ID : MRU_ 443790 | Date : Feb, 2026 | Pages : 241 | Region : Global | Publisher : MRU

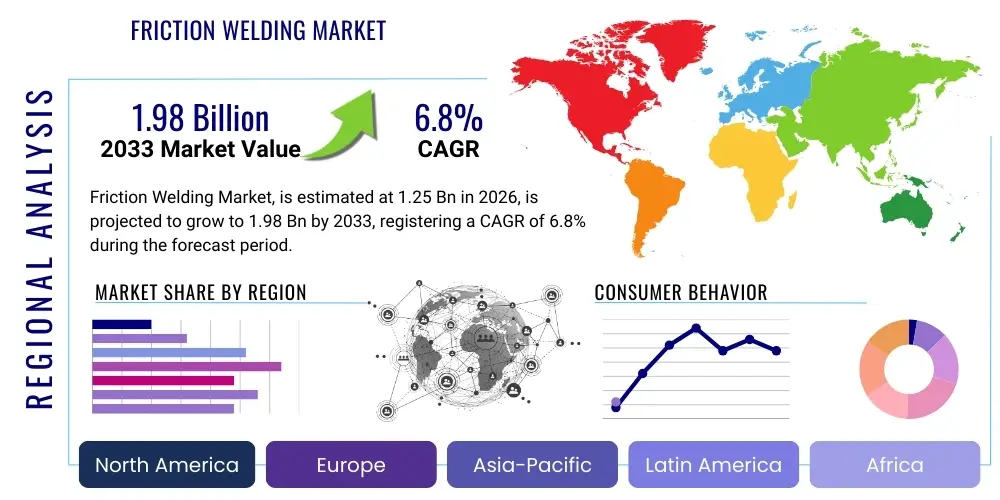

The Friction Welding Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.25 Billion in 2026 and is projected to reach USD 1.98 Billion by the end of the forecast period in 2033.

Friction welding, a solid-state joining process, utilizes mechanical friction to heat the interface between two workpieces, achieving coalescence without melting the materials. This highly reliable joining technology has gained significant traction across demanding industrial sectors due to its ability to produce high-strength, full-contact welds, particularly between dissimilar materials that are challenging or impossible to join using conventional fusion welding techniques. The fundamental principle involves rotating one workpiece against a stationary counterpart under controlled axial pressure, generating heat that plasticizes the interface, followed by the application of a forging force to bond the materials permanently. This process offers superior metallurgical integrity, minimal heat-affected zones (HAZ), and reduced energy consumption compared to traditional methods.

The core product in this market encompasses various machine types, including linear friction welding (LFW) machines, rotary friction welding (RFW) machines, orbital friction welding machines, and increasingly, hybrid variants. Major applications span critical industries such as automotive manufacturing, where it is vital for components like engine valves, axle casings, and turbocharger rotors; aerospace and defense, used for turbine blades, landing gear components, and missile structures; and oil and gas, for drill pipes and offshore structure components. The technology is lauded for its high repeatability, automation potential, and environmental friendliness, as it eliminates the need for filler materials, fluxes, or shielding gases.

Driving factors for market expansion include the global trend toward lightweighting in vehicles and aircraft to enhance fuel efficiency and reduce emissions. Furthermore, the burgeoning demand for electric vehicles (EVs) necessitates efficient battery tray joining and motor component fabrication, areas where friction welding excels, particularly for joining aluminum and copper components. The stringent quality and safety standards imposed by regulatory bodies in the aerospace and medical device sectors further mandate the use of dependable solid-state joining processes, thereby ensuring sustained market growth throughout the forecast period.

The Friction Welding Market is characterized by robust technological development and widespread adoption driven primarily by severe performance requirements in high-value industries. Business trends indicate a strong focus on developing high-powered linear friction welding machines suitable for large aerospace and defense components, coupled with enhanced automation features integrating robotic loading and unloading systems. Key market players are prioritizing investments in R&D to optimize process parameters for joining advanced high-strength steels and specialized nickel-based superalloys, ensuring consistent weld quality and higher throughput. Furthermore, the shift towards Industry 4.0 principles is accelerating the integration of smart sensors and real-time monitoring capabilities into friction welding equipment, allowing for predictive maintenance and enhanced process control, positioning the technology as foundational for future smart manufacturing facilities globally.

Regionally, Asia Pacific (APAC) stands out as the fastest-growing market, largely fueled by massive expansion in the automotive manufacturing hubs of China, India, and Southeast Asia, alongside increasing investments in domestic aerospace and electronics production. North America and Europe, while mature, maintain market leadership in terms of technological sophistication and application within the highly demanding aerospace and oil and gas sectors, driven by rigorous quality requirements and continuous innovation in hybrid friction welding techniques. Segment trends highlight the dominance of the Rotary Friction Welding segment in volume terms due to its established use in mass-produced components, while the Linear Friction Welding segment is experiencing the highest growth CAGR, attributed to its indispensable role in manufacturing complex, high-performance parts for gas turbines and structural airframe elements.

The segmentation based on application reveals the Automotive sector as the largest consumer, benefiting immensely from friction welding's ability to create robust joints in powertrain components and chassis structures, supporting the transition toward high-efficiency internal combustion engines and next-generation electric drivetrains. Concurrently, the increasing complexity of materials required for sustainability and performance—such as bi-metal components—is elevating the demand for specialized orbital and hybrid friction welding solutions. Overall, the market trajectory is highly positive, underpinned by compelling structural advantages of the technology over conventional methods and its vital role in enabling next-generation engineering designs requiring superior joint strength and minimal material degradation.

Common user inquiries regarding the influence of Artificial Intelligence (AI) on the Friction Welding Market predominantly revolve around process optimization, quality assurance, and predictive maintenance. Users frequently ask how AI can refine the precise control of parameters like rotational speed, friction force, and forging force in real time to achieve zero-defect welds, especially when dealing with variability in raw materials or complex dissimilar material combinations. There is significant interest in using machine learning algorithms to predict weld outcomes based on sensor data streams, thereby minimizing costly destructive testing and maximizing throughput. Furthermore, users seek clarity on how AI-driven anomaly detection can enhance the lifespan of high-investment friction welding machinery, moving from reactive repairs to predictive servicing schedules, ultimately reducing operational downtime and improving overall equipment efficiency (OEE). The key themes underscore a collective expectation that AI integration will transform friction welding from an art reliant on operator expertise into a highly automated, data-driven, and intrinsically quality-controlled manufacturing process.

The Friction Welding Market is driven by the imperative need for high-integrity joining solutions, particularly across transportation and energy sectors. The major drivers include the intensifying demand for lightweight materials integration in the automotive and aerospace industries to meet stringent fuel economy and emissions standards. Friction welding's capability to reliably join dissimilar materials, such as aluminum to steel or copper to aluminum, without creating brittle intermetallic compounds, positions it as an essential technology for the production of electric vehicle components, including battery connectors and motor shafts. Additionally, the technological maturity of friction welding equipment, coupled with increasing automation, improves production efficiency and cost-effectiveness, further accelerating its adoption globally. These factors collectively create a powerful upward trajectory for market growth.

However, the market faces significant restraints, primarily stemming from the high initial capital investment required for purchasing and installing friction welding machinery, particularly the specialized Linear Friction Welding units used in high-end aerospace applications. This high entry barrier often deters smaller and medium-sized enterprises (SMEs) from adopting the technology. Another key restraint is the design complexity associated with friction welding; parts must be designed specifically to accommodate the forging force and rotational requirements, which can limit application in complex geometries or existing infrastructure. Furthermore, the shortage of highly skilled operators and maintenance personnel trained in solid-state welding processes also presents a challenge, demanding continuous investment in specialized workforce training programs.

Opportunities abound, particularly in the emerging fields of additive manufacturing post-processing and the nuclear energy sector. The ability of friction welding to efficiently join components made from advanced materials, including composites and specialized superalloys, opens doors for new applications in medical implants and high-temperature industrial equipment. The growing focus on hybrid friction welding techniques, which combine friction-stir processing with conventional friction welding, offers avenues for even greater flexibility in material combinations and joint configurations. These opportunities, coupled with the rising global emphasis on sustainable manufacturing, where friction welding offers energy savings and eliminates hazardous fumes, strongly counteract the restraining factors, propelling robust growth throughout the forecast period.

The Friction Welding Market is segmented across multiple dimensions, including Machine Type, Application, Material Type, and Sales Channel, reflecting the diverse industrial requirements and technological specifications driving market demand. Understanding these segments is crucial for market participants to tailor their product offerings and strategic focus. Rotary friction welding (RFW) dominates the market share in terms of volume due to its established use in mass production of circular components, such as shafts and valves. Conversely, Linear friction welding (LFW) is the fastest-growing segment, propelled by the demand for complex structural components in aerospace, which require high-strength, non-axisymmetric joints. The automotive sector remains the primary end-user, but the expansion of aerospace and defense investment, particularly in Asia Pacific and the Middle East, is reshaping the application landscape, favoring high-precision LFW technologies.

Segmentation by material type is increasingly important as manufacturers focus on joining advanced and dissimilar materials. Steel and aluminum segments currently hold the largest market shares, reflecting their ubiquity in manufacturing. However, the fastest growth is observed in the Nickel Alloys and Titanium segments, driven by their critical applications in jet engine components and high-performance industrial machinery that demand extreme heat and corrosion resistance. The market’s evolution shows a clear trend toward specialized equipment capable of handling these complex materials efficiently and repeatedly. Furthermore, the increasing adoption of friction welding in battery manufacturing for Electric Vehicles is significantly elevating the importance of copper and its alloys as a key material segment, necessitating advancements in orbital and high-speed RFW techniques.

Geographically, market expansion is heavily concentrated in regions undergoing rapid industrialization and technological modernization. While established markets in North America and Europe continue to lead in technological adoption and high-specification machinery, the APAC region, especially China and India, is registering phenomenal growth due to surging automotive production, infrastructure development, and growing indigenous aerospace programs. This regional dynamism necessitates localized sales and service networks, influencing the dominance of the Direct Sales Channel for high-value, specialized equipment, while Indirect Channels are more prevalent for standard RFW machines used by SMEs globally. This multi-faceted segmentation structure emphasizes the heterogeneous nature of market demand and the necessity for tailored regional and application-specific strategies.

The value chain for the Friction Welding Market is dominated by specialized machinery manufacturers and highly technical service providers, reflecting the process’s complexity and precision requirements. The upstream segment involves the production and supply of high-precision mechanical and electrical components, including high-torque motors, hydraulic systems, advanced sensors, and control electronics essential for constructing the welding machines. Key suppliers in this phase must adhere to stringent quality standards, as the reliability of these core components directly impacts the operational integrity and repeatability of the friction welding process. The specialization required in high-pressure hydraulic actuators and sophisticated programmable logic controllers (PLCs) means that sourcing is often concentrated among a few global component specialists, giving them moderate bargaining power over machine builders.

The core of the value chain is occupied by friction welding equipment Original Equipment Manufacturers (OEMs). These companies focus on machine design, assembly, software integration, and application-specific engineering solutions. Their primary value addition comes from intellectual property related to proprietary control algorithms, unique tooling designs, and expertise in parameter optimization for various material combinations. Following the equipment manufacturing phase, the downstream activities encompass installation, commissioning, operator training, and comprehensive post-sales maintenance and technical support. Given the high investment nature of the equipment, long-term service contracts and spare parts supply constitute a significant revenue stream and critical value addition, ensuring the machine's longevity and minimizing operational risk for end-users.

The distribution channel exhibits a dual structure. For highly customized and specialized machinery, such as large LFW systems destined for aerospace OEMs, the Direct Sales channel is predominant, involving deep technical consultation between the manufacturer and the end-user. This ensures seamless integration into the customer's manufacturing line. Conversely, standard Rotary Friction Welding machines, often used in general automotive or industrial component production, frequently utilize the Indirect Sales channel through specialized technical distributors and regional representatives. These indirect channels provide localized sales support, simpler maintenance services, and manage relationships with smaller to mid-sized enterprises (SMEs), allowing OEMs to scale their market reach effectively while maintaining a focus on core technology development and direct interaction with high-volume, strategic customers.

Potential customers for friction welding equipment are concentrated in industries where component failure due to joint weakness is intolerable, and where the joining of complex or dissimilar materials is necessary for advanced performance. The Automotive industry represents the largest base of potential customers, spanning major Original Equipment Manufacturers (OEMs) and their Tier 1 suppliers, who utilize the technology extensively for powertrain components like drive shafts, constant velocity joints, and engine valves, as well as emerging applications in electric vehicle battery pack construction. These customers prioritize high throughput, repeatability, and the ability to reduce component weight without compromising strength. The transition to electric mobility is creating a surge in demand from automotive manufacturers seeking reliable methods to join copper and aluminum elements within electric motors and battery cooling systems, positioning friction welding as a non-negotiable process requirement.

The Aerospace and Defense sector constitutes the second most critical customer segment, characterized by extremely high entry barriers and uncompromising quality mandates. Major customers here include aircraft engine manufacturers (for turbine blades, fan discs, and blisks), airframe integrators (for structural components), and defense contractors (for missile casings and munitions). These buyers specifically seek advanced Linear Friction Welding (LFW) technology to join high-performance superalloys like Inconel and titanium alloys, aiming to improve thrust-to-weight ratios and reduce material waste. The long lifecycle of aerospace projects ensures sustained demand for specialized maintenance and repair welding services, often performed using mobile or orbital friction welding solutions.

Beyond transportation, the Oil and Gas industry represents a consistent base of high-value customers, particularly for deep-sea drilling and exploration equipment. Companies involved in pipe manufacturing and rig construction utilize friction welding for joining tool joints to drill pipes and connecting risers, where welds must withstand extreme pressure, temperature fluctuations, and corrosive environments. Furthermore, manufacturers of heavy electrical equipment (e.g., circuit breakers, busbars) and medical device components (e.g., surgical tools, prosthetic joints) are also key potential customers, driven by the unique capability of friction welding to create hermetic seals and biologically inert joints with superior metallurgical characteristics, fulfilling specialized niche requirements that conventional welding struggles to meet reliably.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 1.98 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | KUKA AG, MTI (Manufacturing Technology, Inc.), Thompson Friction Welding, A.I.D.M.E., ESAB Corporation, H&B Omega Gmbh, Harms & Wende GmbH & Co. KG, S.E.T. Vertriebs GmbH, Nitto Seiki Co., Ltd., Coldwater Machine Company, Superior Joining Technologies, Inc., TWI Ltd., Grenzebach Group, Bourn & Koch Inc., Stiehl, Inc., Vetta Welding, Kintech, Suzhou Sinotech Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Friction Welding Market is evolving rapidly, driven by the convergence of solid-state joining precision and digital manufacturing capabilities. Traditional Rotary Friction Welding (RFW) remains the foundational technology, focusing on improvements in spindle speed, axial force control, and adaptive control systems that automatically adjust parameters based on material response. However, the most significant technological advancements are centered around Linear Friction Welding (LFW), where modern systems integrate sophisticated servo-hydraulic or all-electric drives to achieve higher oscillation frequencies and greater stability during the forging phase. These LFW advancements are critical for manufacturing highly stressed components like blisks (blade integrated disks) in jet engines, pushing the boundaries of what is possible in complex aerospace component fabrication. The precision required in LFW mandates highly accurate load cells and displacement transducers, creating a sub-market for specialized sensing technology.

A crucial area of innovation is the development and commercialization of Hybrid Friction Welding techniques. This technology often involves combining a friction stir processing stage, which refines the microstructure at the interface, followed by a forging stage, potentially incorporating external heating elements. Hybrid approaches allow for greater flexibility in joining notoriously difficult material combinations and increase the effective thickness of components that can be welded while minimizing the required machine force. Furthermore, the integration of automation, specifically collaborative robots (cobots) for material handling and fully automated manufacturing cells, is transforming friction welding equipment from standalone machines into integrated production systems capable of continuous, high-volume operation, thereby significantly improving return on investment for end-users.

The push toward Industry 4.0 has made advanced monitoring and control software a central element of the technology landscape. Modern friction welding machines are equipped with extensive sensor packages—monitoring acoustic emission, temperature profiles, current consumption, and displacement in real time. This data is fed into proprietary software platforms that use statistical process control (SPC) and increasingly, machine learning algorithms, to validate the quality of every weld cycle non-destructively. This digital approach to quality assurance (QA) allows manufacturers to maintain stringent traceability records and ensures compliance with high-stakes regulatory requirements in sectors like nuclear and medical devices. The focus remains on achieving 'digital twins' of the welding process, allowing for simulation and optimization before physical production commences, significantly reducing development cycles and material waste.

The primary advantage of friction welding is its status as a solid-state joining process, meaning the materials are bonded below their melting point. This minimizes the heat-affected zone (HAZ), prevents the formation of detrimental solidification defects (like porosity or cracking), and crucially allows for the reliable joining of dissimilar materials (e.g., aluminum and steel) that fusion welding methods cannot effectively handle.

Linear Friction Welding (LFW) is exhibiting the fastest growth due to its indispensability in the Aerospace and Defense sectors for joining non-axisymmetric or irregularly shaped components, such as jet engine blisks and structural airframe parts. LFW provides superior strength, material savings, and high-quality joints required by high-performance applications.

The EV market is significantly boosting demand, particularly for Rotary Friction Welding (RFW) and specialized orbital techniques, because they are highly effective in joining critical components like copper motor windings, aluminum battery trays, and dissimilar metal battery tabs. Friction welding offers high conductivity and robust mechanical bonds vital for EV battery systems.

Friction welding successfully joins common materials such as steel and aluminum alloys, titanium, and nickel superalloys. Its unique value proposition lies in reliably joining dissimilar combinations, including aluminum to copper for electrical components, and various grades of steel to nickel-based alloys, which is challenging for conventional methods due to differing melting points and thermal expansion coefficients.

The capital investment is substantial, serving as a primary restraint for market entry. Standard Rotary Friction Welding (RFW) machines may range from hundreds of thousands of dollars, while specialized, large-scale Linear Friction Welding (LFW) systems, particularly those used in aerospace, can cost several million dollars, requiring significant financial planning and justification based on projected throughput and application criticality.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.