ID : MRU_ 428020 | Date : Oct, 2025 | Pages : 242 | Region : Global | Publisher : MRU

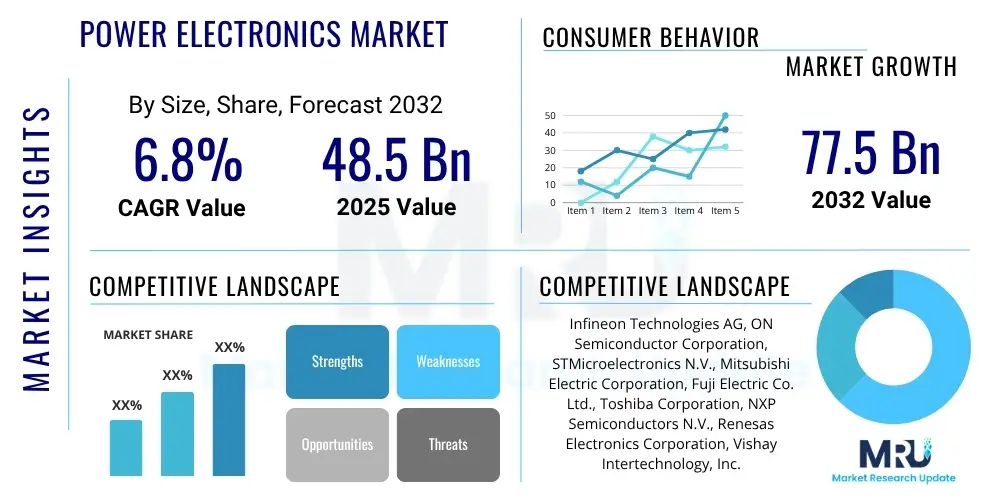

The Power Electronics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2032. The market is estimated at USD 48.5 billion in 2025 and is projected to reach USD 77.5 billion by the end of the forecast period in 2032.

The Power Electronics Market encompasses a broad spectrum of electronic components and systems designed to control and convert electric power. This crucial technology forms the backbone of modern electrical infrastructure, enabling efficient energy management across diverse applications. Power electronics devices, ranging from discrete components like MOSFETs and IGBTs to integrated power management ICs and complex power modules, are engineered to optimize power delivery, minimize energy loss, and enhance the performance and reliability of electrical systems. Their fundamental function involves switching, conditioning, and converting electrical energy from one form to another, such as AC to DC, DC to AC, DC to DC, or AC to AC, with minimal energy dissipation.

The products within this market are instrumental in achieving high efficiency in energy conversion, making them indispensable for sustainable development and cost-effective operation in various sectors. Major applications span critical areas including automotive systems, particularly in electric and hybrid vehicles; industrial machinery, such as motor drives and robotics; renewable energy systems like solar inverters and wind turbine converters; consumer electronics, optimizing power for devices from smartphones to home appliances; and information and communication technology (ICT) infrastructure, supporting data centers and telecommunications networks. These devices also play a vital role in aerospace & defense, medical equipment, and smart grid applications.

The primary benefits derived from advanced power electronics include significantly improved energy efficiency, which translates into reduced operational costs and lower carbon emissions. They enable compact and lightweight designs for electronic products, enhance system reliability and longevity, and facilitate precise control over power flow, leading to superior performance. The market is currently driven by several macro and microeconomic factors, notably the global push towards electrification and decarbonization, the accelerating adoption of electric vehicles, rapid advancements in renewable energy installations, and the escalating demand for energy-efficient solutions in data centers and industrial automation. Technological innovations in semiconductor materials like Silicon Carbide (SiC) and Gallium Nitride (GaN) are further catalyzing market expansion by enabling higher power densities, faster switching speeds, and superior thermal performance, addressing critical needs in high-power and high-frequency applications.

The Power Electronics Market is experiencing robust growth, propelled by transformative business trends centered on sustainability, digitalization, and electrification across global industries. Key business trends include the intensified focus on energy efficiency regulations and standards, which compel manufacturers to integrate advanced power semiconductor devices into their designs. There is a strong industry shift towards modular and integrated power solutions, simplifying system design, reducing size, and improving reliability. Furthermore, strategic collaborations and mergers among semiconductor manufacturers and system integrators are shaping the competitive landscape, aiming to offer comprehensive, end-to-end power management solutions. The increasing investment in smart manufacturing and Industry 4.0 initiatives is also driving demand for high-performance power electronics in industrial automation and robotics, optimizing production processes and enhancing operational efficiency.

From a regional perspective, Asia Pacific continues to dominate the market, primarily due to its robust manufacturing base for consumer electronics, automotive components, and industrial equipment, alongside significant investments in renewable energy and electric vehicle infrastructure, particularly in China, Japan, and South Korea. North America and Europe are also demonstrating substantial growth, fueled by stringent environmental regulations, supportive government policies for clean energy, and a strong drive towards vehicle electrification. These regions are witnessing increased R&D activities and adoption of advanced materials like SiC and GaN, positioned at the forefront of technological innovation and high-power application development. Latin America, the Middle East, and Africa are emerging as growing markets, driven by infrastructure development projects, increasing industrialization, and efforts to diversify energy sources, creating new opportunities for power electronics adoption.

Segmentation trends highlight the increasing prominence of advanced material-based devices, with Silicon Carbide (SiC) and Gallium Nitride (GaN) power semiconductors gaining significant traction over traditional Silicon-based devices, particularly in high-voltage, high-frequency, and high-temperature applications. The Automotive segment, especially electric vehicles (EVs) and hybrid electric vehicles (HEVs), remains the largest and fastest-growing application area, demanding higher power density and efficiency from traction inverters, on-board chargers, and DC-DC converters. The Industrial and Energy & Power sectors are also substantial contributors, driven by the expansion of industrial automation, factory electrification, and the global transition to renewable energy sources, which necessitate reliable and efficient power conversion solutions for motor drives, solar inverters, and grid infrastructure. This dynamic interplay of technology, regional initiatives, and end-use demand underscores a vibrant and continuously evolving market landscape.

The integration of Artificial Intelligence (AI) is set to profoundly transform the Power Electronics Market, addressing long-standing challenges and unlocking new avenues for innovation. Users frequently inquire about how AI can enhance the design, operation, and maintenance of power electronic systems. Common questions revolve around AI’s role in optimizing efficiency, predicting failures, enabling smarter control, and accelerating the development of next-generation devices. The key themes emerging from user concerns include leveraging AI for real-time fault detection and diagnostics to improve system reliability and reduce downtime, employing machine learning algorithms to optimize power conversion efficiency under varying load conditions, and using AI in the design phase to simulate and validate complex power circuits more rapidly and accurately. Furthermore, there is significant interest in how AI can facilitate the integration of renewable energy sources into the grid more intelligently and manage energy storage systems more effectively, ultimately leading to more resilient, efficient, and autonomous power systems. Expectations are high for AI to enable predictive maintenance, smart grid capabilities, and highly adaptive power management, moving beyond static control methodologies to dynamic, data-driven optimization.

The Power Electronics Market is shaped by a confluence of robust Drivers, significant Restraints, promising Opportunities, and impactful forces that dictate its trajectory. The primary drivers underpinning market growth include the burgeoning global demand for energy-efficient electronic devices and systems, fueled by rising energy costs and increasingly stringent environmental regulations aimed at reducing carbon emissions. The rapid electrification of the automotive sector, characterized by the accelerated adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs), significantly boosts demand for high-performance power semiconductors in traction inverters, on-board chargers, and battery management systems. Furthermore, the massive expansion of renewable energy generation capacity, particularly solar and wind power, necessitates advanced power electronics for efficient power conversion and grid integration. Industrial automation and the advent of Industry 4.0 also serve as powerful drivers, as factories increasingly rely on precise motor control and efficient power supplies for robotics and machinery, enhancing productivity and operational efficiency.

Despite these compelling drivers, the market faces several notable restraints. The high initial cost associated with advanced power semiconductor materials like Silicon Carbide (SiC) and Gallium Nitride (GaN) can deter widespread adoption, especially for cost-sensitive applications, despite their long-term efficiency benefits. The inherent complexity in designing and manufacturing power electronic devices, particularly for high-power and high-frequency applications, requires specialized expertise and sophisticated fabrication processes, leading to longer development cycles and higher R&D investments. Additionally, the challenge of managing thermal issues in compact, high-power density modules remains a significant technical hurdle, impacting device reliability and longevity. Supply chain disruptions, often triggered by geopolitical tensions or global events, can also affect the availability and pricing of critical raw materials and components, leading to production delays and increased costs.

Looking ahead, the market is rife with significant opportunities. The continuous technological advancements in wide bandgap semiconductors (SiC and GaN) present a substantial opportunity to develop even more efficient, compact, and high-performance power electronic solutions, addressing the evolving demands of various industries. The emergence of smart grid technologies and the ongoing modernization of electrical infrastructure worldwide create new avenues for intelligent power management and control systems. Furthermore, the growing demand for fast charging infrastructure for EVs and the development of wireless power transfer technologies offer lucrative growth prospects. The increasing integration of power electronics with artificial intelligence (AI) and machine learning (ML) for predictive maintenance, optimized control, and enhanced system resilience also represents a transformative opportunity. These impact forces collectively define a dynamic market environment where technological innovation, regulatory pressures, and evolving application demands continually reshape the landscape and drive future growth.

The Power Electronics Market is broadly segmented based on various criteria, including device type, material, end-use industry, and application. This segmentation provides a granular view of the market dynamics, revealing specific growth drivers and technological preferences within each category. Understanding these segments is crucial for stakeholders to identify lucrative opportunities, tailor product development strategies, and effectively position themselves in this complex and evolving market. The diverse range of power electronic devices caters to an equally diverse set of applications, from miniature consumer electronics to large-scale industrial and energy systems, each with unique performance requirements and market characteristics. The shift towards higher efficiency and power density is a common thread influencing developments across all segments, pushing innovation in materials and device architectures.

A comprehensive Value Chain Analysis of the Power Electronics Market reveals a multi-stage process, beginning with raw material sourcing and culminating in the delivery of sophisticated power management solutions to diverse end-users. The upstream segment of the value chain is critical, focusing on the procurement and processing of fundamental semiconductor materials such as silicon, silicon carbide, and gallium nitride. This stage involves highly specialized chemical processing and crystal growth techniques to produce high-purity wafers, which are the foundational substrates for power semiconductor devices. Key activities also include the manufacturing of other crucial components like magnetics, capacitors, resistors, and intricate packaging materials. Innovation at this upstream level, particularly in wide bandgap materials, significantly influences the performance and cost-effectiveness of the final power electronic products. The intense capital expenditure and technological expertise required for wafer fabrication and material synthesis characterize this segment, with a concentrated number of highly specialized suppliers.

Moving downstream, the value chain progresses through the design, fabrication, and assembly of the power electronic devices themselves. This involves advanced semiconductor manufacturing processes, including photolithography, doping, etching, and metallization, to create power ICs, discrete components, and modules. Design houses, Integrated Device Manufacturers (IDMs), and outsourced semiconductor assembly and test (OSAT) providers play pivotal roles here, transforming raw wafers into functional chips and then integrating them into robust packages. The integration of advanced packaging technologies, such as system-in-package (SiP) and module-level integration, is crucial for achieving higher power densities, improved thermal management, and enhanced reliability. Rigorous testing and quality assurance procedures are integral at every stage to ensure device performance and adherence to industry standards.

The distribution channel for power electronics is multifaceted, encompassing both direct and indirect sales strategies. Direct channels typically involve Original Equipment Manufacturers (OEMs) purchasing components directly from large semiconductor manufacturers, especially for high-volume or custom-designed applications in sectors like automotive and industrial. This direct engagement allows for close technical collaboration and tailored solutions. Indirect channels involve a network of distributors, value-added resellers (VARs), and sales representatives who cater to a broader customer base, including small and medium-sized enterprises (SMEs) and fragmented markets. These intermediaries provide local support, technical expertise, and inventory management, making products accessible to a wider array of customers who may not have the capacity for direct procurement from major manufacturers. The selection of distribution channels often depends on market reach, customer segmentation, product complexity, and the required level of technical support, ensuring efficient market penetration and customer satisfaction across the globe.

The Power Electronics Market serves an incredibly diverse range of potential customers, spanning across nearly all sectors that rely on electrical energy conversion and control. The primary end-users and buyers of power electronics products are enterprises and organizations involved in manufacturing, energy production, transportation, consumer goods, and critical infrastructure. A significant segment of the customer base consists of Original Equipment Manufacturers (OEMs) in the automotive industry, particularly those specializing in Electric Vehicles (EVs), Hybrid Electric Vehicles (HEVs), and their charging infrastructure. These OEMs require advanced power modules and discrete components for traction inverters, on-board chargers, DC-DC converters, and battery management systems, driving innovation in high-power, high-efficiency solutions. The increasing regulatory pressure for reduced emissions and the global shift towards sustainable transportation continue to expand this customer segment, demanding robust and reliable power electronics for new vehicle platforms.

Another major customer group comprises industrial manufacturers and automation companies. This includes producers of industrial motor drives, robotics, factory automation equipment, and uninterruptible power supplies (UPS). These entities prioritize power electronics that offer high efficiency, durability, and precise control to optimize manufacturing processes, reduce operational costs, and enhance overall productivity. The ongoing trend of Industry 4.0 and smart manufacturing further stimulates demand from this segment, as power electronics underpin the intelligence and energy efficiency of modern industrial machinery. The energy and power sector also represents a substantial customer base, including utility companies, renewable energy developers (solar and wind farm operators), and grid infrastructure providers. These customers require power electronics for solar inverters, wind turbine converters, power transmission and distribution systems, and energy storage solutions, all critical for managing and integrating diverse energy sources and ensuring grid stability.

Beyond these large-scale industrial and infrastructure customers, the market extends to manufacturers of consumer electronics, such as smartphones, laptops, home appliances, and various smart devices. These buyers seek compact, efficient, and cost-effective power management ICs and discrete components to deliver superior performance and extended battery life in their products. The Information and Communication Technology (ICT) sector, encompassing data centers and telecommunications companies, is another key customer, demanding high-efficiency power supplies and converters to minimize energy consumption and operational costs for servers, networking equipment, and base stations. Furthermore, power electronics find applications in specialized markets such as aerospace & defense for avionics and radar systems, and healthcare for medical imaging and diagnostic equipment, where reliability, precision, and performance are paramount. This broad and continuously expanding customer base underscores the pervasive and indispensable role of power electronics in the modern technological landscape.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 48.5 billion |

| Market Forecast in 2032 | USD 77.5 billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, ON Semiconductor Corporation, STMicroelectronics N.V., Mitsubishi Electric Corporation, Fuji Electric Co. Ltd., Toshiba Corporation, NXP Semiconductors N.V., Renesas Electronics Corporation, Vishay Intertechnology, Inc., Texas Instruments Incorporated, ABB Ltd., Hitachi, Ltd., Littelfuse, Inc., ROHM Co. Ltd., Semikron Danfoss, Wolfspeed, Inc., Microchip Technology Inc., Alpha and Omega Semiconductor Limited, Danfoss A/S, Bel Fuse Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Power Electronics Market is characterized by a dynamic and continuously evolving technology landscape, driven by the relentless pursuit of higher efficiency, increased power density, improved reliability, and reduced costs. At the forefront of this evolution are advancements in semiconductor materials, with Silicon Carbide (SiC) and Gallium Nitride (GaN) emerging as game-changers. These wide bandgap (WBG) materials offer superior properties compared to traditional silicon, including higher breakdown voltage, faster switching speeds, and better thermal conductivity. SiC devices are particularly well-suited for high-voltage and high-power applications such as electric vehicle traction inverters, industrial motor drives, and solar inverters, enabling smaller, lighter, and more efficient systems. GaN, on the other hand, excels in high-frequency applications at lower to medium power levels, finding increasing adoption in consumer electronics power adapters, data center power supplies, and telecommunication infrastructure, leading to significant reductions in size and weight while boosting efficiency.

Beyond material innovation, significant technological developments are occurring in packaging and module design. Advanced packaging techniques, such as copper clip bonding, silver sintering, and improved substrate materials, are crucial for enhancing thermal management, reducing parasitic inductances, and increasing the reliability and power density of modules. Integrated power modules (IPMs), which combine multiple power semiconductor devices, gate drivers, and protection circuits into a single compact package, are gaining traction, simplifying system design and improving performance. The shift towards System-in-Package (SiP) and System-on-Chip (SoC) solutions integrates more functionalities, including control and sensing, directly into the power electronic component, leading to more intelligent and autonomous power management systems. This integration minimizes external components, reduces board space, and improves overall system robustness and electromagnetic compatibility (EMC).

Furthermore, innovations in control algorithms and digital power management are significantly impacting the market. Digital control techniques, often leveraging microcontrollers and digital signal processors (DSPs), offer greater flexibility, precision, and adaptability compared to traditional analog control. These advanced algorithms enable features such as adaptive switching frequency optimization, predictive control, and sophisticated fault detection and protection, leading to higher efficiency and better dynamic response. The ongoing integration of Artificial Intelligence (AI) and Machine Learning (ML) into power electronics control systems is a burgeoning area, promising even greater optimization, predictive maintenance capabilities, and autonomous operation. This includes AI-driven thermal management, intelligent grid integration, and self-tuning power converters. These convergent technological advancements are collectively pushing the boundaries of what is achievable in power conversion, ensuring the continuous evolution and expansion of the Power Electronics Market into new and demanding applications.

Power electronics are electronic devices and systems that control and convert electric power efficiently. They are crucial for minimizing energy loss, enabling high-performance electrical systems, and are vital for modern applications like electric vehicles, renewable energy, and industrial automation.

The primary materials include Silicon (Si), which is traditional and cost-effective; Silicon Carbide (SiC), ideal for high-voltage, high-frequency, and high-temperature applications; and Gallium Nitride (GaN), preferred for high-frequency, low-to-medium power applications with superior efficiency.

The growing adoption of electric vehicles (EVs) is a major driver for the Power Electronics Market. EVs require high-efficiency power semiconductors for traction inverters, on-board chargers, and DC-DC converters, leading to significant demand for advanced power modules and SiC/GaN devices.

AI is transforming power electronics by enabling enhanced design optimization, predictive maintenance, intelligent control systems, and rapid fault detection. It contributes to higher efficiency, improved reliability, and more adaptive power management in complex systems like smart grids and industrial automation.

Asia Pacific is the dominant region due to its strong manufacturing base and investments in EVs and renewable energy. North America and Europe also show robust growth, driven by stringent regulations, technological advancements, and a focus on electrification and sustainability.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.