ID : MRU_ 436503 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

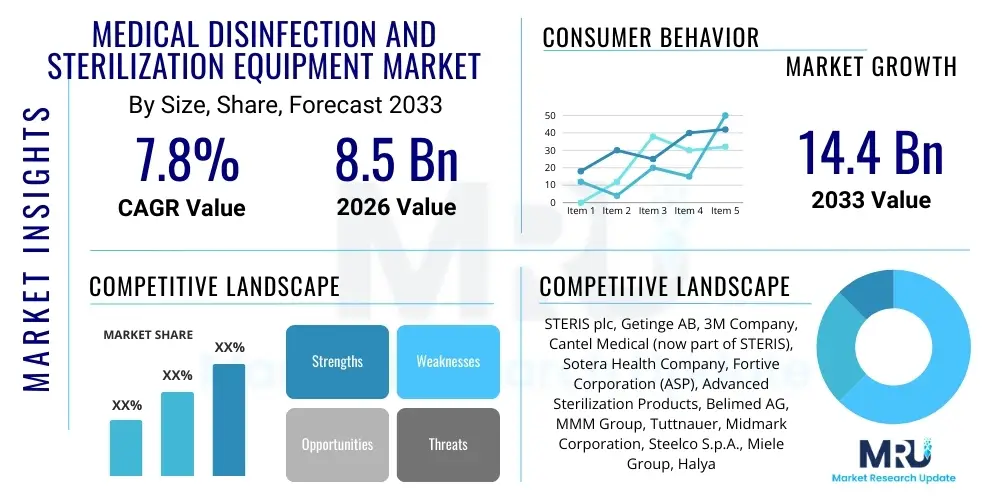

The Medical Disinfection and Sterilization Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 8.5 Billion in 2026 and is projected to reach USD 14.4 Billion by the end of the forecast period in 2033.

The Medical Disinfection and Sterilization Equipment Market encompasses instruments, consumables, and services essential for preventing healthcare-associated infections (HAIs) and ensuring patient safety across various medical settings. These critical products, ranging from large-scale sterilizers (autoclaves, ethylene oxide sterilizers) and washer-disinfectors to specialized consumables (disinfectants, sterilization wraps, indicators), are indispensable for processing reusable medical devices such as surgical instruments, endoscopes, and implants. The primary goal is the complete elimination or reduction of pathogenic microorganisms to safe levels, thereby upholding regulatory compliance and minimizing morbidity and mortality related to cross-contamination in hospitals, clinics, and ambulatory surgical centers. The stringent regulatory environment imposed by bodies like the FDA and EMA drives continuous innovation in equipment design, particularly focusing on faster cycle times, lower energy consumption, and enhanced traceability of sterilization processes.

Major applications of this equipment span surgical theaters, central sterile supply departments (CSSD), dental clinics, and diagnostic laboratories. The increasing complexity of modern medical devices, particularly heat-sensitive and minimally invasive instruments, mandates the adoption of advanced low-temperature sterilization methods, such as hydrogen peroxide gas plasma and vaporized hydrogen peroxide (VHP). Benefits derived from robust sterilization practices include significant reduction in healthcare expenditures associated with HAIs, improved operational efficiency through automated device reprocessing, and enhanced patient confidence in healthcare services. Furthermore, the global rise in surgical volumes, aging populations requiring frequent medical interventions, and the heightened awareness of infection control following global health crises are powerful underlying factors driving market expansion.

Driving factors for sustained market growth include mandatory safety standards for reprocessing complex surgical instruments, especially endoscopes, which are notoriously difficult to clean and sterilize effectively. The shift towards single-use disposable items in certain high-risk applications simultaneously influences the market dynamics, but the core need for reprocessing high-value, multi-use equipment remains paramount. Investment in upgrading aging sterilization infrastructure in developed economies and the establishment of sophisticated healthcare facilities in emerging markets further solidify the demand trajectory for advanced disinfection and sterilization technologies. Continuous technological advancements focused on integrating data logging, automation, and remote diagnostics capabilities into sterilization equipment are crucial for meeting modern workflow demands and ensuring data integrity for regulatory audits.

The Medical Disinfection and Sterilization Equipment Market is characterized by robust growth, primarily fueled by the accelerating global awareness regarding infection control and stringent regulatory mandates requiring hospitals to upgrade and validate their sterile processing workflows. Business trends indicate a strong move toward consolidated supply chains and integrated solutions, where key market players offer comprehensive packages encompassing equipment, consumables, and validation services, moving away from standalone product sales. There is a palpable shift toward environmentally sustainable sterilization methods, pushing manufacturers to innovate systems that reduce water consumption, minimize toxic chemical use, and optimize energy efficiency, aligning with broader corporate social responsibility goals and reducing operational costs for healthcare providers. Furthermore, the rapid expansion of ambulatory surgical centers (ASCs) and specialized dental clinics, which require decentralized but high-standard sterilization capabilities, presents a significant growth avenue distinct from traditional hospital procurement cycles.

Regional trends highlight North America and Europe as dominant markets, primarily due to established healthcare infrastructure, high HAI prevalence awareness, and mandatory compliance with international sterilization standards (e.g., ISO guidelines). However, the Asia Pacific (APAC) region is poised for the fastest growth, driven by massive government investment in expanding healthcare access, the proliferation of modern multi-specialty hospitals in countries like China and India, and the rising adoption of sophisticated medical procedures demanding complex sterile instrument reprocessing. Emerging economies in Latin America and the Middle East and Africa (MEA) are also showing increased adoption, often bypassing older technology generations and directly investing in automated, technologically advanced sterilization solutions to rapidly meet rising quality standards.

Segment trends reveal that the equipment segment, particularly low-temperature sterilizers, is experiencing rapid uptake due to the increasing use of heat-sensitive robotics and flexible endoscopes. Concurrently, the consumables segment remains pivotal, generating consistent revenue driven by mandatory replacement cycles for indicators, biological monitoring systems, and specialized cleaning chemistries. Within end-users, hospitals maintain the largest market share due to the sheer volume and complexity of procedures performed, but the fastest growing segment comprises the pharmaceuticals and medical device manufacturing industries, which require highly specialized, compliant sterilization methods for their final products. The focus across all segments is on achieving complete traceability and documentation, leveraging digitalization to ensure every sterilization cycle is recorded, validated, and accessible for audit purposes, thereby enhancing safety margins and reducing liability exposure.

User inquiries regarding the impact of Artificial Intelligence (AI) on the sterilization market frequently center on three core themes: operational efficiency, regulatory compliance, and predictive maintenance. Users are concerned about how AI can streamline the complex workflows within Central Sterile Supply Departments (CSSD), especially regarding instrument tracking, inventory management, and optimizing sterilization cycle parameters to reduce bottlenecks and human error. Key expectations revolve around AI's capability to analyze vast datasets generated by modern sterilizers and disinfectors to predict equipment failure before it occurs, ensuring zero downtime and continuous operation. Furthermore, there is significant interest in AI-driven automated visual inspection systems replacing manual checks for instrument cleanliness and integrity post-disinfection, thereby improving the consistency and safety of the reprocessing pathway, addressing the critical concern of ineffective cleaning being a primary cause of sterilization failure.

The initial deployment of AI in the medical disinfection space is focused less on the chemical or physical sterilization process itself, but heavily on the surrounding logistics and validation layers. AI algorithms are beginning to be integrated into instrument tracking systems (ITS) to analyze workflow patterns, identify inefficiencies, dynamically allocate resources, and prioritize instrument sets based on surgical schedules and urgency. This data-driven approach allows hospital management to optimize the utilization of high-cost sterilization equipment and labor, significantly cutting down on turnaround times and preventing surgical delays caused by instrument shortages. The predictive analytics capabilities of AI are particularly transformative, moving maintenance schedules from reactive or time-based models to condition-based monitoring, which maximizes the lifespan and reliability of complex machinery like VHP sterilizers and automated endoscope reprocessors.

The ultimate impact of AI will manifest in creating a "smart CSSD," where the entire reprocessing chain is interconnected, self-optimizing, and fully traceable. AI enhances compliance by cross-referencing sterilization records with required standards and automatically flagging deviations or incomplete documentation, minimizing the risk of regulatory non-compliance. While initial investment costs and the complexity of integrating AI platforms with existing hospital IT infrastructure pose challenges, the long-term benefits in terms of infection reduction, operational cost savings, and verifiable safety documentation position AI as an inevitable and high-impact disruptor, transitioning sterilization from a mechanical task to an intelligent, validated process.

The Medical Disinfection and Sterilization Equipment Market is driven by the confluence of mandatory health standards, demographic shifts, and rapid technological progression, while simultaneously facing constraints related to operational costs and complex regulatory adherence. The primary driver is the undeniable necessity for minimizing Healthcare-Associated Infections (HAIs), which imposes significant financial burdens and quality risks on healthcare systems globally. Regulatory bodies continually enforce stricter guidelines for device reprocessing, particularly for complex devices like flexible endoscopes, mandating the adoption of advanced, often expensive, sterilization methods and validation systems. Furthermore, the global increase in surgical procedures, driven by an aging global population and rising chronic diseases, continuously elevates the demand for sterile instruments, pushing facilities to increase capacity and efficiency in their sterile processing departments. The push for automated solutions that reduce manual handling errors and ensure reproducible results acts as a secondary but powerful driver.

However, significant restraints temper the market's trajectory. The substantial initial capital expenditure required for purchasing high-tech sterilization equipment, such as large-scale autoclaves, VHP systems, and automated endoscope reprocessors (AERs), often creates budget limitations, especially in resource-constrained public hospitals and smaller clinics. Additionally, the operational expenses associated with specialized consumables (indicators, biological media, dedicated chemistries) and the need for highly specialized technical staff to operate and validate these complex systems represent ongoing financial burdens. A critical restraint involves the perceived compatibility issues between new sterilization methods and legacy medical devices; healthcare facilities must carefully balance the need for advanced sterilization with the risk of damaging expensive, sensitive instruments, often delaying the adoption of newer technologies until device manufacturers provide explicit reprocessing validation.

Opportunities for market players are abundant, primarily revolving around the development of next-generation, environmentally sustainable sterilization technologies that address the mounting pressure to reduce the use of harmful chemicals like ethylene oxide (EtO). Miniaturized and modular sterilization units tailored specifically for the rapidly expanding Ambulatory Surgical Center (ASC) market and point-of-care settings represent a key untapped potential. Furthermore, the rising demand for comprehensive service contracts, including maintenance, validation, and advanced data analytics, offers recurring revenue streams for manufacturers, shifting the market toward a service-oriented model. The impact forces compelling growth are rooted in societal and governmental pressures for absolute patient safety, making investment in state-of-the-art sterilization technology non-negotiable for maintaining institutional reputation and accreditation.

The Medical Disinfection and Sterilization Equipment Market is highly segmented based on the type of product, the method utilized for sterilization, and the end-user setting where the equipment is deployed. This multilayered segmentation reflects the diverse requirements of the healthcare sector, ranging from high-throughput, centralized hospital sterile processing units to specialized needs in dental offices and life sciences research laboratories. The primary segments, equipment and consumables, showcase distinct market dynamics; equipment purchases are cyclical and capital-intensive, driven by regulatory updates and infrastructure expansion, while consumables represent stable, high-volume recurring revenue essential for every cycle run. The complexity of modern medical instruments dictates the continuous evolution within the sterilization method segment, driving low-temperature sterilization to prominence over traditional steam methods for sensitive materials. Understanding these segments is crucial for manufacturers to tailor product development and market strategies effectively.

Product segmentation further delineates the market into specific machinery types, such as heat sterilization equipment (autoclaves), low-temperature sterilization equipment (EtO, VHP), filtration systems, and specialized cleaning and disinfection machinery (washer-disinfectors, AERs). The effectiveness and safety profile of each technology determine its adoption rate across different clinical applications. For instance, the demand for Automated Endoscope Reprocessors (AERs) is escalating dramatically due to numerous high-profile infection outbreaks linked to improper endoscope cleaning, compelling regulatory focus and mandatory high-level disinfection protocols. The end-user analysis confirms that hospitals remain the largest consumer base due to scale, but the fastest market expansion is expected from non-hospital settings like pharmaceuticals and research institutions, which adhere to Good Manufacturing Practice (GMP) guidelines necessitating exceptionally high-standard, validated sterilization processes, often requiring customized industrial-grade equipment.

The growth within the consumables sector is noteworthy, driven by the critical function of chemical and biological indicators, sterilization packaging, and specialized cleaning enzymatic detergents. These consumables are non-negotiable components of a validated sterilization cycle, ensuring that the process parameters (time, temperature, concentration) were met and the sterility assurance level (SAL) was achieved. Market players increasingly focus on innovation within these consumables to improve ease of use, reduce monitoring time, and integrate data logging for compliance. The overall market segmentation highlights a fundamental shift towards integrated systems that combine advanced machinery, validated consumables, and digital tracking software to provide comprehensive sterility assurance solutions, mitigating risks across the entire reprocessing workflow.

The value chain for the Medical Disinfection and Sterilization Equipment Market is complex, spanning raw material sourcing, highly specialized manufacturing, rigorous distribution channels, and essential post-sales services. The upstream analysis begins with the procurement of high-grade materials, including specialized stainless steel for equipment chassis, durable plastics for consumables, and advanced chemical compounds for disinfectants and EtO cartridges. Manufacturers must adhere to stringent quality control standards at this stage, as the reliability and longevity of the equipment depend heavily on material quality, especially given the continuous exposure to high heat, moisture, and corrosive chemicals. Key upstream relationships involve suppliers of electronic components for automation and control systems, which are increasingly critical for ensuring precise cycle validation and data logging capabilities required by regulatory bodies. Innovation upstream focuses on developing less environmentally harmful chemical precursors and more resilient material designs to withstand rigorous reprocessing protocols.

The midstream involves the core manufacturing and assembly of complex sterilization units and the production of high-volume consumables. Equipment manufacturers differentiate themselves through technological patents, focusing on enhanced safety features, faster cycle times, energy efficiency, and integrating digital connectivity (IoT) for remote monitoring and diagnostics. Manufacturing activities are highly regulated, demanding ISO certifications (e.g., ISO 13485) and often country-specific regulatory approvals before market entry. Consumable manufacturers operate on high-volume production, focusing on minimizing unit cost while ensuring the accuracy and efficacy of indicators and packaging materials. Vertical integration is a notable trend, where key players acquire specialized consumable producers or service providers to gain greater control over the entire value proposition and streamline the supply of essential recurring items.

Downstream analysis focuses on distribution and end-user engagement. Distribution channels are critical and typically involve a mix of direct sales teams for large hospital capital equipment purchases and indirect channels (specialized distributors or third-party logistics providers) for reaching smaller clinics and managing the constant supply of consumables. Direct channels ensure technical expertise and detailed installation and validation services, crucial for complex machinery. Post-sales support, including equipment maintenance, calibration, mandatory annual validation services, and user training, forms a significant part of the downstream value proposition and contributes substantially to recurring service revenue. The market increasingly values bundled offerings where equipment, consumables, and services are provided under a long-term contract, ensuring optimal performance and compliance for the end-user. The ability to provide prompt, expert technical support is a major differentiator in winning long-term customer loyalty.

The core customer base for Medical Disinfection and Sterilization Equipment is overwhelmingly comprised of institutions that provide patient care or manufacture health-related products, with varying needs based on scale, regulatory environment, and procedural complexity. Hospitals, particularly large tertiary and quaternary care centers with Central Sterile Supply Departments (CSSD), represent the largest and most valuable segment. These facilities require industrial-grade, high-capacity equipment capable of handling massive volumes of instruments across diverse surgical specialties, demanding high redundancy and rapid reprocessing turnaround times. Procurement in this segment is driven by capital budgeting cycles, replacement of aging infrastructure, and adherence to evolving standards for infection control, especially in high-risk areas like cardiothoracic and orthopedic surgery.

A rapidly expanding segment of potential customers includes Ambulatory Surgical Centers (ASCs) and specialized clinics (e.g., ophthalmology, gastroenterology, dental). These facilities require compact, efficient, and user-friendly sterilization solutions that can meet high standards of practice without the infrastructure footprint of a large hospital CSSD. Their demand often leans towards automated endoscope reprocessors (AERs) and smaller, quick-cycle autoclaves suitable for decentralized operations. The procurement drivers here are efficiency, ease of operation for non-specialized staff, and minimizing compliance risk in an increasingly scrutinized outpatient environment. The rapid growth of the ASC sector globally makes this segment strategically important for future market penetration.

Finally, the industrial sector, encompassing pharmaceutical companies, biotechnology firms, and medical device manufacturers, constitutes a highly specialized and lucrative customer base. These entities require ultra-high levels of sterility assurance for final product packaging or manufacturing environments, often adhering to strict GMP and governmental pharmacopeia standards. Their needs typically involve large-scale, customized industrial sterilizers (often utilizing EtO or radiation) and advanced cleanroom disinfection protocols, prioritizing validation documentation, reproducibility, and minimal operational variability. Their procurement decisions are heavily influenced by regulatory audit requirements and the need for zero product recall risk associated with sterility failure.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 14.4 Billion |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | STERIS plc, Getinge AB, 3M Company, Cantel Medical (now part of STERIS), Sotera Health Company, Fortive Corporation (ASP), Advanced Sterilization Products, Belimed AG, MMM Group, Tuttnauer, Midmark Corporation, Steelco S.p.A., Miele Group, Halyard Health, TSO3 (A Cantel Medical Company), CISA Group, Ecolab Inc., Metrex Research, Matachana Group, Shinva Medical Instrument Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Medical Disinfection and Sterilization Equipment Market is rapidly evolving, driven primarily by the need for faster cycle times, reduced reliance on toxic chemicals, and the necessity to safely process increasingly complex and delicate medical devices. Traditional high-temperature steam sterilization (autoclaves) remains the gold standard for robust, heat-tolerant instruments due to its efficacy and cost-effectiveness. However, the dominant technological shift is toward low-temperature sterilization modalities, critical for preserving the integrity of advanced instruments containing sensitive electronics, plastics, and fiber optics, particularly those used in robotic and minimally invasive surgery. Key low-temperature technologies include Hydrogen Peroxide Gas Plasma, which offers fast cycle times and leaves non-toxic residuals, and Vaporized Hydrogen Peroxide (VHP), known for its broad material compatibility and suitability for terminal sterilization of medical devices in manufacturing settings. Manufacturers are focusing on enhancing the penetration capabilities and material compatibility of these low-temperature agents to broaden their application scope.

Significant innovation is also centered on enhancing the cleaning and disinfection stages which precede sterilization, recognizing that inadequate pre-cleaning is the primary cause of sterilization failure. This includes advanced ultrasonic cleaning systems with improved cavitation effectiveness and automated washer-disinfectors that utilize complex enzymatic detergents and validated thermal disinfection cycles. Automated Endoscope Reprocessors (AERs) represent a high-growth technological area, integrating automated leak testing, high-level disinfection (HLD) using peracetic acid or glutaraldehyde alternatives, and crucial alcohol flushing and drying cycles to prevent residual moisture contamination. The latest generation of AERs incorporates RFID tracking and data logging capabilities to ensure every step of the complex reprocessing cycle is meticulously recorded, verifiable, and compliant with updated multisociety guidelines, enhancing accountability and reducing infection risk associated with flexible scopes.

Furthermore, digitalization and connectivity are transforming sterilization equipment from standalone machines into integrated components of the hospital ecosystem. This involves the use of Internet of Things (IoT) sensors and connectivity to facilitate remote diagnostics, predictive maintenance, and seamless data transfer to hospital information systems (HIS) or specialized instrument tracking software (ITS). This integration allows CSSD managers to monitor equipment status in real-time, generate automated reports for regulatory audits, and ensure efficient workflow management. Advancements in biological and chemical indicator technologies are also critical, with a trend toward rapid readout biological indicators (ROBIs) that drastically reduce the time needed to confirm sterilization efficacy, allowing instruments to be released faster and improving surgical workflow efficiency without compromising patient safety.

The primary driver is the increasing use of complex, heat-sensitive medical devices, particularly flexible endoscopes, robotics instruments, and advanced implants containing plastics or delicate electronics, which cannot withstand the high temperatures of traditional steam autoclaves. Low-temperature methods (like VHP or gas plasma) ensure device integrity while achieving the required sterility assurance level.

Regulatory bodies such as the FDA, EMA, and ISO play a critical, pervasive role by establishing mandatory performance standards, validation protocols, and reprocessing guidelines. These mandates compel healthcare providers to continuously upgrade equipment and strictly adhere to validated cycles, directly dictating market demand for compliant, technologically advanced systems and traceability solutions.

HAIs are infections patients acquire during treatment for other conditions. Their high incidence and associated mortality and cost burden (e.g., related to C. difficile or resistant bacteria) are major market drivers. Preventing HAIs is the core objective of this industry, fueling demand for highly effective disinfection equipment, advanced sterilization monitoring, and improved training services.

While hospitals remain the largest segment, Ambulatory Surgical Centers (ASCs) and specialized medical device/pharmaceutical manufacturers are showing the fastest rate of growth. ASCs require high-throughput, efficient sterilization solutions for quick turnaround, while industrial users require validated, industrial-grade sterilizers to meet strict Good Manufacturing Practice (GMP) requirements for their final products.

IoT and AI integration primarily enhance operational efficiency and regulatory compliance. IoT enables remote monitoring and predictive maintenance, minimizing equipment downtime. AI analyzes instrument tracking data to optimize workflows, prioritize sets, and automatically verify sterilization records, drastically reducing human error and improving the overall safety and throughput of the CSSD.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.