ID : MRU_ 430511 | Date : Nov, 2025 | Pages : 246 | Region : Global | Publisher : MRU

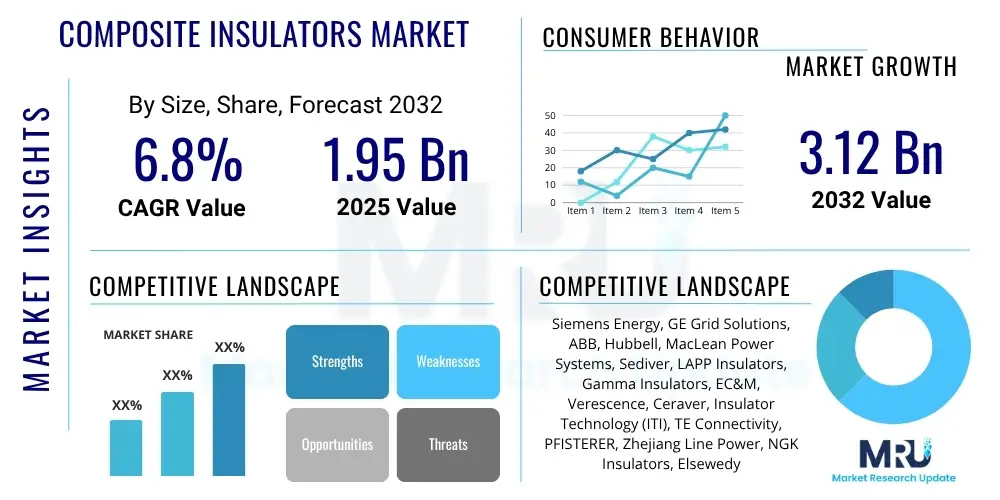

The Composite Insulators Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at USD 1.95 billion in 2025 and is projected to reach USD 3.12 billion by the end of the forecast period in 2032.

The Composite Insulators Market is experiencing significant and sustained expansion, primarily propelled by the global imperative to modernize existing electrical grids and effectively integrate an ever-increasing share of renewable energy sources into national and international power networks. These crucial electrical components are structurally distinct, typically comprising a robust fiberglass core that provides mechanical strength, encapsulated by a polymeric housing—most commonly made from advanced silicone rubber—which offers superior electrical insulation and environmental protection. This innovative design confers a multitude of performance advantages over traditional ceramic insulators, including substantially improved resistance to pollution flashover, a notable reduction in weight which eases logistical and installation challenges, and enhanced safety protocols due to their non-shattering nature, thereby establishing them as the preferred solution for contemporary and future-proof power transmission and distribution infrastructure projects worldwide.

From a product description perspective, composite insulators are meticulously engineered to serve as critical interfaces within high-voltage electrical systems, designed to both physically isolate live high-voltage conductors from ground potential and mechanical support structures, while simultaneously preventing any inadvertent or uncontrolled current leakage to earth. The meticulous design integrates the unparalleled mechanical integrity of the fiberglass rod with the exceptional electrical insulation characteristics and hydrophobic properties of the polymer housing. This synergistic combination ensures unfaltering operational reliability across an extensive spectrum of environmental exigencies, encompassing regions characterized by severe atmospheric pollution, susceptibility to seismic disturbances, or exposure to extreme climatic variations, making them indispensable for maintaining grid stability and safety.

Major applications for composite insulators are expansive and diverse, spanning vital infrastructure sectors. They are predominantly utilized in overhead power transmission and distribution lines, acting as essential supports for conductors over vast distances, and within sophisticated electrical substations to insulate various live components. Furthermore, their application extends significantly to railway electrification systems, where they are integral to the efficient and safe operation of overhead catenary systems. The myriad benefits derived from their deployment, such as their remarkably lighter weight which simplifies transport and installation procedures, significantly reduced long-term maintenance costs attributable to their self-cleaning and weather-resistant surfaces, and their improved aesthetic integration into urban and rural landscapes, collectively contribute to their accelerating global adoption. Key driving forces underpinning this market growth include the global rollout of smart grid initiatives aimed at enhancing grid intelligence and efficiency, an escalating global demand for electricity fueled by population growth and industrial expansion, and continuous, substantial investments in replacing and upgrading aging power infrastructure, especially pronounced in rapidly industrializing economies.

The Composite Insulators Market is currently shaped by a dynamic interplay of business trends that underscore innovation, operational sustainability, and strategic market consolidation. A predominant business trend involves an intensified focus from manufacturers on pioneering the development of insulators with dramatically enhanced performance parameters. This includes the engineering of components capable of handling increasingly higher voltage ratings, extending product material longevity through advanced polymer science, and integrating sophisticated smart functionalities, such as embedded sensors for real-time remote monitoring and diagnostic capabilities. Furthermore, there is a discernible strategic shift towards localizing manufacturing capabilities. This move aims to more effectively cater to distinct regional market demands, simultaneously mitigating the vulnerabilities and complexities associated with global supply chains. Parallel to these efforts, the industry is placing a strong and growing emphasis on achieving rigorous environmental sustainability goals, notably through processes geared towards carbon neutrality in production and the development of recyclable materials, reflecting a broader commitment to ecological stewardship.

From a geographical perspective, regional trends illustrate compelling growth trajectories across various global territories. The Asia Pacific region, in particular, is witnessing extraordinary market expansion, largely propelled by unprecedented rates of urbanization, rapid industrialization, and monumental government and private sector investments in renewable energy infrastructure, with prominent contributions from economic powerhouses such as China and India. Conversely, established markets in North America and Europe are experiencing sustained growth, fundamentally driven by extensive, government-backed grid modernization programs and the systematic replacement of dilapidated, aging infrastructure with more resilient, high-performance composite solutions. These regions are also characterized by a proactive stance towards achieving higher operational efficiencies in power transmission and a commitment to integrating smart grid technologies. Meanwhile, emerging economies across Latin America and the Middle East and Africa are progressively contributing to this global market expansion through a surge in new power generation projects, ambitious national electrification initiatives, and the development of inter-regional transmission corridors, signaling a robust and diversified demand landscape.

An in-depth analysis of segment trends within the Composite Insulators Market reveals distinct patterns of growth and adoption. Suspension insulators continue to command a substantial market share, primarily attributed to their ubiquitous application in extensive overhead transmission lines, where their flexibility and lightweight advantages are highly valued. Concurrently, post insulators are demonstrating accelerated market penetration, particularly within substation environments, where their inherent robust structural support and compact design offer significant operational benefits. When examined by voltage level, the high voltage (HV) and extra high voltage (EHV) application segments are not only the largest but also the fastest-growing sub-sectors. This expansion is directly correlated with the global proliferation of long-distance power transmission networks, including inter-country and inter-continental grid connections. In terms of application, the power transmission and distribution sector remains the preeminent revenue generator, forming the bedrock of demand. However, railway applications are also exhibiting consistent and encouraging growth, as governments globally commit to electrifying their extensive rail networks to enhance operational efficiency, reduce reliance on fossil fuels, and diminish carbon emissions, thereby broadening the market's foundational demand base.

Common user inquiries concerning the influence of Artificial Intelligence on the Composite Insulators Market frequently underscore how AI functionalities can revolutionize critical operational aspects, including the enhancement of predictive maintenance protocols, the optimization of intricate design and manufacturing processes, and the overarching improvement in the reliability and resilience of electrical grids. A central theme emerging from these discussions is the transformative potential of AI to meticulously analyze vast datasets generated from smart insulators. This analytical capability enables the proactive forecasting of potential failures, thereby drastically minimizing unscheduled downtime, reducing catastrophic equipment failures, and significantly lowering long-term operational and maintenance expenditures. Furthermore, there is considerable interest and expectation regarding AI's application in advanced material science research, specifically for accelerating the development of innovative, next-generation polymer compounds that offer superior durability and performance. Similarly, AI is anticipated to play a pivotal role in optimizing complex production lines, leading to heightened manufacturing efficiency, reduced material waste, and improved product consistency. Users widely anticipate that AI will herald a paradigm shift towards more intelligent, self-healing, and largely autonomous grid management systems, where composite insulators, augmented with AI-powered sensors, will serve as indispensable, data-gathering nodes contributing to a comprehensively interconnected and optimized electrical infrastructure.

The Composite Insulators Market is currently undergoing a transformative period, profoundly shaped by a intricate confluence of inherent drivers, persistent restraints, emerging opportunities, and pervasive impact forces that collectively dictate its developmental trajectory. A primary and overwhelmingly influential driver is the accelerating global transition towards more sustainable and diversified energy portfolios, specifically the widespread adoption and integration of renewable energy sources such as expansive solar farms, offshore and onshore wind power installations, and increasingly, tidal energy projects. This energy transition inherently necessitates the construction of robust, highly reliable, and often long-distance transmission infrastructure to efficiently transport generated power from geographically diverse and often remote sites to densely populated load centers. In this context, the inherent lightweight properties, superior pollution performance, and enhanced resilience to extreme weather conditions of composite insulators render them exceptionally advantageous and often indispensable for these new and upgraded power lines, directly fueling substantial market demand. Concurrently, extensive government and utility-led initiatives across the globe are keenly focused on modernizing and fortifying aging power grids, particularly in developed economies. These modernization efforts aim to replace legacy infrastructure with more advanced, resilient, and higher-performing insulating solutions that promise enhanced operational reliability, significantly reduced maintenance burdens over their extended operational lifespans, and improved overall grid efficiency, further cementing the market position of composite insulators.

Despite the strong tailwinds, the market is not without its notable restraints. A significant challenge stems from the inherent volatility in the global prices of key raw materials, particularly advanced silicone rubber polymers and fiberglass composites. These fluctuations can exert considerable pressure on manufacturing costs and subsequently compress profit margins for composite insulator producers, necessitating agile supply chain management and strategic procurement. While composite insulators demonstrably offer substantial long-term cost benefits derived from reduced maintenance and extended service life, their initial capital investment can sometimes be perceived as higher when directly compared to conventional ceramic alternatives. This initial cost differential can occasionally present a budgetary hurdle for certain utilities or project developers operating under tight financial constraints or adhering to conservative investment policies. Furthermore, the industry operates within a highly regulated environment, characterized by stringent international and national standards, as well as the imperative for rigorous testing and certifications for high-voltage electrical components. Navigating these complex regulatory landscapes and achieving multiple certifications can pose formidable challenges for both established market players and new entrants, requiring substantial and continuous investments in research and development, quality assurance, and compliance efforts, which can slow down innovation and market entry.

Notwithstanding these restraints, substantial and exciting opportunities are continually emerging and evolving, promising further market expansion. The ongoing and projected expansion of High Voltage Direct Current (HVDC) transmission lines represents a particularly fertile ground for growth. HVDC technology is rapidly gaining prominence as the most efficient and practical method for bulk power transfer over very long distances, for interconnecting asynchronous grids, and for integrating large-scale renewable energy projects. Composite insulators are ideally suited for these demanding applications due to their high performance characteristics under DC voltage stress. The burgeoning global movement towards smart grid initiatives also presents a profound opportunity for composite insulators that are intelligently designed with integrated sensing, monitoring, and communication capabilities. These "smart" insulators can provide real-time condition assessment, facilitate early fault detection, and enable advanced asset management, thereby becoming critical data-generating nodes within a smarter, more responsive grid. Additionally, the rapid and sustained pace of industrialization and urbanization across burgeoning economies in Asia, Africa, and Latin America is driving an unprecedented need for the construction of entirely new power infrastructure, offering expansive greenfield opportunities for composite insulator deployment. Concomitant impact forces such as relentless technological advancements in advanced material science, an escalating global awareness of environmental concerns that promotes the adoption of durable and sustainable infrastructure components, and a period of sustained global economic growth continue to exert a powerful and positive influence, perpetually pushing the boundaries for innovation and accelerating the wider adoption of composite insulators across diverse electrical applications.

The Composite Insulators Market is meticulously segmented across multiple critical dimensions, including the specific insulator type, the operational voltage level, the end-use application, and the constituent material composition. This comprehensive segmentation methodology is fundamental for acquiring a granular and insightful understanding of the nuanced market dynamics, enabling both strategic forecasting and targeted business development initiatives. Such a detailed breakdown provides invaluable clarity regarding which specific product categories, within particular voltage ratings, catering to distinct end-use sectors, and manufactured from certain material compositions, are currently experiencing the most pronounced growth trajectories and highest rates of adoption. Consequently, this granular market intelligence is indispensable for manufacturers to strategically align and tailor their product portfolios to meet evolving market demands, for power utilities and project developers to make well-informed and optimized procurement decisions that ensure long-term reliability, and for potential investors to accurately identify high-potential, lucrative sub-segments within the broader market landscape. The ability to disaggregate the market in this manner allows stakeholders to not only react to current trends but also to anticipate future shifts, fostering a more agile and competitive market environment.

The intricate value chain within the Composite Insulators Market is a meticulously structured progression, beginning with the fundamental sourcing of raw materials and culminating in the final deployment and operation of the product in diverse end-use applications. This chain involves several distinct yet interconnected stages and a multitude of essential stakeholders who collectively contribute to the product's journey to market. The initial stage, often termed upstream analysis, centers on the diligent procurement of foundational components that are absolutely essential for the precise manufacturing of composite insulators. This critical phase primarily involves securing high-grade fiberglass rods, which are instrumental in providing the unparalleled mechanical strength and structural integrity characteristic of these insulators. Equally important is the acquisition of various sophisticated polymer materials, predominantly silicone rubber, but also including EPDM or other proprietary composite compounds, which are meticulously molded to form the weather sheds and provide the primary layer of electrical insulation and environmental protection. Furthermore, the reliable sourcing of precisely engineered metal end fittings, typically fabricated from robust galvanized steel or specialized aluminum alloys, is paramount for securely connecting the insulator to both the live power line conductor and its supporting structural framework. The consistent quality, timely availability, and cost-effectiveness of these foundational raw materials directly and profoundly influence the ultimate performance attributes, manufacturing efficiency, and final market pricing of the composite insulator product, making strong supplier relationships a competitive advantage.

Progressing through the value chain, the midstream activities encompass the highly specialized and technical processes of manufacturing and assembly. This pivotal stage involves the meticulous design, precision molding, high-pressure injection, and secure crimping of the various composite insulator components. During these processes, raw materials are expertly transformed into fully functional, high-performance electrical apparatus through the application of advanced engineering principles and sophisticated production techniques. Stringent and continuous quality control measures, comprehensive electrical and mechanical testing protocols, and rigorous adherence to international and national certification standards (such as IEC, ANSI, and others) are absolutely paramount at this stage. These critical steps ensure that every manufactured insulator not only meets but often exceeds the most demanding utility specifications and industry benchmarks for reliability, safety, and operational longevity. Any deviation in quality at this stage can have profound implications for grid stability and safety, emphasizing the non-negotiable importance of robust manufacturing practices and comprehensive validation.

The downstream analysis then meticulously examines the distribution, logistics, and ultimate deployment of the meticulously manufactured composite insulators. This crucial phase involves strategically reaching the diverse array of end-users through a variety of well-established distribution channels, which can be broadly categorized as either direct or indirect. Direct channels typically entail direct engagement between composite insulator manufacturers and large-scale power utilities, major Engineering, Procurement, and Construction (EPC) contractors, and national railway companies. These engagements often involve long-term supply agreements, customized product solutions tailored to specific project requirements, and direct sales teams providing technical support. Conversely, indirect distribution channels leverage an extensive network of regional distributors, specialized agents, and local strategic partners. These intermediaries are vital for facilitating sales to smaller municipal utilities, diverse industrial clients, and various maintenance service providers, particularly in regions where direct manufacturer presence is less feasible or where localized logistical and technical support is critically required. The efficiency, reliability, and breadth of these distribution networks are absolutely crucial for ensuring the timely and secure delivery, as well as the professional installation, of insulators. This seamless integration into the power infrastructure is indispensable for maintaining the uninterrupted continuity and unwavering reliability of electricity supply networks and other critical electrical systems globally, highlighting the interconnectedness of the entire value chain for market success.

The core demographic of potential customers and ultimate buyers for composite insulators is remarkably broad and encompasses a spectrum of entities that are fundamentally engaged in the generation, efficient transmission, and reliable distribution of electrical power, alongside those operating extensive and critical electrical infrastructure across various industrial and public sectors. At the forefront of this customer base are the myriad power utilities, both publicly owned entities and privately operated corporations, which represent the largest and most consistent segment of purchasers. These utilities are perpetually involved in the expansion of their vast electrical networks, the systematic upgrading of their existing infrastructure to meet evolving demands, and the rigorous maintenance of operational reliability across their entire service areas. Consequently, they are continuous and significant procurers of composite insulators for a wide array of applications, including extensive overhead power lines, complex electrical substations, and various other high-voltage electrical apparatus. Their procurement decisions are fundamentally driven by an ever-increasing global demand for electricity, the urgent necessity to replace aging and less efficient components within their grid, and strict regulatory mandates that compel them to enhance grid resilience, safety, and environmental performance.

Another critically important and rapidly growing customer segment comprises Engineering, Procurement, and Construction (EPC) companies. These specialized firms bear the comprehensive responsibility for the design, construction, and ultimate commissioning of large-scale power projects. This often includes the establishment of new, high-capacity transmission lines spanning vast distances, the construction of intricate substations, and the development of large-scale renewable energy generation facilities such as expansive solar parks and towering wind farms. EPC contractors procure composite insulators as absolutely integral components within their overarching project scope, frequently necessitating adherence to highly specific technical specifications, stringent quality standards, and often, very aggressive project timelines. Their purchasing decisions are profoundly influenced by a complex evaluation of product performance characteristics, the overall cost-effectiveness over the project lifecycle, the proven reputation of manufacturers for delivering reliable products, and their demonstrable capability to adhere to strict delivery schedules, making supplier reliability a paramount concern in their selection process.

Beyond the traditional confines of the power generation and transmission sector, railway operators constitute an increasingly vital and expanding segment of potential customers for composite insulators. Propelled by a pervasive global impetus towards railway electrification, aimed at fostering cleaner, more efficient, and sustainable public transportation systems, composite insulators are experiencing accelerated adoption for the critical overhead catenary systems that power electric trains. These insulators offer compelling advantages such as their inherently lightweight design, which simplifies installation and reduces structural loads, coupled with their exceptional resistance to the often-harsh and dynamic environmental conditions encountered along railway corridors. Furthermore, large-scale industrial complexes that necessitate robust and fail-safe electrical isolation for their intricate internal power distribution systems also represent a steadfast and continuous customer base. This includes heavy manufacturing plants, extensive mining operations, and expansive commercial facilities. Finally, developers of renewable energy projects, particularly those involved in the construction and operation of solar and wind farms, are significant buyers. They require high-performance, durable composite insulators to reliably connect their geographically dispersed generation facilities to the existing national and regional electricity grids, ensuring efficient and stable power evacuation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 1.95 billion |

| Market Forecast in 2032 | USD 3.12 billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Siemens Energy, GE Grid Solutions, ABB, Hubbell, MacLean Power Systems, Sediver, LAPP Insulators, Gamma Insulators, EC&M, Verescence, Ceraver, Insulator Technology (ITI), TE Connectivity, PFISTERER, Zhejiang Line Power, NGK Insulators, Elsewedy Electric, Shreem Electric, Dalian Insulator, Bharat Heavy Electricals Limited (BHEL), Aditya Birla Insulators, Alstom Grid (now part of GE Grid Solutions) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Composite Insulators Market is characterized by continuous innovation and rapid evolution, propelled by ongoing advancements in material science, sophisticated manufacturing processes, and seamless integration with emerging smart grid paradigms. A central and profoundly influential aspect of this technological progression resides in the relentless development and refinement of advanced polymer materials, with particular emphasis on silicone rubber formulations. Researchers and material scientists are intensely focused on engineering new and improved compounds that exhibit dramatically enhanced hydrophobicity—preventing water film formation—superior resistance to ultraviolet (UV) radiation, exceptional tracking and erosion resistance even under severe arcing conditions, and extended operational longevity. The objective is to produce materials capable of enduring increasingly aggressive environmental conditions, thereby significantly prolonging the product lifespan, drastically reducing maintenance cycles, and delivering unparalleled electrical performance. Furthermore, pioneering innovations in nanocomposites and various hybrid material systems are steadily gaining significant traction, with a clear aim to further bolster the mechanical strength and lighten the overall weight of insulators, all while meticulously preserving or even enhancing their already outstanding electrical insulation properties. This quest for advanced materials is fundamental to pushing the boundaries of insulator performance.

Complementing these material science breakthroughs, advanced manufacturing technologies play an absolutely pivotal role in ensuring the consistent quality, high performance, and structural integrity of composite insulators. Specialized production techniques such as high-precision injection molding for fabricating the weather sheds, robust crimping methods for securely attaching the metal end fittings, and advanced pultrusion processes for producing high-strength fiberglass rods are under constant refinement. These continuous improvements are aimed at optimizing manufacturing efficiency, minimizing production defects, reducing material waste, and facilitating the scalable production of insulators for increasingly higher voltage applications. The pervasive trend towards greater automation in assembly lines, coupled with the strategic deployment of advanced robotic systems, is becoming increasingly prevalent across the industry. This shift is leading to the attainment of significantly higher levels of manufacturing precision, unparalleled product consistency, and substantial reductions in direct labor costs. Moreover, the implementation of sophisticated non-destructive testing (NDT) methodologies, including advanced ultrasonic inspection, X-ray analysis, and highly precise electrical testing protocols, is critically important. These rigorous testing regimes are indispensable for comprehensively guaranteeing the inherent reliability, uncompromising safety, and long-term performance of every single finished product before it is cleared for deployment into critical power infrastructure, underpinning the industry's commitment to quality.

The most transformative trend currently shaping the market's technological frontier is the profound integration of smart technologies into composite insulators. This includes the strategic embedding of highly sensitive and intelligent sensors directly within the insulator body, designed for the real-time monitoring of a diverse array of critical operational parameters. These parameters typically include leakage current levels, precise temperature readings, the extent of surface pollution accumulation, and even mechanical stress. These "smart" insulators are engineered with advanced communication capabilities, allowing them to wirelessly transmit vital operational data directly to central grid operators or cloud-based analytics platforms. This unprecedented flow of real-time data enables sophisticated predictive maintenance strategies, facilitates the early and accurate detection of potential faults, and supports highly optimized asset management programs. This dynamic convergence of cutting-edge material science, highly efficient advanced manufacturing processes, and sophisticated digital intelligence is fundamentally transforming composite insulators from passive, static components into active, intelligent, and data-generating elements within the broader architecture of modern smart grids. This evolution is not merely incremental but represents a significant paradigm shift, ultimately contributing to dramatically enhanced grid resilience, improved operational efficiency, reduced outage times, and a more sustainable and responsive electrical power ecosystem for the future.

Composite insulators are advanced electrical components primarily consisting of a high-strength fiberglass core, an outer housing typically made of hydrophobic polymer (like silicone rubber), and metal end fittings. They are increasingly preferred over traditional ceramic insulators in modern power grids due to several superior attributes: their significantly lighter weight simplifies handling and installation, they offer exceptional resistance to pollution flashover and harsh environmental conditions, possess higher mechanical strength-to-weight ratio, exhibit improved seismic performance, and require considerably less maintenance, all contributing to enhanced grid reliability and reduced operational costs.

The Composite Insulators Market is primarily driven by global grid modernization initiatives aimed at enhancing efficiency and resilience of power infrastructure, the escalating worldwide integration of renewable energy sources (such as wind and solar) which often necessitate new transmission lines, rapid urbanization and industrialization particularly in developing economies demanding expanded power networks, and the inherent superior performance characteristics of composite insulators, including their longevity and reduced environmental impact. Additionally, government investments in smart grid technologies and electrification programs further accelerate market expansion.

Artificial Intelligence is projected to profoundly impact the Composite Insulators Market by enabling advanced predictive maintenance capabilities through the analysis of real-time data from smart sensors embedded in insulators, thereby preventing costly failures and minimizing downtime. AI will also optimize material design and manufacturing processes, leading to the development of more durable and efficient insulators with reduced production waste. Furthermore, AI-powered systems will facilitate automated inspection using drones and enhance overall grid intelligence by integrating insulator health data into broader asset management platforms, significantly improving operational efficiency and grid reliability.

Composite insulators find extensive applications predominantly in three key sectors: high-voltage power transmission and distribution lines, where their lightweight and superior insulating properties are crucial for long-distance power transfer and grid stability; railway electrification systems, specifically for supporting overhead catenary lines due to their robust performance in dynamic and often polluted environments; and various industrial facilities that require reliable high-voltage insulation for their internal power systems. Their adaptability to diverse harsh conditions and reduced maintenance requirements make them ideal for these critical infrastructures.

The primary challenges restraining the Composite Insulators Market include the volatility in the prices of key raw materials like silicone rubber and fiberglass, which can impact manufacturing costs and profitability. Additionally, while offering long-term savings, the initial capital investment for composite insulators can sometimes be higher compared to traditional ceramic options, posing a barrier for some buyers. Furthermore, stringent regulatory standards and the necessity for rigorous testing and certification processes for high-voltage components can increase development costs and extend market entry timelines for new products.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.