ID : MRU_ 431789 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

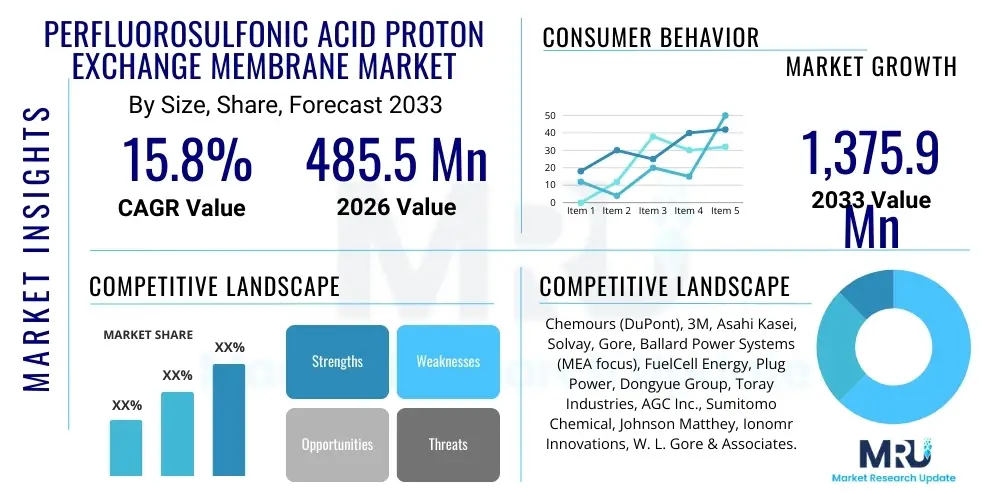

The Perfluorosulfonic Acid Proton Exchange Membrane Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2026 and 2033. The market is estimated at USD 485.5 million in 2026 and is projected to reach USD 1,375.9 million by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating global commitment to sustainable energy sources, particularly the rapid commercialization of hydrogen fuel cell technology across transportation and stationary power generation sectors. PFSA membranes, renowned for their superior proton conductivity and chemical stability, remain the gold standard material critical to the efficient operation of Proton Exchange Membrane Fuel Cells (PEMFCs) and water electrolyzers.

The Perfluorosulfonic Acid Proton Exchange Membrane (PFSA PEM) market centers around high-performance polymer electrolytes essential for converting chemical energy into electrical energy (fuel cells) or producing hydrogen through water splitting (electrolyzers). PFSA membranes, typified by materials like Nafion, possess a robust perfluorinated backbone attached to highly acidic sulfonate groups, enabling exceptionally high proton conductivity and thermal stability necessary for demanding electrochemical environments. These characteristics make them irreplaceable components in high-efficiency hydrogen technologies, positioning them at the core of the burgeoning hydrogen economy. The major applications for PFSA PEMs span Fuel Cell Electric Vehicles (FCEVs), grid-scale energy storage, and the generation of green hydrogen.

The key driving factors propelling the PFSA PEM market expansion include stringent global emissions regulations pushing for zero-emission vehicles, massive governmental investments in hydrogen infrastructure, and technological advancements reducing the required platinum loading in membrane electrode assemblies (MEAs). Furthermore, the inherent benefits of PFSA membranes—such as long service life, mechanical robustness, and operational efficiency across a broad temperature range—solidify their indispensable role in next-generation power systems. However, ongoing research focuses heavily on optimizing thickness uniformity and reducing the overall cost of production to accelerate mass adoption across industrial scales.

Product descriptions emphasize the membrane's equivalent weight, thickness (ranging from 10 to 100 micrometers), and performance metrics like proton conductivity and gas crossover rate. The market recognizes PFSA membranes as foundational technology, directly impacting the power density and durability of fuel cell stacks. Primary benefits include high power output, environmental sustainability compared to fossil fuels, and rapid refueling capabilities in the transportation sector. These factors ensure continued demand growth, especially in Asia Pacific, where FCEV deployment is aggressively prioritized.

The Perfluorosulfonic Acid Proton Exchange Membrane market is characterized by intense technological competition and significant capitalization stemming from the global energy transition. Business trends show a strong emphasis on strategic partnerships between chemical manufacturers (suppliers of PFSA polymer), MEA fabricators, and automotive OEMs, aiming to stabilize the supply chain and scale production capacity, particularly for ultra-thin membranes crucial for high-power density applications. Regional trends highlight Asia Pacific (APAC) as the dominant and fastest-growing region, driven by extensive government incentives in China, Japan, and South Korea to deploy hydrogen mobility and stationary fuel cells. Europe is also a pivotal hub, focusing on green hydrogen production via large-scale electrolyzers, aligning with the EU’s Hydrogen Strategy. Segment trends reveal the automotive segment (FCEVs) holding the largest market share due to volume requirements, while the electrolysis segment is poised for the highest growth CAGR, reflecting the urgent need for large-scale green hydrogen production to decarbonize industrial processes and energy grids.

User queries regarding AI's influence in the PFSA PEM sector commonly revolve around how artificial intelligence can overcome traditional material science limitations, specifically focusing on cost reduction, lifespan extension, and optimization of manufacturing consistency. Key themes identified include the application of machine learning for novel polymer synthesis screening, predictive modeling of membrane degradation under various operating conditions, and optimization of the complex coating processes involved in fabricating membrane electrode assemblies (MEAs). Users are keen to understand if AI can accelerate the transition to less expensive or more durable alternatives while maintaining the high performance characteristic of traditional PFSA membranes. The summary indicates that AI is increasingly viewed as a crucial tool for accelerating R&D cycles, improving quality control in high-volume production, and drastically enhancing the efficiency of catalyst application to the membrane surface, thereby directly addressing the high cost and complexity constraints currently facing the mass commercialization of fuel cells and electrolyzers.

The PFSA PEM market dynamics are shaped by powerful Drivers (D), significant Restraints (R), and compelling Opportunities (O), which collectively define the Impact Forces governing market expansion. Key drivers include accelerating government policies supporting clean energy and FCEV deployment, coupled with technological advancements that increase the power density and durability of fuel cell stacks. Restraints primarily involve the persistently high cost of PFSA materials and the dependency on complex, capital-intensive manufacturing processes, alongside environmental concerns associated with per- and polyfluoroalkyl substances (PFAS). Opportunities arise from the burgeoning green hydrogen economy, demanding vast quantities of membranes for electrolyzers, and the potential for developing next-generation membranes (e.g., reinforced PFSA) to enhance operational temperature tolerance. These forces collectively dictate market trajectory, pushing for innovation in cost reduction while capitalizing on global decarbonization mandates.

The Perfluorosulfonic Acid Proton Exchange Membrane market is segmented primarily based on membrane thickness, end-use application, and proton exchange equivalent weight (EW). Thickness is a critical factor, as thinner membranes (below 30 micrometers) are required for high-power density automotive applications, while thicker membranes offer enhanced durability for stationary power. Segmentation by application clearly defines the primary demand vectors: transportation (FCEVs and buses), stationary power (backup power, combined heat and power), and electrolysis (hydrogen generation). The equivalent weight (EW), which represents the grams of dry polymer per mole of sulfonic acid groups, dictates conductivity and water management characteristics, serving as a key metric for performance customization, allowing manufacturers to tailor membranes specifically for high-temperature or low-humidity operations. This comprehensive segmentation provides a clear framework for understanding varied market needs and targeting specific technological advancements.

The value chain for the PFSA PEM market is highly specialized and capital-intensive, starting with the upstream supply of specialized raw materials. Upstream activities involve the production of high-purity perfluorinated monomers and subsequent polymerization processes to create the PFSA ionomer resin. This stage is dominated by a few global chemical giants due to the complexity and proprietary nature of the fluorochemical synthesis. Raw material purity is paramount, directly influencing the final membrane conductivity and durability. The midstream involves the crucial step of solution casting or extrusion of the PFSA resin into thin film membranes, followed by chemical treatments (acid treatment) and integration into the membrane electrode assembly (MEA) by specialist fabricators. This fabrication step is critical, as it defines the final product’s performance characteristics.

Downstream analysis focuses on the integration of MEAs into functional fuel cell stacks and electrolyzer systems. Distribution channels are predominantly direct, characterized by long-term contracts between MEA manufacturers and major system integrators (e.g., automotive OEMs, stationary power providers, and hydrogen plant developers). Indirect channels are less common but exist through specialized distributors providing finished fuel cell stacks or repair components to niche markets. The high technical specification and need for customized solutions necessitate close collaboration throughout the supply chain, ensuring that the membranes meet the rigorous demands of automotive or industrial environments.

The overall structure of the value chain shows significant vertical integration attempts by key players seeking to control the supply of ionomers and improve MEA consistency, thereby reducing overall manufacturing costs and ensuring competitive pricing. Controlling the upstream chemical synthesis provides significant market leverage. The market's high barriers to entry, driven by intellectual property and required technical expertise, solidify the positions of established manufacturers across the entire chain, from raw resin production to stack integration.

Potential customers, or end-users/buyers, of Perfluorosulfonic Acid Proton Exchange Membranes fall into several high-growth, technically demanding industries centered on energy conversion and storage. The primary customer base consists of major automotive manufacturers (Original Equipment Manufacturers or OEMs) focused on developing Fuel Cell Electric Vehicles (FCEVs) like cars, buses, and heavy-duty trucks, where high power density and extended range are critical. The second largest and rapidly expanding customer group includes green hydrogen developers and industrial engineering firms that purchase membranes for large-scale water electrolyzers (e.g., Polymer Electrolyte Membrane Electrolyzers or PEMELs) used in grid balancing, industrial feedstock production, and synthetic fuel synthesis. Additionally, manufacturers of stationary power systems, particularly those providing uninterruptible power supplies (UPS) and combined heat and power (CHP) units for data centers and remote applications, represent a stable segment of potential customers seeking reliable, long-duration power solutions. Research institutions and military contractors also constitute a niche but essential customer segment requiring specialized membrane formulations for testing and defense applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 485.5 million |

| Market Forecast in 2033 | USD 1,375.9 million |

| Growth Rate | 15.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Chemours (DuPont), 3M, Asahi Kasei, Solvay, Gore, Ballard Power Systems (MEA focus), FuelCell Energy, Plug Power, Dongyue Group, Toray Industries, AGC Inc., Sumitomo Chemical, Johnson Matthey, Ionomr Innovations, W. L. Gore & Associates. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for the Perfluorosulfonic Acid Proton Exchange Membrane market is focused heavily on enhancing efficiency, extending lifespan, and achieving manufacturing economies of scale. Current core technologies center on the chemical synthesis of PFSA ionomers, primarily through dispersion polymerization or melt extrusion processes, ensuring the polymer backbone exhibits optimal mechanical strength and thermal resilience. A key technological focus is the development of ultra-thin membranes (less than 20 µm) which significantly reduce ohmic losses within the fuel cell stack, thereby maximizing power output density essential for FCEVs. These ultra-thin structures, however, require specialized reinforcement techniques, often involving ePTFE (expanded polytetrafluoroethylene) or other porous substrates, to maintain mechanical integrity and prevent pinhole formation during operation.

A significant area of ongoing R&D is the refinement of the membrane electrode assembly (MEA) preparation, which utilizes the PFSA membrane. Critical innovations include the implementation of advanced coating techniques, such as decal transfer or slot-die coating, to precisely apply catalyst layers (typically platinum or platinum alloys) onto the membrane or gas diffusion layer (GDL). Achieving uniform catalyst distribution and minimizing loading without sacrificing performance is crucial for cost reduction. Furthermore, there is growing interest in high-temperature PFSA membranes, which aim to operate efficiently above 100°C, simplifying water management in fuel cells by reducing the need for extensive humidification systems, thus offering better thermal efficiencies in demanding applications like heavy transport.

The technological evolution is also focused on developing PFSA alternatives, particularly partially fluorinated or non-fluorinated hydrocarbon-based membranes, driven by regulatory pressure regarding PFAS chemicals and the desire for lower-cost solutions. However, PFSA technology currently retains market dominance due to its unparalleled performance metrics, forcing innovation within the PFSA category itself. Key patent activity revolves around novel side-chain chemistries for increased chemical stability and the integration of inorganic fillers (hybrid membranes) to mitigate membrane dehydration and swelling, thereby stabilizing performance during dry cycling and extended usage periods, particularly in the rapidly growing PEM electrolyzer sector.

Regional dynamics play a crucial role in shaping the PFSA PEM market, largely correlating with governmental support for the hydrogen economy and the penetration rate of fuel cell electric vehicles and industrial electrolyzers. Asia Pacific (APAC) currently dominates the market share and is projected to exhibit the highest growth rate. This leadership is underpinned by aggressive national hydrogen strategies in countries like China, Japan, and South Korea, involving massive subsidies for FCEV adoption and significant investment in hydrogen refueling infrastructure. China, in particular, is driving demand through large-scale deployment of fuel cell buses and commercial vehicles, positioning it as the key manufacturing hub and consumer of PFSA membranes, requiring immense scale and consistency from suppliers.

Europe represents the second most critical region, with market growth heavily skewed towards green hydrogen production via PEM electrolyzers. The European Union’s commitment to decarbonization and the targets set forth in the European Hydrogen Strategy are driving significant capacity build-out, especially in countries like Germany, the Netherlands, and Scandinavia. This focus translates into robust demand for large-format, durable PFSA membranes optimized for continuous industrial electrolysis. Regulations promoting clean energy and the phase-out of internal combustion engines further stimulate the adoption of fuel cell systems in maritime and heavy transport applications across the continent.

North America, led by the United States and Canada, presents a mature yet accelerating market. Market expansion here is fueled by state-level hydrogen hubs (e.g., California, Northeast Corridor) and significant federal investments aimed at reducing the cost of clean hydrogen production (Hydrogen Shot initiative). While FCEV adoption is strong, particularly in commercial fleet operations, North America is also a major innovator in membrane technology, housing key R&D facilities and major suppliers. The combination of established suppliers, technological leadership, and renewed federal backing ensures sustained high demand for high-performance PFSA membranes across automotive, stationary, and utility-scale hydrogen generation segments.

The primary applications driving demand are Fuel Cell Electric Vehicles (FCEVs), particularly heavy-duty trucks and buses requiring high power density, and Polymer Electrolyte Membrane (PEM) electrolyzers utilized for the large-scale production of green hydrogen.

The main challenge is the high cost of the perfluorinated raw materials and the complex, precision-dependent manufacturing processes required to produce ultra-thin, highly durable, and contamination-resistant membranes suitable for long-term use in dynamic electrochemical environments.

Thinner membranes (10-30 µm) increase power density by reducing ohmic resistance, making them ideal for automotive use, but they require advanced reinforcement to maintain mechanical strength. Thicker membranes offer greater durability for stationary or electrolysis applications.

Asia Pacific (APAC), specifically driven by governmental commitments and technological adoption in China, Japan, and South Korea, leads the market due to robust investments in FCEV deployment and localized manufacturing capabilities for membrane electrode assemblies.

Yes, significant research is focused on developing non-fluorinated hydrocarbon-based membranes and partially fluorinated alternatives to address concerns regarding Per- and Polyfluoroalkyl Substances (PFAS). However, PFSA remains the benchmark due to its superior proton conductivity and chemical stability.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.