ID : MRU_ 431617 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

The Lutein and Lutein Esters Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 350 Million in 2026 and is projected to reach USD 558 Million by the end of the forecast period in 2033.

The Lutein and Lutein Esters Market encompasses the global trade and utilization of these crucial carotenoids, derived primarily from marigold flowers (Tagetes erecta) or synthesized chemically, although natural sources dominate production due to consumer preference for clean-label ingredients. Lutein is a xanthophyll known for its antioxidant properties and its vital role in eye health, particularly in filtering harmful blue light in the macula. Lutein esters, which are fatty acid esters of lutein, offer enhanced stability and bioavailability, making them highly desirable for incorporation into various matrices, including oils and powders used in dietary supplements and functional foods. The market is fundamentally driven by the rising global awareness regarding age-related macular degeneration (AMD) and other vision impairments caused by prolonged digital screen exposure.

Major applications for lutein and lutein esters span across functional foods, dietary supplements, animal feed, and cosmetics. In functional foods, they are often integrated into dairy products, beverages, and baked goods to provide added nutritional value, catering to the health-conscious consumer base seeking preventive wellness solutions. Dietary supplements, however, remain the largest segment, offering highly concentrated doses tailored specifically for vision support, cognitive function enhancement, and skin health. The inherent benefits of these compounds—ranging from powerful antioxidant defense against free radicals to crucial support for cognitive sharpness—solidify their position as indispensable ingredients in the rapidly expanding nutraceutical industry.

Key driving factors propelling market expansion include favorable regulatory approvals allowing the use of lutein in food fortifications across developed economies, coupled with significant research validating its systemic health benefits beyond ocular protection, such as cardiovascular support. Furthermore, the global demographic shift towards an aging population, which is inherently more susceptible to vision issues, significantly bolsters demand for preventative carotenoid supplementation. Supply chain advancements focused on sustainable sourcing and improved extraction technologies, ensuring higher purity and yield, also contribute substantially to the market’s steady growth trajectory.

The global Lutein and Lutein Esters Market exhibits robust expansion, primarily steered by accelerating demand within the dietary supplement sector and intensified efforts in functional food fortification, addressing prevailing consumer trends focused on proactive health management. Key business trends highlight a strategic shift among major manufacturers towards vertical integration, controlling the supply chain from raw material cultivation (marigold flowers) to final ingredient processing, ensuring consistent quality, and stabilizing pricing structures amidst fluctuating raw material costs. Innovation in delivery formats, such as microencapsulation and specialized oil formulations designed to maximize absorption, represents another critical business trend, enhancing product efficacy and consumer appeal, particularly in high-growth markets like North America and Europe.

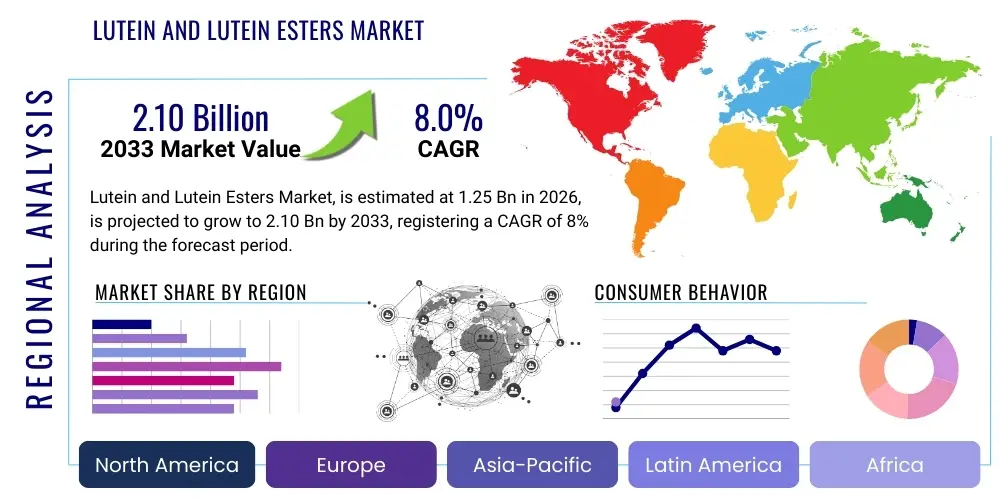

From a regional perspective, North America maintains its dominance due to high disposable incomes, significant consumer expenditure on premium health supplements, and established regulatory frameworks supporting health claims for vision-related products. Asia Pacific (APAC) is projected to register the fastest CAGR, fueled by massive population growth, increasing urbanization, rising prevalence of chronic lifestyle diseases, and growing consumer education regarding nutritional deficiencies, particularly in China and India. European regional trends emphasize stricter quality standards and a preference for naturally sourced, sustainably produced ingredients, pushing manufacturers towards achieving certifications for organic or non-GMO status, further influencing market dynamics.

Segmentation trends indicate that the natural source segment, primarily derived from marigold, will retain its market leadership, reflecting the overarching clean-label trend. However, synthetic alternatives continue to hold relevance in the animal feed and certain food coloring applications due to cost-effectiveness. Application-wise, the Eye Health segment remains paramount, though the Functional Foods and Beverages segment is rapidly gaining traction as mainstream food manufacturers integrate these ingredients into everyday consumer packaged goods. By form, powder and oil suspensions are the most favored, owing to their versatility in formulation and ease of incorporation into capsules, tablets, or liquid functional drinks, dictating current manufacturing priorities.

Users frequently inquire about how Artificial Intelligence (AI) can optimize the production, formulation, and market analysis of lutein and lutein esters, seeking understanding on AI’s role in predicting crop yields and ensuring supply chain transparency. A common thread of concern revolves around leveraging AI-driven personalized nutrition platforms to recommend specific dosages of lutein based on individual health profiles and genetic markers, thereby customizing the consumption of supplements. Furthermore, there is significant interest in using AI for advanced spectroscopic analysis during the extraction and purification phases, guaranteeing ingredient purity and detecting contaminants more efficiently than traditional methods. The key themes summarize into using AI for supply chain resilience, optimization of bioprocesses (e.g., maximizing lutein yield in marigold cultivation), and enhancing consumer personalization and predictive efficacy modeling for clinical applications.

The application of predictive analytics, a core capability of AI, is fundamentally transforming the agricultural side of the market. AI models can analyze weather patterns, soil conditions, and historical yield data to optimize marigold cultivation schedules, predicting the optimal harvest time to maximize lutein content, thereby stabilizing raw material supply and reducing waste. In the downstream processing, machine learning algorithms are being deployed to monitor fermentation or extraction processes in real-time, adjusting parameters such as temperature and solvent ratios to achieve the highest possible yield and purity of lutein esters, significantly lowering production costs and improving consistency—a critical advantage in a highly competitive ingredients market.

Moreover, AI is playing a crucial role in market intelligence and product development. By analyzing vast datasets of consumer preferences, clinical trial results, and regulatory changes globally, AI tools assist manufacturers in identifying emerging regional demands for specific dosage forms or combination products (e.g., lutein combined with zeaxanthin or omega-3s). This speeds up the product formulation lifecycle and ensures that new offerings are precisely targeted to the evolving needs of the health and wellness sector, optimizing inventory and sales forecasts based on granular predictive insights. This shift towards data-driven strategy elevates the competitive landscape within the Lutein and Lutein Esters Market.

The Lutein and Lutein Esters Market is shaped by a powerful confluence of driving forces stemming from demographic trends, consumer awareness, and technological advancements, yet it faces significant restraints centered on supply chain volatility and competitive substitutes. The primary driver is the exponentially increasing incidence of age-related eye disorders globally, exacerbated by widespread digital device usage leading to blue light exposure, which positions lutein as a critical protective supplement. Opportunities abound in leveraging personalized medicine trends, expanding applications beyond traditional eye health into cognitive and skin health, and penetrating untapped emerging markets with lower current supplement usage rates. These forces collectively dictate the strategic priorities for market participants, emphasizing sustainable sourcing and innovative formulation development to mitigate supply risks while capitalizing on burgeoning consumer health demands.

Drivers: The fundamental growth driver is the rising awareness among consumers, supported by extensive clinical evidence, regarding the prophylactic benefits of lutein against Age-Related Macular Degeneration (AMD) and cataracts. Furthermore, the global proliferation of smartphones and computers has intensified blue light exposure, prompting preventative supplementation across younger demographics. Regulatory bodies in key regions, such as the FDA and EFSA, recognizing the safety and efficacy of lutein, have facilitated its incorporation into mainstream food and beverage categories, making it accessible to a wider consumer base. The increasing elderly population, a demographic highly dependent on vision health solutions, consistently drives sustained demand for high-potency lutein products.

Restraints: Significant restraints include the volatility of raw material prices, primarily marigold oleoresin, which is highly susceptible to climatic changes and geopolitical instabilities affecting agricultural output, leading to unpredictable input costs for manufacturers. Secondly, the market faces strong competition from alternative eye health supplements, such as synthetic zeaxanthin, astaxanthin, and various omega-3 fatty acids, which sometimes possess overlapping functional claims. Additionally, challenges in product stability, particularly the degradation of lutein when exposed to heat, light, or oxygen during processing and storage, necessitate costly microencapsulation technologies, increasing the final product price and potentially limiting market penetration in cost-sensitive segments. Misinformation or lack of standardized dosage recommendations in some developing regions also hinders broader consumer acceptance.

Opportunities: Major opportunities reside in the diversification of application areas, particularly the emerging adoption of lutein in clinical nutrition products targeted at patients with chronic inflammatory conditions, owing to its potent anti-inflammatory properties. The development of novel, highly bioavailable delivery systems, such as liposomal or nanosuspension formulations, represents a key technological opportunity to enhance efficacy and distinguish premium products in a saturated supplement environment. Geographically, exploring strategic market entry into underserved regions, especially within Africa and specific parts of Latin America, where eye health awareness is rising but supplement penetration remains low, offers substantial avenues for market expansion and revenue growth in the long term.

Impact Forces: The overarching impact force shaping the market is the shift toward preventive healthcare models globally, accelerating the integration of functional ingredients like lutein into daily diets. Furthermore, rapid technological advancements in carotenoid extraction and synthesis methods improve ingredient quality and supply consistency. Regulatory harmonization efforts across different geographical regions—moving towards unified standards for labeling and health claims—also act as a powerful force, facilitating global trade and standardization. Conversely, increasing scrutiny from consumer protection agencies regarding exaggerated health claims remains an influential restraining force, pressuring companies to substantiate efficacy with robust clinical data and transparent labeling practices.

The Lutein and Lutein Esters Market is comprehensively segmented based on source, application, and form, providing a multifaceted view of market dynamics and catering to diverse industrial requirements. Source segmentation differentiates between natural and synthetic origins, reflecting consumer demand for clean-label, plant-derived ingredients versus cost-effective, high-volume production alternatives. Application segmentation dissects end-use industries, highlighting the dominant role of the dietary supplement sector while acknowledging the rapid growth in functional foods and clinical nutrition. Form segmentation addresses formulation versatility, distinguishing between high-purity powder formats preferred for solid dosage supplements and oil suspensions crucial for liquid functional products and fat-soluble food matrices. This structured analysis enables stakeholders to tailor investments and marketing efforts towards the most lucrative and rapidly evolving segments.

The dominance of the natural source segment underscores a global trend towards natural ingredients perceived as safer and more efficacious by end-users. Lutein extracted from marigold petals, particularly through advanced solvent extraction techniques, achieves high purity levels required for premium nutraceutical formulations. The market continues to observe segmentation within the application category, specifically within functional foods, where lutein integration is moving beyond specialized health bars to mainstream items like eggs (by enriching poultry feed), infant formulas, and fortified cereals, driving volume demand. The interplay between source and application dictates pricing power and competitive differentiation across various geographical jurisdictions, ensuring continuous innovation in ingredient processing.

Moreover, the distinct requirements of various end-user industries necessitate clear product differentiation based on form. For instance, the pharmaceutical industry often demands highly standardized crystalline or powdered forms for precise dosing in tablets or capsules, whereas the animal nutrition sector frequently utilizes bulk oil or powder blends. Segmentation based on purity levels also plays an implicit role, with specific clinical applications demanding higher purity standards, justifying premium pricing and specialized manufacturing processes. Understanding these intricate segment dynamics is essential for market players aiming to optimize their product portfolios and distribution channels effectively in this health-driven sector.

The value chain for the Lutein and Lutein Esters Market is complex, beginning with extensive agricultural cultivation, primarily of marigold flowers (Tagetes erecta), which represents the upstream segment. This initial phase involves specialized farming practices optimized for maximizing lutein content, followed by the crucial harvesting and drying processes. Upstream activities require significant capital investment in agricultural technology, quality seeds, and rigorous quality control measures to ensure that the raw biomass meets the requisite standards for subsequent oleoresin extraction. Key risks at this stage include weather volatility, pest infestations, and land utilization costs, which heavily influence the ultimate cost structure of the final ingredient.

The midstream segment involves the extraction, purification, and formulation of the lutein compound. Extraction typically involves solvent-based methods to obtain marigold oleoresin, which is then processed further to produce pure lutein or chemically esterified to create lutein esters. Advanced purification techniques, such as crystallization and chromatography, are necessary to achieve pharmaceutical-grade purity required for premium supplements. Formulation includes the critical steps of stabilization—often via microencapsulation or creation of oil suspensions—to protect the sensitive carotenoid from degradation, ensuring bioavailability and shelf life. This manufacturing segment is technology-intensive, dominated by specialized ingredient manufacturers holding proprietary intellectual property related to yield enhancement and stability.

Downstream activities focus on distribution and reaching the end-user. Distribution channels are bifurcated into direct sales to large, multinational supplement and food manufacturers and indirect sales through specialized ingredient distributors who service smaller formulation companies. The final products—supplements, functional foods, or animal feed—are then distributed through pharmacies, mass retailers, e-commerce platforms, and specialized health food stores. E-commerce platforms are increasingly serving as a direct sales channel, offering transparency and accessibility to consumers. Successful downstream strategy requires efficient logistics, rigorous adherence to regional labeling regulations, and strong marketing focused on educating consumers about the proven health benefits of lutein, ultimately driving sustained market pull.

The primary consumers and end-users of lutein and lutein esters are diverse, spanning multiple high-value industries, although the dietary supplement manufacturers represent the largest and most consistently growing segment. These companies procure bulk lutein ingredients in various forms (powder, oil, beadlets) for encapsulation into dedicated eye health supplements marketed directly to the aging population and proactive consumers concerned with long-term vision protection against digital strain. This customer base demands ingredients with verified purity, strong clinical backing, and often, certifications indicating sustainable and natural sourcing, justifying the premium pricing associated with high-quality lutein products.

Functional food and beverage manufacturers form the second major customer cohort, increasingly integrating lutein into products such as fortified dairy, breakfast cereals, nutritional bars, and juices. Their demand is driven by the desire to differentiate their offerings in a competitive retail environment by adding demonstrable health benefits, moving beyond basic nutrition to preventive wellness. For this sector, form stability and neutral taste profile are paramount, making stabilized oil suspensions or microencapsulated powders the preferred choice, enabling seamless integration into complex food matrices without compromising sensory characteristics.

Other significant buyers include the animal nutrition industry, where lutein is utilized, particularly in poultry and aquaculture feed, to enhance the coloration of egg yolks and fish flesh, respectively, improving product marketability. Furthermore, the burgeoning cosmetics industry is showing increasing interest, incorporating lutein into topical formulations due to its antioxidant and blue-light filtering properties, positioning it as a key active ingredient in anti-aging and skin protection creams. These varied end-users require customized product specifications regarding concentration, regulatory compliance tailored to their respective industries, and robust quality documentation demonstrating ingredient safety and traceability.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 350 Million |

| Market Forecast in 2033 | USD 558 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Kemin Industries, DSM Nutritional Products, BASF SE, Allied Biotech Corporation, Chr. Hansen Holding A/S, Naturex (Givaudan), Sensient Technologies, PIVEG, Inc., Fenchem Biotek, Lycored, Micro Ingredients, DDW, Danisco (DuPont), EID Parry (India) Ltd., Industrial Organica SA (IOSA), Xiamen Kingdomway Group, Zhejiang Medicines & Health Products Import & Export Co., Ltd., Chenguang Biotech Group Co., Ltd., ExcelVite Sdn. Bhd., Divi's Laboratories Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Lutein and Lutein Esters Market is primarily defined by advancements in extraction efficiency, stabilization methods, and bioavailability enhancement. Traditional extraction of lutein from marigold petals utilizes solvent-based methods, often involving hexane or other chemical solvents, which require careful regulation and purification steps to meet food safety standards. Current innovation focuses heavily on green extraction technologies, such as supercritical fluid extraction (SFE) using CO2, which offers a cleaner, solvent-free alternative, yielding higher purity oleoresins while reducing environmental impact. This shift addresses growing regulatory pressures and consumer demand for ingredients manufactured through environmentally sound processes, positioning SFE as a premium technology in the upstream segment.

A critical challenge in working with lutein is its susceptibility to oxidation, requiring advanced stabilization technologies to maintain efficacy and shelf life in final products. Microencapsulation is a dominant technology, involving coating the lutein particles with protective layers (like gelatin, modified starches, or specialized carbohydrates) to shield them from heat, light, and moisture. This technology allows for the creation of stable powders and beadlets that are easily incorporated into tablets and dry functional mixes. Furthermore, the development of self-emulsifying drug delivery systems (SEDDS) and specialized oil matrix formulations is crucial for Lutein Esters, which are inherently more stable but require optimizing absorption rates in the human body, directly impacting product effectiveness and consumer trust.

In the testing and quality control sphere, high-performance liquid chromatography (HPLC) remains the gold standard for accurately quantifying lutein and zeaxanthin content and purity, ensuring compliance with specifications such as the USP (United States Pharmacopeia) monograph. However, the adoption of rapid testing methodologies, including Near-Infrared Spectroscopy (NIR) and advanced mass spectrometry, is accelerating. These technologies allow for real-time monitoring of concentration during processing and swift quality verification of incoming raw materials, minimizing batch deviations and enhancing manufacturing throughput. This continuous technological refinement across cultivation, extraction, and formulation phases is crucial for maintaining competitive edge and meeting the rigorous demands of the global nutraceutical industry.

The United States serves as the epicenter for innovation and consumption, showcasing a strong preference for encapsulated supplements and fortified functional beverages. Canadian market growth mirrors the U.S. trends, albeit on a smaller scale, with a strong focus on natural health products certified by Health Canada. Market expansion strategies in this region often involve partnerships between ingredient suppliers and clinical research organizations to validate product efficacy, enhancing marketing narratives. Consumer education is highly advanced, relying on digital health platforms and professional endorsements from optometrists and nutritionists, maintaining a high market penetration rate for lutein-based products.

Furthermore, the high disposable income allows consumers to opt for specialized, combination supplements that blend lutein with other beneficial carotenoids and omega fatty acids, targeting holistic wellness beyond mere vision support. The region's technological capability ensures high stability and precise formulation of these sensitive ingredients. Regulatory adherence, especially concerning Good Manufacturing Practices (GMP) and accurate label claims, is strictly enforced, compelling manufacturers to invest heavily in quality assurance throughout the supply chain. This maturity and strict quality control reinforce North America's position as a benchmark market for the global lutein industry.

Regulatory nuances within the EU necessitate careful adaptation of product claims and labeling, requiring strong scientific justification for health benefits under Regulation (EC) No 1924/2006. This environment favors large ingredient suppliers capable of conducting extensive toxicological and clinical studies. Germany, with its strong pharmaceutical and nutritional supplement heritage, leads consumption, emphasizing high-dose, pharmaceutical-grade ingredients. The UK market is highly competitive, seeing rapid growth through online pharmacies and specialty health stores, often focusing on branded, proprietary lutein formulations that offer superior absorption.

Eastern Europe is showing accelerated growth, transitioning from traditional medicines to modern dietary supplements as economies strengthen and health consciousness rises. Manufacturers are increasingly prioritizing investment in localized clinical research specific to European demographics to bolster regional market acceptance. The European focus on sustainability also drives innovation in low-carbon footprint extraction methods and ethical sourcing practices, positioning environmental responsibility as a key competitive differentiator in this region.

China dominates regional production, being a major global supplier of marigold oleoresin and processed lutein ingredients, benefiting from large-scale, cost-efficient agricultural production capabilities. However, domestic consumption is also skyrocketing, particularly for eye health and infant formula fortification. India presents a vast, underdeveloped market, where increasing urbanization and greater health literacy are driving consumer adoption, although pricing remains a sensitive factor, favoring cost-effective supplement formats.

Japan and South Korea are mature, high-value markets that prioritize advanced, highly functional ingredients and quick regulatory approvals for 'Foods for Specified Health Uses' (FOSHU) or similar functional claims. These countries are leaders in incorporating lutein into functional beverages and sophisticated cosmetic applications. The regulatory landscape in APAC is fragmented, requiring manufacturers to navigate different standards, but the sheer volume of potential consumers makes it an essential investment destination, often leading to regional customization of product offerings.

Mexico and Brazil are the largest markets, focusing heavily on imported finished goods or locally manufactured products utilizing imported high-purity ingredients. While the region’s regulatory frameworks are often complex and decentralized, the overall trend supports the expansion of dietary supplement accessibility. Challenges include distribution logistics across large geographical areas and price sensitivity among the general population, which necessitates offering varied product lines catering to different economic strata.

The utilization of lutein in animal feed, especially for poultry and fish farming, is a significant volume driver in Latin America, capitalizing on the region's strong agricultural sector. Strategic expansion involves developing localized distribution networks and educational campaigns translated into local languages, emphasizing the value proposition of preventative eye care to overcome historical reliance on reactive treatment methods.

Growth is linked to diversifying economies away from oil dependency, leading to increased focus on modern healthcare and lifestyle product consumption. Religious and cultural preferences strongly influence product acceptance, favoring Halal-certified ingredients and packaging. South Africa is the most established supplement market in the region, exhibiting strong domestic manufacturing capabilities, often leveraging its connection with European quality standards.

Market penetration remains low in most African sub-regions due to economic challenges and limited public health expenditure. Opportunities exist in targeted public-private partnerships focusing on nutritional deficiency programs, particularly where local diets lack sufficient carotenoid intake. The market requires localized strategies addressing distribution limitations, often relying on pharmacies and specialized health clinics for product dissemination in highly regulated urban hubs.

Lutein is the free form of the carotenoid, whereas Lutein Esters are the esterified form, typically bonded with fatty acids. Esters are generally more stable and less prone to oxidation during processing and storage, but they must be cleaved by the body before absorption; free lutein is immediately bioavailable.

The primary growth driver is the dietary supplement industry, particularly for eye health (combating Age-Related Macular Degeneration and digital eye strain). Secondary growth comes from fortification in functional foods, infant formulas, and applications in the animal feed sector to enhance pigmentation.

North America currently holds the largest market share, driven by high consumer spending on health supplements, advanced regulatory frameworks, and high awareness regarding the benefits of carotenoids for vision protection.

Since the primary source is marigold flower oleoresin, which is agricultural, prices are highly susceptible to weather conditions and harvest yields. Volatility necessitates strategic risk management, including long-term sourcing contracts and investment in vertical integration to stabilize input costs.

Key advancements include green extraction methods like Supercritical Fluid Extraction (SFE) for higher purity, and stabilization technologies such as microencapsulation and advanced oil suspensions to protect the sensitive compound from degradation and improve overall bioavailability upon consumption.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.