ID : MRU_ 441711 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

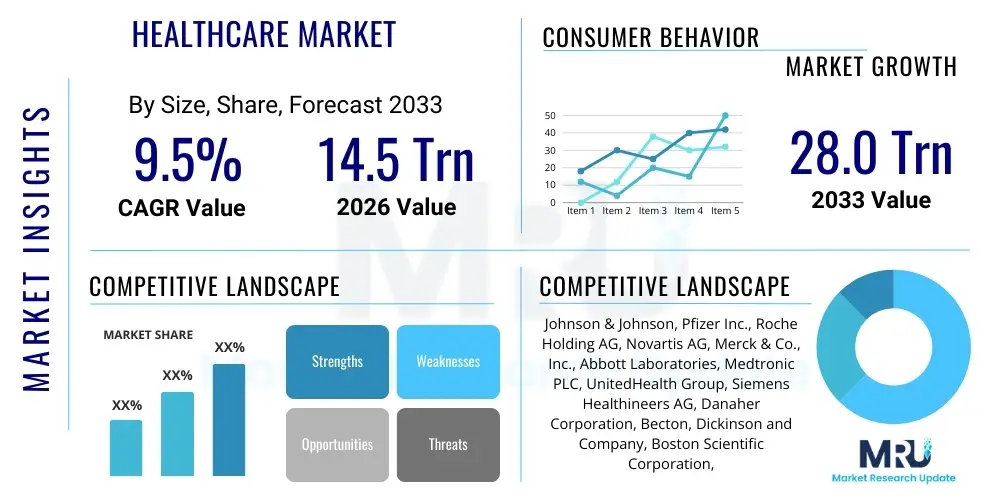

The Healthcare Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 12.7 Trillion in 2026 and is projected to reach USD 20.3 Trillion by the end of the forecast period in 2033.

The global Healthcare Market encompasses a vast ecosystem dedicated to maintaining and improving public and individual health through the provision of services, manufacturing of medical equipment, development of pharmaceuticals, and implementation of sophisticated technological solutions. This sector includes hospitals, clinics, diagnostic laboratories, pharmaceutical companies, biotechnology firms, and medical device manufacturers. The core product offering spans preventive, curative, palliative, and rehabilitative care, underpinned by complex operational frameworks and stringent regulatory environments globally. Key major applications include inpatient care, outpatient services, long-term care, and specialized services such as oncology and cardiology, driven significantly by demographic shifts and the rising prevalence of chronic diseases.

The primary benefits delivered by the healthcare industry involve improved quality of life, increased life expectancy, and effective management of complex medical conditions. Modern healthcare systems leverage advanced technologies like genomics, telemedicine, and minimally invasive surgery, ensuring higher efficiency and better patient outcomes. The continuous evolution of medical science and the adoption of personalized medicine approaches are enhancing the effectiveness of treatments, moving the focus from reactive sickness care to proactive wellness management. This shift is crucial for managing the escalating costs associated with prolonged chronic disease management and optimizing resource allocation across different healthcare settings.

Driving factors for sustained market growth include rapid technological advancements, especially in digital health and Artificial Intelligence (AI), increasing healthcare expenditure worldwide, and the growing elderly population which requires extensive and continuous medical support. Furthermore, enhanced access to insurance coverage in developing economies, coupled with governmental initiatives prioritizing public health infrastructure, are propelling demand across all segments of the market. The increasing awareness regarding preventative healthcare and wellness services also contributes significantly to the market's expansive trajectory, particularly in high-income regions where consumer spending on health-related products and services is high.

The global Healthcare Market is experiencing robust expansion driven by unprecedented technological integration and shifting demographic profiles. Business trends indicate a strong move toward consolidation among major providers and payers, optimizing economies of scale and standardizing care protocols. Investment in digital transformation, particularly Electronic Health Records (EHR) and remote monitoring, is a critical business priority, aimed at enhancing operational efficiency and improving patient engagement. The financial landscape is characterized by increasing venture capital flowing into health-tech startups, signaling confidence in innovative delivery models and disruptive technologies like AI-driven diagnostics and personalized therapeutics.

Regionally, North America maintains market dominance due to high per capita healthcare spending, advanced infrastructure, and a robust research and development ecosystem. However, the Asia Pacific (APAC) region is emerging as the fastest-growing market, fueled by expanding middle-class populations, improving access to healthcare, and significant governmental investment in infrastructure development, particularly in nations like China and India. Europe shows sustained growth, emphasizing value-based care models and public health system improvements, while Latin America and MEA focus on addressing infrastructure gaps and improving the availability of affordable generic medications.

Segmentation trends highlight the rapid growth of the pharmaceuticals segment, particularly in biologics and specialty drugs, addressing complex diseases. The service segment, led by hospitals and outpatient facilities, is shifting toward decentralized care delivery models, emphasizing ambulatory services and home healthcare. Technology segments, including diagnostics and digital health, are witnessing accelerated adoption, driven by the necessity for quicker, more accurate diagnoses and the efficient management of large patient populations through telehealth platforms and monitoring devices. This shift underscores a broader industry pivot toward preventative and predictive healthcare solutions.

Common user questions regarding the impact of Artificial Intelligence (AI) on the Healthcare Market primarily revolve around operational efficiency, diagnostic accuracy, ethical implications, and job displacement. Users frequently inquire about how AI models, particularly machine learning and deep learning, are revolutionizing medical imaging interpretation, accelerating drug discovery timelines, and automating administrative tasks. A significant concern centers on data privacy and the regulatory framework required to govern AI-driven clinical decisions. Expectations are high regarding personalized medicine, where AI can analyze vast genomic datasets to tailor treatments, improving therapeutic outcomes while simultaneously mitigating adverse drug reactions.

AI is transforming the sector by enhancing the precision and speed of medical interventions. In diagnostics, AI algorithms can analyze complex medical images (e.g., X-rays, MRIs, CT scans) with equal or superior accuracy compared to human specialists, often reducing the time required for diagnosis in critical scenarios. This capability aids early disease detection, which is crucial for conditions like cancer and neurological disorders. Furthermore, AI is fundamentally changing the pharmaceutical R&D process, allowing researchers to screen millions of compounds virtually, predict drug efficacy and toxicity, and significantly cut down the time and cost associated with bringing a new therapy to market.

Operationally, AI contributes significantly to reducing the administrative burden on healthcare providers. Automated scheduling, billing, and electronic health record (EHR) management systems powered by AI streamline hospital workflows, allowing clinical staff to dedicate more time to direct patient care. Moreover, predictive analytics utilize AI to forecast disease outbreaks, identify patients at high risk of readmission, and optimize resource allocation within hospital networks, thereby improving overall efficiency and leading to better financial performance for healthcare organizations.

The Healthcare Market is profoundly influenced by a complex interplay of Drivers, Restraints, and Opportunities (DRO). Key drivers include the global aging population, the escalating prevalence of chronic diseases like diabetes and cardiovascular conditions, and continuous technological innovation, especially in digital health and precision medicine. Restraints often manifest as high regulatory hurdles, the significant cost of advanced treatments and pharmaceuticals, and challenges related to interoperability and data security across disparate healthcare systems. Opportunities are centered around leveraging emerging markets, expanding telehealth capabilities, and integrating value-based care models to enhance efficiency and patient outcomes. These forces collectively define the market’s growth trajectory, pushing providers toward greater efficiency and patient-centric delivery models.

The primary impact forces shaping the market involve intense regulatory scrutiny, which mandates compliance with complex safety and efficacy standards, especially for new drugs and medical devices. Economic forces, such as global inflation and pressure from payers (governments and private insurers) to control escalating costs, necessitate constant innovation in cost-effective care delivery. Societal shifts, particularly the growing demand for convenience and personalized care, are compelling the industry to adopt decentralized service models, moving care delivery closer to the patient’s home. The increasing prominence of consumer engagement, driven by accessible health information, forces providers to be more transparent and responsive to patient needs.

Technological forces act as the most significant catalyst, transforming diagnostics, treatment, and administration. The integration of genomic data, coupled with advanced computational power, facilitates the development of highly targeted therapies. Simultaneously, cybersecurity resilience is becoming a critical impact force, as the reliance on interconnected digital health records increases the vulnerability to data breaches. Successfully navigating these impact forces requires healthcare organizations to invest heavily in robust IT infrastructure, maintain rigorous compliance standards, and foster strategic partnerships to mitigate financial risks associated with expensive R&D and regulatory approval processes.

The global Healthcare Market is extensively segmented across multiple dimensions, including Type, Application, Service, and Geography, providing granular insights into sector performance and investment priorities. This segmentation is crucial for understanding the diverse needs of patients, providers, and payers across different economic and regulatory landscapes. The primary segments reflect the core components of the healthcare ecosystem, ranging from medical products and pharmaceuticals (Type) to the specific diseases being treated (Application) and the delivery channels utilized (Service). Analysis of these segments reveals distinct growth patterns, with digital health and pharmaceuticals targeting chronic conditions currently exhibiting the highest growth momentum globally.

The Type segmentation typically divides the market into pharmaceuticals, medical devices, and medical services. Pharmaceuticals remain the largest revenue generator, driven by the launch of novel biological drugs and specialty medications for rare diseases. The medical device segment is witnessing significant innovation in minimally invasive surgical tools and advanced diagnostic imaging equipment. Meanwhile, the Service segment, comprising hospitals, clinics, and ancillary services, is evolving rapidly toward decentralized and outpatient models, driven by cost reduction mandates and patient preference for convenience. The inherent capital intensity and regulatory requirements vary substantially across these segments, influencing entry barriers and competitive strategies.

Further analysis based on Application reveals concentrated growth in high-burden disease areas such as oncology, cardiovascular health, and endocrinology (diabetes management), reflecting global epidemiological trends. The segmentation by Service model highlights the growing preference for home healthcare and remote patient monitoring, especially in developed nations facing labor shortages and resource constraints in traditional hospital settings. Understanding these sub-segments allows stakeholders, including investors and policymakers, to accurately forecast resource needs and prioritize R&D efforts in areas offering the greatest potential societal and economic return.

The healthcare value chain is exceptionally complex, involving numerous interconnected stages from initial research and development (Upstream) to final service delivery and patient consumption (Downstream). Upstream activities involve extensive basic scientific research, clinical trials, and the manufacturing of specialized ingredients (Active Pharmaceutical Ingredients or APIs) and core components for medical devices. This stage is dominated by pharmaceutical and biotech companies, characterized by high investment, long timelines, and significant intellectual property protection. The efficiency and rigor of the upstream process directly dictate the quality and availability of essential medical innovations for the market.

Midstream processes include the intricate manufacturing of finished drugs and medical devices, quality assurance, regulatory approval processes (such as FDA or EMA authorization), and inventory management. Distribution channels form a critical part of the midstream/downstream transition, involving wholesalers, distributors, logistics providers, and specialized cold chain management services necessary for sensitive biological products. Direct distribution models, often employed by high-value specialty drugs, contrast with indirect channels that rely heavily on large-scale hospital networks and retail pharmacy chains to ensure wide accessibility across diverse geographical markets.

Downstream activities focus entirely on patient interaction and service provision, encompassing hospitals, primary care physicians, pharmacies, diagnostic labs, and home healthcare agencies. This stage involves the crucial role of Payers (governments and private insurers) who determine reimbursement policies and pricing, significantly influencing market access and uptake of products. The shift towards integrated delivery networks (IDNs) and Accountable Care Organizations (ACOs) emphasizes collaboration between providers and payers, aiming for value-based outcomes rather than volume, thereby constantly restructuring the downstream dynamics and patient engagement models.

The potential customer base for the Healthcare Market is diverse and multifaceted, encompassing institutional buyers, centralized payment entities, and individual consumers. The largest and most crucial customers are Healthcare Providers, specifically hospitals (public and private), specialized clinics, and integrated delivery systems, which purchase vast quantities of pharmaceuticals, medical devices, and technological infrastructure. These institutional customers require robust supply chain reliability, proven clinical efficacy, and cost-effectiveness, often relying on long-term contracts and bundled purchasing agreements to manage their expenditures efficiently.

Another dominant segment consists of Payers, including government health programs (like Medicare/Medicaid in the US or NHS in the UK), private health insurance companies, and managed care organizations. Although not direct consumers of the product, Payers act as gatekeepers, determining which treatments and devices are reimbursed, thereby heavily influencing the demand curve for manufacturers. Their decision-making is driven by pharmacoeconomic studies and evidence of cost-saving potential or superior patient outcomes, positioning them as essential stakeholders whose approval unlocks mass market access.

Finally, the individual Patient/Consumer segment represents a rapidly growing customer base, particularly in areas like elective procedures, over-the-counter medications, wellness services, and digital health applications. With the rise of consumer-driven healthcare and higher deductible plans, individuals are becoming more proactive in purchasing services directly, especially those related to preventative care and lifestyle management. Pharmaceutical and Biotechnology companies, alongside Research Institutions, also act as substantial B2B customers, purchasing R&D services, clinical trial support, and high-end laboratory equipment necessary for continuous innovation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 12.7 Trillion |

| Market Forecast in 2033 | USD 20.3 Trillion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Johnson & Johnson, Pfizer Inc., Roche Holding AG, Novartis AG, Merck & Co., Inc., Abbott Laboratories, Medtronic plc, Siemens Healthineers AG, GE Healthcare, Danaher Corporation, UnitedHealth Group, CVS Health, Thermo Fisher Scientific Inc., Bristol-Myers Squibb, Sanofi S.A., AstraZeneca PLC, Boston Scientific Corporation, Stryker Corporation, Becton, Dickinson and Company, HCA Healthcare. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Healthcare Market is characterized by rapid adoption of digital tools designed to enhance precision, efficiency, and accessibility of care. Core technologies include Artificial Intelligence (AI) and Machine Learning (ML), which are integral to diagnostic imaging, risk stratification, and drug development processes. Telemedicine platforms, encompassing remote patient monitoring (RPM) and virtual consultations, have seen exponential growth, shifting primary care interactions away from physical infrastructure. These digital tools enable continuous data collection and analysis, allowing for proactive interventions and better management of chronic conditions, significantly reducing the reliance on episodic care.

Further technological advancements are centered around genomics and molecular diagnostics. Next-Generation Sequencing (NGS) technologies are becoming more accessible and affordable, driving the personalized medicine paradigm by enabling detailed genetic profiling for disease susceptibility and treatment selection. Coupled with advanced bioinformatics, these tools allow for highly targeted therapeutic approaches, minimizing the side effects commonly associated with broad-spectrum treatments. The integration of nanotechnology is also emerging, particularly in drug delivery systems, offering enhanced targeting of diseased tissues while sparing healthy cells.

Additionally, the deployment of robust cloud computing infrastructure and the implementation of blockchain technology are crucial for secure data management and interoperability. Cloud services provide the necessary computational power for handling massive datasets generated by EHRs and genomic studies, while blockchain is being explored to create secure, immutable ledgers for patient data sharing across different institutions, addressing key concerns related to privacy and system fragmentation. The adoption of robotics in surgery and hospital logistics also represents a significant technological leap, improving surgical precision and automating sterile materials management.

North America maintains its position as the largest market globally, attributed to high disposable income, sophisticated healthcare infrastructure, and substantial investment in R&D, particularly in biotechnology and advanced medical devices. The United States, in particular, drives the region's growth due to its highly fragmented yet technologically advanced ecosystem, characterized by strong venture funding into digital health startups and a high rate of adoption of specialty pharmaceuticals. Stringent regulatory standards, while posing initial hurdles, ultimately foster high quality and innovation, sustaining the region's premium pricing structure.

The North American market is rapidly transitioning toward value-based care models, encouraged by major payers and government initiatives seeking to curb runaway healthcare costs. This shift necessitates investment in robust IT systems for data integration and predictive analytics, benefiting companies specializing in health information technology and remote monitoring solutions. Furthermore, the region's concentration of leading academic research institutions ensures a continuous pipeline of innovation, particularly in areas like cell and gene therapies.

Europe constitutes the second-largest market, characterized by centralized national health services (like the NHS) alongside significant private sector contributions. The market dynamics are largely influenced by governmental prioritization of universal access and cost-containment measures, favoring the use of generic drugs and promoting efficiency through standardized care pathways. Countries such as Germany and France are leaders in medical device manufacturing and pharmaceutical production, emphasizing high standards of care and early adoption of advanced medical technologies within their public systems. The harmonization of medical device regulations (MDR) across the EU is influencing product approval and market access strategies for international firms.

The European market is seeing increasing penetration of digital health solutions, driven by efforts to manage aging populations and reduce the strain on hospital resources. Telehealth implementation accelerated significantly following recent global health crises, becoming a permanent fixture in many national care strategies. Despite regulatory complexity associated with pan-European data sharing (GDPR), the strong focus on public health funding guarantees stable demand across core services, particularly for chronic disease management and mental health support.

Asia Pacific (APAC) is projected to be the fastest-growing region throughout the forecast period. This accelerated growth is primarily driven by massive, rapidly expanding patient populations, increasing per capita healthcare spending, and substantial governmental investments aimed at modernizing infrastructure. Nations like China and India are experiencing significant healthcare modernization, moving from basic service provision to specialized, high-tech medical capabilities. The rising prevalence of lifestyle diseases combined with improved insurance penetration fuels the demand for premium medical services and specialty pharmaceuticals.

Key market drivers in APAC include medical tourism in countries offering high-quality, cost-effective procedures (e.g., Thailand, Singapore), and the swift adoption of cost-effective digital technologies to bridge geographical accessibility gaps in rural areas. While competition based on pricing is intense, particularly in the generics market, there is a clear appetite for innovative diagnostics and high-end medical equipment, positioning the region as a critical manufacturing hub and a lucrative end-user market for global healthcare companies. Investments in local R&D capabilities are also surging, aiming to address region-specific health challenges.

Latin America represents a developing market segment characterized by diverse public and private healthcare funding mechanisms and significant disparities in access between urban and rural areas. Major markets like Brazil and Mexico are undergoing structural reforms aimed at improving insurance coverage and standardizing public health provisions. The market is primarily driven by the demand for essential pharmaceuticals and medical consumables, with a growing segment dedicated to advanced diagnostics and specialized care in private facilities. Economic volatility and currency fluctuations remain restraining factors that affect large-scale international investment.

Technological adoption in Latin America is focused on scalable, affordable solutions. Telemedicine is gaining traction as a tool to extend specialist consultation reach across vast geographical distances. Local manufacturing capabilities for generic pharmaceuticals are strong, but the region remains reliant on imports for advanced medical devices, creating specific import substitution opportunities for international suppliers able to navigate local regulatory processes efficiently.

The Middle East and Africa (MEA) region presents a fragmented market with unique investment characteristics. The Middle East (specifically GCC countries) is characterized by high, centralized government spending, luxurious healthcare facilities, and a strong push toward medical tourism and specialized care, often driven by international partnerships and advanced technology procurement. Infrastructure investment in flagship healthcare cities is a key driver. Conversely, many parts of Africa face significant infrastructure challenges, with the market predominantly focused on essential drugs, infectious disease management, and public health initiatives supported by global aid organizations and local government programs.

MEA is rapidly adopting digital health to leapfrog traditional infrastructural hurdles, particularly in telehealth and mobile health solutions designed for remote populations. The demand for advanced treatments for non-communicable diseases (NCDs) is rising in the urban centers of both regions. Regulatory harmonization efforts within the GCC aim to facilitate faster market entry, making the region increasingly attractive for high-end pharmaceutical and medical device manufacturers seeking specialized patient populations and high reimbursement rates.

The primary drivers include the rapidly aging global population requiring extensive medical services, the rising prevalence of chronic diseases (like diabetes and cardiovascular conditions), substantial technological advancements in digital health and diagnostics, and increasing healthcare expenditure across emerging economies.

AI is transforming healthcare by improving diagnostic accuracy in medical imaging, accelerating the drug discovery process, enabling personalized treatment protocols based on genomic data, and optimizing hospital operations through predictive analytics and administrative automation.

North America currently holds the largest market share due to advanced infrastructure and high spending. However, the Asia Pacific (APAC) region is projected to be the fastest-growing market, driven by infrastructure development and expanding patient access in nations like China and India.

Key restraints include the extremely high cost of pharmaceutical research and advanced medical technologies, stringent and complex regulatory approval pathways across different regions, and persistent challenges related to data interoperability and maintaining cybersecurity for sensitive patient records.

Personalized medicine is highly significant as it utilizes advanced genomics and AI to tailor treatments to an individual’s genetic makeup, promising higher efficacy and fewer side effects. This shift represents a major opportunity for high-value specialty pharmaceutical and diagnostic segments within the forecast period.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.