ID : MRU_ 427394 | Date : Oct, 2025 | Pages : 248 | Region : Global | Publisher : MRU

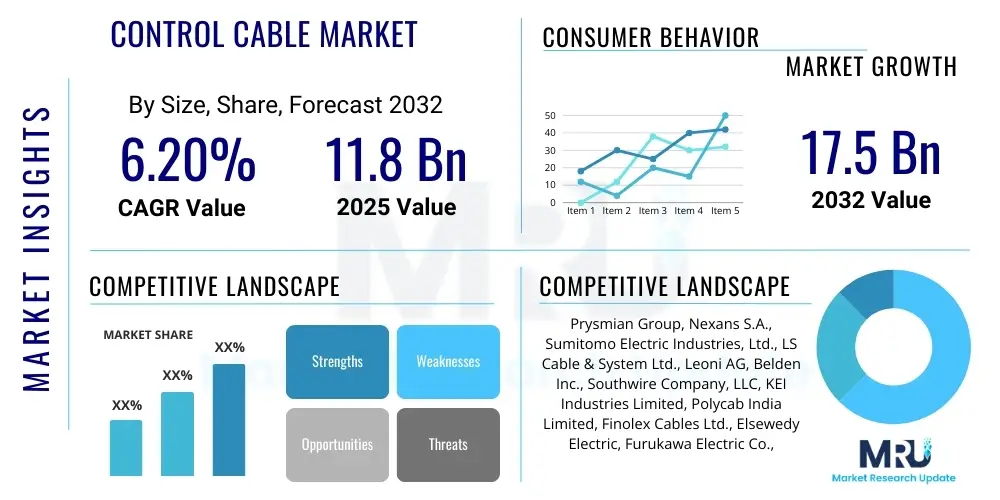

The Control Cable Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2032. The market is estimated at USD 11.8 Billion in 2025 and is projected to reach USD 17.5 Billion by the end of the forecast period in 2032.

The global control cable market is a critical component of modern industrial and infrastructural development, facilitating the precise transmission of signals for monitoring, control, and automation processes. These specialized electrical cables, typically designed for low-voltage applications, are integral to the seamless operation of complex machinery, robust communication networks, and intelligent building systems across diverse sectors. Their core function involves carrying command signals and data, rather than high power, ensuring the accurate and timely response of connected equipment. As industries worldwide increasingly adopt automation and smart technologies, the demand for reliable and high-performance control cables continues to escalate, underpinning the efficiency and safety of operational environments.

Control cables are engineered with specific characteristics to meet the demanding requirements of various environments, including resistance to chemicals, oil, abrasion, and extreme temperatures, along with enhanced flexibility for dynamic applications. They commonly feature multiple insulated conductors within a protective outer sheath, often with shielding to mitigate electromagnetic interference (EMI) and radio frequency interference (RFI), thus ensuring signal integrity. Major applications span manufacturing, energy generation and distribution, transportation, construction, and telecommunications. The benefits derived from these cables include improved operational efficiency, enhanced safety protocols, reduced downtime due to reliable signal transmission, and the ability to integrate complex control systems effortlessly.

Several key factors are driving the robust expansion of the control cable market. Foremost among these is the accelerating pace of industrial automation, including the proliferation of robotics and advanced manufacturing techniques across sectors such as automotive, electronics, and pharmaceuticals. The global thrust towards smart infrastructure, smart cities, and the integration of IoT devices in commercial and residential buildings further fuels demand. Additionally, the expansion of renewable energy projects, requiring sophisticated control systems for wind turbines, solar farms, and grid management, significantly contributes to market growth. These interconnected drivers underscore the indispensable role of control cables in the evolving technological landscape, cementing their position as foundational elements for future industrial and societal advancement.

The control cable market is experiencing dynamic shifts, characterized by evolving business trends, distinct regional growth patterns, and specialized segment advancements. Key business trends include a heightened focus on product innovation, with manufacturers developing cables offering improved fire resistance, halogen-free materials for enhanced safety, and greater data transmission capabilities to support advanced digital applications. There is also an increasing demand for customized control cable solutions tailored to specific industry requirements, alongside a growing emphasis on sustainable manufacturing practices and the adoption of energy-efficient production processes. Strategic collaborations and mergers among market players are also prevalent as companies seek to consolidate market share and expand their technological portfolios.

Geographically, the Asia-Pacific region continues to dominate the control cable market, driven by rapid industrialization, extensive infrastructure development projects, and significant investments in manufacturing and energy sectors, particularly in China, India, and Southeast Asian countries. North America and Europe demonstrate mature but steady growth, propelled by the modernization of existing infrastructure, the integration of smart grid technologies, and the adoption of advanced automation solutions in established industries. Emerging economies in Latin America, the Middle East, and Africa are also contributing to market expansion, spurred by urbanization, industrial growth, and increasing investments in the oil and gas, utilities, and construction sectors, presenting lucrative opportunities for market participants.

Segmentation trends reveal strong growth across various application areas. The industrial automation segment remains a primary driver, with continuous advancements in factory automation, robotics, and process control systems demanding more sophisticated and reliable control cables. The building automation and infrastructure segments are also experiencing significant uptake, fueled by the development of smart buildings, intelligent transportation systems, and modern urban infrastructure that require extensive networks of control cables for lighting, HVAC, security, and communication. Furthermore, the burgeoning renewable energy sector, including solar and wind power installations, is creating substantial demand for control cables specifically designed for harsh outdoor environments and precise energy management, highlighting a diverse and expanding utility for these essential components.

The pervasive influence of Artificial Intelligence (AI) is set to significantly reshape various facets of the control cable market, influencing everything from design and manufacturing to application and maintenance. Common user questions revolve around how AI can optimize cable production, enhance predictive maintenance of industrial systems using AI-powered diagnostics, and if AI-driven control systems will necessitate entirely new specifications for control cables. Users are keen to understand the implications for cable longevity, performance in highly automated environments, and the potential for AI to introduce efficiencies throughout the cable lifecycle. There is a clear expectation that AI will drive demand for smarter, more data-centric control cables capable of integrating seamlessly into intelligent networks and complex autonomous systems.

The primary themes emerging from user inquiries center on the operational enhancements and technological evolution brought about by AI. Concerns include the potential for AI to optimize material usage and reduce waste in manufacturing, improve quality control through automated inspection systems, and enable more precise and adaptive control within end-user applications. Furthermore, users anticipate that AI will facilitate the development of self-aware cable systems that can communicate their health status and predict failure points, thereby revolutionizing maintenance strategies and reducing unplanned downtime. The integration of AI also raises questions about data security within cable networks and the need for control cables that can support higher bandwidths and lower latency for AI-driven real-time data processing.

Overall, users expect AI to drive a paradigm shift towards intelligent cabling solutions, influencing product development towards enhanced connectivity, durability, and diagnostic capabilities. The expectation is that AI will not only optimize the existing market but also spur innovation in new generations of control cables designed for future smart factories, autonomous vehicles, and advanced energy grids. This includes cables that can withstand more demanding operational parameters dictated by AI-optimized processes, along with those that can reliably transmit the vast amounts of data generated by AI systems, thereby solidifying AIs role as a transformative force in the control cable industry.

The control cable market is shaped by a complex interplay of drivers, restraints, opportunities, and broader impact forces. Key drivers include the relentless march of industrial automation and the proliferation of robotics across manufacturing sectors, which necessitates a dense network of reliable control cables for intricate signal transmission. Furthermore, significant investments in infrastructure development globally, encompassing smart cities, transportation networks, and communication systems, continue to fuel demand. The expanding renewable energy sector, particularly solar and wind power installations, is another substantial driver, requiring specialized control cables for efficient energy management and robust system control. These factors collectively create a strong foundation for sustained market growth, pushing innovation in cable design and material science to meet evolving industry needs.

However, the market also faces considerable restraints that temper its growth trajectory. The volatility in raw material prices, especially copper and PVC, directly impacts manufacturing costs and profit margins, creating uncertainty for market players. Stringent regulatory standards and certifications, particularly concerning safety, environmental impact, and performance, impose significant compliance burdens and can slow down product development cycles. Moreover, the high initial investment required for advanced and specialized control cables, coupled with the long product lifecycles in certain applications, can sometimes deter rapid adoption. The intense competitive landscape, characterized by numerous global and regional players, also puts pressure on pricing and necessitates continuous innovation to maintain market position.

Despite these challenges, numerous opportunities abound within the control cable market. The increasing integration of the Internet of Things (IoT) and Industry 4.0 technologies presents a vast opportunity for cables with enhanced data capabilities and smarter connectivity. The demand for customized and application-specific control cable solutions, designed for extreme environments or highly specialized machinery, offers a lucrative niche for manufacturers. Furthermore, the rapid industrialization and urbanization in emerging economies across Asia-Pacific, Latin America, and Africa provide untapped growth potential for market expansion. The ongoing focus on energy efficiency and sustainable development also opens avenues for eco-friendly and halogen-free control cable innovations. The interplay of technological advancements and evolving global industrial landscapes generates dynamic impact forces, constantly reshaping market dynamics and influencing strategic decisions for stakeholders.

The control cable market is comprehensively segmented across various dimensions, reflecting the diverse applications and technical requirements of modern industries. These segmentations enable a granular understanding of market dynamics, highlighting areas of high growth, specific technological demands, and regional preferences. Key criteria for segmentation include the type of insulation material, the conductor material, the specific application areas, the voltage rating, and the overarching end-use industry. This multifaceted approach underscores the markets complexity and the necessity for specialized cable solutions to cater to unique operational environments and performance mandates.

Understanding these segments is crucial for market participants to tailor their product offerings, develop targeted marketing strategies, and identify emerging trends. For instance, the choice of insulation material directly impacts a cables performance characteristics, such as temperature resistance, flexibility, and chemical resilience, making it a critical differentiator. Similarly, the end-use industry segment clearly delineates the demand patterns from sectors ranging from heavy manufacturing to renewable energy, each with distinct volume and specification requirements. The interplay between these segments often drives innovation, compelling manufacturers to develop hybrid cables or integrated solutions that cross traditional boundaries, such as cables combining power, control, and data transmission capabilities.

The growth within these segments is not uniform; some areas exhibit accelerated expansion driven by global megatrends, while others maintain steady demand due to foundational industrial needs. For example, segments tied to industrial automation and smart infrastructure are experiencing robust growth fueled by technological advancements and digitalization initiatives. Conversely, segments serving traditional manufacturing or basic electrical installations provide a stable base demand. This dynamic segmentation landscape necessitates continuous market intelligence and agile product development to capitalize on evolving opportunities and navigate competitive pressures, ensuring that the control cable market remains responsive to global industrial and technological shifts.

The control cable markets value chain is an intricate network spanning from the procurement of raw materials to the final end-user application, involving multiple stakeholders at each stage. At the upstream end, the chain begins with suppliers of critical raw materials, primarily copper for conductors, and various polymers like PVC, XLPE, and rubber for insulation and jacketing. These material suppliers play a pivotal role, as fluctuations in commodity prices directly impact manufacturing costs and, consequently, the final product pricing. Ensuring a stable and high-quality supply of these foundational components is essential for maintaining production continuity and competitiveness in the market. Manufacturers often engage in long-term contracts or diversified sourcing strategies to mitigate risks associated with material availability and cost volatility, forming critical relationships with these upstream partners.

Following raw material procurement, the manufacturing stage forms the core of the value chain, where raw materials are processed into finished control cables. This involves complex processes such as wire drawing, insulation extrusion, stranding, cabling, shielding, and jacketing, requiring specialized machinery and technical expertise. Manufacturers invest heavily in R&D to develop innovative cable designs, advanced insulation materials (e.g., halogen-free, fire-resistant), and enhanced performance characteristics (e.g., flexibility, chemical resistance). Post-manufacturing, cables are then distributed to various markets. This distribution network can be direct, where manufacturers sell directly to large industrial clients or major projects, or indirect, involving a network of wholesalers, distributors, and system integrators who add value through inventory management, logistics, and technical support. The choice of distribution channel often depends on the scale of the customer and the complexity of the project.

The downstream segment of the value chain involves the installation of control cables and their integration into diverse end-user applications. This stage includes electrical contractors, engineering, procurement, and construction (EPC) firms, and specialized system integrators who are responsible for designing, installing, and commissioning the control systems. End-users, ranging from manufacturing plants and power utilities to commercial buildings and transportation networks, represent the final consumer of these products, utilizing the cables for signal transmission, automation, and operational control. Post-installation, the value chain extends to after-sales services, including maintenance, troubleshooting, and potential replacement, underscoring the long-term relationship between manufacturers, distributors, and end-users. Efficiency and collaboration across all these stages are vital for delivering high-quality, cost-effective, and reliable control cable solutions that meet the evolving demands of a technologically advanced global market.

The control cable market caters to a broad spectrum of potential customers, primarily comprising industries and organizations that rely on precise electrical signal transmission and automation for their operations. These end-users are characterized by their need for robust, reliable, and application-specific cabling solutions to manage and monitor various processes, from machinery control in factories to intricate data flow in smart infrastructures. Key segments of potential customers include industrial manufacturers, energy utility providers, infrastructure developers, and commercial building operators. Each segment presents unique demands regarding cable specifications, volume, and compliance with industry-specific standards, driving manufacturers to offer a diverse portfolio of products tailored to these varied needs. Understanding the operational intricacies and technical requirements of these customer groups is paramount for market penetration and sustained growth.

Within the industrial sector, potential customers are expansive, encompassing automotive assembly plants, electronics manufacturing facilities, chemical processing units, pharmaceutical production lines, and food and beverage processing plants. These industries require control cables for their Programmable Logic Controllers (PLCs), robotic systems, conveyor belts, motor control centers, and various sensors and actuators that form the backbone of modern automation. The demand here is often for cables that offer high flexibility, resistance to oil, chemicals, and abrasion, and excellent electromagnetic compatibility (EMC) to ensure signal integrity in electrically noisy environments. The consistent drive towards Industry 4.0 and advanced manufacturing techniques across these sectors further expands the customer base, as more sophisticated automation necessitates advanced cabling solutions.

Beyond traditional manufacturing, significant potential customers exist in the energy and utilities sector, including conventional power plants, renewable energy installations (solar farms, wind turbines), and smart grid operators. These entities require control cables for switchgear, control panels, monitoring systems, and for connecting various components within generation and distribution networks, often demanding cables with enhanced fire resistance, UV resistance, and durability for outdoor or harsh environments. The burgeoning smart building and infrastructure development sectors also represent a vast customer base, with demand for control cables in HVAC systems, lighting controls, security systems, fire alarms, and intelligent transportation networks. As urbanization and technological integration continue to accelerate globally, the pool of potential customers across these diverse industries is expected to grow, underscoring the critical and expanding role of control cables in modern society.

The technological landscape of the control cable market is continuously evolving, driven by advancements in materials science, manufacturing processes, and the increasing demand for high-performance, specialized solutions. A primary focus is on insulation and jacketing materials, with innovations moving towards improved safety, environmental friendliness, and enhanced durability. For instance, the adoption of Cross-Linked Polyethylene (XLPE) is growing due to its superior thermal and electrical properties compared to traditional PVC, allowing cables to operate effectively at higher temperatures and with greater current carrying capacity. Furthermore, the development of halogen-free, low smoke, and zero halogen (LSZH) compounds is a significant trend, addressing safety concerns by reducing the emission of toxic fumes and corrosive gases in the event of a fire, making them crucial for applications in public buildings and critical infrastructure. These material innovations are pivotal in meeting stringent regulatory standards and customer expectations for safety and performance.

Another crucial area of technological advancement revolves around cable design and construction to meet specific application demands. This includes the development of highly flexible cables for dynamic applications, such as those found in robotics and drag chains, where continuous motion requires exceptional mechanical robustness and fatigue resistance. Multi-core and composite cables, which integrate power, control, and data transmission into a single cable, are gaining traction, simplifying installation and reducing wiring complexity in integrated systems like those found in smart factories and IoT environments. Enhanced shielding technologies, utilizing materials like braided copper or aluminum foil, are also critical for minimizing electromagnetic interference (EMI) and radio frequency interference (RFI), thereby ensuring signal integrity in electrically noisy industrial settings. These design innovations are essential for supporting the reliability and efficiency of increasingly complex and interconnected control systems.

The integration of digital and smart technologies is also profoundly influencing the control cable markets technological trajectory. There is a growing demand for control cables that can seamlessly support high-speed data communication protocols, facilitating the real-time data exchange necessary for Industry 4.0, IoT devices, and AI-driven automation systems. This includes developments in twisted pair and fiber optic integrated control cables that can handle greater bandwidth and lower latency. Predictive maintenance capabilities, enabled by integrating sensors directly into cables or through advanced diagnostic tools, represent another significant technological frontier, allowing for real-time monitoring of cable health and performance. Overall, the market is characterized by a drive towards greater functionality, enhanced safety features, and a higher degree of intelligence and connectivity within cabling solutions, ensuring they remain fit for purpose in an increasingly digital and automated world.

A control cable is a multi-core electrical cable designed to transmit low-voltage signals, data, or power for the purpose of controlling, monitoring, or measuring automated processes and equipment. Its primary functions include connecting control panels, sensors, actuators, and machinery in industrial automation, building management systems, and other complex operational environments, ensuring precise and reliable command execution.

The control cable markets growth is primarily driven by escalating industrial automation and the proliferation of robotics across manufacturing sectors, increasing global investments in infrastructure development and smart city initiatives, and the rapid expansion of the renewable energy sector. Additionally, the continuous demand for enhanced safety, efficiency, and precise control in various industrial and commercial applications significantly contributes to market expansion.

Environmental conditions profoundly impact control cable selection, dictating the choice of insulation, jacketing materials, and overall cable construction. Factors such as temperature extremes, exposure to moisture, chemicals, oils, UV radiation, and mechanical stress (e.g., abrasion, bending) necessitate specialized cables. Manufacturers offer solutions with enhanced resistance to ensure durability, operational integrity, and safety in harsh or demanding environments.

Digitalization and the IoT are critical drivers in the control cable market, fostering demand for cables with enhanced data transmission capabilities, higher bandwidths, and improved connectivity features. These trends necessitate cables that can reliably support smart sensors, networked control systems, and real-time data exchange, enabling intelligent automation, predictive maintenance, and integrated building management in modern industrial and urban infrastructures.

Emerging technological trends include the development of halogen-free, low smoke (HFFR/LSZH) cables for improved fire safety, the integration of composite cables combining power, control, and data transmission in a single unit, and advancements in highly flexible and durable cables for dynamic applications like robotics. Further innovations focus on enhanced shielding for electromagnetic compatibility, thinner insulation, and the incorporation of smart features for self-monitoring and predictive diagnostics, aligning with Industry 4.0 demands.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.