ID : MRU_ 435576 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

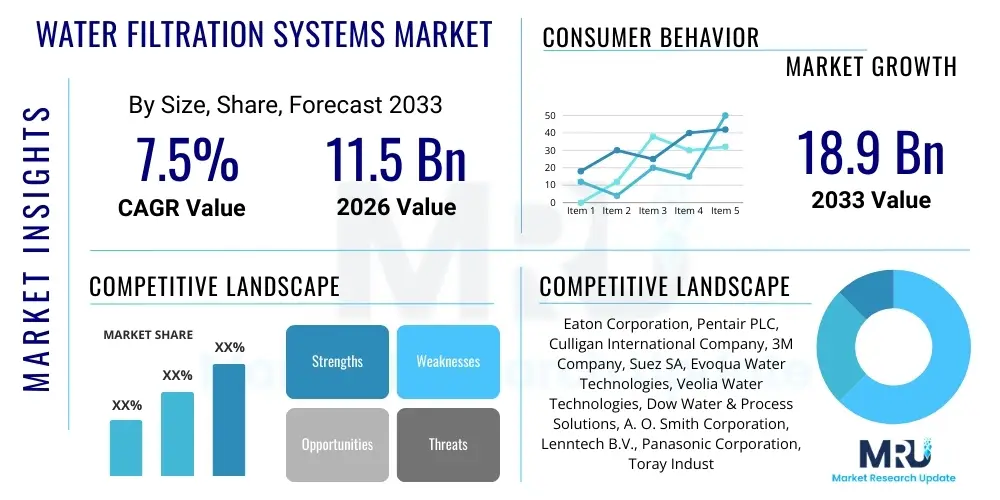

The Water Filtration Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at USD 11.5 Billion in 2026 and is projected to reach USD 18.9 Billion by the end of the forecast period in 2033.

The Water Filtration Systems Market encompasses technologies and devices designed to remove contaminants, impurities, and undesirable particles from water sources, ensuring safety and improving taste. These systems range from simple activated carbon filters used in residential pitchers to complex industrial membrane filtration units utilized in manufacturing and municipal treatment plants. The fundamental necessity for clean water, coupled with increasing public awareness regarding waterborne diseases and chemical pollutants like PFAS, heavy metals, and microplastics, serves as the primary impetus for market expansion globally. Product diversity spans Point-of-Use (POU) systems, installed at a specific water outlet (e.g., faucets, sinks), and Point-of-Entry (POE) systems, which treat all incoming water to a residence or facility. The technological landscape is evolving rapidly, incorporating advancements such as nanotechnology, electro-deionization, and smart monitoring capabilities to enhance efficiency and effectiveness.

Major applications of water filtration systems are broadly categorized across residential, commercial, and industrial sectors. Residential adoption is driven by aesthetic concerns (taste, odor) and health protection, favoring technologies like Reverse Osmosis (RO) and Ultrafiltration (UF). Commercial applications, including restaurants, hospitals, and educational institutions, demand high-volume, reliable filtration to meet specific operational standards, such as sterile water for medical use or quality water for beverage production. Industrially, water treatment is mission-critical for process integrity in sectors such as pharmaceuticals, semiconductors, power generation, and food and beverage manufacturing, where strict purity standards are essential to prevent equipment scaling, product contamination, and regulatory non-compliance. This wide applicability ensures sustained demand across diverse economic activities.

The key driving factors propelling the market include deteriorating global water quality due to pollution and aging infrastructure, stricter governmental regulations concerning municipal and industrial discharge standards, and technological innovation making filtration systems more affordable and efficient. Furthermore, urbanization and population growth in developing economies, often coupled with inadequate public water infrastructure, significantly boost the demand for reliable household filtration solutions. The perceived benefits, including reduced consumption of single-use plastic bottled water and enhanced protection against emerging contaminants, solidify the market's robust growth trajectory, positioning water filtration as a crucial investment in public health and environmental stewardship.

The global Water Filtration Systems Market is poised for significant growth, underpinned by escalating concerns over water safety and the necessity for robust infrastructure modernization. Key business trends indicate a strong shift towards digitalization and integration of Internet of Things (IoT) capabilities, enabling real-time monitoring of filter performance and automated maintenance scheduling, thereby enhancing user convenience and system efficacy. Furthermore, there is a pronounced commercial interest in sustainable filtration media and processes that reduce wastewater generation and minimize energy consumption, addressing both operational costs and environmental mandates. Competitive dynamics are increasingly focused on vertical integration and strategic partnerships, allowing manufacturers to control the supply chain from raw materials (e.g., membrane polymers) to end-user servicing, particularly crucial in the complex industrial filtration sector where customized solutions are paramount.

Regional trends reveal the Asia Pacific (APAC) region as the dominant and fastest-growing market, primarily fueled by rapid industrialization, large-scale infrastructural deficits, and high population density requiring immediate and effective decentralized filtration solutions. North America and Europe, characterized by established markets and high regulatory standards, are primarily focused on replacement demand, technological upgrades (e.g., systems capable of removing pharmaceutical residues and microplastics), and the premium residential segment driven by consumer health awareness. Emerging markets in Latin America and the Middle East & Africa (MEA) are seeing substantial investment in municipal and commercial water reuse projects, although residential adoption is still nascent, often constrained by initial investment costs and limited consumer education regarding long-term cost benefits compared to bottled water alternatives.

Segmentation trends highlight the increasing importance of Point-of-Use (POU) systems in the residential category, particularly under-the-sink and countertop units, favored for their convenience and targeted contaminant removal. Within the technology segment, Reverse Osmosis (RO) remains the gold standard for comprehensive removal, though Ultrafiltration (UF) and nanofiltration are gaining traction due to their lower energy requirements and higher recovery rates, especially in industrial applications requiring selective particle separation. The component segment shows robust demand for replacement filters and cartridges, representing a stable recurring revenue stream for market players, emphasizing the importance of long-term customer retention strategies and subscription-based service models for filter maintenance.

User queries regarding the intersection of Artificial Intelligence (AI) and the Water Filtration Systems Market predominantly center on how AI can enhance operational efficiency, predictive maintenance, and water quality monitoring accuracy. Common user concerns revolve around the cybersecurity risks associated with integrating smart sensors and machine learning algorithms into critical infrastructure, as well as the complexity and cost of retrofitting older, non-smart filtration plants. Users frequently express expectations that AI will enable seamless optimization of filtration processes, such as dynamically adjusting chemical dosages or membrane backwashing cycles based on real-time raw water quality data, ultimately leading to significant reductions in operational expenditure (OPEX) and prolonged equipment lifespan. The key themes summarized from user inquiries emphasize intelligence, efficiency, and resilience in water treatment management.

AI's role transcends simple automation, moving towards highly sophisticated decision-making and optimization within complex filtration environments. Machine learning models are becoming adept at analyzing vast datasets encompassing historical water usage patterns, predictive fouling rates for membranes, and sensor readings related to turbidity, pH, and contaminant levels. This capability allows municipal and large-scale industrial operators to transition from reactive maintenance schedules to highly accurate predictive models, anticipating equipment failure or performance degradation days or weeks in advance. This proactive approach ensures continuous system uptime and guarantees that treated water consistently meets stringent regulatory standards, minimizing public health risks associated with temporary system failures.

The integration of AI also significantly impacts the development cycle of new filtration technologies. Computational fluid dynamics coupled with AI optimization algorithms are accelerating the design of more efficient filter materials and housing structures, maximizing surface area exposure and minimizing pressure drop. Furthermore, AI-powered systems are crucial for managing decentralized water treatment networks, especially in developing regions or remote areas. These smart systems can self-diagnose minor faults and remotely alert technicians to major issues, providing diagnostic guidance, thereby democratizing access to professional-grade water management tools and enhancing overall infrastructure resilience against environmental variability and sudden pollution events.

The Water Filtration Systems Market is fundamentally shaped by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO), which collectively constitute the primary impact forces. A primary driver is the accelerating deterioration of global water resources due to industrial discharge, agricultural runoff, and climate change effects, necessitating higher quality and more diverse filtration solutions to manage emerging contaminants like microplastics, heavy metals, and persistent organic pollutants (POPs). Concurrent with environmental pressure, regulatory bodies worldwide are consistently tightening drinking water standards, forcing both municipal utilities and private consumers to upgrade or adopt advanced filtration technologies. These forces generate substantial, non-discretionary market demand.

However, the market faces significant restraints, notably the high initial capital investment required for installing advanced Point-of-Entry (POE) or industrial filtration systems, particularly in developing economies where budgetary constraints are severe. Furthermore, consumer lack of awareness regarding proper filter maintenance and the necessity of timely replacement often leads to system underperformance or abandonment, undermining product effectiveness and potentially damaging brand trust. Operational challenges, such as the energy intensity of technologies like Reverse Osmosis and the complex waste disposal requirements for used filtration media, also present hurdles that require continuous innovation to overcome, particularly in regions facing energy scarcity or strict waste management laws.

Opportunities for exponential growth are concentrated in two key areas: technological miniaturization and digital integration. The development of compact, highly efficient filtration units leveraging nanotechnology (e.g., carbon nanotubes, graphene oxide membranes) is opening new avenues for decentralized, off-grid water purification, particularly relevant in rural or disaster-stricken areas. Moreover, the burgeoning trend of smart water management, driven by IoT and AI, offers lucrative opportunities for market players who can provide holistic service models, including remote monitoring, predictive maintenance, and data-driven optimization, transforming the market from a simple product sale to a continuous service delivery model, ultimately driving market penetration and stability.

The Water Filtration Systems Market is intricately segmented based on technology, product type, application, and end-user, providing a granular view of specific market dynamics and growth areas. Understanding these segments is crucial for strategic planning, as different technologies address varying contaminant challenges and specific end-user needs. For example, membrane separation technologies, while costly, are essential for achieving ultra-pure water in the semiconductor industry, whereas activated carbon filters dominate the residential POU market due to their effectiveness in removing chlorine and improving taste at a lower cost. The residential segment remains the largest volume driver, but the industrial segment offers higher value due to the complexity and customization required for high-flow, high-purity systems.

Segmentation by product type typically distinguishes between Point-of-Use (POU) and Point-of-Entry (POE) systems. POU systems, which include faucet-mounted, countertop, and under-the-sink units, are driven by consumer convenience and targeted health protection against local contaminants. POE systems, or whole-house filters, address broad issues like sediment and hardness, protecting plumbing and appliances throughout a facility. Furthermore, the segmentation by technology details the prevalence of conventional methods (activated carbon, sediment filters) versus advanced separation techniques (RO, UF, NF, MF, UV sterilization), reflecting investment trends towards higher efficacy and specialized purification required by emerging contaminants.

The application segmentation reveals critical market demand sectors, including municipal water treatment, which focuses on large-scale infrastructure projects; industrial process water, demanding specific quality standards across pharmaceuticals, power, and F&B; and the crucial residential segment. Geographical segmentation remains pivotal, as regulatory environments, contaminant profiles (e.g., arsenic in Asia vs. lead in older North American cities), and disposable income levels dictate the most viable technologies and pricing strategies within each region, highlighting the need for localized product offerings and distribution channels tailored to specific environmental and economic conditions.

The Value Chain for the Water Filtration Systems Market begins with raw material sourcing and upstream activities, primarily involving the procurement and refinement of polymers for membrane production (e.g., cellulose acetate, polyamide), specialized carbon materials for activated filters, and stainless steel or high-grade plastics for housing components. Upstream efficiency is critical; fluctuations in petroleum prices directly impact polymer costs, while the availability of high-quality carbon source materials (like coconut shells or specialized coal) influences filter media efficacy and pricing. Manufacturers often integrate backwards to secure reliable and cost-effective material supply, particularly for proprietary membrane formulations that provide a competitive edge in performance and longevity.

The core midstream activities involve manufacturing, assembly, and quality control. This stage differentiates players based on their technological prowess, particularly in membrane fabrication (e.g., hollow fiber spinning, flat sheet manufacturing) and system integration, which includes incorporating electronics for smart monitoring and pump systems. Large manufacturers benefit from economies of scale, enabling them to produce complex RO and UF units cost-effectively. Quality assurance, encompassing certifications from bodies like NSF International, is non-negotiable, acting as a crucial gatekeeper for market access and consumer trust, especially in the sensitive residential and healthcare application segments.

Downstream analysis focuses on distribution channels, which are bifurcated into direct and indirect methods. Direct distribution is common for large industrial and municipal contracts, involving specialized engineering sales teams and technical support. Indirect channels, essential for the high-volume residential market, rely heavily on e-commerce platforms, specialized plumbing suppliers, large retail chains (e.g., home improvement stores), and local installers. Effective channel management, coupled with robust after-sales service for filter replacements and maintenance contracts, is paramount for securing long-term revenue streams and ensuring customer satisfaction. The proliferation of online channels has also necessitated greater investment in digital marketing and consumer education regarding product selection and maintenance.

The primary spectrum of potential customers for Water Filtration Systems spans three core demographic and institutional categories: residential consumers focused on household purity and health, commercial entities requiring process-specific water quality for operations, and major industrial operators demanding ultra-pure water for manufacturing integrity. Residential customers, particularly those residing in areas with documented water quality issues (e.g., hard water, aging infrastructure leading to lead contamination) or who have higher discretionary income, are prime buyers of POU systems, driven by concerns over taste, odor, and protection against emerging contaminants like pharmaceuticals and microplastics. This segment favors user-friendly, certified systems requiring minimal maintenance.

Commercial end-users constitute a rapidly growing customer base, including hospitality (hotels, restaurants), healthcare facilities (hospitals, clinics), and institutional buildings (schools, universities). Restaurants and beverage makers require specific filtration levels to ensure consistent product quality, while hospitals mandate stringent sterilization and purification for laboratories, dialysis units, and surgical processes. These customers prioritize reliability, compliance with health codes, and cost-efficiency in terms of water usage and energy consumption. They typically purchase medium-sized, centralized filtration systems and often engage in long-term service contracts for maintenance and filter management.

Industrial customers represent the highest-value segment, encompassing sophisticated operations in sectors such as semiconductor fabrication, power generation (boiler feed water), food and beverage processing, and chemical manufacturing. These industries require extremely high purity levels, often measured in parts per trillion (ppt), to prevent product defects, corrosion, or scaling of expensive equipment. These buyers demand highly customized, large-scale systems utilizing combinations of advanced technologies (e.g., RO, electrodeionization, UV) and prioritize technical consulting, comprehensive system integration, and dedicated maintenance support from vendors capable of managing complex regulatory and operational environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 11.5 Billion |

| Market Forecast in 2033 | USD 18.9 Billion |

| Growth Rate | CAGR 7.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Eaton Corporation, Pentair PLC, Culligan International Company, 3M Company, Suez SA, Evoqua Water Technologies, Veolia Water Technologies, Dow Water & Process Solutions, A. O. Smith Corporation, Lenntech B.V., Panasonic Corporation, Toray Industries Inc., Kurita Water Industries Ltd., Kinetico Incorporated, Watts Water Technologies, LG Chem, DuPont, Aquaphor, BWT AG, Resintech. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Water Filtration Systems Market is characterized by continuous innovation aimed at increasing efficiency, reducing energy consumption, and expanding the spectrum of manageable contaminants. Membrane filtration techniques—including Reverse Osmosis (RO), Ultrafiltration (UF), Nanofiltration (NF), and Microfiltration (MF)—form the backbone of modern high-purity systems. RO remains dominant for comprehensive deionization and removal of dissolved solids, utilized extensively in both high-end residential and industrial processes like desalination. However, the market is actively exploring lower-pressure alternatives like NF and UF, which offer superior energy profiles and higher water recovery rates, making them particularly attractive for water reuse applications and pretreatments, demonstrating a clear shift toward sustainability without compromising effective particle exclusion.

Beyond traditional membrane systems, the incorporation of advanced media and disinfection methods is crucial for addressing emerging water quality challenges. Activated Carbon technology is being refined with new material sources (e.g., coconut shells, specialized wood) and binding processes to enhance adsorption capacity for specialized organic contaminants such as PFAS (Per- and polyfluoroalkyl substances) and certain volatile organic compounds (VOCs). Simultaneously, UV disinfection systems, often integrated downstream of particle filters, are witnessing robust growth due to their chemical-free efficacy against bacteria, viruses, and protozoa, offering a safe and environmentally sound method for microbial inactivation, particularly in POU systems and municipal tertiary treatment.

The integration of digital and smart technologies is perhaps the most transformative trend in the current technological landscape. Smart filtration systems now leverage IoT sensors for real-time monitoring of filter lifespan, water quality parameters, and system pressure. This data, often processed by AI and machine learning algorithms, allows for predictive maintenance, remote diagnostics, and automated process adjustments, dramatically reducing operational expenditure and ensuring optimal performance. Furthermore, the development of self-cleaning membranes and electro-deionization techniques minimizes chemical use and waste production, pushing the industry closer to truly closed-loop, sustainable water management solutions, which represents the cutting edge of filtration engineering.

North America: Market Maturity and Regulatory Compliance

North America holds a substantial share of the global market, characterized by high consumer awareness, robust regulatory frameworks enforced by the EPA, and significant investment in smart water infrastructure. The demand in this region is largely driven by replacement cycles for existing municipal and industrial infrastructure, coupled with high consumer adoption of residential POU systems due to specific regional contamination events (e.g., Flint, MI water crisis) and pervasive concerns over lead, chlorine byproducts (THMs), and emerging contaminants like PFAS. The region is a leader in implementing IoT-enabled filtration, allowing consumers and businesses to monitor water consumption and purity via mobile applications, fostering a premium market segment focused on high-performance, aesthetically pleasing appliances. Furthermore, the industrial sector, particularly in pharmaceuticals and electronics manufacturing, dictates extremely high-purity standards, ensuring continuous investment in state-of-the-art membrane technologies and advanced media filtration.

The stringent regulatory environment, particularly concerning industrial effluent discharge and municipal drinking water quality, mandates continuous upgrades to filtration and treatment protocols. This has led to widespread adoption of certified products (NSF, WQA standards) and a favorable environment for technological innovation focused on complex contaminant removal, such as endocrine-disrupting chemicals. The market structure is dominated by major multinational corporations providing integrated solutions, often utilizing extensive dealer networks and established retail partnerships to reach the sophisticated consumer base. The strong emphasis on water reuse and recycling in water-stressed states further fuels demand for advanced membrane bioreactors (MBRs) and ultrafiltration systems within both commercial and industrial settings, cementing the region's position as a technological benchmark.

Europe: Diverse Regulations and Sustainability Focus

The European market presents a diverse landscape, influenced by the European Union’s Drinking Water Directive and varying levels of infrastructure quality across member states. Western European countries, like Germany and the UK, exhibit high saturation in industrial and municipal treatment, driving growth through maintenance, system refurbishment, and adoption of energy-efficient technologies. Central and Eastern European countries, conversely, show higher growth potential due to ongoing infrastructure modernization efforts and increasing adoption of residential filtration spurred by rising awareness of water hardness issues and perceived risks from municipal supply inadequacies. Sustainability is a paramount consideration, leading to high adoption rates for systems that minimize water waste (high-recovery RO) and avoid chemical use (UV, ozone treatment).

The region is a key hub for innovation in membrane technology, particularly in developing forward osmosis and membrane bioreactor technologies for circular economy applications and industrial water reuse. Consumer preferences often favor point-of-use systems like activated carbon filters and softeners, driven more by aesthetic improvements (taste, reduction of scale/hardness) than widespread concerns over microbial contamination, which is generally well-managed by municipal utilities. The competitive landscape is fragmented, featuring strong local specialized firms alongside major global players. Regulatory pressures around microplastic contamination and stricter controls on residual pesticides are expected to catalyze further technological advancements in the nanofiltration segment throughout the forecast period, especially in food and beverage production processes.

Asia Pacific (APAC): Rapid Growth and Infrastructure Needs

APAC is the fastest-growing region in the Water Filtration Systems Market, propelled by rapid urbanization, explosive population growth, and vast differences in water access and quality. In densely populated areas, deteriorating infrastructure combined with high levels of industrial and agricultural pollution severely strains existing treatment capabilities, leading to high dependence on domestic filtration systems. Countries like China and India represent massive opportunities for both residential POU/POE systems and large-scale industrial water treatment infrastructure projects. Government initiatives, such such as India's Jal Jeevan Mission and China's ambitious national water quality programs, are injecting substantial capital into the municipal and rural water treatment sectors, directly driving the adoption of centralized filtration solutions.

The regional market is dominated by affordability and efficacy. RO technology is highly popular in countries where Total Dissolved Solids (TDS) levels are high, even though UF and MF systems are also prevalent due to their lower maintenance costs and energy requirements in specific rural settings. The industrial demand is immense, particularly from the booming manufacturing sectors (textiles, electronics, pharmaceuticals) in Southeast Asia and China, where environmental regulations are tightening, forcing industries to invest in zero-liquid discharge (ZLD) systems and advanced wastewater recycling technologies. Competitive success in APAC hinges on establishing localized distribution networks and offering a diverse product portfolio that caters to extreme price sensitivities across different income brackets, from basic pitcher filters to high-end whole-house solutions.

Latin America (LATAM): Urbanization and Consumer Trust Deficits

The Latin American market is characterized by significant disparities in water management capabilities, where rapidly growing urban centers often outpace the ability of municipal systems to deliver consistent, high-quality water. Consumer trust in public water supply is relatively low in many major cities, leading to high consumption of bottled water and accelerating the adoption of residential POU filtration systems as a reliable alternative. Market penetration is steadily increasing, particularly in high-growth economies like Brazil and Mexico, driven by enhanced consumer education regarding health benefits and the long-term cost savings compared to purchasing bottled water. The market is primarily served by imported technologies, although local assembly and manufacturing capabilities are slowly increasing.

Industrial demand is concentrated in resource-intensive sectors such as mining, oil and gas, and food processing, particularly requiring effective water treatment for process optimization and environmental compliance related to resource extraction activities. Water scarcity issues in certain areas also prompt investment in water reuse and recycling technologies utilizing advanced membrane filtration to secure operational stability. The challenge in LATAM remains the high cost of imported components and the complexity of establishing robust after-sales service and filter replacement networks in remote areas. However, as disposable incomes rise and access to consumer financing improves, the market is expected to witness robust growth across the residential and smaller commercial sectors.

Middle East and Africa (MEA): Scarcity, Desalination, and Infrastructure Investment

The MEA region presents a unique market dynamic dominated by severe water scarcity and significant investment in alternative water sources. The Middle Eastern component is heavily reliant on large-scale desalination projects, making it a critical market for high-volume, robust filtration and reverse osmosis membrane suppliers. High government expenditure on industrial and municipal water security drives the demand for sophisticated pre-treatment and post-treatment systems necessary to handle highly saline feedwater and brine disposal. Meanwhile, the African continent is experiencing growing demand driven by rapid infrastructure development, population growth, and high necessity for basic, reliable water purification in underserved areas.

In Africa, the market is characterized by a strong need for decentralized solutions, including solar-powered filtration units and simple POU systems, addressing both microbial contamination and accessibility challenges. Commercial demand is steadily increasing from the hospitality, healthcare, and infrastructure construction sectors across both sub-regions. Opportunities exist for technologies that are resilient to challenging raw water quality, require minimal chemical intervention, and offer low operational complexity. The introduction of standardized regulatory frameworks and increased foreign direct investment into water sector modernization are crucial factors poised to accelerate market penetration and the adoption of advanced filtration technologies throughout the diverse nations comprising the MEA region.

Advanced water filtration systems, particularly those utilizing Nanofiltration and specialized activated carbon, are increasingly essential for removing emerging contaminants such as Per- and polyfluoroalkyl substances (PFAS), microplastics, pharmaceuticals, and endocrine-disrupting chemicals (EDCs) that conventional chlorine treatment often fails to neutralize, ensuring enhanced public health protection.

IoT integration significantly enhances efficiency by providing real-time monitoring of filter lifespan, water flow, and contaminant levels. This allows for predictive maintenance, automatic alerts for filter replacement, and remote diagnostics, ensuring the system operates optimally and reducing the risk of consuming contaminated water due to overdue maintenance.

The semiconductor and electronics industry typically relies on a multi-stage purification process, culminating in Reverse Osmosis (RO) followed by Electrodeionization (EDI) and sometimes Ultrafiltration (UF) at the point of use. This combination is necessary to remove dissolved ions, trace organics, and particulate matter to achieve the critical resistivity levels required for high-precision manufacturing processes.

The main driver is the persistent lack of reliable and safe centralized municipal water infrastructure coupled with high consumer awareness regarding waterborne diseases. POU systems offer an affordable, immediate, and effective barrier against localized microbial and chemical contamination, ensuring safe drinking water directly at the tap, often replacing expensive bottled water consumption.

The primary sustainability challenges involve high energy consumption required for pressurization and the substantial wastewater stream (brine) generated during the process. Newer high-recovery RO systems and innovations in energy recovery devices are being developed to mitigate these issues, increasing water efficiency and reducing the environmental impact of brine disposal.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.