ID : MRU_ 431417 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

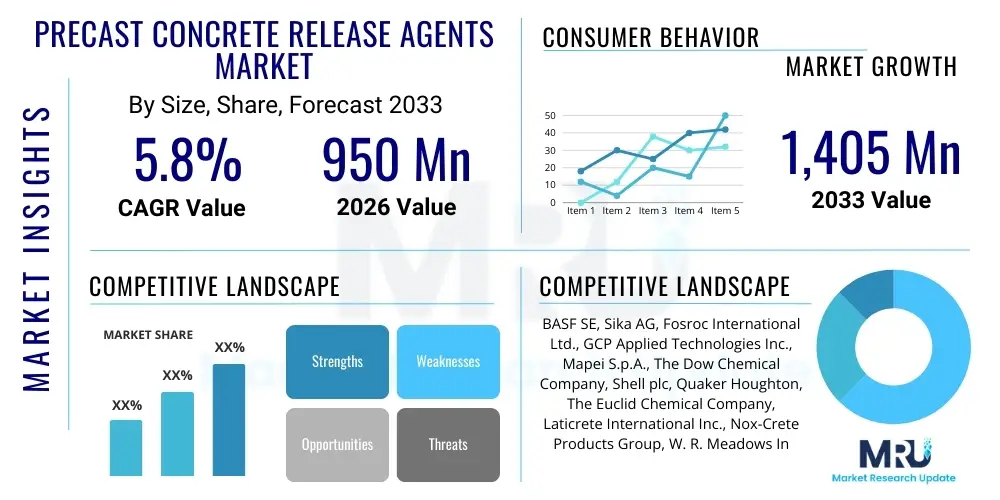

The Precast Concrete Release Agents Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 950 million in 2026 and is projected to reach USD 1,405 million by the end of the forecast period in 2033. This robust growth trajectory is primarily fueled by the accelerating adoption of sustainable construction practices and the increasing global demand for standardized, high-quality infrastructure components produced efficiently in precast facilities. The shift towards automated and high-throughput concrete molding processes necessitates superior release agents that ensure mold integrity, minimize surface blemishes, and reduce cleaning time, thereby boosting operational efficiency in large-scale construction projects.

The market expansion is intrinsically linked to macro-economic indicators such as urbanization rates and governmental investments in public works, particularly in emerging economies across Asia Pacific and Latin America. As precast concrete gains preference over traditional cast-in-place methods due to its speed, precision, and cost-effectiveness, the consumption of specialized release agents rises proportionally. Furthermore, technological advancements in agent formulations, including the introduction of bio-degradable and non-staining variants, are addressing stringent environmental regulations and driving premium pricing, contributing significantly to the overall market valuation increase throughout the forecast period.

A crucial factor influencing market size is the recurring demand nature of these consumable chemicals. Release agents are essential components in every precasting cycle, making the market highly sensitive to fluctuations in the global construction industry's output. While short-term economic downturns might momentarily affect construction starts, the underlying, long-term trend toward modular and prefabricated construction methods solidifies the sustained demand for high-performance release agents. Companies are focusing on optimizing product delivery and storage stability to cater to diverse climates and operational scales, ensuring continuous market penetration and value capture.

Precast Concrete Release Agents are specialized chemical formulations applied to the surface of molds or forms before concrete pouring to prevent the fresh concrete from adhering to the mold surface. These agents are crucial for ensuring the smooth, clean demolding of finished precast elements, resulting in high-quality surface finishes and extending the operational life of expensive molds. The fundamental function is to create a thin, protective barrier or chemical reaction layer between the concrete and the formwork. Major applications span structural elements (beams, columns, panels), transportation infrastructure (railroad ties, barriers), architectural components, and utility structures (pipes, vaults). Key benefits include reduced labor costs associated with mold cleaning, decreased damage to concrete components during stripping, and improved aesthetic quality of the final product.

The product portfolio within this market is diverse, generally categorized by chemical composition, primarily including oil-based (mineral and vegetable oils), water-based, and synthetic/chemical reactive agents. Oil-based agents, particularly those derived from renewable resources like vegetable oil, are gaining traction due to their enhanced environmental profile and reduced volatile organic compound (VOC) emissions, aligning with global sustainability mandates. Reactive agents, which chemically interact with the calcium hydroxide in the cement, offer superior performance for intricate molds and high-density concrete mixes, providing a virtually stain-free release necessary for architectural precast elements.

Driving factors for this market are multi-faceted, encompassing rapid global infrastructure development, particularly in Asia Pacific, the mandatory shift towards greener construction materials, and the increasing standardization of construction processes utilizing precast technology. The growing labor shortage in traditional construction methods further accelerates the adoption of efficient, factory-controlled precast production. Moreover, stringent quality requirements for specialized precast products, such as high-strength concrete elements for bridges and high-rises, demand premium release agents that guarantee dimensional accuracy and impeccable surface finish, thereby sustaining market growth and innovation.

The Precast Concrete Release Agents Market is characterized by robust growth, driven primarily by the global pivot towards industrialized construction methods and heightened regulatory focus on environmental compliance. Business trends indicate a significant shift from traditional mineral oil-based agents towards water-based and bio-degradable formulations. Key industry players are heavily investing in R&D to develop proprietary chemical reactive agents that offer zero residue and superior protection for advanced formwork materials like polymer composites and high-density plastics. Strategic mergers, acquisitions, and long-term supply agreements with major precast manufacturers are common tactics employed to consolidate market share and ensure stable distribution networks globally. The competitiveness is centered not just on pricing, but increasingly on technical support and customized formulations tailored to specific concrete mix designs and curing environments.

Regionally, the Asia Pacific (APAC) market dominates in terms of consumption volume, propelled by massive urbanization projects and significant governmental spending on high-speed rail and utility infrastructure in countries like China and India. North America and Europe, while slower in volume growth, lead the market in terms of value and technological adoption, primarily focusing on high-performance, sustainability-focused products compliant with strict VOC regulations (e.g., EU REACH). The Middle East and Africa (MEA) region is experiencing accelerated growth due to substantial construction activities related to major events and economic diversification initiatives, demanding fast-curing concrete elements and corresponding specialized release chemistries.

In terms of segmentation trends, the water-based agents segment is exhibiting the fastest CAGR, largely due to its superior environmental footprint and ease of cleanup, making it highly attractive for indoor precasting facilities. By application, the Structural Elements segment maintains the largest market share, reflecting the widespread use of precast technology in foundational and load-bearing construction. Furthermore, mold material segmentation shows rising demand for agents optimized for non-traditional formwork materials, such as rubber, fiberglass, and specialized metal alloys, which require minimal abrasive interaction and maximum surface preservation. These segmented trends underline a market moving towards specialization, efficiency, and ecological responsibility.

User inquiries regarding AI's influence on the Precast Concrete Release Agents Market primarily revolve around optimizing application processes, predicting consumption patterns, and enhancing quality control. Users often question how machine learning (ML) models can be integrated into automated precasting lines to precisely calculate the required volume of release agent per square meter, minimizing overspray and waste. A recurring theme is the expectation that AI can analyze data collected from curing environments (temperature, humidity, concrete mix specifications) to recommend the optimal release agent formulation and concentration for a specific batch, thereby maximizing demolding efficiency and guaranteeing a flawless finish. Concerns also focus on the integration cost and the necessity of specialized sensors and IoT infrastructure within precast plants to gather the requisite data for meaningful AI utilization.

The practical application of AI in this niche market is concentrated on process optimization rather than chemical innovation. Predictive maintenance algorithms are being deployed to monitor the degradation and residue accumulation on expensive molds, signaling when and how much agent should be reapplied or which type of cleaning is required, significantly extending formwork longevity. Furthermore, AI-driven computer vision systems can instantaneously inspect the surface finish of demolded concrete elements, comparing actual results against desired quality metrics and providing immediate feedback loop adjustments to the agent application robots, ensuring consistent quality across high-volume production lines. This transition from manual, experience-based application to data-driven, precise coating is critical for high-volume, automated precasting facilities.

The overarching impact of AI is the transition toward a 'smart factory' environment where material inputs, including release agents, are managed as variables in a complex predictive model aimed at maximizing throughput and minimizing defects. This necessitates closer collaboration between release agent manufacturers and automation providers, leading to the development of agents specifically formulated for robotic spray systems with tight tolerance parameters. AI ensures that the selection and application of these agents are no longer based on standardized procedures but dynamically adjusted in real-time based on fluctuating environmental or material conditions, thus elevating the role of high-tech chemical suppliers in the construction technology ecosystem.

The market for precast concrete release agents is subjected to a powerful combination of Driving factors, Restraints, and Opportunities (DRO), collectively forming significant Impact Forces. Key drivers include the global infrastructural boom, particularly the rapid expansion of affordable housing and commercial infrastructure demanding fast construction schedules facilitated by precast technology. The environmental driver is equally strong, mandating a shift toward sustainable, low-VOC, and bio-degradable chemical agents, which pushes innovation and premium pricing. Opportunities are largely concentrated in the development of highly specialized agents for niche applications, such as self-compacting concrete (SCC) or ultra-high-performance concrete (UHPC), and the expansion into emerging markets where precast adoption is still nascent but rapidly growing. These dynamic forces shape the investment strategies and competitive landscape of the market.

However, the market faces significant restraints. The primary challenge is the volatility of raw material prices, particularly petrochemical derivatives and natural oils, which directly affects the production costs and final pricing of release agents. Furthermore, the lack of standardized regulatory frameworks across developing countries regarding VOC content and biodegradability can slow the adoption of higher-cost, specialized green agents. There is also a technical restraint involving the potential incompatibility between certain release agent chemistries and complex admixtures used in modern concrete mixes, sometimes leading to discoloration or impaired bond strength if not applied correctly. These restraints necessitate meticulous product testing and robust technical support from suppliers.

The Impact Forces are heavily skewed towards positive growth driven by technological adaptation and sustainability mandates. The immediate impact is the rapid obsolescence of traditional, non-biodegradable mineral oil-based agents in developed economies. The long-term impact involves cementing the position of high-performance, water-based, and chemical reactive agents as industry standards. The need for operational efficiency in automated precast plants ensures that specialized agents which reduce mold cleaning time and guarantee flawless finishes will command a premium. This continuous demand for specialized, high-quality, and environmentally sound products acts as a powerful, sustained upward pressure on market value, mitigating the effects of periodic raw material price volatility.

The Precast Concrete Release Agents market is meticulously segmented based on product type (chemical composition), application (end-use sectors), formwork material, and region, allowing manufacturers to precisely target specific industrial needs. The chemical composition segmentation is crucial, differentiating between oil-based (further subdivided into mineral and vegetable oil derivatives), water-based emulsions, and chemical reactive agents. Water-based agents, which utilize surfactants and emulsifiers to achieve separation, are highly favored in eco-conscious markets due to their low environmental impact and ease of handling. This granular segmentation reflects the high degree of specialization required to meet the varied requirements of modern precast manufacturing, which utilize diverse mix designs and curing techniques.

Segmentation by application highlights the distinct demands of various construction sectors. The structural elements segment, encompassing beams, columns, and foundational components, is the largest consumer due to the sheer volume of material required for commercial and residential construction. Conversely, the architectural precast segment, focusing on aesthetic panels and intricate facades, drives the demand for premium, non-staining, chemical-reactive agents that ensure perfect surface quality. This application-based differentiation dictates the performance criteria, pricing, and packaging strategies adopted by suppliers, recognizing that a standard agent suitable for basic structural components may be inadequate for complex architectural pours.

Further analysis of segmentation by formwork material (e.g., steel, plywood, plastic, fiberglass) is essential because the effectiveness of a release agent is intrinsically linked to the mold surface porosity and composition. Agents designed for high-density, non-porous steel molds differ significantly from those required for porous timber or fiberglass forms. The trend towards specialized formwork materials, particularly polymer and composite molds used for highly detailed or repetitive shapes, ensures sustained demand for customized, high-adhesion release films. Overall, the market's segmentation underscores a shift from generic chemical sales to highly technical, solution-oriented offerings tailored to specific concrete production environments.

The value chain for the Precast Concrete Release Agents Market initiates with upstream activities, focusing on the sourcing and processing of core raw materials. These materials primarily include base oils (mineral oils, vegetable oils like rapeseed or coconut oil), specialized surfactants, emulsifiers, anticorrosive additives, and various chemical reactants. Manufacturers in the upstream segment must secure stable supplies of these commodities, which are often subject to volatile global prices. The quality and purity of these sourced components directly influence the performance and regulatory compliance (e.g., VOC limits, biodegradability) of the final release agent product. Efficiency in this stage involves minimizing waste during chemical synthesis and optimizing logistics for bulk ingredients.

Midstream activities involve the formulation, blending, and packaging of the release agents. Chemical companies and specialized manufacturers undertake proprietary blending processes to create agents tailored for specific concrete types, curing temperatures, and mold materials. This stage adds significant value through intellectual property and technical expertise, ensuring the finished product provides reliable performance under varying operational conditions. Stringent quality control and certification processes (e.g., ISO standards, environmental certifications) are integral parts of the midstream value chain, validating product effectiveness and safety before distribution. Manufacturers often operate specialized regional production facilities to minimize transportation costs of bulk liquids.

Downstream activities center on distribution channels and end-user engagement. Distribution channels include direct sales to large precast concrete manufacturers, where high volumes justify direct technical support and customized formulations, and indirect sales through specialized chemical distributors and construction material retailers for smaller precasting operations. Direct sales allow manufacturers to maintain greater control over product application and gather immediate performance feedback. Indirect channels provide broader market reach. Key downstream services involve technical training, application guidance (e.g., optimal spray patterns, dilution ratios), and post-sale troubleshooting, all aimed at maximizing the effectiveness of the agent for the end-user and cementing supplier-client relationships. The final consumers are the precast concrete plants themselves, demanding reliable, consistent, and compliant products.

The primary customers and end-users of precast concrete release agents are manufacturing entities operating within the built environment sector, specifically those specializing in controlled, factory-based concrete production. This predominantly includes large-scale precast concrete manufacturers who produce standardized elements for residential, commercial, and industrial construction projects. These customers require agents in substantial volumes, often delivered in bulk quantities, and demand high-performance agents that guarantee zero surface defects to maintain the high quality of their products, which are typically subjected to stringent engineering standards and inspections. Their purchasing decisions are heavily influenced by factors such as mold life extension, agent cleaning complexity, and alignment with sustainable procurement policies.

A secondary, yet rapidly growing customer base, consists of specialized infrastructure contractors and public works departments utilizing precast technology for complex projects like tunnel segments, bridge girders, railroad ties, and utility vaults. These customers often work with high-performance concrete mixes (like SCC or UHPC) that require highly reactive and sophisticated release agents to ensure intricate geometrical precision and high compressive strength post-curing. For this segment, performance consistency under harsh environmental conditions and rapid turnaround times are paramount, driving the demand for premium, technologically advanced formulations over generic, cost-effective options.

Furthermore, small and medium-sized enterprises (SMEs) involved in producing specific ornamental, landscaping, or non-structural precast items (e.g., paving stones, statues, garden features) also form a substantial customer segment. While their volume consumption is lower, their demand is highly segmented, often requiring user-friendly, non-hazardous, water-based agents that are easy to store and apply manually. Suppliers target these SMEs through regional distributors and focused product portfolios emphasizing ease of use and environmental safety, providing a robust base for regional market stability and penetration outside major industrial hubs. The common denominator among all potential customers is the need for an agent that ensures clean separation, minimizes residue, and does not compromise the structural integrity or aesthetic quality of the concrete.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 950 million |

| Market Forecast in 2033 | USD 1,405 million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BASF SE, Sika AG, Fosroc International Ltd., GCP Applied Technologies Inc., Mapei S.p.A., The Dow Chemical Company, Shell plc, Quaker Houghton, The Euclid Chemical Company, Laticrete International Inc., Nox-Crete Products Group, W. R. Meadows Inc., Cemex S.A.B. de C.V., CHRYSO SAS (Saint-Gobain), Kurita Water Industries Ltd., KAO Corporation, Henkel AG & Co. KGaA, US Specialty Coatings, Axim Italcementi Group, and FOSAN Chemical Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape for Precast Concrete Release Agents is rapidly evolving, driven by the imperatives of environmental compliance and enhanced concrete quality. The most significant technological shift involves the development of advanced surfactant and emulsification systems that allow for the creation of highly stable water-based (H₂O) release agents. These technological breakthroughs enable manufacturers to deliver performance comparable to traditional solvent-based agents while drastically reducing VOC emissions and eliminating hazardous material handling concerns. Sophisticated blending techniques are essential to ensure that the water-based emulsions remain homogenous and effective across diverse temperature ranges and storage conditions, a critical requirement for global distribution and use in varying climates.

Another pivotal technology focuses on chemical reactive agents, often incorporating fatty acid derivatives or other organic compounds that react with the free lime (calcium hydroxide) present in the setting concrete. This chemical reaction forms a metallic soap film at the interface, ensuring superior, non-adherent separation without leaving sticky or concrete-marring residues. Innovation here centers on optimizing the reaction speed and coverage rate, ensuring effectiveness even with accelerated curing techniques (e.g., steam curing) common in modern precast plants. The goal is to maximize the cleanliness of the demolded surface, which is particularly vital for architectural and specialty precast elements where aesthetic perfection is mandatory.

Furthermore, technology is being deployed not just in the composition of the agent but also in its application. This includes the integration of ultrasonic nozzle technology and precision robotic spray systems designed to apply a consistently thin, micron-level coating. This optimization reduces agent consumption and guarantees uniform coverage, preventing the concrete "burn" or discoloration often associated with manual or inconsistent application. Smart packaging and delivery systems, including IoT-enabled bulk dispensing units that monitor inventory and usage, also represent technological advancements aimed at improving operational efficiency and reducing waste within high-volume precasting operations.

The global market exhibits distinct regional dynamics reflecting varying levels of infrastructural maturity, regulatory environments, and adoption rates of precast technology. Asia Pacific (APAC) stands as the largest and fastest-growing region, primarily due to massive investments in residential, commercial, and public infrastructure projects, particularly in China, India, and Southeast Asian countries. The sheer volume of construction activity necessitates high-volume consumption of release agents. While cost-effectiveness often drives purchasing decisions in this region, increasing environmental regulations, especially in developed APAC nations like Japan and South Korea, are rapidly accelerating the shift toward water-based and bio-degradable agents.

Europe represents a mature market characterized by stringent environmental regulations, particularly concerning VOC content and product biodegradability, driven by EU directives such as REACH. Consequently, European demand is highly concentrated on premium, advanced water-based and specialty chemical reactive agents that guarantee compliance and superior finish quality. Innovation in Europe often centers on agents designed for advanced formwork and specialized concrete mixes like UHPC used in sophisticated architectural and civil engineering structures. The market growth here is stable, driven more by value and technological upgrades than by volume expansion.

North America maintains a strong market position, driven by robust private sector construction and governmental infrastructure modernization programs. Similar to Europe, the focus in the U.S. and Canada is increasingly on high-performance, compliant formulations. The adoption of automated precasting facilities in North America necessitates agents compatible with robotic application systems, driving technological integration. The Middle East and Africa (MEA) region shows significant growth potential, fueled by mega-projects and diversification efforts in the Gulf Cooperation Council (GCC) countries. These projects require rapid construction and high quality, ensuring sustained demand for specialized release agents capable of performing reliably in high-temperature environments.

Chemical reactive agents interact with the cement's free lime to form a non-stick soap film, offering superior, stain-free release ideal for architectural precast. Barrier agents, such as oils, physically separate the concrete and the mold, best suited for basic structural elements and highly porous formwork materials like plywood.

Sustainability is driving significant market transformation, pushing manufacturers towards low-VOC (Volatile Organic Compound), non-toxic, and bio-degradable formulations, primarily water-based and vegetable oil-based agents, to comply with stricter environmental regulations and green building standards globally.

The Asia Pacific (APAC) region currently holds the largest market share in terms of volume consumption, driven by extensive governmental and private investment in massive infrastructure and urbanization projects across emerging economies like China and India.

Agent selection is determined by the formwork material (e.g., steel vs. timber), the type of concrete mix (e.g., standard vs. self-compacting concrete), the desired surface finish quality (aesthetic vs. structural), and the local environmental and safety regulations regarding VOC content.

High-quality release agents protect molds by preventing concrete adhesion and abrasion during demolding and cleaning. Agents minimize physical wear and chemical damage, significantly reducing maintenance costs and extending the useful operational life of expensive formwork, especially specialized steel or polymer molds.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.