ID : MRU_ 432329 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

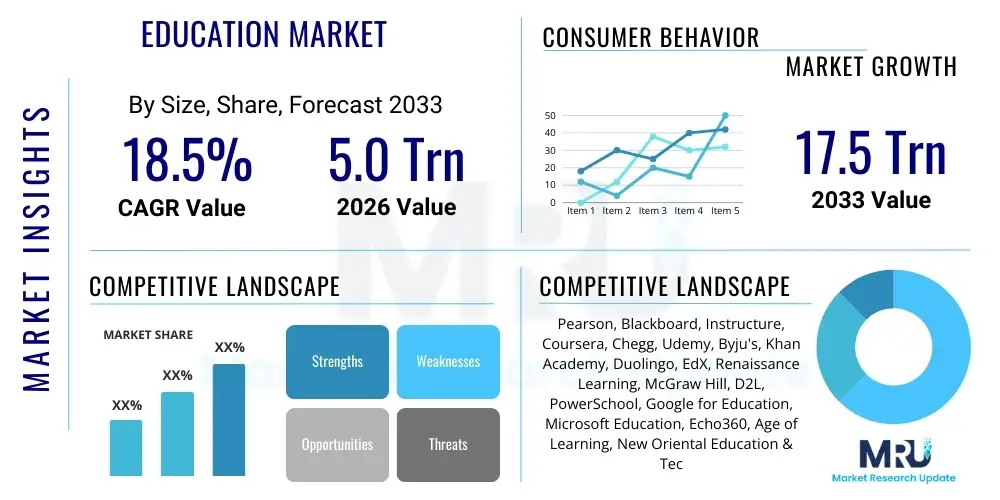

The Education Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at $5.0 Trillion in 2026 and is projected to reach $17.5 Trillion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the rapid global integration of educational technologies (EdTech) and the increasing demand for personalized, flexible learning solutions across K-12, higher education, and corporate training sectors. The digitalization mandate accelerated by recent global shifts has permanently altered educational delivery mechanisms, pushing institutions to adopt cloud-based infrastructure, advanced learning management systems (LMS), and sophisticated digital content libraries to maintain competitiveness and reach broader demographics.

The global Education Market encompasses all services, products, and technologies utilized in the delivery and facilitation of learning and skill development across various age groups and professional stages. This vast ecosystem includes traditional academic institutions (K-12 and higher education), vocational and technical training centers, corporate learning and development (L&D) departments, and the burgeoning sector of EdTech platforms and digital content providers. Key products range from physical textbooks and classroom infrastructure to advanced digital solutions such as Learning Management Systems (LMS), Massive Open Online Courses (MOOCs), simulation tools, and adaptive learning software, forming a complex matrix designed to enhance learning outcomes and access.

Major applications of the market span synchronous and asynchronous learning environments, professional certification, continuous skill upgrade (reskilling and upskilling), and standardized testing preparation. The primary benefits derived from the modernization of the education sector include improved accessibility to high-quality instruction regardless of geographical location, increased flexibility in learning pace and schedule, and the capability to offer highly customized learning paths tailored to individual student needs. This transition addresses the critical need for a globally skilled workforce capable of navigating rapidly evolving technological landscapes, making continuous education a necessity rather than a luxury.

Driving factors for the market’s explosive growth include demographic shifts leading to larger student populations, particularly in emerging economies, coupled with increased government spending on educational infrastructure and digitization initiatives worldwide. Furthermore, the rising awareness among parents and employers regarding the crucial role of specialized skills in modern employment fuels the demand for advanced and supplementary educational services. The technological advancements, particularly in areas like mobile computing, cloud services, and artificial intelligence integration, serve as powerful accelerators, enabling scale and cost-effectiveness in delivering educational content globally, thereby transforming traditional pedagogical models.

The Education Market is currently undergoing a profound structural shift characterized by rapid technological adoption, geopolitical prioritization of digital literacy, and increasing private sector investment in EdTech startups. Business trends are dominated by strategic mergers and acquisitions among established publishing houses and technology firms, aiming to create integrated educational ecosystems that cover content creation, delivery, and assessment. A major commercial focus is placed on subscription-based learning models and SaaS deployment for institutional software, ensuring recurring revenue streams and seamless software updates. The shift towards personalized learning, powered by data analytics and AI, is redefining product offerings, moving away from one-size-fits-all curricula toward highly adaptive, modular content tailored to individual learner progression and performance metrics.

Regionally, Asia Pacific (APAC) stands out as the fastest-growing market, primarily fueled by massive population bases, increasing disposable income dedicated to education, and proactive government policies promoting digital transformation in schooling, especially in countries like India and China. North America and Europe, while mature, remain dominant in innovation, leading the development and adoption of sophisticated AI-driven tutoring and advanced simulated learning environments. Latin America and the Middle East and Africa (MEA) are emerging as critical expansion zones, characterized by significant infrastructural investment gaps that EdTech solutions are poised to fill, focusing initially on mobile-first learning solutions due to high mobile penetration rates.

Segment trends highlight the exceptional growth of the Higher Education segment due to the pervasive adoption of online degree programs and professional certifications required for career advancement. Within components, the Software and Services segment, particularly concerning Learning Management Systems (LMS), Student Information Systems (SIS), and cloud infrastructure services, exhibits the highest growth rate, reflecting the operational necessity for institutions to manage digital curricula and student data efficiently. Furthermore, vocational training and corporate L&D are experiencing robust expansion, driven by the global necessity for workforce reskilling to meet the demands of automation and digital economies, positioning lifelong learning as a core driver of future market dynamics.

Common user questions regarding the impact of AI on the Education Market typically revolve around whether AI tools will replace human teachers, how personalized learning can be truly implemented at scale, and concerns about data privacy and algorithmic bias in assessment systems. Users are keenly interested in the efficacy of generative AI for content creation and whether adaptive tutoring systems genuinely improve long-term educational outcomes versus traditional methods. The analysis confirms key themes centered on efficiency gains through automated administration, enhanced accessibility via AI-driven translation and accessibility features, and the expectation that AI will transition the teacher's role from content delivery to mentorship and socio-emotional development facilitation. The overarching sentiment is one of cautious optimism, acknowledging AI’s potential to democratize and individualize education, provided ethical deployment and data security standards are rigorously maintained.

The market dynamics of the Education sector are governed by a robust interplay of Drivers, Restraints, and Opportunities (DRO), which collectively shape the competitive landscape and strategic direction. The primary driving force is the global imperative for digital transformation, accelerated by the need for continuous workforce development and the expanding reach of high-speed internet infrastructure worldwide, particularly 5G technology. Simultaneously, the inherent inertia and long procurement cycles within large public education systems, coupled with significant concerns regarding the digital skills gap among educators, serve as powerful restraints. Opportunities primarily lie in leveraging emerging technologies like virtual reality (VR) and augmented reality (AR) for immersive learning experiences and penetrating underserved markets through affordable mobile-based solutions, especially in vocational training and lifelong learning contexts.

Impact forces analyze the influence of these DRO factors on market profitability and competitive intensity. The Threat of New Entrants is moderate but rising, as low barriers to entry exist for niche EdTech content providers, although high capital investment is needed for scalable LMS platforms. Buyer Power (students, parents, institutions) is high due to the abundance of competitive digital offerings and the increasing transparency in quality and pricing of educational products, pushing providers toward value-added services and flexible payment models. Supplier Power (technology providers, established publishers) is moderate; while technology firms hold significant intellectual property related to AI and cloud infrastructure, content creators face intense competition and the democratization of content through open educational resources (OER).

The Threat of Substitutes is significant, driven by the proliferation of highly credible, free or low-cost alternatives like YouTube tutorials, OER, and certification programs offered directly by major technology companies (e.g., Google, Microsoft). This forces traditional institutions and EdTech companies to focus on credentials, accreditation, and human-led support services that substitutes often lack. Finally, Competitive Rivalry is extremely high and intensifying, characterized by aggressive pricing, frequent product innovation, and global expansion efforts, particularly between well-funded venture capital-backed EdTech startups and traditional established educational content providers fighting for market share in both B2B institutional sales and B2C direct-to-consumer models.

The Education Market is segmented based on the component, sector, and delivery mode, offering a comprehensive view of market dynamics across diverse educational settings. Segmentation provides clarity on where investment is concentrated and highlights high-growth niches. The Component segment distinguishes between the underlying technological infrastructure (hardware and software) and the necessary human expertise and support (services). The Sector segmentation categorizes the market by the traditional recipient base, ranging from foundational schooling to professional development. Delivery Mode analyzes the structural organization of learning, distinguishing between physical classroom-based teaching, fully digital experiences, and hybrid models, reflecting the evolving preferences of learners globally.

The shift toward digital ecosystems means that the most rapidly expanding segments are typically Software (LMS and specialized applications) and Services (consulting, implementation, and content development). In terms of sectors, corporate L&D is showing remarkable acceleration as companies prioritize agility and continuous employee training. The long-term trend strongly favors hybrid and blended learning approaches, offering institutions the flexibility to scale digital resources while retaining the critical social and physical interaction benefits of traditional learning environments, thereby optimizing resource utilization and maximizing student engagement.

The value chain for the Education Market is complex, encompassing the entire process from foundational knowledge creation to final skill acquisition by the end-user. Upstream activities involve intellectual property creation, raw content generation (authors, subject matter experts), and the development of core software infrastructure (SaaS providers, cloud services). These entities establish the foundational quality and technological capabilities of the final educational offering. Downstream analysis focuses on the final delivery and consumption—this involves academic institutions, corporate L&D departments, and individual consumers accessing platforms, requiring robust technological support for seamless user experience and effective pedagogical execution.

The distribution channel is increasingly diversified. Direct channels involve B2C sales where platforms sell subscriptions directly to individual learners (e.g., MOOCs, tutoring apps). Indirect channels are dominated by B2B sales to institutional clients (schools, universities, corporations) facilitated by system integrators, EdTech distributors, and consulting firms who manage the implementation and integration of complex software ecosystems (LMS, SIS). The efficiency of the distribution channel is critical, as it determines the market reach and scalability of digital products, particularly in emerging markets where localized support and distribution networks are vital.

A key focus in modern education value chain optimization is the integration between content creators and technology platforms. Instead of rigid, static content (like traditional textbooks), modern systems emphasize dynamic, modular content that is instantly updateable and personalized via the delivery platform. This tight vertical integration reduces time-to-market for new curricula and enhances adaptive learning capabilities, creating a highly responsive feedback loop between learning effectiveness and content modification. Efficient data governance and secure cloud hosting are paramount at every stage of the modern educational value chain.

The potential customer base for the Education Market is exceptionally broad, spanning every demographic requiring skill acquisition or certification. The primary end-users fall into three major categories: institutional buyers, corporate buyers, and individual consumers. Institutional buyers (K-12 schools and higher education facilities) are the largest consumers of large-scale infrastructure, integrated management systems (LMS/SIS), and comprehensive digital curriculum licenses. Their purchasing decisions are often centralized, regulated, and focused on accreditation compliance and scalable technology solutions that serve thousands of students simultaneously.

Corporate buyers (businesses ranging from SMEs to Fortune 500 companies) purchase customized training solutions, professional certifications, and platforms designed for continuous employee upskilling and compliance training. These customers prioritize measurable ROI, relevance to specific business objectives, and highly flexible, on-demand content delivery mechanisms, often preferring personalized micro-learning modules integrated into their existing workflow. The expansion of automation necessitates continuous workforce retraining, positioning corporate L&D as a high-value, high-growth segment.

Individual consumers represent the direct-to-consumer (D2C) segment, comprising parents purchasing supplementary tutoring for their children, students seeking test preparation or degree programs, and working professionals pursuing personal development or career transition credentials. This segment is highly sensitive to pricing, reputation, user experience, and the portability/recognition of digital credentials. Marketing efforts in this segment rely heavily on digital channels, personalized recommendations, and clear outcome guarantees to drive adoption of direct online courses and educational apps.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $5.0 Trillion |

| Market Forecast in 2033 | $17.5 Trillion |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Pearson, Blackboard, Instructure, Coursera, Chegg, Udemy, Byju's, Khan Academy, Duolingo, EdX, Renaissance Learning, McGraw Hill, D2L, PowerSchool, Google for Education, Microsoft Education, Echo360, Age of Learning, New Oriental Education & Technology Group, TAL Education Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Education Market is intrinsically linked to rapid advancements in digital infrastructure and software development, fundamentally transforming pedagogical delivery. Key technologies revolve around maximizing accessibility, personalizing content, and enhancing engagement. Central to the current landscape are robust Learning Management Systems (LMS) such as Canvas and Moodle, which serve as the central hubs for content distribution, student interaction, and performance tracking. Alongside LMS, cloud computing platforms (e.g., AWS, Azure) provide the necessary scalability and data storage capabilities to manage large volumes of student data and facilitate global reach for educational providers. Furthermore, the increasing adoption of mobile learning applications ensures that educational access is no longer limited by fixed locations, driving market growth through smartphone penetration.

A second critical layer of the technology landscape involves immersive learning tools and artificial intelligence. Virtual Reality (VR) and Augmented Reality (AR) technologies are moving from niche experiments to mainstream applications, especially in vocational training and science education, offering high-fidelity simulations for practical skill development without physical risk or expensive equipment. This is complemented by the widespread integration of AI and machine learning algorithms, which power sophisticated adaptive testing, automated feedback systems, and predictive analytics that guide both students and educators. The effective integration of these diverse technologies necessitates robust cybersecurity measures and compliance with global data privacy regulations (like GDPR and FERPA) to maintain trust among users and institutions.

Beyond content delivery, efficiency technologies are vital. Blockchain technology is emerging as a secure method for managing digital academic credentials and verifying qualifications, minimizing fraud and simplifying transfer processes between institutions. Furthermore, the rapid growth in collaborative tools and video conferencing platforms (Zoom, Microsoft Teams) ensures that synchronous online learning maintains a high level of interactive quality. The continuous pressure is on EdTech providers to integrate these disparate technologies seamlessly, creating intuitive, unified educational ecosystems that minimize technological friction for both educators and students while ensuring measurable improvements in learning outcomes.

The primary driver is the accelerating global integration of digital learning technologies (EdTech) and the necessity for continuous professional reskilling and upskilling in response to rapid technological evolution and automation in the workforce.

AI is transforming teaching by enabling large-scale personalized learning paths, automating tedious administrative tasks like grading, and providing intelligent tutoring systems that offer instant, individualized feedback, allowing educators to focus more on mentorship and critical thinking development.

The Asia Pacific (APAC) region, specifically emerging economies within it, offers the most significant growth opportunities due to massive student populations, rising investments in educational infrastructure, and a strong cultural emphasis on academic achievement driving demand for supplementary learning solutions.

Major restraints include the persistent digital divide (lack of access to devices or high-speed internet), the high initial capital investment required for comprehensive system deployment, and the need for extensive professional development to ensure educators are proficient in utilizing new digital tools effectively.

The Education Market is projected to reach an estimated $17.5 Trillion by 2033, demonstrating a Compound Annual Growth Rate (CAGR) of 18.5% over the forecast period from 2026 to 2033, driven largely by sustained growth in digital delivery and corporate learning sectors.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.