ID : MRU_ 434218 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

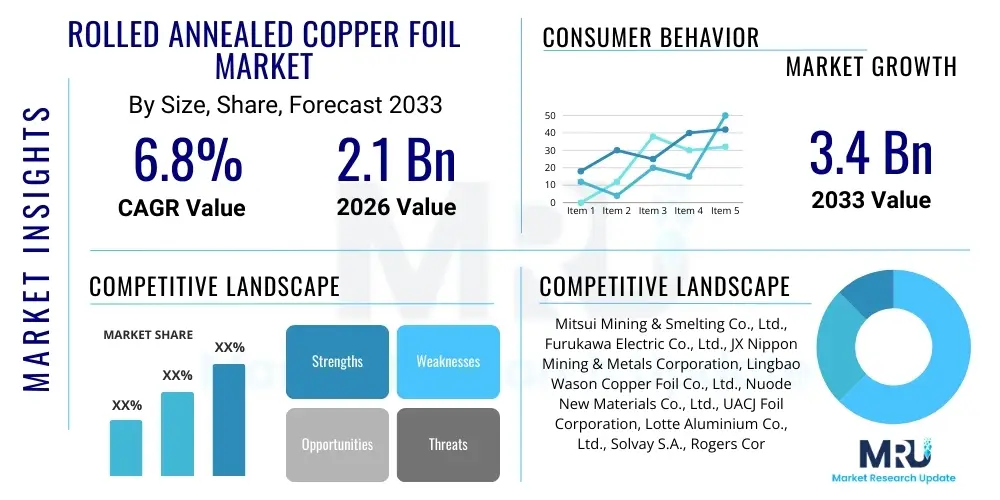

The Rolled Annealed Copper Foil Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 2.1 Billion in 2026 and is projected to reach USD 3.4 Billion by the end of the forecast period in 2033.

The Rolled Annealed Copper Foil Market encompasses the manufacturing and distribution of specialized copper sheeting characterized by superior mechanical properties, including high ductility, excellent flexibility, and exceptional grain structure uniformity, achieved through meticulous rolling and subsequent annealing processes. Unlike standard electrodeposited (ED) copper foil, Rolled Annealed (RA) copper foil offers enhanced bending fatigue resistance and higher tensile strength, making it indispensable in demanding applications requiring maximum reliability and performance stability. This specific manufacturing methodology ensures a smooth surface finish and precise thickness control, which are critical parameters for high-density circuit integration and advanced thermal management solutions. The superior physical characteristics of RA copper foil are positioning it as the material of choice across several high-growth industries globally.

Key applications driving the demand for RA copper foil include the production of Flexible Printed Circuit Boards (FPCBs), Shielding Materials, Lithium-Ion Battery Anodes, and high-frequency communication modules where signal integrity is paramount. In FPCBs, the inherent flexibility and high crack resistance of RA foil enable complex designs for compact, mobile, and wearable electronic devices. Furthermore, the material's low resistance and high conductivity enhance energy transfer efficiency, a vital consideration in electric vehicle (EV) battery packs and sophisticated power electronics. The benefits of using RA copper foil extend beyond mere conductivity; its structural integrity under repeated mechanical stress significantly prolongs the lifespan of end products, offering substantial competitive advantage in sectors prioritizing long-term durability and miniaturization. The stringent quality requirements of aerospace and medical electronics further solidify the specialized demand for RA foil over conventional alternatives.

Major driving factors underpinning market expansion include the exponential proliferation of consumer electronics, particularly smartphones and tablets, which heavily rely on FPCBs for compact designs. Furthermore, the global transition towards electric mobility is generating massive demand for high-performance battery components, where RA copper foil serves as the current collector in anodes, optimizing energy density and charging cycles. The rollout of 5G and future 6G communication technologies necessitates materials with superior signal transmission capabilities at ultra-high frequencies, where the structural homogeneity of RA copper minimizes signal loss and interference. Regulatory pressures promoting energy efficiency and device reliability also incentivize manufacturers to adopt premium materials like RA copper foil, ensuring market vitality across diverse technological landscapes.

The Rolled Annealed Copper Foil market is experiencing robust growth driven by accelerating digitalization, the proliferation of electric vehicles (EVs), and foundational advancements in 5G infrastructure, positioning it as a critical enabler in high-performance electronics. Business trends indicate a heightened focus on capacity expansion among leading manufacturers, particularly those specializing in ultra-thin foil production (below 9 µm), catering to the density requirements of advanced IC packaging and high-efficiency battery designs. Strategic mergers and acquisitions are observed as major players seek to consolidate supply chains and acquire proprietary annealing and rolling technologies, ensuring superior quality control and cost efficiency. Furthermore, sustainability initiatives are influencing business strategies, leading to investments in closed-loop manufacturing processes to minimize copper waste and energy consumption, appealing to environmentally conscious downstream partners.

Regionally, Asia Pacific (APAC) maintains overwhelming dominance, largely attributable to the massive manufacturing bases for consumer electronics, automotive components, and lithium-ion batteries located in China, South Korea, Japan, and Taiwan. Government subsidies and favorable policies promoting EV production in APAC further solidify its market leadership. North America and Europe, while smaller in volume, exhibit strong growth in high-value, specialized segments such as aerospace, defense, and high-reliability medical devices, driven by stringent quality standards and a demand for localized, secure supply chains. Emerging markets in Latin America and the Middle East are beginning to show increased demand, primarily related to telecommunications infrastructure upgrades and foundational industrial electronics manufacturing, though they currently represent a minor share of the global market.

Segment trends highlight the exceptional growth of the Battery Application segment, which is consistently outpacing traditional PCB applications due to the global energy storage boom. Within the thickness segmentation, foils ranging from 6 µm to 12 µm are commanding the highest demand volumes for standard FPCB and battery applications, while the ultra-thin segment (<6 µm) is witnessing the steepest growth rate, driven by cutting-edge miniaturization requirements. The preference for high-purity copper (>99.99%) remains universal across all segments, emphasizing the non-negotiable requirement for material quality to ensure optimal electrical and thermal performance. The continuous refinement of rolling technologies is enabling manufacturers to meet increasingly tight tolerance specifications demanded by next-generation electronics architecture.

User queries regarding the impact of Artificial Intelligence (AI) on the Rolled Annealed Copper Foil Market predominantly revolve around three critical areas: optimization of manufacturing processes, predictive maintenance for high-precision equipment, and the derivative demand driven by AI hardware infrastructure. Users are concerned about how AI can enhance the difficult process of achieving uniform grain size and surface smoothness, key determinants of RA foil quality, and whether AI-driven predictive analytics can minimize defects and scrap rates in the highly capital-intensive rolling mills. A major theme is the indirect market boost: the exponential growth of AI and Machine Learning (ML) hardware, particularly high-performance computing (HPC) and advanced data centers, necessitates complex, high-reliability PCBs and advanced cooling systems, increasing the demand for premium RA copper foil with exceptional thermal management capabilities. Furthermore, the sophistication of new AI devices, such as specialized neural processing units (NPUs), demands increasingly miniaturized and flexible circuitry, directly driving innovation in ultra-thin RA foil production.

The Rolled Annealed Copper Foil market dynamics are shaped by a complex interplay of robust technological drivers, significant capital investment constraints, burgeoning opportunities in emerging technology sectors, and the resulting impact forces that dictate competitive positioning and pricing strategies. Drivers, such as the accelerating adoption of electric vehicles and the widespread deployment of 5G networks globally, are creating sustained, high-volume demand, pushing manufacturers to enhance production capacity and technological capabilities. Concurrently, restraints including the high initial capital expenditure required for sophisticated rolling and annealing equipment, coupled with the volatility in global raw copper prices, impose significant barriers to entry and affect profit margins. Opportunities are primarily centered on developing ultra-thin foils (<5 µm) for advanced packaging and flexible electronics, alongside geographical expansion into nascent manufacturing hubs. These dynamics translate into strong impact forces, leading to increased focus on technological differentiation and strategic long-term supply agreements with major EV battery and FPCB manufacturers to secure market share and mitigate raw material risk.

Key drivers include the indispensable role of RA copper foil in enhancing battery performance, particularly in terms of energy density and fast-charging capability, which is critical for the automotive industry's electrification roadmap. The requirement for flexible, highly durable interconnects in sophisticated consumer devices, such as foldable smartphones and medical implants, also acts as a powerful driver, prioritizing RA foil’s superior mechanical resilience over electrodeposited alternatives. Conversely, the market faces strong headwinds from technological substitution risks, particularly the research into alternative current collector materials, although copper remains the gold standard for conductivity and cost-effectiveness. The reliance on highly specialized, imported equipment for precision rolling further restrains expansion flexibility in several key regions, necessitating strategic partnerships or deep technological expertise for scaling operations effectively.

The opportunity landscape is defined by the potential integration of RA foil into next-generation energy storage solutions, including solid-state batteries, and its increasing application in aerospace and defense systems that demand zero-failure components due to extreme operating environments. Furthermore, improving energy efficiency standards globally fosters the adoption of high-quality materials like RA foil in power modules and induction components. The impact forces compel market players towards continuous process innovation, particularly in surface treatment technologies (e.g., low-profile treatment or adhesion-promoting coatings) that enhance the bond strength between the copper foil and dielectric substrate. Intense competition necessitates efficiency improvements throughout the value chain, ensuring that premium quality is delivered at a competitive cost, while global regulatory standards for material traceability and sustainability increasingly become factors of competitive differentiation.

The Rolled Annealed Copper Foil Market is meticulously segmented based on key differentiators including thickness, application area, and end-use industry, reflecting the diverse and specialized requirements of downstream electronics and energy sectors. Thickness segmentation is crucial as it directly relates to the application, with ultra-thin foils (<6 µm) targeting advanced packaging and high-frequency communication, while thicker foils (18 µm and above) are generally used for power modules and standard PCB grounding layers. The application segmentation clearly delineates the market into Flexible Printed Circuit Boards (FPCBs), which prioritize flexibility and fatigue resistance, and Lithium-Ion Battery Anodes, which prioritize current collection efficiency and lifespan under electrochemical cycling. Understanding these segmentation nuances is vital for manufacturers to align their specific rolling and annealing capabilities with distinct market demands, ensuring optimal product specifications and maximum revenue capture in high-growth niches.

The FPCB application segment remains a stable driver, heavily reliant on the continuous evolution of consumer electronics demanding more compact and flexible designs, necessitating RA foil due to its superior mechanical bend radius capabilities compared to ED foil. However, the Battery Application segment is forecasted to exhibit the highest CAGR, driven by global gigafactory expansions and the mandate for higher energy density in EVs, which requires thinner, more uniformly processed copper foil to maximize active material loading. Geographically, segmentation analysis emphasizes the critical role of the APAC region as the primary consumption hub across all segments, dictating global pricing trends and influencing technological investment cycles, especially in battery-grade foil production.

Furthermore, segmentation by end-use industry—Automotive, Consumer Electronics, Industrial, and Aerospace/Defense—reveals varying quality and regulatory requirements. The Automotive segment, particularly for EV battery packs, demands extremely high purity and consistent performance over prolonged periods, influencing supplier selection criteria. Conversely, the Consumer Electronics segment, while volume-driven, is highly sensitive to cost and rapid product cycles, requiring swift response and robust supply chain resilience from RA foil producers. The strict quality and traceability demanded by Aerospace applications represent a premium, lower-volume segment, emphasizing the market's differentiation based on performance characteristics tailored for specific industrial mandates.

The value chain for the Rolled Annealed Copper Foil Market initiates with the upstream sourcing and refining of high-purity electrolytic copper cathodes, which is a highly capital-intensive stage influenced by global commodity markets and geopolitical stability. This raw material, demanding consistency of over 99.99% purity, is then processed into copper slabs or ingots ready for the primary manufacturing stage. Key upstream analysis focuses on ensuring consistent supply and stable pricing mechanisms, often involving long-term contracts with major copper miners and refiners. The conversion process—involving hot rolling, cold rolling, and the critical annealing stage to achieve the desired grain structure and mechanical properties—represents the core value addition, demanding specialized technology and stringent process control to meet the micron-level specifications required for modern electronics. Manufacturers must constantly optimize their rolling programs to minimize internal stress and defect formation, which are particularly challenging when producing ultra-thin foils.

The distribution channel involves both direct sales and indirect routes. Direct distribution is predominantly utilized for major, high-volume customers such as Tier 1 battery manufacturers and large FPCB houses, enabling customized product specifications and detailed technical support. Indirect channels, involving specialized distributors and agents, cater to smaller electronics manufacturers and regional markets, providing necessary inventory buffering and localized technical expertise. The choice of channel depends heavily on the volume, complexity of requirements, and the geographic reach of the end-user. Effective distribution relies on maintaining specialized handling procedures, as RA copper foil, especially the ultra-thin variety, is sensitive to damage, oxidation, and contaminants during transit, necessitating robust packaging and controlled environmental storage.

Downstream analysis focuses on the integration of RA foil into final products, primarily conducted by FPCB fabricators, battery cell manufacturers, and shielding component producers. This integration requires high-precision lamination, etching, and subsequent assembly processes. Performance feedback from these downstream users is crucial for continuous product improvement, particularly regarding adhesion strength and etching consistency. The end-use application ultimately dictates the quality requirements and profitability of the RA foil. For instance, an automotive battery manufacturer's strict qualification process ensures that only suppliers with proven reliability and scale can participate. Therefore, continuous engagement across the downstream segment, supported by robust technical collaboration, is essential for sustaining long-term market leadership and adapting to evolving technological standards, such as those related to higher voltage battery platforms and advanced packaging solutions.

The primary potential customers and end-users of Rolled Annealed Copper Foil are concentrated within sectors experiencing hyper-growth and requiring miniaturized, high-reliability electronic components, demanding materials with superior mechanical and electrical characteristics. The foremost buyers are Lithium-Ion Battery Cell Manufacturers, particularly those servicing the rapidly expanding Electric Vehicle (EV) and grid-scale Energy Storage System (ESS) markets. These customers require high-volume supply of RA copper foil, often surface-treated, to function as the current collector in the anode, prioritizing thickness consistency, low impurity levels, and mechanical durability to ensure long battery life and safety under repeated cycling. The stringent quality audits and long qualification cycles inherent in the battery sector necessitate robust supplier partnerships and guaranteed material traceability.

Another major customer base includes Flexible Printed Circuit Board (FPCB) Fabricators and Advanced IC Substrate Manufacturers, who rely on RA foil for producing intricate, multi-layer flexible circuits used in mobile phones, wearable technology, and high-density computing modules. For FPCB buyers, the non-negotiable requirement is the foil's high resistance to bending fatigue, allowing their final products to withstand frequent flexing and thermal stress without circuit failure. The continuous drive towards smaller form factors and higher operational frequency in consumer electronics ensures sustained, high-value demand from this segment. Furthermore, specialized manufacturers of Radio Frequency (RF) and Microwave components also constitute a critical customer segment, utilizing RA foil for high-frequency signal integrity due to its smooth surface and uniform structure minimizing insertion loss.

The industrial and specialized sectors, encompassing medical device manufacturers (e.g., implantable devices, diagnostic equipment) and aerospace/defense contractors, represent high-margin, albeit lower-volume, potential customers. These buyers demand the highest possible reliability, often specifying custom foil thicknesses and requiring exhaustive documentation and certification (e.g., AS9100, ISO 13485 compliance). For these critical applications, failure rates must be near zero, making the proven consistency and superior mechanical properties of RA copper foil an indispensable procurement choice. Targeting these sectors requires specialized sales expertise focused on regulatory compliance and long-term performance assurance, solidifying their status as highly valued niche customers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 2.1 Billion |

| Market Forecast in 2033 | USD 3.4 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Mitsui Mining & Smelting Co., Ltd., Furukawa Electric Co., Ltd., JX Nippon Mining & Metals Corporation, Lingbao Wason Copper Foil Co., Ltd., Nuode New Materials Co., Ltd., UACJ Foil Corporation, Lotte Aluminium Co., Ltd., Solvay S.A., Rogers Corporation, Targray Technology International Inc., Chang Chun Group, KCC Corporation, SK Nexilis Co., Ltd., Taiwan Union Technology Corporation, Iljin Materials Co., Ltd., Greatech Technology Berhad, Nippon Denkai, LLC, Shanghai Jima Electromechanical Co., Ltd., Kingboard Chemical Holdings Ltd., Retac Electro-Materials Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Rolled Annealed Copper Foil market is defined by continuous innovation focused on achieving thinner gauges, superior mechanical resilience, and highly customized surface treatments crucial for optimizing downstream integration. The core technology centers around precision cold rolling, often utilizing multi-roll cluster mills (e.g., 20-high mills) to achieve micron-level thickness uniformity and exceptionally smooth surfaces (low Rz values). This precision mechanical processing is immediately followed by controlled atmosphere annealing, the most critical step, which involves precise temperature and time management to induce recrystallization, thereby manipulating the internal grain structure to maximize ductility and fatigue life while minimizing residual stress. Advancements in annealing technology, such as continuous vacuum annealing processes, are paramount for high-volume production of battery-grade and FPCB-grade foil, ensuring consistent crystal orientation across long lengths of material.

Beyond the primary rolling and annealing processes, surface treatment technology represents a vital area of competitive differentiation. Rolled Annealed foil often requires specialized surface roughening (low-profile treatment) or coating with adhesion promoters (e.g., zinc or copper alloys) to enhance its bonding strength with organic polymer substrates used in FPCBs or the active material slurry in lithium-ion batteries. Manufacturers are heavily investing in proprietary surface morphology control techniques to optimize adhesion without compromising the electrical properties or adding excessive resistance. The integration of advanced metrology and sensor technology, including in-line thickness measurement systems and eddy current testing for defect detection, is standard practice, ensuring that the final product adheres to the tightest industrial tolerances, often specified in fractions of a micron.

Emerging technological trends include the development of specialized RA copper alloys engineered for high-temperature or ultra-high-frequency applications, introducing trace elements to improve thermal stability or modify the coefficient of thermal expansion (CTE). Furthermore, there is significant R&D dedicated to sustainable manufacturing processes, specifically addressing lubrication management and energy recovery systems within the rolling mills to reduce the environmental footprint and operational costs. The use of advanced simulation software (Finite Element Analysis) to model stress distribution during rolling and predict the optimal annealing profile is becoming standard, facilitating rapid prototyping of new foil specifications and significantly shortening the time-to-market for products targeted at next-generation flexible and solid-state battery technologies.

RA copper foil is mechanically rolled and annealed, resulting in a dense, uniform crystalline structure (fibrous grain) that provides superior ductility, flexibility, and fatigue resistance, making it ideal for Flexible Printed Circuit Boards (FPCBs) and high-stress battery applications. ED foil is produced electrochemically, often having a vertical grain structure and rougher surface, making it cost-effective but less mechanically resilient.

The Lithium-Ion Battery Anode application segment is the fastest-growing sector, driven by the explosive global demand for Electric Vehicles (EVs) and large-scale Energy Storage Systems (ESS). RA foil is crucial here for its consistent current collection properties and mechanical durability under thermal and electrochemical cycling.

RA copper foil features an exceptionally smooth surface finish and homogeneous structure, which is critical for minimizing signal loss (insertion loss) and ensuring signal integrity at the high frequencies utilized by 5G and advanced communication modules. Its uniform thickness also allows for precise impedance control in complex circuitry.

Key advancements include the mass production capability of ultra-thin foils (below 6 µm) necessary for advanced IC packaging and high-energy-density batteries, along with innovations in proprietary surface treatments designed to optimize adhesion and chemical resistance without compromising electrical conductivity.

The Asia Pacific (APAC) region, spearheaded by China, South Korea, and Japan, dominates the global market. This dominance is due to the concentration of major FPCB manufacturers, consumer electronics producers, and the world's largest lithium-ion battery gigafactories in the area.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.