ID : MRU_ 432534 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

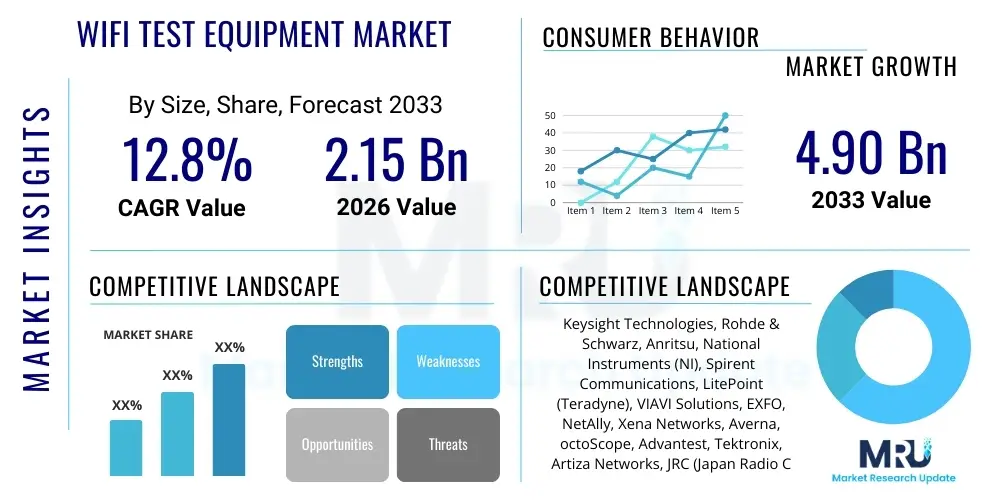

The WIFI Test Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2026 and 2033. The market is estimated at USD 2.15 Billion in 2026 and is projected to reach USD 4.90 Billion by the end of the forecast period in 2033. This growth trajectory is fundamentally driven by the accelerated global adoption of next-generation connectivity standards, notably Wi-Fi 6 (802.11ax) and the emerging Wi-Fi 7 (802.11be), which necessitate more sophisticated and high-frequency testing solutions to ensure performance, reliability, and interoperability across complex network environments. The continuous proliferation of Internet of Things (IoT) devices in residential, commercial, and industrial settings further fuels the demand for robust equipment capable of handling massive device density and heterogeneous traffic profiles.

Market expansion is also supported by mandatory compliance requirements and the intensifying competitive landscape among consumer electronics manufacturers and telecommunication service providers. As users demand higher throughput and lower latency for critical applications such as 4K/8K video streaming, augmented reality (AR), and virtual reality (VR), the need for high-precision validation tools becomes paramount. These tools must accurately simulate real-world interference scenarios, multi-user MIMO (MU-MIMO) configurations, and highly dense operating environments. Furthermore, regulatory bodies frequently update spectrum usage rules, such as the opening of the 6 GHz band, compelling equipment developers to invest heavily in test solutions that cover wider bandwidths and utilize advanced waveform analysis techniques.

The WIFI Test Equipment Market encompasses a broad spectrum of instruments and solutions designed to measure, analyze, validate, and optimize the performance and reliability of wireless networking products and infrastructures utilizing the IEEE 802.11 standard. This equipment is critical across the entire product lifecycle, from initial chip design and hardware development (R&D) to mass production quality assurance (QA) and field deployment maintenance. Products include network analyzers, spectrum analyzers, signal generators, protocol testers, conformance systems, and sophisticated channel emulators. These tools are indispensable for addressing complex challenges related to coverage, throughput, latency, interference, and security in modern Wi-Fi ecosystems, particularly those leveraging the 5 GHz and 6 GHz frequency bands, which are prone to environmental volatility.

Major applications of WIFI test equipment span diverse industries, including telecommunications, where they are used by carriers to validate access points and optimize customer premises equipment (CPE); consumer electronics, for testing smartphones, laptops, and smart home devices; and enterprise networking, for deploying reliable corporate wireless local area networks (WLANs). Benefits derived from utilizing high-quality test equipment include faster time-to-market for new products, reduced post-deployment failure rates, enhanced customer experience through superior connectivity performance, and assured compliance with global regulatory standards like FCC, CE, and Wi-Fi Alliance certification requirements. The equipment ensures that devices function correctly under stress, utilize advanced features like Orthogonal Frequency-Division Multiple Access (OFDMA) efficiently, and maintain low power consumption.

The market is primarily driven by the unrelenting consumer and industrial demand for faster wireless speeds and seamless connectivity, necessitating rapid upgrades to Wi-Fi infrastructure. Key driving factors include the massive rollout of Wi-Fi 6 and Wi-Fi 6E, the approaching commercialization of Wi-Fi 7 (802.11be Extremely High Throughput), and the exponential growth of IoT and machine-to-machine (M2M) communications which place unprecedented density demands on existing networks. Furthermore, the convergence of 5G cellular networks with Wi-Fi offloading strategies requires integrated testing solutions that can evaluate handover performance and unified access network efficiency, pushing test equipment manufacturers to innovate sophisticated, software-defined testing methodologies.

The WIFI Test Equipment market is characterized by robust business trends centered on automation, higher frequency coverage, and integrated solution platforms. Leading market players are pivoting away from discrete hardware instruments toward modular, software-centric testing solutions that offer scalability and flexibility essential for handling the rapid iterations of Wi-Fi standards (6, 6E, 7). There is a significant trend towards offering cloud-based or subscription models for software upgrades and specialized testing libraries, allowing users, particularly R&D labs and service providers, to access the latest capabilities without major capital expenditures on new hardware. Business growth is strongly correlated with capital expenditure cycles in the telecommunications and semiconductor manufacturing sectors, particularly in Asia Pacific, which has become the global hub for consumer electronics production and 5G/Wi-Fi convergence development.

Regionally, Asia Pacific (APAC) currently dominates the market and is projected to maintain the highest growth rate throughout the forecast period. This dominance is attributed to the massive scale of manufacturing operations in countries like China, Taiwan, and South Korea, which require continuous quality assurance testing for high-volume consumer electronic exports. Furthermore, the rapid expansion of smart cities, industrial IoT (IIoT), and digital infrastructure projects across developing APAC economies necessitates extensive deployment and validation of robust Wi-Fi networks. North America and Europe, while mature markets, drive demand for high-end, complex testing solutions primarily within R&D and aerospace/defense sectors, focusing on performance validation for 6 GHz and future 7 GHz bands, as well as adherence to stringent regulatory compliance and advanced cybersecurity testing protocols integrated into the Wi-Fi equipment validation process.

Segment trends reveal that the manufacturing/production segment, encompassing quality control and assembly line testing, holds the largest market share due to the sheer volume of devices being produced globally, demanding fast, reliable, and automated testing setups. However, the Research and Development (R&D) application segment is anticipated to witness the fastest growth, fueled by the complex requirements of developing Wi-Fi 7 chips and equipment that utilize ultra-wide bandwidths (up to 320 MHz) and sophisticated coding schemes. From a product perspective, dedicated Wi-Fi protocol analyzers and comprehensive channel emulators are seeing increased adoption over traditional, general-purpose spectrum analyzers, reflecting the shift toward application-specific, in-depth protocol layer testing required to troubleshoot intricate wireless connectivity issues and ensure optimal multi-link operation (MLO) performance characteristic of next-generation standards.

Common user questions regarding AI's impact on WIFI Test Equipment revolve around automation capabilities, predictive failure analysis, and managing the complexity inherent in Wi-Fi 6/7 networks. Users frequently ask: Can AI reduce test cycles and time-to-market? How effectively can AI diagnose transient and intermittent network faults that manual testing often misses? Will AI-driven solutions replace the need for skilled RF engineers? The consensus among these inquiries highlights an expectation that AI must transition testing from reactive fault detection to proactive, predictive optimization. Users are particularly concerned about the sheer volume of data generated by modern test setups and look to AI for intelligent data aggregation, correlation, and pattern recognition to accelerate decision-making, especially in complex, crowded spectral environments utilizing technologies like OFDMA and beamforming, where manual optimization is highly impractical.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally transforming the operational landscape of the WIFI Test Equipment market, shifting the paradigm from static measurements to dynamic, intelligent diagnostics. AI algorithms are being deployed to automate the creation of optimal test cases, drastically reducing the labor and time associated with complex compliance and performance validation procedures. By learning from millions of data points generated during testing, AI systems can identify subtle, non-linear relationships between configuration settings and network performance, leading to highly optimized device firmware and infrastructure deployment strategies. This capability is vital for managing the complex spatial streams and diverse frequency channels introduced by 6 GHz operations and the high-density requirements of IoT ecosystems, providing insights that traditional rule-based monitoring tools cannot offer.

Furthermore, AI is crucial for enhancing field-deployed testing and network monitoring, moving beyond R&D applications into operational excellence. AI-powered tools can continuously monitor live Wi-Fi networks, automatically categorize traffic patterns, detect anomalies indicative of impending hardware failure or security vulnerabilities, and provide root-cause analysis in real-time. This predictive maintenance capability minimizes network downtime for service providers and large enterprises. AI also significantly aids in spectrum utilization management, intelligently identifying and mitigating sources of intermittent interference by distinguishing between Wi-Fi and non-Wi-Fi signals, thus optimizing channel selection and improving overall network resilience and quality of service (QoS) delivery for latency-sensitive applications.

The WIFI Test Equipment Market is shaped by powerful and interacting forces of growth, constraint, and technological opportunity. The primary driver is the pervasive adoption of new, complex Wi-Fi standards (Wi-Fi 6/6E and Wi-Fi 7) which mandate specialized testing capabilities to validate features like Orthogonal Frequency-Division Multiple Access (OFDMA), Target Wake Time (TWT), and 320 MHz channel widths. These advancements create an immediate and non-negotiable demand for compatible test instruments. A parallel driver is the massive expansion of the IoT landscape, covering smart homes, smart factories (Industry 4.0), and connected vehicles, all requiring reliable, low-latency Wi-Fi connectivity validation at scale, pushing manufacturers towards automated and high-throughput production test solutions. These driving factors amplify the need for precision and speed, creating a significant positive impact force.

However, the market faces inherent restraints, most notably the extremely high capital expenditure required for purchasing high-end, wide-bandwidth test equipment, particularly specialized signal generators and protocol analyzers capable of handling multi-gigabit speeds and the 6 GHz spectrum. This high cost can deter smaller enterprises or newly established R&D facilities. Furthermore, the rapid evolution of Wi-Fi standards poses a significant technological challenge, leading to product obsolescence risk; test equipment purchased today may lack the features required for Wi-Fi 7 validation tomorrow, creating uncertainty for long-term investment planning. These restraints exert a moderating influence on market growth, pushing vendors towards software-defined and modular hardware solutions to mitigate rapid obsolescence risks for end-users.

Opportunities in the market are centered around convergence and emerging applications. The synergy between 5G cellular technology and Wi-Fi 6/7 provides a major opportunity, requiring integrated testing solutions that can validate seamless mobility and traffic offloading between these two domains. The automotive sector, driven by connected car features and autonomous driving requirements, presents a rapidly growing vertical for high-reliability, mission-critical Wi-Fi testing. Moreover, the global push towards unlicensed spectrum utilization, particularly in the 6 GHz band (Wi-Fi 6E/7), creates specialized opportunities for spectrum sharing and co-existence testing equipment. These opportunities indicate future growth areas, where equipment manufacturers can diversify their product portfolios beyond traditional telecom and consumer electronics sectors and utilize the impact forces to foster sustainable long-term expansion through innovation.

The WIFI Test Equipment Market is segmented across several critical dimensions, including component type, connectivity standard, application, and end-user. This layered segmentation is vital for understanding the diverse needs of the market, ranging from pure silicon testing to large-scale network deployment validation. The Component segment typically divides the market into Hardware (Analyzers, Emulators, Meters) and Software (Testing Suites, Automation Tools, Firmware). The shift towards Software-Defined Radio (SDR) and modular hardware is heavily influencing this segment, making software functionality increasingly critical for managing complex waveforms and protocol specifications found in newer standards.

Segmentation by Connectivity Standard is perhaps the most dynamic, driven by the rapid adoption cycle of new IEEE 802.11 iterations. Key categories include equipment compatible with Wi-Fi 4 (802.11n), Wi-Fi 5 (802.11ac), and the high-growth segments of Wi-Fi 6 (802.11ax), Wi-Fi 6E (6 GHz band), and the anticipated Wi-Fi 7 (802.11be). This specific segmentation allows test vendors to target investments where development and manufacturing are most active. Application-wise, the market is broadly segmented into R&D (High-fidelity testing for new product design), Manufacturing/Production (High-throughput, automated QA/QC testing), and Deployment/Maintenance (Field analysis and troubleshooting), with Manufacturing currently holding the largest volume share.

Finally, the End-User segmentation distinguishes between crucial vertical markets. These include Semiconductor Companies (chip testing), Device Manufacturers (CPE, routers, smart devices), Telecommunication Service Providers (network optimization, service validation), and Enterprise/IT Departments (WLAN deployment and management). Each end-user group has distinct requirements; for instance, semiconductor firms demand high-precision physical layer testers, while service providers prioritize robust, portable field analyzers with strong diagnostic software capabilities for rapid service restoration and optimization. Understanding these differences allows market participants to tailor sales and support strategies effectively, focusing on solution integration rather than just component provision.

The value chain of the WIFI Test Equipment Market is complex, beginning with upstream component suppliers and extending through specialized manufacturing and diverse distribution channels to the highly demanding end-users. Upstream analysis focuses on the providers of high-precision electronic components, specialized RF chips, digital signal processing (DSP) hardware, and software operating systems essential for building accurate and reliable test instruments. These suppliers, often specializing in high-frequency, wide-bandwidth components, are crucial as the capabilities of the final test equipment are directly limited by the quality and speed of these fundamental building blocks, especially those required for 6 GHz and 7 GHz operations. Collaboration and assured supply chain integrity in the upstream segment are paramount for maintaining cost competitiveness and manufacturing lead times in a rapidly evolving technological environment.

The midstream segment involves the core activities of the test equipment manufacturers (TEMs) who design, assemble, and integrate the instruments. This stage involves significant investment in R&D to develop proprietary measurement algorithms, user interfaces, and sophisticated calibration techniques necessary to meet evolving Wi-Fi Alliance and IEEE standards. Manufacturers differentiate themselves through software features, automation capabilities (often AI/ML integration), modularity, and overall measurement accuracy. Downstream activities involve distribution channels, which are bifurcated into direct and indirect models. Direct sales are typically favored for high-value, complex R&D systems sold to large semiconductor or defense clients, ensuring specialized technical support and customization.

Indirect distribution, involving regional distributors, value-added resellers (VARs), and system integrators, is utilized more frequently for high-volume, lower-cost production testers and field maintenance tools. These partners often provide localized support, calibration services, and training crucial for widespread adoption. End-users, who are the final consumers in the value chain, exert significant pressure on manufacturers regarding price, performance, and compatibility with the latest standards. Strong customer relationships and responsive after-sales service, including continuous software updates, are vital for securing recurring revenue, particularly in the telecom and enterprise segments where long-term maintenance contracts are common. The efficiency of the distribution channel dictates time-to-market for new equipment and accessibility for regional customers.

The potential customers for WIFI Test Equipment are highly diversified, encompassing every entity involved in the design, manufacture, deployment, or maintenance of Wi-Fi-enabled products and infrastructure. Primary buyers are Semiconductor Companies, which require high-frequency, highly accurate testers for validating physical layer performance of baseband chips and RF front-end modules intended for new Wi-Fi standards (e.g., Wi-Fi 7). Their demand is characterized by the need for complex signal generation and analysis capabilities to ensure chip performance under various stressful, real-world conditions, utilizing extensive channel emulation features to replicate dense urban environments.

Another major buyer segment includes Consumer Electronics Manufacturers, such as producers of smartphones, smart TVs, IoT gateways, and networking equipment (routers, access points). These customers prioritize high-throughput, automated production line testing solutions (QA/QC) that can rapidly verify device functionality, power consumption, and regulatory compliance at scale with minimal human intervention. Their purchasing decisions often hinge on the speed of the tester and the total cost of ownership (TCO) per test station. Furthermore, Telecommunication Service Providers (ISPs and mobile carriers) constitute a critical customer base, relying on rugged, portable field analyzers to troubleshoot customer premises equipment (CPE), optimize network deployments, manage interference, and validate service quality metrics across their large footprint.

Emerging key customer segments include the Automotive Industry, which uses specialized equipment to test vehicle-to-everything (V2X) communication modules and in-vehicle infotainment systems utilizing Wi-Fi; and Aerospace and Defense organizations, which require robust, secure, and often custom-designed testing solutions for mission-critical wireless applications where performance assurance is non-negotiable. Enterprise IT departments and system integrators also form a substantial customer pool, purchasing field testing tools to commission and maintain complex enterprise WLAN deployments in challenging corporate, medical, or educational environments, focusing heavily on coverage mapping, spectrum utilization, and security validation capabilities.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 2.15 Billion |

| Market Forecast in 2033 | USD 4.90 Billion |

| Growth Rate | 12.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Keysight Technologies, Rohde & Schwarz, Anritsu, National Instruments (NI), Spirent Communications, LitePoint (Teradyne), VIAVI Solutions, EXFO, NetAlly, Xena Networks, Averna, octoScope, Advantest, Tektronix, Artiza Networks, JRC (Japan Radio Co.), Good Will Instrument Co., Ltd. (GW Instek), Telewave, Inc., Astronics Corporation, Wireless Test Solutions. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the WIFI Test Equipment Market is currently dominated by the shift to high-frequency and ultra-wideband measurement capabilities, necessary to support Wi-Fi 6E and Wi-Fi 7 standards. A critical technological requirement is the ability to accurately test in the 6 GHz unlicensed band (5.925 GHz to 7.125 GHz), which demands test equipment with superior spectral purity, wider instantaneous bandwidths (up to 320 MHz for Wi-Fi 7), and extremely low noise floors. Over-the-Air (OTA) testing in anechoic chambers is becoming mandatory, especially for devices incorporating advanced Massive MIMO and beamforming technologies, where traditional conducted testing fails to accurately capture real-world performance metrics. Manufacturers are increasingly utilizing Software-Defined Radio (SDR) architectures, allowing a single hardware platform to be reconfigured through software updates to handle future standards and diverse modulation schemes, thus future-proofing customer investments and enhancing equipment versatility.

Another crucial technological advancement is the integration of advanced protocol analysis and channel emulation capabilities. Modern testing cannot merely rely on physical layer measurements; it must validate the efficiency of higher-layer protocols, especially those introduced in Wi-Fi 6 and 7, such as Orthogonal Frequency-Division Multiple Access (OFDMA), Multi-User Multiple-Input Multiple-Output (MU-MIMO), and Multi-Link Operation (MLO). Sophisticated channel emulators are essential for accurately replicating the challenging propagation environments (fading, path loss, Doppler shift) that devices encounter, particularly for applications like industrial automation (IIoT) and connected cars, ensuring reliability under hostile conditions. These emulators must dynamically switch between environments and accurately model inter-channel interference in dense deployments.

Furthermore, the drive toward production efficiency is accelerating the adoption of automated test platforms utilizing Artificial Intelligence (AI) and Machine Learning (ML). The goal is to maximize throughput and minimize test time in manufacturing lines. Key technologies here include parallel testing architectures, where multiple devices under test (DUTs) can be tested simultaneously, and the integration of highly intuitive, script-based automation software. The market is also seeing a push toward highly integrated testers that combine signal generation, analysis, and protocol testing in a single box, simplifying complex test setups and reducing the physical footprint required in R&D labs and production facilities while ensuring compliance with stringent regulatory frameworks and Wi-Fi Alliance certification programs.

The primary factor driving demand is the mandatory transition to and validation of next-generation connectivity standards, specifically Wi-Fi 6E (802.11ax operating in the 6 GHz band) and the upcoming Wi-Fi 7 (802.11be), which necessitate equipment capable of handling ultra-wide bandwidths, advanced modulation techniques (e.g., 4096-QAM), and Multi-Link Operation (MLO) protocols that older testers cannot support efficiently or accurately.

Wi-Fi 7 (802.11be) adoption necessitates significant investment in high-fidelity test equipment that supports up to 320 MHz channel bandwidths and sophisticated spatial multiplexing techniques. This is pushing the industry toward modular, software-defined architectures and complex channel emulators to accurately simulate the extremely high throughput and low latency performance required for future critical applications like metaverses and industrial automation, driving the R&D segment growth.

R&D testing demands flexible, high-precision equipment (signal analyzers, complex emulators) focused on validating fundamental physics and new features for chip and device design. Conversely, Manufacturing testing requires high-throughput, highly automated, and cost-effective solutions (e.g., dedicated wireless testers) focused on rapid Go/No-Go quality assurance and compliance checks for high-volume production lines to ensure fast time-to-market.

The Asia Pacific (APAC) region currently holds the largest market share, predominantly due to its extensive consumer electronics manufacturing base, including global leaders in chip fabrication and device assembly (e.g., China, Taiwan, South Korea). This high-volume production environment creates continuous, large-scale demand for automated production line test equipment and supporting quality control infrastructure, supplementing strong telecommunication investment.

AI integration significantly improves testing by enabling automated test case generation, reducing manual intervention, and accelerating test cycles. Furthermore, AI/ML tools provide predictive diagnostics and intelligent root cause analysis by correlating vast amounts of network performance data, efficiently identifying intermittent failures, optimizing spectrum usage, and proactively managing complex network configurations in real-time deployed environments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.