europe represents another mature and significant market, driven by the strong adoption of sepsis management guidelines and the presence of several key industry players headquartered within the region. Countries such as Germany, the UK, and France exhibit high adoption rates due to well-established critical care networks and public health investments aimed at reducing sepsis-related mortality. The regulatory environment, primarily overseen by the European Medicines Agency (EMA), facilitates the faster market entry of innovative devices compared to some other regions, contributing to the quick diffusion of technologies like specialized polymeric resins for liver support and immunoadsorption systems. Ongoing collaborative research initiatives across the European Union further bolster clinical confidence and drive steady consumption growth for both devices and consumables.

Asia Pacific (APAC) is forecast to be the fastest-growing region during the forecast period. This rapid expansion is fueled by massive demographic shifts, increasing public and private healthcare expenditure, and a significant unmet need stemming from the high burden of endemic infectious diseases, poisoning, and chronic conditions like liver failure, especially in highly populated nations such as China and India. Local manufacturers in APAC are increasingly competitive, developing cost-effective alternatives to Western products, thereby expanding access to hemoperfusion systems in lower-tier cities and rural hospitals. Improving critical care standards, combined with governmental initiatives to modernize hospital infrastructure, ensures that the APAC region will play a vital role in determining the future global demand for hemoperfusion technology, offering substantial opportunities for market expansion and geographical diversification.

Hemoperfusion primarily uses direct adsorption—passing blood over a highly porous solid adsorbent (like activated carbon or polymer resins)—to remove toxins, drugs, or inflammatory mediators. Hemodialysis relies on diffusion and ultrafiltration across a semi-permeable membrane to remove small uremic toxins and excess fluid. Hemoperfusion is superior for removing large, protein-bound, or lipophilic substances that dialysis cannot clear efficiently, making it crucial for acute poisoning and cytokine removal.

The application segment demonstrating the highest growth is the treatment of Sepsis and Septic Shock. This acceleration is driven by the rising prevalence of critical infections and the proven efficacy of cytokine adsorption cartridges (e.g., utilizing polymeric resins) in reducing the hyper-inflammatory response, thereby mitigating organ damage and improving patient survival outcomes in Intensive Care Units globally.

Key technological advancements focus on enhanced selectivity of adsorbent materials, moving toward specialized synthetic resins and immunoadsorbents that target specific molecules (like single cytokines or autoantibodies). Additionally, the integration of systems with AI-driven monitoring and flow control to personalize treatment parameters and optimize cartridge performance in real-time is a major disruptive trend in the device landscape.

The Asia Pacific (APAC) region offers the most significant untapped opportunity. This is due to rapidly improving healthcare access, substantial population growth leading to higher incidence of critical illnesses, and increasing governmental investments in critical care infrastructure, particularly in developing economies such as China and India where the current penetration rate is relatively lower than in Western markets.

The primary restraints include the high total cost of the procedure, encompassing both the specialized device and the single-use adsorbent cartridges. Furthermore, the requirement for highly specialized training for critical care staff to operate and manage the extracorporeal circulation safely and effectively remains a substantial operational hurdle, limiting rapid adoption in facilities with constrained resources or insufficient training programs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.