ID : MRU_ 436569 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

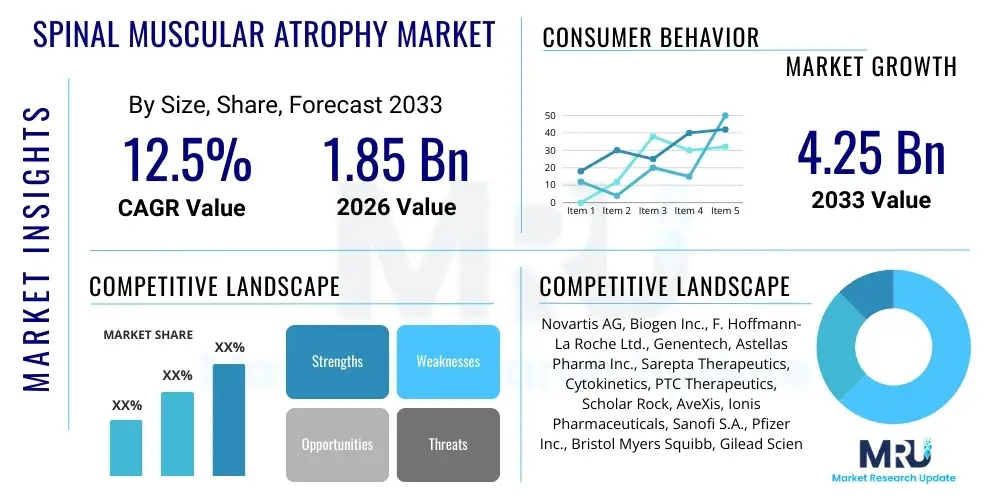

The Spinal Muscular Atrophy Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2026 and 2033. The market is estimated at USD 1.85 Billion in 2026 and is projected to reach USD 4.25 Billion by the end of the forecast period in 2033.

The Spinal Muscular Atrophy (SMA) market encompasses the global landscape of diagnostics and therapeutics aimed at treating this rare, debilitating neuromuscular disorder caused by a deficiency in the Survival Motor Neuron 1 (SMN1) gene. SMA leads to progressive muscle weakness and atrophy, severely impacting mobility, breathing, and swallowing, particularly in infants and young children. The introduction of disease-modifying therapies (DMTs) has fundamentally revolutionized patient prognosis, shifting the market focus from symptomatic management to curative and disease-stopping interventions. These landmark therapeutic advances, particularly gene therapy and antisense oligonucleotide (ASO) treatments, represent high-value opportunities and underscore the pharmaceutical industry's capability to address previously intractable rare diseases.

Major applications within the SMA market revolve primarily around three therapeutic modalities: gene replacement therapy, small molecule drugs that modulate SMN2 splicing, and antisense oligonucleotides. Gene therapy, exemplified by Zolgensma (onasemnogene abeparvovec), offers a one-time treatment delivering a functional copy of the SMN1 gene, mainly targeting pediatric patients, especially Type 1 SMA. ASO therapies, such as Spinraza (nusinersen), require regular intrathecal administration but have demonstrated efficacy across a broader spectrum of SMA types and ages. Small molecule drugs, like Evrysdi (risdiplam), offer an oral, non-invasive administration route, enhancing patient compliance and accessibility, thereby broadening the market reach globally. The ongoing clinical success of these modalities serves as the primary driver for market expansion.

The core benefits derived from the current SMA therapeutics include significant improvements in motor function milestones—such as sitting, standing, and walking—and crucially, enhanced survival rates, particularly for severe Type I patients. Driving factors for market growth include widespread adoption of newborn screening programs in developed economies, enabling early diagnosis and prompt treatment initiation before irreversible motor neuron damage occurs. Furthermore, robust research and development pipelines focusing on next-generation oral drugs, combination therapies, and improved delivery methods continue to attract substantial investment, ensuring sustained innovation and market dynamism over the forecast period.

The global Spinal Muscular Atrophy market is characterized by high therapeutic prices, rapid technological adoption, and a strong presence of monopolistic or oligopolistic competition among key players. Business trends indicate a continued shift towards early intervention, driven by conclusive evidence that pre-symptomatic treatment yields optimal clinical outcomes. This has placed significant pressure on healthcare systems worldwide to integrate effective and rapid diagnostic pathways. Furthermore, pharmaceutical companies are increasingly investing in post-marketing surveillance and real-world data collection to justify the high cost-effectiveness of these transformative therapies, especially in discussions with payers and governmental health agencies regarding reimbursement policies.

Regional trends demonstrate North America's dominance in market share, primarily attributed to high disposable income, sophisticated healthcare infrastructure, aggressive adoption of newborn screening protocols, and premium pricing structures for advanced therapies. Europe follows closely, driven by centralized regulatory approval processes (EMA) and increasing governmental willingness to fund curative treatments, although pricing negotiations remain fragmented across individual member states. Asia Pacific is emerging as the fastest-growing region, fueled by rising awareness, improving healthcare access in countries like China and India, and a large patient pool, which is gradually gaining access to global standards of care through government initiatives and local manufacturing partnerships.

Segment trends highlight the dominance of the treatment segment, specifically gene therapy, due to its one-time administration and profound clinical impact, commanding the highest revenue share. However, the small molecule segment is poised for rapid growth, benefiting from its non-invasive oral route, which improves convenience and ease of access outside specialized centers. SMA Type I remains the largest disease type segment due to its severity and the immediate need for high-cost intervention. The overall market trajectory is leaning towards personalized medicine approaches, where treatment selection is increasingly guided by age, SMN2 copy number, and disease severity, optimizing resource allocation and patient care.

User queries regarding AI's influence in the Spinal Muscular Atrophy market frequently center on two main themes: accelerating the discovery of novel therapeutic targets beyond SMN1/SMN2 modulation, and optimizing the precision and delivery of existing high-cost treatments. Users are keenly interested in how machine learning can interpret complex patient data—including genetic profiles, electrophysiological measurements, and real-time motor assessments—to predict disease progression more accurately and determine the optimal dose or combination regimen for personalized care. Concerns often revolve around data privacy, regulatory challenges in validating AI-driven diagnostics, and ensuring equitable access to these computationally intensive tools across different healthcare settings globally. The expectation is that AI will streamline clinical trials, identifying ideal patient cohorts and predicting therapeutic response, thereby significantly reducing the enormous financial and time investment associated with rare disease research.

The application of Artificial Intelligence (AI) and machine learning (ML) is fundamentally transforming the R&D pipeline for SMA, moving beyond traditional laboratory screening methods. AI algorithms are being deployed to analyze vast genomics and transcriptomics datasets to identify secondary and tertiary genetic modifiers that contribute to SMA severity, offering new targets for drug development that could complement existing SMN-restoring therapies. Furthermore, AI excels in identifying and validating biomarkers—such as neurofilament light chain (NfL) levels—that can serve as non-invasive indicators of disease activity and treatment efficacy, thereby enhancing the objectivity and efficiency of clinical assessments. This capability is critical in a market dominated by extremely high-cost treatments, where objective evidence of response is paramount for continued reimbursement.

In clinical practice, AI-powered tools are improving diagnostic speed and accuracy, particularly in interpreting complex genetic sequencing data obtained from newborn screening. Moreover, computer vision and motion analysis techniques, often powered by deep learning, are being utilized to quantify subtle changes in motor function in SMA patients during clinical visits or even remotely via telemedicine platforms. This high-resolution, objective measurement of functional endpoints provides more sensitive data than traditional physical assessments, which is crucial for managing treatment adjustments and demonstrating long-term functional stability, ensuring patients receive the most personalized and effective therapeutic pathway possible.

The Spinal Muscular Atrophy market is shaped by a powerful interplay of compelling growth drivers, significant economic restraints, and substantial opportunities for expansion, collectively managed by intense competitive and regulatory impact forces. The core driver is the remarkable clinical efficacy demonstrated by approved disease-modifying therapies, which have fundamentally altered the natural history of SMA, transforming a previously fatal disease into a manageable chronic condition. This clinical success, coupled with the high incidence rate of SMA (approximately 1 in 10,000 live births), ensures sustained demand. However, the primary restraint is the exorbitant cost of these cutting-edge therapies, particularly gene therapy, which creates substantial budgetary pressures on healthcare systems globally and raises significant ethical and access challenges. Opportunities exist in expanding treatment into emerging markets and developing lower-cost, orally available treatments that offer greater accessibility, while the impact forces include stringent regulatory pathways for novel biologicals and the necessity for global harmonization of newborn screening policies.

Key drivers include the global adoption of mandatory newborn screening for SMA, enabling pre-symptomatic treatment which dramatically improves outcomes and fuels market revenue. Substantial R&D investment, supported by venture capital and pharmaceutical giants, continues to push the boundaries of genetic and neurological medicine, fostering the development of next-generation therapies, including combination treatments targeting multiple pathways. Furthermore, strong patient advocacy groups play a vital role in lobbying for timely regulatory approvals, favorable reimbursement policies, and increased public awareness, directly accelerating market penetration and demand for available treatments. The shift towards non-invasive, oral administration options, such as risdiplam, also acts as a driver by simplifying long-term treatment management outside of specialized hospital settings.

Restraints are heavily dominated by the economic burden associated with the high acquisition cost of current therapies, which necessitates complex value-based pricing negotiations and limits accessibility in low- and middle-income countries. Additionally, the limited number of specialized treatment centers capable of administering gene therapy or intrathecal injections (for ASO) restricts geographical reach. Regulatory hurdles remain complex, especially regarding long-term safety data for novel gene therapies, which require decades of follow-up studies. Opportunities are focused on the development of biosimilars (though challenging in gene therapy), expanding indication labels for existing drugs to cover older patients or milder SMA types, and exploring combination treatments that target both the central nervous system and peripheral tissues for synergistic effects. The dominant impact forces include intense intellectual property disputes between leading drug manufacturers and the necessity for establishing global real-world evidence registries to track long-term safety and efficacy outcomes.

The Spinal Muscular Atrophy (SMA) market is segmented based on disease type, treatment type, and distribution channel, providing a granular view of revenue generation and market dynamics. Understanding these segments is crucial for strategic planning, as different treatment modalities cater to specific patient populations defined by age and severity. The disease type segmentation reflects the clinical classification of SMA (Types 0 to IV), where Type I, being the most severe and most frequently diagnosed early, currently drives the highest immediate need for intervention and commands the largest revenue share. The treatment type segmentation reveals the technological shift from supportive care to high-impact disease modification, with gene therapies and antisense oligonucleotides dominating the current landscape.

Segmentation by Treatment Type is perhaps the most critical determinant of market value, featuring three dominant classes: Gene Therapy, Antisense Oligonucleotides (ASO), and Small Molecules. Gene therapy is highly valuable due to its curative intent and single-dose model, positioning it as the leading segment in terms of per-patient revenue. ASOs provide continuous treatment for a wider age range, offering a steady, recurring revenue stream. Small molecules, being oral and less invasive, are increasingly preferred for maintenance therapy and by patients or families who prioritize ease of administration, rapidly expanding their revenue footprint, particularly in regions lacking advanced infrastructure for injection-based treatments.

Segmentation by Distribution Channel reflects the specialized nature of SMA treatments. Due to high cost, complex administration, and strict temperature requirements, most SMA drugs are distributed exclusively through specialty pharmacies or hospital pharmacies that are equipped to handle these ultra-orphan drugs. Direct distribution models are often employed by manufacturers to maintain strict control over the supply chain and ensure adherence to safety protocols. This specialized distribution structure emphasizes the market's high barrier to entry and the necessity for established, secure cold-chain logistics for biological products.

The value chain for the Spinal Muscular Atrophy market is highly centralized and characterized by intense R&D investment and highly specialized manufacturing processes, distinguishing it significantly from generic drug markets. The upstream segment is dominated by intense intellectual property development, focusing on gene editing techniques, viral vector design (specifically AAV), and sophisticated oligonucleotide chemistry. Biotech and pharmaceutical companies invest heavily in preclinical research, clinical trials, and regulatory engagement, forming the foundation of the market's value. Specialized contract research organizations (CROs) play a crucial role in managing the complex clinical trial phases required for rare diseases, which often involve multinational collaboration to recruit sufficient patient numbers.

The midstream section involves the highly regulated and complex manufacturing of biological agents. For gene therapies, this requires specialized Good Manufacturing Practice (GMP) facilities capable of producing high-titer, high-purity viral vectors. For ASOs, specialized chemical synthesis and purification are mandatory. Due to the high value and limited shelf life of these products, supply chain management is extremely critical, requiring robust cold-chain logistics and secure transportation protocols. Pricing and reimbursement negotiations occur at this stage, setting the economic terms for market access in different geographies, which is particularly challenging given the ultra-high costs associated with transformative treatments.

The downstream segment focuses on distribution and patient care. Distribution channels are predominantly indirect, relying on specialty pharmacies and high-level hospital clinics that can handle the storage and administration protocols. Gene therapy requires highly specialized hospital centers for infusion, while ASOs necessitate intrathecal administration by skilled neurologists or anesthetists. Direct channels, though less common, are sometimes employed by manufacturers for direct supply management to specific treatment centers. End-users—patients and their caregivers—rely heavily on ongoing specialized medical monitoring, physical therapy, and multidisciplinary care teams, cementing the importance of specialized tertiary care centers in the final delivery of therapeutic value.

Potential customers for Spinal Muscular Atrophy treatments primarily consist of patients diagnosed with SMA, ranging from pre-symptomatic infants identified via newborn screening to adults with milder forms (Type IV). The primary buyers and decision-makers, however, are large institutional entities and government bodies responsible for funding healthcare. These include national healthcare systems (e.g., NHS in the UK, provincial health plans in Canada), governmental regulatory and funding agencies (e.g., NICE, FDA, EMA), and major private insurance companies in highly commercialized markets like the United States. Due to the high cost of therapy, individual patient purchasing power is largely irrelevant; institutional reimbursement policies are the central determinant of market access and sales volume.

Within the clinical setting, the immediate institutional buyers are tertiary care hospitals, specialized pediatric neurology centers, and neuromuscular disease clinics equipped to handle the complex administration and monitoring of these advanced therapies. These centers are responsible for stocking, administering, and managing the entire patient pathway, often requiring significant investment in specialized staff and infrastructure. The influence of medical professionals—pediatricians, neurologists, genetic counselors, and patient advocacy groups—is substantial, as they drive diagnosis, recommend specific treatments based on patient profile (age, SMN2 copies), and lobby payers for coverage.

A growing segment of potential customers includes emerging markets and developing economies, where access to these therapies is currently limited but rapidly increasing due to improving economic conditions and philanthropic initiatives. As pricing models evolve (e.g., outcome-based agreements or tiered pricing), a broader global customer base becomes addressable. Ultimately, pharmaceutical companies view payers as their most critical customers, as securing favorable formulary placement and robust reimbursement coverage dictates the financial success of any SMA therapeutic.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 4.25 Billion |

| Growth Rate | CAGR 12.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Novartis AG, Biogen Inc., F. Hoffmann-La Roche Ltd., Genentech, Astellas Pharma Inc., Sarepta Therapeutics, Cytokinetics, PTC Therapeutics, Scholar Rock, AveXis, Ionis Pharmaceuticals, Sanofi S.A., Pfizer Inc., Bristol Myers Squibb, Gilead Sciences, Regeneron Pharmaceuticals, Takeda Pharmaceutical Company Limited, Eli Lilly and Company, Novo Nordisk A/S, Merck KGaA |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Spinal Muscular Atrophy market relies on a highly sophisticated and innovative technology landscape primarily centered around genetic medicine and oligonucleotide chemistry. The most revolutionary technology is Adeno-Associated Virus (AAV) vector-based gene therapy. This technology involves using a modified, non-pathogenic virus (AAV9 serotype, capable of crossing the blood-brain barrier) to deliver a functional copy of the SMN1 gene directly to motor neurons. The success and high commercial valuation of treatments like Zolgensma are intrinsically linked to advancements in optimizing AAV vector production, purification, and targeted delivery, ensuring high transduction efficiency and long-term therapeutic expression following a single intravenous injection.

Another foundational technology is Antisense Oligonucleotide (ASO) technology, exemplified by Spinraza. ASOs are short, synthetic chains of nucleotides designed to specifically bind to target RNA sequences, modifying gene expression. In the context of SMA, ASOs are engineered to bind to the SMN2 messenger RNA precursor, altering its splicing pattern to produce full-length, functional SMN protein instead of truncated, non-functional protein. This requires meticulous chemical modification of the oligonucleotide backbone to enhance stability, resistance to degradation by nucleases, and facilitate delivery into the central nervous system via intrathecal injection.

The third critical technology involves small molecule drug discovery focused on modulating the SMN2 gene. Unlike ASOs, these orally bioavailable compounds (like risdiplam) can cross the blood-brain barrier and target the splicing machinery systemically. The development of such drugs utilizes advanced high-throughput screening and medicinal chemistry to identify small molecules that effectively increase the inclusion of exon 7 in the SMN2 transcript. Parallel technological advancements in diagnostics, specifically droplet digital PCR (ddPCR) and next-generation sequencing (NGS), are also vital, enabling accurate and rapid identification of SMN1 deletions and SMN2 copy numbers, which are essential for timely intervention and determining treatment eligibility.

The regional analysis of the Spinal Muscular Atrophy market reveals significant disparities in market penetration, driven primarily by economic factors, healthcare infrastructure, and the speed of regulatory adoption of high-cost treatments.

The high cost of SMA therapies, particularly gene therapy, is primarily driven by the intensive research and development investment required for ultra-orphan diseases, the complex, highly specialized manufacturing processes (e.g., AAV vector production), and the transformative, potentially curative value proposition offered to patients.

Newborn screening programs have revolutionized the SMA market by enabling pre-symptomatic diagnosis, which allows for immediate therapeutic intervention. Treatment initiated before symptom onset yields dramatically superior clinical outcomes, making early diagnosis a crucial driver of both medical success and market revenue for disease-modifying therapies.

The small molecule segment, represented by oral treatments such as risdiplam, is projected to exhibit robust growth. This growth is attributed to the convenience of oral administration, enhanced patient compliance, and improved accessibility, particularly in regions lacking the infrastructure required for intravenous or intrathecal delivery.

While APAC offers immense potential, the expansion faces challenges related to heterogeneous regulatory pathways, varying levels of healthcare spending among countries, limited penetration of comprehensive newborn screening outside of developed nations like Japan, and the necessity for building specialized infrastructure for therapy administration.

AI is crucial for accelerating future SMA treatment development by optimizing drug discovery, identifying novel non-SMN therapeutic targets, personalizing dosage regimens based on patient genetic profiles, and enhancing the objective measurement of clinical endpoints through advanced analysis of motor function data.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.