ID : MRU_ 443286 | Date : Feb, 2026 | Pages : 246 | Region : Global | Publisher : MRU

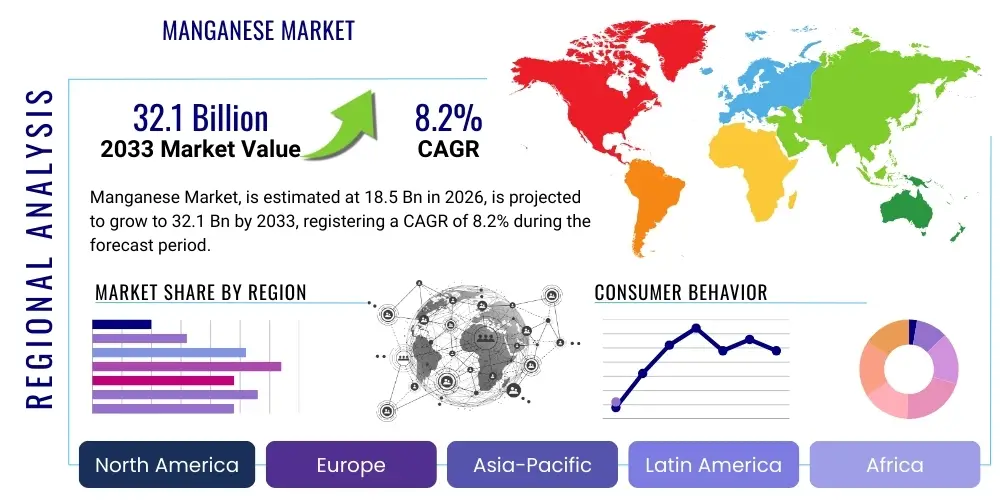

The Manganese Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2026 and 2033. The market is estimated at USD 18.5 Billion in 2026 and is projected to reach USD 32.1 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by the escalating global demand for steel, where manganese acts as a critical deoxidizer and alloying agent, indispensable for enhancing strength, hardness, and durability. Concurrently, the burgeoning electric vehicle (EV) sector is exerting unprecedented pressure on the high-purity manganese segment, necessary for advanced lithium-ion battery cathodes, signaling a significant shift in value proposition from traditional metallurgical uses to high-tech energy applications.

Market valuation reflects the intricate interplay between geopolitical stability in key mining regions, such as South Africa and Australia, and the capital expenditure dedicated to refining and processing capabilities across Asia-Pacific, particularly China. Furthermore, the future trajectory of the market is heavily reliant on technological advancements aimed at sustainable mining practices and efficient production of high-purity manganese sulfate monohydrate (HPMSM). Investors and major stakeholders are increasingly prioritizing supply chain resilience and vertical integration to secure access to critical raw materials, positioning the manganese sector as a focal point for industrial strategic development in the coming decade, extending beyond basic commodity trading into specialized chemical manufacturing.

The Manganese Market encompasses the exploration, mining, processing, and distribution of manganese ore and its various derivatives, which are primarily categorized into metallurgical grades and chemical/battery grades. Manganese (Mn) is the twelfth most abundant element in the Earth’s crust and is crucial for global industrial activity due to its versatility and low cost relative to other alloying elements. The product description spans raw ore (typically 30% to 50% Mn content), ferroalloys (ferro-manganese and silico-manganese, essential for steelmaking), electrolytic manganese metal (EMM), electrolytic manganese dioxide (EMD), and specialized high-purity manganese compounds (HPMSM) used in niche applications.

Major applications of manganese are predominantly centered around the steel industry, consuming over 90% of global output, where it is utilized to remove sulfur and oxygen during steel production and to impart desirable properties such as corrosion resistance and tensile strength. Secondary, yet rapidly growing, applications include its use in aluminum alloys, fertilizers, catalysts, water treatment, and increasingly, in alkaline batteries and the cathodes of lithium-ion batteries powering Electric Vehicles (EVs) and grid storage solutions. The benefit profile of manganese lies in its economic feasibility, superior metallurgical performance in ferroalloys, and its critical function in stabilizing the crystal structure of nickel-cobalt-manganese (NCM) and nickel-manganese-cobalt-aluminum (NMCA) battery chemistries, offering enhanced energy density and safety.

Driving factors propelling the market include rapid urbanization and infrastructure development in emerging economies, notably India and Southeast Asia, which necessitates high volumes of steel production. Furthermore, stringent global emission standards are accelerating the transition towards electric mobility, leading to exponential growth in demand for high-purity manganese derivatives. Technological shifts towards high-performance steel grades and the development of manganese-rich battery cathodes (such as LMFP – Lithium Manganese Iron Phosphate) are creating new premium market segments, ensuring sustained investment in exploration and value-added processing capabilities, mitigating risks associated with reliance solely on conventional metallurgical demand cycles.

The Manganese Market exhibits strong business trends characterized by dual-market dynamics: the mature, volume-driven metallurgical segment and the nascent, high-growth, high-value battery segment. Strategic investment is heavily skewed towards securing high-purity manganese supply chains, driven by major automotive and battery manufacturers seeking long-term stability and traceability. Consolidation is observable among primary miners and processors aiming for economies of scale, while technological innovation focuses on reducing energy consumption in EMM and HPMSM production. Global economic performance, particularly in construction and automotive manufacturing, remains the primary short-term determinant for the metallurgical grade market, while regulatory mandates supporting electrification dictate the long-term outlook for chemical grades, leading to divergent pricing structures and capital allocation strategies across the sector.

Regional trends highlight the continued dominance of the Asia Pacific (APAC) region, specifically China, which is the world’s largest consumer of manganese, driven by its expansive steel industry and pre-eminence in battery manufacturing and processing. South Africa, holding a significant portion of global manganese reserves, remains crucial for supply, although logistical and power supply challenges introduce volatility. North America and Europe are focusing on establishing domestic and near-shored processing facilities to reduce dependence on Chinese refining capacity, often supported by government initiatives like the Critical Raw Materials Act (CRMA) in Europe. This shift underscores a broader trend towards supply chain de-risking and regional self-sufficiency, influencing global trade flows and investment patterns significantly in the forecast period.

Segmentation trends indicate that the Ferroalloys segment (Ferro-Manganese and Silico-Manganese) will maintain the largest market share by volume due to the indispensable role of manganese in steel. However, the High-Purity Manganese Chemicals segment (EMD, HPMSM) is projected to record the highest Compound Annual Growth Rate (CAGR) by value, reflecting the premium pricing associated with battery-grade materials. Within applications, the Electric Vehicle segment is outpacing all others in growth, demanding stringent quality control and sustainable sourcing, thereby fragmenting the market based on purity levels and sustainability certifications. This rapid evolution requires market participants to rapidly adapt their operational profiles, moving from bulk commodity handling to sophisticated chemical manufacturing.

Common user questions regarding AI's impact on the Manganese Market frequently revolve around how artificial intelligence and machine learning (AI/ML) can enhance the efficiency of resource identification, optimize complex mining operations, and improve the energy-intensive processing of ferroalloys and high-purity chemicals. Stakeholders are particularly concerned with leveraging AI for predictive maintenance in heavy machinery to minimize costly downtime in remote mining sites, and for optimizing the complex chemical parameters involved in producing battery-grade materials like HPMSM, where yield and purity are paramount. The summarized consensus suggests that while AI adoption is nascent compared to IT-intensive sectors, its potential for dramatically reducing operational expenditure (OpEx), enhancing worker safety through automated monitoring, and improving material traceability across the supply chain is viewed as transformative, shifting the industry towards higher efficiency and greater predictability in supply.

The Manganese Market is primarily driven by robust global steel production and the accelerating adoption of electric vehicles (EVs), which necessitates increasing volumes of both metallurgical and high-purity chemical grades, respectively. These drivers are tempered by significant restraints, including the highly concentrated geographical supply base, particularly in South Africa, leading to geopolitical risks and supply chain fragility, coupled with the high energy intensity and subsequent carbon footprint associated with ferroalloy production and electrolytic processing. Opportunities abound in the development of sustainable, low-carbon mining techniques, the scaling of high-purity manganese sulfate (HPMSM) capacity outside of traditional refining hubs (e.g., North America and Europe), and the potential for enhanced manganese utilization in emerging battery chemistries, such as Manganese-rich NCM (NMC 811, NMC 90/05/05) and LMFP cathodes. The combined impact forces of EV policy acceleration and infrastructure demand significantly outweigh short-term volatility caused by global economic cycles affecting steel production, ensuring a fundamentally strong, high-growth trajectory for the chemical segment, while the metallurgical segment remains exposed to commodity price cycles and regulatory pressures regarding energy use and emissions.

The Manganese Market is rigorously segmented based on product type, application, and end-user, reflecting the diverse industrial requirements and purity standards. Product segmentation is essential as it dictates the level of processing complexity and market price, ranging from low-cost ores to premium battery chemicals. Application segmentation clearly delineates the massive volume consumption by the traditional steel sector versus the specialized, quality-intensive consumption by the high-tech battery sector. Furthermore, geographic segmentation reveals stark differences in consumption patterns, production capacities, and regulatory environments, influencing strategic decisions regarding mining development and processing plant location. Understanding these segments is paramount for strategic planning, allowing companies to focus on high-margin growth areas like HPMSM while maintaining operational efficiency in the volume-driven ferroalloy markets.

The Manganese Market value chain is inherently complex, starting with highly concentrated upstream mining and progressing through energy-intensive beneficiation and midstream processing to reach diverse downstream end-users. Upstream analysis focuses on ore extraction, dominated by a few key players primarily located in South Africa, Australia, and Gabon. Key activities here involve geological surveys, capital-intensive mine development, and initial crushing and screening. Critical challenges upstream include logistical bottlenecks due to long distances from mines to ports and increasing regulatory scrutiny regarding environmental and social governance (ESG) compliance, pressuring miners to adopt more sustainable practices and reduce water consumption in beneficiation processes.

Midstream activities encompass the transformation of raw ore into marketable products, primarily ferroalloys and high-purity chemicals. This stage is characterized by high energy consumption, particularly for electric arc furnaces used in ferroalloy production and electrolysis cells for EMM and EMD. China dominates this processing stage due to historical cost advantages and established infrastructure, although new facilities are emerging in North America and Europe to localize processing for battery materials. The transition from metallurgical-grade processing to high-purity chemical processing involves significant investment in specialized purification technologies, such as leaching and solvent extraction, representing a crucial value-add step.

The downstream analysis involves the distribution channels and end-use manufacturing sectors. Distribution is bifurcated: bulk metallurgical products are often sold directly to large integrated steel mills or via major commodity traders (indirect channel), while specialized battery chemicals (HPMSM, EMD) require stringent quality control and often involve direct, long-term supply agreements between processors and cathode manufacturers (direct channel). The shift towards EV batteries necessitates robust traceability systems to ensure ethical sourcing and purity standards are maintained across the entire chain, from mine to cathode cell, driving higher integration and less reliance on spot market trading for specialized grades.

Potential customers for the Manganese Market span several distinct industrial sectors, reflecting the dual nature of manganese consumption. The largest customer base, by sheer volume, comprises integrated steel producers and specialized ferroalloy manufacturers globally, particularly in major steel-producing nations like China, India, and the United States. These customers require consistent, high-volume supply of standard and refined ferro-manganese products to ensure the quality and structural integrity of their final steel products used in construction, machinery, and automotive chassis. Contractual stability and competitive pricing are critical determinants for serving this established customer base, often requiring complex logistical solutions to manage bulk freight across continents.

A second, rapidly growing segment includes lithium-ion battery cathode manufacturers and precursors producers. Companies like LG Energy Solution, CATL, and Panasonic, along with specialized chemical manufacturers focused on high-purity salts, constitute a premium customer base. These buyers demand stringent purity specifications (typically 99.9% or higher), guaranteed low levels of heavy metal impurities, and demonstrable supply chain sustainability compliance, making HPMSM and EMD manufacturers their primary suppliers. The purchasing criteria for this segment prioritize long-term certainty, technical partnership, and product quality consistency over simple cost minimization, driving premiums for certified battery-grade materials.

Additional customer segments include producers of primary batteries (e.g., Duracell, Energizer), agricultural chemical companies requiring manganese sulfate for fertilizers, and specialized chemical companies utilizing potassium permanganate for water treatment and industrial synthesis. These niche segments, while smaller in volume, provide market diversity and stability. Furthermore, emerging end-users in the grid-scale energy storage sector, exploring manganese-based flow batteries and advanced sodium-ion technologies, represent future growth potential, driven by global mandates for renewable energy integration and reliable grid stabilization solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 32.1 Billion |

| Growth Rate | 8.2% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | South32, Anglo American plc, Eramet, Manganese Metal Company (MMC), Tronox Holdings plc, Tesla, Inc. (indirectly through supply agreements), Vedanta Resources, Vale S.A., Manganin, American Manganese Inc., Mesa Minerals Limited, China Minmetals Corporation, Xiangtan Electrochemical Scientific, CITIC Dameng, Guangxi Nonferrous Metals Group, Maxeon, Sibelco, Tosoh Corporation, Euro Manganese Inc., Tanco Manganese Mine. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Manganese Market is undergoing a rapid evolution, primarily driven by the need to increase purity levels for battery applications and to enhance sustainability in mining and processing operations. In metallurgical applications, ongoing refinements focus on optimizing smelting furnace designs and utilizing advanced process control systems (often AI-assisted) to reduce energy consumption per ton of ferroalloy produced. Innovations in pre-treatment of lower-grade ores, such as improved sintering and pelletizing techniques, aim to increase yield and reduce the carbon intensity of traditional smelting processes, addressing mounting regulatory pressure from entities like the European Union's Carbon Border Adjustment Mechanism (CBAM).

The most significant technological advancements are concentrated within the chemical and battery-grade segment. Traditional production of EMD often relies on energy-intensive electrolytic processes. Newer hydrometallurgical routes are being commercialized for the direct production of HPMSM from manganese ore or even recycled sources. These advanced leaching and solvent extraction technologies offer superior control over impurity removal, crucial for meeting the stringent specifications demanded by EV battery manufacturers. The development of direct-to-cathode material production, bypassing intermediate chemical forms, is a key focus area, promising efficiency gains and cost reduction in the critical path from mine to EV cell.

Furthermore, technology related to resource efficiency and circular economy principles is gaining traction. This includes research into effective recycling methods for manganese from spent lithium-ion and alkaline batteries, though manganese recovery remains technically and economically challenging compared to nickel and cobalt. Companies are investing in proprietary leaching chemistries and separation techniques to make manganese recycling viable at scale. Simultaneously, in the mining sector, the adoption of digital technologies, remote monitoring, and automated fleet management is enhancing operational safety and reducing environmental impact, crucial for maintaining social license to operate in politically sensitive regions.

The Manganese Market exhibits pronounced regional disparities concerning resource availability, processing capability, and consumption patterns, which fundamentally shape global trade dynamics. Asia Pacific (APAC) holds the dual distinction of being the largest consumer and the principal processing hub, largely due to China's dominant position in global steel production (accounting for approximately 50% of worldwide output) and its established, highly scaled capacity for manufacturing ferroalloys, EMM, EMD, and HPMSM. The region also includes significant producers like Australia and India, who possess substantial ore reserves and increasingly sophisticated domestic processing industries, catering to burgeoning local automotive and construction demand. Investment in South Korea and Japan is primarily directed towards securing long-term contracts for high-purity materials to fuel their respective large-scale battery manufacturing ecosystems.

Africa, specifically the Southern Africa region (South Africa, Gabon), remains indispensable as the global cornerstone of manganese ore supply, holding the vast majority of the world's accessible, high-grade reserves. South Africa alone accounts for a substantial percentage of global production, making the region's political stability, regulatory framework, and logistical infrastructure crucial determinants of global supply security and price stability. However, the continent primarily operates in the upstream segment, exporting ore, meaning minimal value addition occurs locally. This dynamic drives international strategic efforts to ensure reliable transport links from interior mines to coastal ports, which frequently face capacity constraints and operational challenges.

North America and Europe, while possessing limited high-grade reserves compared to Africa and Australia, are aggressively focusing on midstream processing capacity development, driven by governmental mandates aimed at critical raw material independence and supply chain localization (e.g., the U.S. Inflation Reduction Act and the E.U. Critical Raw Materials Act). These regions are prioritizing the establishment of facilities capable of converting imported manganese ore into battery-grade HPMSM and EMD, aiming to bridge the gap between mining and final battery manufacturing and reduce reliance on APAC processing. This strategic push is creating significant demand for technology transfer and investment in sustainable processing techniques compliant with stringent Western environmental standards.

The predominant driver is the global transition to Electric Vehicles (EVs) and the resultant exponential demand for lithium-ion batteries. High-purity manganese, specifically HPMSM (High-Purity Manganese Sulfate Monohydrate), is essential for producing NCM and LMFP cathodes, which offer stability, safety, and reduced cost compared to cobalt-heavy alternatives, directly impacting EV range and affordability.

The steel industry remains the largest consumer by volume, typically accounting for over 90% of global manganese demand. Manganese is indispensable as a key deoxidizer and desulfurizer, and as an alloying element that enhances the strength, hardness, and durability of virtually all commercial steel grades used in construction and infrastructure.

South Africa is the overwhelming leader in global manganese ore reserves and production, followed by Australia, Gabon, and Brazil. This high concentration of supply in a few geographical regions creates inherent geopolitical risks and supply chain vulnerabilities, prompting consumer nations to seek diversification and localized processing.

Electrolytic Manganese Metal (EMM) is a refined product used mainly in specialized steel, aluminum alloys, and some traditional battery chemistries. High-Purity Manganese Sulfate Monohydrate (HPMSM) is a chemical compound produced through further advanced processing (often hydrometallurgy) tailored specifically to meet the extremely strict purity requirements (99.9%+) for modern lithium-ion battery cathode production.

Key challenges include the high energy consumption and greenhouse gas emissions associated with ferroalloy smelting and electrolytic processing, significant water usage in mining, and the necessity of ensuring responsible sourcing, particularly concerning labor practices and environmental remediation in developing mining nations like South Africa and Gabon.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.