ID : MRU_ 428146 | Date : Oct, 2025 | Pages : 242 | Region : Global | Publisher : MRU

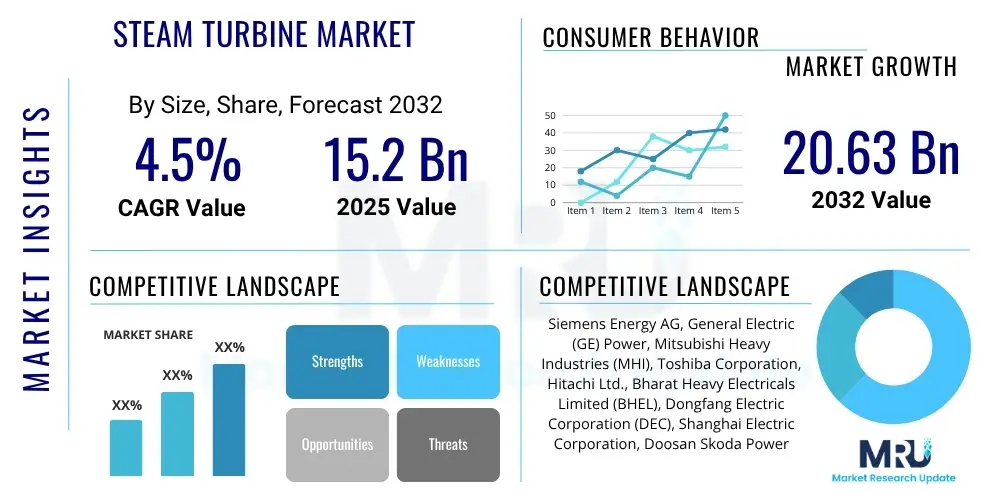

The Steam Turbine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2032. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 20.63 Billion by the end of the forecast period in 2032.

The global steam turbine market represents a cornerstone of the world's energy infrastructure, serving as a critical component in various power generation and industrial applications. At its core, a steam turbine is a mechanical device that extracts thermal energy from pressurized steam and converts it into rotational motion, which is then typically used to drive an electric generator or other machinery. This fundamental technology has been refined over centuries, evolving from early rudimentary designs to highly efficient, sophisticated systems capable of operating under extreme conditions of temperature and pressure. The market encompasses a wide array of turbine types, capacities, and designs, each tailored to specific operational requirements, ranging from large-scale utility power plants to industrial co-generation facilities and marine propulsion systems.

Product descriptions within this market highlight the engineering marvels involved, featuring components such as rotors, blades, casings, bearings, and control systems, all designed for optimal performance, durability, and safety. These turbines are predominantly classified by their operational principles, including condensing turbines, back-pressure turbines, and extraction turbines, each offering distinct advantages in terms of efficiency, heat recovery, and flexibility. Major applications span the entirety of the power sector, including thermal power plants (coal, gas, nuclear), combined cycle power plants, concentrated solar power (CSP) facilities, geothermal power, and biomass energy conversion. Beyond electricity generation, steam turbines are indispensable in heavy industries like petrochemicals, pulp and paper, and steel manufacturing, where they often drive compressors, pumps, and other essential equipment while simultaneously providing process heat.

The benefits of steam turbines are manifold, underscoring their enduring relevance despite the growing penetration of renewable energy sources. They offer high reliability, robust performance, and the ability to operate continuously for extended periods, contributing to grid stability and industrial productivity. Furthermore, advancements in design and materials have led to significant improvements in thermal efficiency, reducing fuel consumption and emissions. Key driving factors for the market include the ever-increasing global demand for electricity, particularly in emerging economies, the necessity for base-load power generation, and the ongoing modernization and expansion of industrial infrastructure. The push for greater energy efficiency, coupled with developments in waste-to-energy and concentrated solar power technologies, also significantly bolsters the market's trajectory, emphasizing steam turbines' role in a diverse energy mix.

The Steam Turbine Market is poised for steady expansion, driven by a confluence of business trends, regional dynamics, and segment-specific growth trajectories. From a business trends perspective, the industry is witnessing a significant shift towards more efficient, flexible, and environmentally conscious turbine designs. There is an increasing emphasis on digitalization, incorporating advanced analytics and IoT for predictive maintenance and optimized operational performance, which not only extends asset life but also enhances overall efficiency and reduces downtime. Furthermore, strategic collaborations and mergers and acquisitions are prevalent as companies seek to expand their technological portfolios, geographic reach, and service capabilities. The aftermarket services segment, including maintenance, repair, and overhaul (MRO), is experiencing robust growth, reflecting the extensive installed base of steam turbines globally and the imperative to maximize their operational lifespan and efficiency.

Regional trends indicate diverse growth patterns influenced by varying energy policies, industrial development, and infrastructure investments. Asia Pacific continues to dominate the market, propelled by rapid industrialization, urbanization, and a surging demand for electricity in countries like China, India, and Southeast Asian nations, leading to extensive investments in new power generation capacities, including nuclear and ultra-supercritical coal plants. North America and Europe, while mature markets, are experiencing growth primarily through the modernization of existing power plants, the adoption of combined heat and power (CHP) systems, and increasing deployment in waste-to-energy and concentrated solar power projects. Latin America and the Middle East & Africa regions are also contributing to market expansion, driven by energy infrastructure development projects and the exploitation of natural gas reserves for power generation.

Segmentation trends highlight particular areas of strength within the market. By type, condensing turbines remain the largest segment due to their widespread use in utility-scale power generation, but back-pressure and extraction turbines are gaining traction in industrial applications due where process heat recovery is critical for energy efficiency. In terms of capacity, large-scale turbines (over 100 MW) continue to be vital for national grids, while medium and small-scale turbines are finding increasing applications in distributed power generation, industrial co-generation, and renewables like biomass and geothermal. The end-use segment is predominantly driven by power generation, encompassing thermal, nuclear, and renewables, but the industrial sector, including chemical, petrochemical, and pulp & paper industries, represents a substantial and growing demand for process steam and mechanical drive applications, reflecting their continuous need for reliable and efficient energy solutions.

Users frequently inquire about the transformative potential of Artificial Intelligence (AI) in the steam turbine market, particularly regarding its ability to enhance operational efficiency, predictive maintenance, and overall system reliability. Common questions revolve around how AI can optimize performance by analyzing vast datasets from sensors, leading to proactive adjustments that prevent failures and extend asset life. There is also significant interest in AI's role in improving design processes, simulating complex operating conditions, and accelerating the development of next-generation turbines. Users are keen to understand how AI-driven solutions can contribute to reducing operational costs, minimizing environmental impact through optimized fuel consumption, and enabling more flexible operations in response to fluctuating grid demands, especially in hybrid power systems. Concerns often include data security, the initial investment required for AI integration, and the need for skilled personnel to manage these advanced systems.

The integration of Artificial Intelligence into the steam turbine market promises to revolutionize various aspects of the product lifecycle, from design and manufacturing to operation and maintenance. By leveraging machine learning algorithms, steam turbine operators can move beyond traditional reactive maintenance strategies to highly accurate predictive maintenance. AI systems analyze real-time operational data, identifying subtle anomalies and predicting potential equipment failures long before they occur, thereby significantly reducing unscheduled downtime and costly repairs. This capability not only enhances the reliability and availability of steam turbines but also optimizes maintenance schedules, ensuring resources are deployed efficiently and effectively. Furthermore, AI can process complex correlations between numerous operational parameters, such as steam flow, pressure, temperature, vibration levels, and power output, to provide prescriptive insights for optimizing turbine performance under varying load conditions, leading to tangible improvements in energy efficiency and reduced fuel consumption.

Beyond operational enhancements, AI is poised to impact the design and engineering phases of steam turbine development. Generative design tools, powered by AI, can rapidly explore thousands of design permutations, optimizing for factors such as aerodynamic efficiency, material stress, and manufacturing feasibility, resulting in lighter, stronger, and more efficient turbine components. In manufacturing, AI-driven robotics and quality control systems can improve precision and consistency, reducing defects and waste. Moreover, AI's ability to analyze market trends and operational data from an extensive installed base provides valuable feedback loops for product development, ensuring that new turbine designs are highly responsive to evolving market demands and technological advancements. As the energy landscape continues to evolve towards greater digitalization and interconnectedness, AI will serve as a crucial enabler for more intelligent, resilient, and sustainable steam turbine operations.

The Steam Turbine Market is influenced by a dynamic interplay of drivers, restraints, opportunities, and pervasive impact forces that collectively shape its growth trajectory and competitive landscape. Key drivers include the relentless global increase in electricity demand, especially from rapidly industrializing nations and urbanizing populations, necessitating robust base-load power generation capabilities where steam turbines excel. Furthermore, the imperative for energy security in many countries prompts investments in diverse energy portfolios, including thermal and nuclear power plants that rely heavily on steam turbines. Industrial expansion across sectors such as petrochemicals, cement, and pulp & paper also fuels demand for steam turbines for mechanical drives and combined heat and power (CHP) applications, where they offer significant energy efficiency benefits by utilizing waste heat. Lastly, the global trend towards replacing aging power generation infrastructure with more efficient and environmentally compliant units provides a steady demand for new turbine installations and upgrades.

However, the market also faces notable restraints. The high initial capital investment required for steam turbine power plants, coupled with long project development cycles, can be a significant barrier for new entrants and can sometimes deter investment in favor of less capital-intensive alternatives. Environmental concerns regarding greenhouse gas emissions from fossil-fuel-fired thermal power plants continue to exert pressure on the market, leading to stricter regulations and a societal shift towards cleaner energy sources. The rapidly declining costs and increasing deployment of renewable energy technologies such as solar photovoltaic and wind power present a formidable competitive challenge, particularly for new grid-scale power generation projects. Additionally, geopolitical instability, fluctuating raw material prices (e.g., steel, nickel alloys), and complex regulatory frameworks pertaining to power generation can introduce uncertainties and impede market growth.

Despite these challenges, significant opportunities abound for the steam turbine market. The modernization and refurbishment of existing power plants represent a substantial opportunity to enhance efficiency, extend operational life, and reduce emissions without constructing entirely new facilities. The growing adoption of nuclear power as a clean and reliable base-load energy source in several countries is a major long-term growth avenue for large-capacity steam turbines. Furthermore, the increasing focus on waste-to-energy and concentrated solar power (CSP) projects, which predominantly utilize steam turbine technology, provides new niche markets. The development of advanced materials, digital technologies for predictive maintenance, and smart control systems offers avenues for innovation, improving turbine performance, flexibility, and overall cost-effectiveness. The rising demand for industrial co-generation and district heating systems also presents a consistent stream of opportunities for smaller to medium-sized steam turbines.

The Steam Turbine Market is extensively segmented to provide a detailed understanding of its diverse components and growth dynamics. This segmentation typically covers critical aspects such as turbine type, capacity, end-use application, and fuel source, allowing for granular analysis of market trends and opportunities within each category. Understanding these segments is crucial for manufacturers, investors, and policymakers to identify key growth areas, tailor product offerings, and formulate effective market strategies. Each segment possesses distinct characteristics influenced by technological advancements, economic factors, and regional energy policies, collectively shaping the market's comprehensive landscape.

The value chain for the steam turbine market is a complex ecosystem involving multiple stages, from raw material sourcing and component manufacturing to assembly, installation, operation, and end-of-life services. Understanding this chain is crucial for identifying areas of value creation, competitive advantage, and potential bottlenecks. The upstream segment of the value chain is dominated by raw material suppliers and component manufacturers. This includes suppliers of specialized alloys (such as nickel, chromium, molybdenum, and vanadium steels) capable of withstanding high temperatures and pressures, precision forging and casting companies for turbine rotors and casings, and manufacturers of high-tolerance blades, bearings, and control systems. The quality and availability of these specialized materials and components directly impact the performance, durability, and cost-effectiveness of the final steam turbine unit. Strong relationships with reliable and technologically advanced upstream partners are critical for maintaining production quality and supply chain resilience, especially given the global nature of sourcing for high-tech components.

Moving downstream, the value chain encompasses the core activities of steam turbine manufacturers, including research and development, design, engineering, assembly, testing, and system integration. This stage involves significant intellectual property and specialized engineering expertise to optimize turbine aerodynamics, thermodynamic cycles, and overall system efficiency. Leading manufacturers often develop proprietary technologies and invest heavily in R&D to maintain their competitive edge. Post-manufacturing, the focus shifts to installation, commissioning, and project management, which often involves collaboration with EPC (Engineering, Procurement, and Construction) firms specializing in large-scale power plant projects. The complexity of these projects requires extensive coordination and technical know-how to ensure seamless integration of the steam turbine with boilers, generators, condensers, and other balance-of-plant components. Effective project execution in this phase is paramount for timely delivery and operational readiness, directly impacting customer satisfaction and project profitability.

The distribution channels for steam turbines are predominantly direct, given the custom nature, high value, and technical complexity of the products. Manufacturers typically engage directly with utility companies, independent power producers (IPPs), and large industrial end-users through dedicated sales teams, technical consultants, and a network of regional offices. These direct channels facilitate close collaboration with clients, allowing for tailored solutions that meet specific project requirements and regulatory standards. Indirect channels may involve agents or distributors for smaller components or specialized services, particularly in regions where manufacturers do not have a direct presence. Post-sales services, including maintenance, repair, overhaul (MRO), spare parts supply, and digital services (e.g., remote monitoring, predictive analytics), constitute a significant and growing part of the downstream value chain. These services are crucial for ensuring the long-term reliability and efficiency of the installed fleet, contributing substantially to recurring revenue and strengthening customer relationships. The entire value chain is characterized by a high degree of technical expertise, capital intensity, and long-term commitment.

The potential customers for the steam turbine market are diverse and span across various sectors, primarily driven by the fundamental need for reliable and efficient power generation and process heat. At the forefront are utility companies and independent power producers (IPPs) who own and operate large-scale power plants responsible for supplying electricity to national grids. These entities represent the largest segment of buyers, investing in new thermal, nuclear, combined cycle, concentrated solar power (CSP), and geothermal facilities, as well as undertaking extensive modernization and life extension projects for existing plants. Their purchasing decisions are influenced by factors such as grid stability requirements, fuel availability, environmental regulations, capital expenditure budgets, and the long-term cost-effectiveness of energy production. These customers require highly reliable, high-capacity steam turbines capable of continuous operation and often seek comprehensive service contracts from manufacturers.

Beyond the traditional power generation sector, a significant segment of potential customers emerges from heavy industries that require substantial amounts of both electricity and process steam. Industries such as petrochemicals, oil refineries, pulp and paper mills, steel plants, cement factories, sugar mills, and food & beverage processing facilities frequently utilize steam turbines for combined heat and power (CHP) or co-generation applications. In these settings, back-pressure and extraction turbines are particularly attractive as they allow for the efficient generation of electricity while simultaneously providing steam for industrial processes, leading to substantial energy cost savings and reduced carbon footprints. These industrial end-users prioritize energy efficiency, operational reliability, and the ability of turbines to integrate seamlessly with their existing plant infrastructure and process demands, often making long-term investment decisions based on total cost of ownership.

Furthermore, the growing emphasis on sustainable energy solutions has expanded the customer base to include developers and operators of waste-to-energy (WtE) plants and biomass power facilities. These projects leverage steam turbines to convert municipal solid waste or organic biomass into electricity and heat, contributing to both waste management and renewable energy targets. Geothermal power plant operators also represent a niche but important customer segment, utilizing steam generated from the Earth's heat to drive turbines. Additionally, the marine sector, particularly for large cargo vessels, cruise ships, and naval fleets, continues to be a customer for steam turbines, especially for propulsion systems that demand high power output and reliability. As the global energy landscape evolves, the diversity of these end-users underscores the broad applicability and enduring importance of steam turbine technology across critical economic sectors worldwide.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2032 | USD 20.63 Billion |

| Growth Rate | 4.5% CAGR |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Siemens Energy AG, General Electric (GE) Power, Mitsubishi Heavy Industries (MHI), Toshiba Corporation, Hitachi Ltd., Bharat Heavy Electricals Limited (BHEL), Dongfang Electric Corporation (DEC), Shanghai Electric Corporation, Doosan Skoda Power, MAN Energy Solutions, Fuji Electric Co., Ltd., Elliott Group, Ansaldo Energia S.p.A., Harbin Electric Corporation, Kawasaki Heavy Industries Ltd., Dresser-Rand (Siemens Energy Business), Peter Brotherhood (part of Baker Hughes), Steam Turbine and Generator (STG) Inc., Qingdao Jieneng Steam Turbine Co., Ltd., Shaanxi Blower (Group) Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The steam turbine market is continuously evolving, driven by significant technological advancements aimed at improving efficiency, reliability, flexibility, and environmental performance. One of the primary areas of focus is the development of ultra-supercritical and advanced ultra-supercritical (A-USC) steam turbines. These technologies operate at extremely high steam temperatures and pressures (above 600°C and 28 MPa), enabling much higher thermal efficiencies (approaching 50% for coal-fired plants) compared to conventional subcritical or supercritical units. This translates directly into reduced fuel consumption and lower greenhouse gas emissions per unit of electricity generated, making them critical for countries seeking to maximize efficiency from their thermal power fleets while addressing climate concerns. Innovations in material science, particularly in high-temperature alloys, are central to the feasibility and durability of these advanced turbine designs, allowing components to withstand the severe operational conditions.

Another crucial technological trend is the integration of digital solutions and advanced control systems. This includes the deployment of Industrial Internet of Things (IIoT) sensors throughout the turbine, real-time data analytics, and machine learning algorithms for predictive maintenance. Digital twins, which are virtual replicas of physical assets, are increasingly being used to simulate turbine behavior, optimize performance, and identify potential issues before they lead to operational disruptions. These smart monitoring and diagnostic systems significantly enhance operational efficiency, minimize unscheduled downtime, and extend the lifespan of turbine assets. Furthermore, advanced control systems allow for greater operational flexibility, enabling steam turbines to ramp up and down more quickly and efficiently, which is vital for balancing power grids that are increasingly integrating intermittent renewable energy sources like wind and solar.

Beyond efficiency and digitalization, advancements in manufacturing techniques and turbine design are also shaping the market. Additive manufacturing (3D printing) is being explored for producing complex turbine components, offering the potential for faster prototyping, custom geometries, and lightweight designs with improved aerodynamic properties. Furthermore, research into modular turbine designs aims to reduce installation times and costs, making them more adaptable to various plant configurations and capacities, including smaller-scale distributed generation projects. The development of steam turbines optimized for specific renewable energy applications, such as high-temperature concentrated solar power (CSP) and diverse waste-to-energy technologies, also represents a critical area of innovation. These specialized designs focus on maximizing energy extraction from varying steam conditions and integrating seamlessly with non-conventional heat sources, underscoring the ongoing technological dynamism within the steam turbine industry.

The market research report includes a detailed profile of leading stakeholders in the Steam Turbine Market.

The Steam Turbine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2032, driven by increasing global electricity demand and industrial expansion.

Key drivers include the surging global demand for electricity, particularly in emerging economies, industrial sector growth, the need for energy security, and ongoing modernization of aging power generation infrastructure globally.

AI is significantly impacting the market by enabling advanced predictive maintenance, optimizing operational efficiency in real-time, enhancing turbine design and engineering processes, and facilitating better resource management for extended asset life and reduced downtime.

Asia Pacific is the largest and fastest-growing region due to rapid industrialization, while North America and Europe focus on modernization and efficiency. Latin America and MEA are growing due to energy infrastructure development.

The main types are Condensing (for utility-scale power generation), Back-Pressure (for industrial combined heat and power), and Extraction Turbines (for flexible power and process steam supply), each tailored to specific energy and industrial needs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.