ID : MRU_ 431112 | Date : Nov, 2025 | Pages : 258 | Region : Global | Publisher : MRU

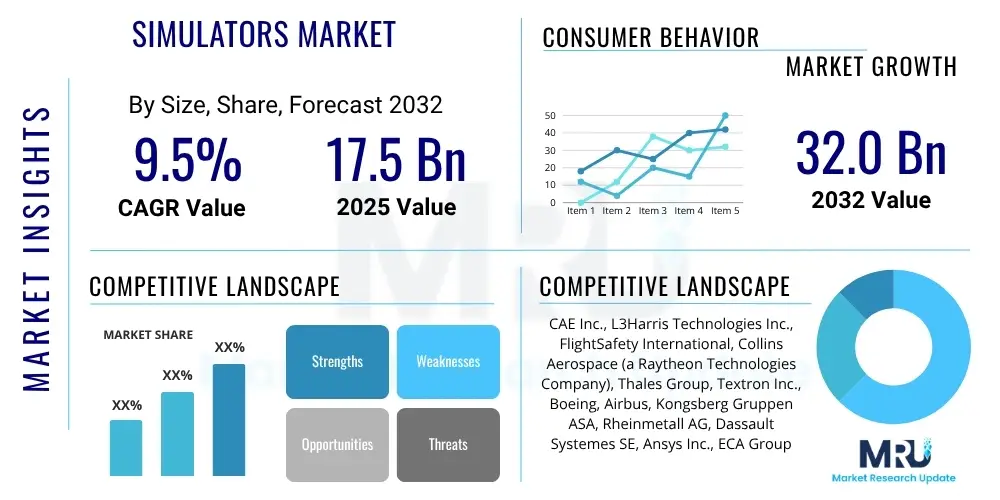

The Simulators Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2032. The market is estimated at $17.5 Billion in 2025 and is projected to reach $32.0 Billion by the end of the forecast period in 2032.

The global simulators market encompasses a wide array of advanced technological systems designed to replicate real-world environments, conditions, and operational scenarios for various purposes including training, research, design, and entertainment. These sophisticated systems integrate hardware and software components to provide immersive and interactive experiences, allowing users to practice skills, test theories, or develop products in a controlled and risk-free setting. The fundamental objective of a simulator is to offer a high degree of fidelity, mirroring the behavior and responses of the actual system or environment being simulated, thereby facilitating effective learning and critical decision-making processes.

Products within this market range from highly specialized flight and surgical simulators used for professional training to complex industrial process and automotive driving simulators for design validation and skill enhancement. Major applications span across critical sectors such as aerospace and defense, healthcare, automotive, marine, and heavy industry, where the consequences of errors are significant and hands-on experience in real environments is either impractical, dangerous, or excessively costly. Simulators provide an invaluable platform for mastering complex tasks, experimenting with new designs, and understanding system dynamics without incurring the risks or expenditures associated with live operations.

The primary benefits of utilizing simulators include enhanced safety, substantial cost reduction compared to real-world training, accelerated skill acquisition, and the ability to test innovative concepts in a controlled virtual space. These systems significantly improve operational efficiency and competency across industries by providing repetitive, standardized, and measurable training modules. Key driving factors propelling market growth include the escalating demand for highly skilled professionals, continuous technological advancements in areas like virtual reality (VR), augmented reality (AR), and artificial intelligence (AI), stringent safety regulations across industries, and the persistent need for cost-effective training and development solutions that minimize environmental impact and resource consumption.

The Simulators Market is experiencing robust growth, primarily fueled by technological advancements and the increasing demand for high-fidelity, risk-free training and development solutions across diverse sectors. Business trends highlight a significant shift towards integrating advanced technologies such as virtual reality, augmented reality, and artificial intelligence into simulation platforms, enhancing realism and adaptability. The market is also witnessing a rising adoption of cloud-based simulation services, enabling greater accessibility, scalability, and collaborative capabilities for users worldwide, which is particularly appealing to smaller enterprises and educational institutions that may lack the capital for extensive on-premise infrastructure. Furthermore, the focus on sustainable and efficient operational practices is driving industries to invest in simulation for optimized resource utilization and reduced environmental impact, fostering a culture of continuous improvement through virtual prototyping and scenario testing.

Regional trends indicate North America and Europe as mature markets characterized by high adoption rates in aerospace, defense, and healthcare sectors, driven by well-established technological infrastructures and significant R&D investments. The Asia Pacific region is emerging as the fastest-growing market, propelled by rapid industrialization, increasing defense expenditures, and a burgeoning demand for skilled labor in developing economies. Countries like China, India, and Japan are investing heavily in advanced manufacturing, automotive, and aviation industries, necessitating sophisticated simulation solutions for training and product development. Latin America, the Middle East, and Africa are also showing promising growth, particularly in sectors such as mining, oil and gas, and transportation, as these regions seek to enhance operational safety and efficiency.

Segment trends reveal that the Aerospace and Defense sector continues to be a dominant application area, driven by continuous demand for pilot, crew, and maintenance training, alongside complex weapon system development. However, the Healthcare segment is rapidly expanding, with surgical and patient simulators becoming indispensable for medical education and procedural practice, significantly improving patient outcomes and practitioner proficiency. The Automotive sector is also exhibiting substantial growth, particularly with the advent of autonomous vehicle technology and advanced driver-assistance systems (ADAS), where simulators are critical for testing, validation, and driver training. Furthermore, the increasing sophistication of gaming and entertainment applications, leveraging immersive VR and AR technologies, is broadening the consumer market for high-quality simulation experiences, pushing the boundaries of realism and interactivity across the entire industry landscape.

Common user questions regarding the impact of Artificial Intelligence on the Simulators Market frequently revolve around how AI can enhance realism, personalize training experiences, optimize operational efficiency, and potentially lead to more autonomous simulation systems. Users are keen to understand if AI integration will significantly reduce development costs and time for new simulation scenarios, as well as if it can adapt to individual user performance in real-time to provide more effective and tailored learning paths. There is also interest in AI's role in predictive maintenance for simulator hardware and software, ensuring higher uptime and reliability. Additionally, concerns often arise about data privacy with AI-driven analytics and the potential for over-reliance on AI in critical training, questioning the balance between human instructor involvement and AI-driven automation.

The key themes emerging from this analysis highlight a strong expectation for AI to revolutionize the fidelity and responsiveness of simulation environments, making them more dynamic and representative of unpredictable real-world situations. Users anticipate AI will move simulators beyond predefined scripts, enabling them to generate adaptive scenarios, intelligent adversaries, and more complex environmental interactions. The potential for AI to provide granular, data-driven feedback and performance assessment is also a significant area of interest, promising to transform how skills are learned and evaluated. Furthermore, the ability of AI to process vast amounts of data from real-world operations to continuously update and improve simulation models is seen as a critical evolution, leading to more accurate and relevant training outcomes.

The Simulators Market is significantly driven by an escalating global demand for highly realistic and cost-effective training solutions across critical industries where errors carry severe consequences. Strict regulatory requirements for operational safety and continuous professional development, particularly in sectors such as aerospace, defense, healthcare, and transportation, compel organizations to adopt advanced simulation technologies. Furthermore, rapid technological advancements in computing power, graphics processing, virtual reality (VR), augmented reality (AR), and haptic feedback systems are enabling the creation of increasingly immersive and high-fidelity simulations, thereby enhancing their efficacy and expanding their application scope. The inherent ability of simulators to reduce operational costs, minimize risks associated with real-world training, and accelerate skill acquisition serves as a compelling incentive for widespread adoption.

However, the market faces several notable restraints that could temper its growth trajectory. The initial high capital investment required for developing, purchasing, and installing advanced simulator systems remains a significant barrier for many potential buyers, particularly smaller enterprises or those in developing economies. The complexity involved in designing, integrating, and maintaining these sophisticated systems necessitates specialized expertise and resources, contributing to operational challenges. Moreover, the inherent ethical considerations, such as the potential for over-reliance on simulated training versus actual hands-on experience, and concerns around data security and privacy within highly integrated virtual environments, also pose considerable challenges that market players must address comprehensively to build user trust and ensure responsible deployment.

Opportunities within the Simulators Market are abundant, primarily stemming from the continuous evolution of digital technologies and the expansion into untapped application areas. The increasing integration of AI, machine learning, and cloud computing is paving the way for more adaptive, personalized, and scalable simulation solutions. Emerging markets, especially in Asia Pacific and Latin America, present vast potential for growth as these regions invest heavily in infrastructure development, industrialization, and enhancing their workforce capabilities. The proliferation of VR and AR technologies beyond traditional enterprise applications into consumer gaming and commercial entertainment further broadens the market base. Impact forces such as rapid technological innovation, evolving regulatory frameworks, and shifting global economic conditions significantly shape the market landscape, dictating investment priorities, technological trends, and the overall pace of adoption across various end-user segments.

The Simulators Market is highly diverse and segmented across various dimensions, reflecting the wide range of applications and technological complexities involved in replicating real-world environments. This comprehensive segmentation allows for a detailed understanding of market dynamics, growth drivers, and specific challenges within different product categories, end-user industries, and technological approaches. Analyzing these segments provides crucial insights into how market players are innovating and tailoring their offerings to meet distinct industry requirements, from hardware components like motion platforms to sophisticated software for scenario generation and data analysis. The market is broadly categorized by component, application, end-user, and technology, each presenting unique characteristics and growth opportunities within the global landscape.

The component segmentation differentiates between the physical infrastructure, the computational brain, and the essential support services that ensure optimal functionality and user experience. Application-based segmentation highlights the primary objectives for which simulators are deployed, ranging from highly structured training programs to innovative research and development initiatives. End-user categories pinpoint the specific industries that leverage simulation technologies, each with its unique demands regarding fidelity, scalability, and safety standards. Finally, the technology segmentation emphasizes the underlying innovations, such as virtual reality or artificial intelligence, that empower these simulation systems, driving their capabilities and expanding their potential across an ever-evolving technological frontier.

The value chain for the Simulators Market is intricate, beginning with extensive upstream activities focused on the development and supply of foundational components and intellectual property. This segment primarily involves specialized hardware manufacturers providing motion platforms, visual displays, control panels, and sensory feedback systems, alongside software developers who create sophisticated modeling and simulation engines, physics-based algorithms, and scenario generation tools. Key upstream players also include providers of advanced computing hardware, graphics processing units (GPUs), and specialized sensors essential for capturing real-world data and rendering high-fidelity virtual environments. The quality and innovation at this initial stage are crucial, as they directly influence the realism, performance, and overall capability of the final simulation system, requiring significant R&D investment and expertise in specialized engineering disciplines.

Midstream activities in the value chain involve the integration and assembly of these diverse components into complete, functional simulation systems. This stage is dominated by system integrators and simulation solution providers who possess the engineering prowess to combine various hardware and software elements, customize them to specific client requirements, and ensure seamless interoperability. These companies often develop proprietary platforms and methodologies to optimize the integration process, performing rigorous testing and calibration to meet stringent performance and safety standards. The ability to manage complex project lifecycles, from conceptual design to installation and commissioning, is paramount here, as custom solutions are frequently required for niche applications in defense, aviation, and healthcare sectors, making direct collaboration with end-users a critical aspect of their operational model.

Downstream analysis focuses on the distribution channels and post-sale services that deliver the final product to end-users and ensure its long-term operational effectiveness. Distribution primarily occurs through direct sales channels, where simulator manufacturers and integrators engage directly with large institutional clients such as military organizations, airlines, hospitals, and major industrial corporations. This direct model allows for extensive customization, comprehensive support, and tailored service agreements, reflecting the high value and complexity of these systems. Indirect channels, although less prevalent for highly customized solutions, include specialized distributors or value-added resellers (VARs) who might cater to smaller enterprises or specific geographical markets, offering localized support and broader market reach. Post-sale services, including maintenance, upgrades, technical support, and ongoing training, form a critical part of the value proposition, ensuring high simulator uptime, longevity, and continuous alignment with evolving industry standards and technological advancements.

The Simulators Market serves a remarkably diverse range of potential customers, spanning across nearly every industry where high-stakes operations, complex machinery, or intricate procedures demand rigorous training, precise development, or safe testing environments. At the forefront are military and defense organizations globally, requiring advanced flight, naval, ground vehicle, and weapon system simulators to train personnel, rehearse missions, and develop new combat capabilities without risking human lives or expensive equipment. Commercial airlines and aviation academies represent another significant customer segment, heavily investing in flight simulators for pilot certification, recurrent training, and emergency procedure drills, driven by stringent regulatory requirements and the continuous need for highly skilled aviation professionals. These customers prioritize ultra-high fidelity and regulatory compliance to ensure maximum training transfer.

Beyond aviation, the healthcare sector is a rapidly expanding customer base, with hospitals, medical universities, and training centers adopting surgical simulators, patient simulators, and diagnostic imaging simulators. These tools enable medical professionals, from students to experienced surgeons, to practice complex procedures, improve diagnostic skills, and manage critical scenarios in a risk-free environment, ultimately enhancing patient safety and clinical outcomes. The automotive industry, including major vehicle manufacturers and Tier 1 suppliers, forms another vital customer segment. They utilize driving simulators for vehicle design validation, testing Advanced Driver-Assistance Systems (ADAS) and autonomous driving algorithms, and training professional drivers, providing a controlled setting for evaluating vehicle dynamics and human-machine interaction before physical prototyping.

Furthermore, heavy industries such as mining, construction, and maritime operations represent substantial potential customers for simulators designed to train operators of cranes, excavators, ships, and other heavy machinery. These simulators are crucial for improving operational efficiency, reducing accidents, and complying with safety regulations in environments where real-world training is hazardous or costly. Educational institutions and research organizations also constitute a significant customer group, leveraging simulation technologies for scientific research, engineering design courses, and virtual labs, facilitating experiential learning and innovative problem-solving. Lastly, the entertainment and gaming industries are increasingly adopting advanced simulation platforms, particularly with the proliferation of virtual reality (VR) and augmented reality (AR) technologies, to create highly immersive and interactive experiences for consumers in theme parks, arcades, and home gaming setups, expanding the market's reach into broader consumer segments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $17.5 Billion |

| Market Forecast in 2032 | $32.0 Billion |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | CAE Inc., L3Harris Technologies Inc., FlightSafety International, Collins Aerospace (a Raytheon Technologies Company), Thales Group, Textron Inc., Boeing, Airbus, Kongsberg Gruppen ASA, Rheinmetall AG, Dassault Systemes SE, Ansys Inc., ECA Group, Moog Inc., Cubic Corporation, Siemens AG, Unity Technologies, Epic Games, Altair Engineering, CACI International Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Simulators Market is characterized by continuous innovation and the convergence of several cutting-edge advancements that collectively contribute to increasingly realistic, immersive, and effective simulation experiences. Core to this evolution are high-fidelity graphics and visualization technologies, leveraging powerful Graphics Processing Units (GPUs) and advanced rendering engines to create visually indistinguishable virtual environments. This includes photorealistic textures, dynamic lighting, complex weather effects, and accurate physics-based object interactions, which are critical for achieving a high degree of immersion and cognitive fidelity, especially in flight, driving, and medical simulations where visual cues are paramount for effective training and decision-making.

Beyond visual fidelity, motion platforms represent a fundamental technology, providing physical feedback to users by replicating accelerations, vibrations, and movements experienced in real-world scenarios. These platforms, ranging from basic two-degree-of-freedom systems to complex six-degree-of-freedom hydraulic or electric systems, are crucial for simulating forces and sensations encountered in aircraft, vehicles, and vessels, enhancing the physiological realism of the simulation. Complementing motion, haptic feedback technologies integrate tactile sensations, allowing users to feel textures, resistance, and impacts through gloves, joysticks, or other control devices. This adds another layer of realism, particularly important for tasks requiring fine motor skills such as surgical procedures or operating heavy machinery, where touch provides critical sensory input.

The integration of Virtual Reality (VR), Augmented Reality (AR), and Mixed Reality (MR) technologies is fundamentally transforming the simulator market, offering unparalleled immersion and interaction capabilities. VR headsets provide completely enclosed virtual environments, while AR overlays digital information onto the real world, and MR blends physical and digital realities seamlessly. These technologies enable a more intuitive and natural user interface, allowing trainees to interact with virtual objects and environments as they would in real life. Furthermore, Artificial Intelligence (AI) and Machine Learning (ML) are becoming indispensable, driving adaptive learning algorithms, intelligent scenario generation, autonomous virtual entities, and data analytics for personalized training feedback. Cloud computing infrastructure is also gaining traction, enabling scalable, on-demand simulation resources, collaborative training environments, and remote accessibility, reducing the need for extensive on-premise hardware and fostering a more agile and interconnected simulation ecosystem. These technological advancements collectively underpin the market's expansion and its ability to address complex training and development challenges across diverse industries.

The Simulators Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2032, indicating robust expansion driven by increasing demand across various industries.

AI significantly enhances simulators by enabling adaptive learning paths, dynamic scenario generation, intelligent virtual entities, and sophisticated performance analytics, leading to more personalized, realistic, and effective training experiences.

Simulators offer critical benefits such as enhanced safety by removing risk, substantial cost reduction compared to real-world operations, accelerated skill acquisition through repetitive practice, and the ability to test complex scenarios in a controlled environment.

The largest end-users of simulator technology include Aerospace & Defense, Healthcare, Automotive, Marine, and various Industrial sectors, all requiring high-fidelity training and development solutions for critical operations.

Key technological advancements driving innovation include the integration of Virtual Reality (VR), Augmented Reality (AR), Artificial Intelligence (AI), advanced haptics, motion platforms, and cloud computing, all contributing to increased realism and immersive capabilities.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.