ID : MRU_ 443546 | Date : Feb, 2026 | Pages : 243 | Region : Global | Publisher : MRU

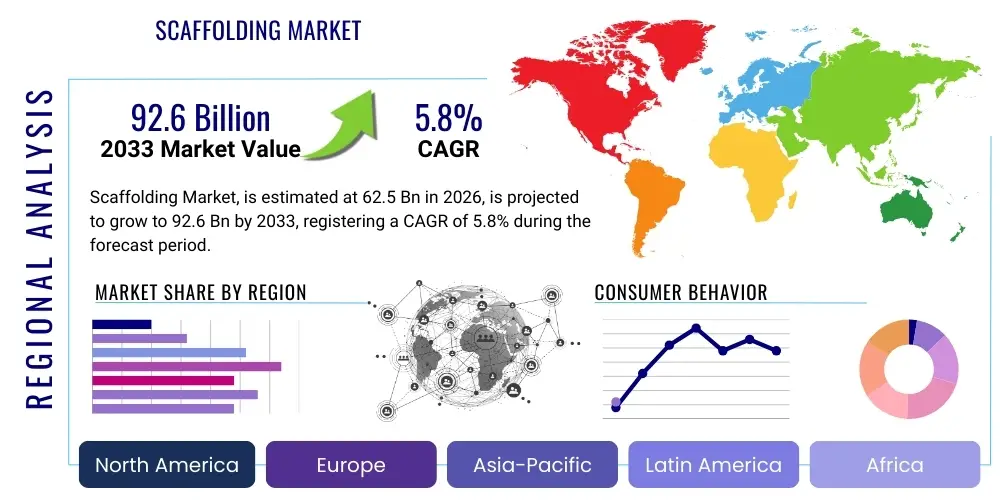

The Scaffolding Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 62.5 Billion in 2026 and is projected to reach USD 92.6 Billion by the end of the forecast period in 2033.

This robust expansion is primarily driven by escalating global infrastructure spending, particularly in emerging economies focused on rapid urbanization and public works. Developing nations are witnessing unprecedented construction activity in residential, commercial, and industrial sectors, necessitating reliable and high-capacity temporary access structures. Furthermore, stringent safety regulations worldwide mandate the use of certified and modern scaffolding systems, replacing outdated or less secure methods, thereby supporting market revenue growth across mature and emerging markets.

The Scaffolding Market encompasses the provision, rental, sale, and erection of temporary structures used to support work crews and materials during the construction, maintenance, or repair of buildings and other man-made structures. Key products include modular, supported, suspended, and rolling scaffolds, fabricated primarily from materials such as steel, aluminum, and sometimes fiberglass or composite materials. Major applications span the entirety of the construction industry, including large-scale civil engineering projects (bridges, dams), commercial high-rise development, residential housing, and extensive industrial maintenance, particularly in the oil and gas or manufacturing sectors. The inherent flexibility and necessity of scaffolding for safe, elevated access underscore its indispensable role in the global construction value chain.

The primary benefits of modern scaffolding systems include dramatically improved worker safety, enhanced operational efficiency through organized access, and compliance with increasingly stringent occupational health and safety standards (OHS). Driving factors for market growth include demographic shifts leading to increased housing demand, government investment in infrastructure upgrades (e.g., smart city projects, railway expansion), and the cyclical nature of renovation and refurbishment activities in developed economies. Technological advancements, such as the introduction of lightweight alloys and digital modeling for scaffold design, are further contributing to market dynamism and efficiency.

Despite being a mature industry, innovation remains crucial, focusing on ease of assembly, durability, and integration with modern Building Information Modeling (BIM) processes. The shift toward specialized systems like mobile scaffolding or mast climbing work platforms (MCWPs) in specific applications reflects the industry's continuous effort to optimize access solutions. Overall market performance is highly correlated with global GDP growth and capital expenditure in the real estate and infrastructure sectors, positioning scaffolding as a vital enabling segment for global economic activity.

The Scaffolding Market is characterized by intense regional competition and a pronounced shift toward rental models due to high upfront costs associated with purchasing complex systems, particularly among smaller contractors. Business trends indicate a strong move toward standardization and modularity, which facilitates quicker assembly, reduces labor costs, and improves system reuse across multiple projects. Furthermore, safety and compliance are no longer just regulatory necessities but key competitive differentiators, pushing major vendors to invest heavily in training, certification, and robust quality assurance processes for their products. Digital transformation is beginning to permeate the sector through inventory management, drone-based inspection, and augmented reality tools for assembly guidance, optimizing project timelines significantly.

Regionally, Asia Pacific (APAC) stands out as the engine of growth, fueled by massive urbanization projects in India, China, and Southeast Asian nations, leading to unprecedented demand for basic and modular steel scaffolding. North America and Europe, while slower in new construction growth, exhibit high demand for sophisticated systems like access towers and suspended platforms, driven by refurbishment activities and stringent labor safety laws that necessitate high-quality, certified aluminum and system scaffolding. The Middle East and Africa (MEA) market shows fluctuating demand, strongly tied to large-scale, government-funded projects, particularly in Saudi Arabia and the UAE, emphasizing heavy-duty industrial scaffolding for energy infrastructure.

In terms of segmentation, the system scaffolding segment (e.g., Ringlock and Cuplock) is experiencing the fastest adoption rate, valued for its load-bearing capacity and versatility compared to traditional tube and coupler systems. The industrial application segment, encompassing refineries, power plants, and maritime structures, provides the highest margin opportunities due to the specialized nature and complex safety requirements of the equipment used. Material trends suggest a steady increase in the utilization of lightweight aluminum, particularly in regions where labor costs are high and ease of transport is prioritized, although steel remains the dominant material globally due to its cost-effectiveness and durability.

User queries regarding AI in the Scaffolding Market predominantly revolve around three key themes: how AI can enhance site safety and risk assessment, its role in optimizing complex scaffold design and inventory logistics, and the potential for automated inspection protocols. Users are keen to understand if AI-driven analysis of structural data (gathered via sensors or drones) can predict failure points or misuse patterns before accidents occur. There is also significant interest in how machine learning algorithms can streamline the bidding and planning process by accurately estimating material needs and optimal assembly sequences based on project specifications, minimizing waste and delays inherent in traditional manual planning.

AI is set to revolutionize the way scaffolding planning and site operations are managed. Through the integration of computer vision and machine learning models, construction companies can deploy smart cameras and drone technology to continuously monitor erected scaffolding for compliance with safety standards, detecting unauthorized modifications, missing components, or overloading in real-time. This predictive maintenance approach drastically reduces occupational hazards and ensures regulatory adherence, transforming safety from a reactive measure to a proactive, continuously optimized process. Furthermore, AI-powered BIM tools can generate optimal scaffold blueprints, considering factors like wind load, material availability, and worker access paths more efficiently than human planners.

Beyond safety and design, AI applications extend deeply into supply chain management. Machine learning algorithms can analyze historical project data, supplier lead times, and current demand fluctuations to provide predictive insights for scaffold rental companies and suppliers, ensuring optimal inventory levels and minimizing logistics bottlenecks. This level of optimization translates directly into reduced project costs and improved profitability for both the scaffolding provider and the general contractor. While the physical erection process remains labor-intensive, AI is positioned to be the critical intelligence layer managing the entire lifecycle of the temporary structure, from initial design optimization to final dismantle verification.

The dynamics of the Scaffolding Market are governed by a complex interplay of Drivers, Restraints, and Opportunities, collectively summarized as DRO & Impact Forces. The primary driver is the accelerating pace of global construction and infrastructure development, supported by government investments aimed at boosting economic recovery and enhancing connectivity. Conversely, the market faces significant restraints, chiefly the inherent volatility of raw material prices (steel and aluminum) and the persistent challenge of ensuring skilled labor availability for safe assembly and dismantling. Opportunities are vast, particularly through technological integration, such as the adoption of advanced materials (composites) and digital solutions (BIM, robotics), which address long-standing issues of efficiency and labor dependency. These forces exert considerable impact, pushing the industry toward safer, more standardized, and technologically integrated solutions.

Key drivers include increasingly stringent regulatory environments globally, especially in mature markets like North America and Western Europe, where occupational safety bodies impose high standards for temporary work platforms, thereby promoting the adoption of certified system scaffolding over traditional methods. Furthermore, the growth in energy and industrial sectors, including maintenance and retrofitting of aging facilities (e.g., power plants, refineries), necessitates specialized, durable, and heavy-duty scaffolding solutions, maintaining demand even during cyclical downturns in residential construction. The rapid growth of megacities in Asia and Africa acts as a perpetual demand generator for high-volume, cost-effective access systems.

Major restraints involve the significant capital investment required for large-scale rental inventory and the logistical complexities associated with transporting, managing, and maintaining vast quantities of specialized components across diverse project sites. The cyclical nature of the construction industry often leads to unpredictable demand, complicating inventory planning for rental businesses. However, opportunities abound in developing markets where localized manufacturing and training can address supply chain gaps. The rise of automation in logistics and site management, coupled with the potential for recycling and repurposing older materials, offers compelling pathways for future cost reduction and sustainability improvements across the scaffolding ecosystem.

The Scaffolding Market is segmented based on critical parameters including Type (Supported, Suspended, Rolling, etc.), Material (Steel, Aluminum, Wood, Others), Application (Construction, Industrial, Residential), and End-User (Rental Companies, Contractors, Others). Supported scaffolding, which includes system and modular types, dominates the market share due to its versatility, stability, and widespread application across most construction projects. The Material segment is predominantly controlled by steel due to its high load capacity and economic pricing, though aluminum is gaining traction in niche markets requiring reduced weight and quick assembly, especially for façade work and aircraft maintenance.

The application segmentation highlights the construction sector as the largest consumer, driven by continuous infrastructure investment. However, the industrial segment is characterized by higher value per project, requiring specialized and often custom-engineered scaffolding for complex maintenance tasks in environments with high heat, chemical exposure, or limited access. Rental companies form the backbone of the market's distribution structure, holding the majority of the inventory and offering flexible solutions to contractors who prefer operational expenditure over capital investment. This widespread preference for rental services ensures a stable revenue stream for large scaffolding providers.

Strategic segmentation allows market players to tailor their product offerings and services. For instance, focusing on the system scaffolding segment with robust training and certification programs targets high-growth, high-safety-compliance regions like North America and Europe. Conversely, targeting the residential segment in emerging Asia Pacific markets often involves prioritizing cost-effective, standard supported scaffolding solutions. Understanding the interplay between material selection and application requirements is vital for capitalizing on regional economic activity and specialized industry demands.

The Scaffolding Market value chain is initiated at the upstream stage with raw material procurement, primarily steel and aluminum manufacturers, which determines the fundamental cost structure of the end product. Key activities in the upstream segment include sourcing high-grade alloys, ensuring material certification, and negotiating bulk purchases to maintain competitive pricing. Given the reliance on commodities, price volatility in metal markets significantly impacts the profitability of downstream manufacturers. Efficient material management and strategic supplier relationships are crucial for mitigating supply chain risks and ensuring continuous production of components that meet global tensile strength and quality standards.

The midstream section involves the core manufacturing process, where raw materials are transformed into standardized scaffolding components (e.g., tubes, couplers, frames, ledgers). This stage involves high precision engineering, welding, galvanization (for steel), and rigorous quality testing. Manufacturers often specialize in specific types, such as system scaffolding (Ringlock, Cuplock) or specialized industrial access solutions. The distribution channel plays a critical intermediate role, linking manufacturers to end-users. Direct distribution often involves large manufacturers selling directly to major EPC (Engineering, Procurement, and Construction) firms or national rental chains, ensuring large-volume transactions and customized services.

Downstream activities are dominated by rental services, which represent the primary business model globally. Rental companies purchase inventory, manage logistics, and provide erection and dismantling services, often bundled with engineering consultation and safety audits. Indirect distribution involves smaller regional distributors or local hardware stores supplying smaller contractors or individual projects. The market is ultimately driven by the efficiency and safety of the erection and dismantling services provided by skilled labor, as the value proposition shifts from the physical product itself to the temporary access solution provided, making after-sales service and technical support essential components of the downstream value proposition.

Potential customers for scaffolding systems are diverse, encompassing the entire spectrum of the built environment and industrial operations where elevated or temporary access is required. The largest and most frequent buyers, though often indirect, are large EPC companies and general construction contractors engaged in commercial, infrastructure, and high-rise residential projects. These entities require comprehensive, reliable, and standardized system scaffolding solutions in large quantities, often preferring long-term rental contracts that include engineering planning and technical on-site support to minimize their capital expenditure and operational risks. Speed of deployment and adherence to strict project deadlines are paramount concerns for this customer segment.

A second major customer category includes industrial facility owners and operators, particularly those in the oil and gas, petrochemical, power generation, and maritime industries. These customers require highly specialized scaffolding for planned shutdowns, maintenance, and emergency repairs. Their needs often lean towards non-corrosive materials (like aluminum or fiberglass), systems designed for confined spaces, or structures that can withstand extreme environmental conditions. For these industrial applications, the primary purchasing criteria focus heavily on material specifications, safety certifications, and the provider's proven track record in complex industrial environments, often prioritizing quality and specialization over minimal cost.

Finally, scaffolding rental companies themselves are major purchasers of new equipment from manufacturers. These companies act as the primary intermediary, buying inventory in bulk to service a vast network of smaller local contractors and residential builders who cannot justify owning the equipment. Residential builders typically require basic frame and aluminum rolling scaffolds, favoring solutions that are easy to transport and set up. The success of manufacturers is intrinsically tied to the procurement cycles and expansion strategies of these large rental fleet operators who consistently upgrade and increase their inventory to maintain market competitiveness and safety standards.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 62.5 Billion |

| Market Forecast in 2033 | USD 92.6 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Layher GmbH & Co KG, BrandSafway, ULMA Group, Altrad Group, PERI GmbH, Waco International, Sunshine Enterprise, Inc., Safway Group Holdings LLC, AT-PAC, HAKI AB, Tianbao Steel Pipe Co., Ltd., Instant UpRight, G.D.O. S.p.A., ADTO Group, Pilosio Group, Atlantic Pacific Equipment, Stepup Scaffold, Doka GmbH, MJ-Gerüst GmbH, Scafom-rux. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Scaffolding Market is evolving from purely mechanical structures towards integrated, smarter systems designed for enhanced safety, rapid deployment, and reduced operational footprint. One major technological shift involves the increasing adoption of advanced material science, specifically the use of high-strength, low-weight aluminum alloys and composite materials (like fiberglass reinforced plastics). These materials are crucial for applications where weight restriction, non-conductivity (e.g., electrical work), or resistance to corrosion (e.g., offshore platforms) is paramount. This move addresses the ongoing industry challenge of improving transportation logistics and minimizing worker fatigue associated with lifting heavy components, ultimately improving assembly times and safety compliance, though the cost barrier remains a consideration for widespread adoption.

Digitalization is rapidly transforming planning and management processes within the market. The integration of Building Information Modeling (BIM) software is critical, allowing contractors and scaffold designers to create precise 3D models of the scaffold structure overlaid onto the main project model. This facilitates clash detection, ensures structural integrity against project loads and wind factors, and generates accurate material lists, significantly reducing errors and waste during both design and erection phases. Furthermore, IoT sensors and RFID tags are being implemented on scaffolding components. These technologies allow rental companies to track inventory location, monitor usage duration, and schedule necessary maintenance, enhancing asset utilization and reducing loss rates across complex, large-scale projects globally.

A burgeoning area of technology is Smart Scaffolding and Remote Monitoring. This involves equipping scaffold structures with sensors that monitor structural health parameters such as load, inclination, and displacement in real-time. Data captured is analyzed using cloud-based platforms to alert site managers instantly to potential safety breaches or excessive load stress, thereby preventing accidents. Furthermore, the use of drones for automated inspection is gaining significant momentum. Drones equipped with high-resolution cameras and thermal imaging capabilities can quickly and safely inspect large, complex scaffolds for compliance and damage without requiring human workers to climb the full structure, drastically cutting inspection time and mitigating inherent risks associated with high-altitude work.

Asia Pacific (APAC): Dominance in Volume and Growth

The APAC region is the undisputed leader in the global Scaffolding Market, commanding the largest market share primarily due to the intense pace of urbanization and the sheer scale of infrastructure investment, particularly in China, India, and Southeast Asian countries. Government initiatives focused on developing smart cities, expanding transportation networks (high-speed rail, ports), and addressing massive residential housing shortages are the core drivers of scaffolding demand. While traditional steel tube and coupler systems remain highly popular due to their cost-effectiveness, rising awareness regarding worker safety and the influx of international construction firms are steadily promoting the adoption of modular system scaffolding (e.g., Ringlock). The market here is volume-driven, with significant emphasis on manufacturing localization and competitive pricing strategies.

However, the APAC region faces challenges related to inconsistent safety regulation enforcement across various developing nations, which can sometimes slow the adoption of higher-quality, more expensive certified systems. India and Indonesia, in particular, represent immense potential, characterized by burgeoning construction pipelines. The trend in APAC is toward hybrid solutions: combining cost-effective steel basic frames for external structure access with advanced system scaffolding for specialized, high-load bearing applications within the structure itself. The rapid industrial expansion, especially in automotive and heavy manufacturing, further ensures sustained demand for maintenance access solutions.

North America: Focus on Safety, Aluminum, and Rentals

North America is characterized by mature construction practices, extremely stringent occupational health and safety (OHS) standards, and a predominant reliance on the rental model. The market here places a premium on efficiency, safety features, and quality certification (OSHA compliance). Aluminum scaffolding, despite its higher initial cost, holds a significant market share due to its lightweight nature, which reduces labor costs and speeds up erection/dismantling—critical factors given high labor costs in the US and Canada. Demand is driven less by entirely new residential construction, which is cyclical, and more by large-scale commercial real estate development, infrastructure rehabilitation (e.g., bridge repair), and industrial retrofitting projects.

Technological adoption, including advanced BIM integration and the early deployment of smart scaffolding components for real-time monitoring, is highest in North America. The competitive landscape is dominated by large national and international rental corporations that leverage sophisticated logistics and extensive inventory to service complex, multi-state projects. The aging infrastructure across the region necessitates continuous maintenance access solutions, guaranteeing a resilient demand base regardless of fluctuations in new building starts.

Europe: High Standardization and System Scaffolding Leadership

Europe is defined by its rigorous safety standards (e.g., EN standards), high standardization levels, and the widespread use of sophisticated system scaffolding (e.g., Layher, PERI systems). The focus on worker protection and environmental sustainability is stronger than in other regions, driving innovation in modular design for reusability and reduced waste. The demand is largely stable, fueled by the conservation and restoration of historical buildings, ongoing energy sector maintenance, and moderate commercial development. Germany, the UK, and France are the key markets, characterized by highly organized rental industries and a focus on specialized access solutions like facade scaffolding and weather protection systems.

The European market leads in the development and adoption of high-tech access solutions, including Mast Climbing Work Platforms (MCWPs) and specialized suspended platforms, especially in urban areas where ground footprint minimization is necessary. The trend towards prefabricated modules and integrated safety components reflects the region's priority on minimizing on-site construction time and maximizing worker efficiency. Sustainability initiatives are beginning to influence material selection, encouraging the use of highly recyclable materials and designs optimized for long service life.

Latin America (LATAM): Growth Driven by Infrastructure Needs

The Latin American market is highly fragmented but shows significant growth potential, tightly linked to macroeconomic stability and governmental investment in public infrastructure. Countries like Brazil, Mexico, and Chile are witnessing increasing demand for scaffolding due to mining operations, energy projects, and urbanization efforts. While cost remains a significant determinant, driving the use of basic tube and coupler systems, there is a growing trend toward adopting imported or licensed system scaffolding, primarily in major cities and projects backed by foreign investment, where international safety standards are enforced.

Challenges in LATAM include logistical complexities, varying levels of regulatory enforcement, and economic instability that can halt or delay major construction projects. However, the pressing need for housing and improved transportation infrastructure provides a strong underlying driver. Market participants often focus on forming strategic partnerships with international firms to gain access to modern technology and standardized training, aiming to bridge the gap between low-cost traditional methods and high-safety modular systems.

Middle East and Africa (MEA): Project-Based Volatility and Specialized Demand

The MEA market, particularly the Gulf Cooperation Council (GCC) states (Saudi Arabia, UAE, Qatar), is project-centric, meaning demand for scaffolding can experience high volatility based on the timeline and scale of government-funded mega-projects (e.g., Neom, Expo-related construction). These projects typically demand vast quantities of heavy-duty, certified system scaffolding, often requiring specialized designs for extreme heat and desert environments. The region is a major consumer of industrial scaffolding for its massive oil, gas, and petrochemical complexes, where safety and explosion-proof specifications are critical.

The African segment is highly nascent, with growth concentrated in South Africa and Nigeria, driven by resource extraction and rapidly developing commercial hubs. While African markets primarily rely on basic, cost-effective steel scaffolding, the Middle East represents a premium market focused on quality, speed, and large-scale, complex access requirements for iconic architecture. Logistics management and the mobilization of massive temporary inventories are key operational challenges and competitive factors in the GCC states.

The choice is driven by project requirements concerning load capacity, weight, and assembly speed. Steel scaffolding offers superior load-bearing capacity and cost-effectiveness, dominating high-rise and heavy industrial construction. Aluminum scaffolding is favored for its lightweight properties, corrosion resistance, and ease of assembly, making it ideal for maintenance, façade work, and projects where labor efficiency is prioritized.

Strict safety regulations, such as OSHA and European EN standards, are significantly driving the shift away from traditional tube and coupler systems toward certified modular (system) scaffolding, like Ringlock and Cuplock. These systems offer integrated safety features, standardized connections, and certified load tables, drastically reducing the risk of structural failure and non-compliance fines.

The rental model is overwhelmingly prevalent globally, particularly among small to medium-sized contractors. Rental offers flexibility, reduces the need for large capital expenditure, minimizes maintenance and storage costs for the contractor, and ensures the use of equipment that meets the latest safety standards, which are managed by the rental fleet operators.

Key technological advancements include the integration of BIM for precise design modeling, the use of IoT sensors for real-time load and structural health monitoring (Smart Scaffolding), and the deployment of drones for automated safety inspection and rapid progress verification across large construction sites.

The Asia Pacific (APAC) region is expected to lead market growth throughout the forecast period due to large-scale, sustained government investment in infrastructure, rapid urbanization, and a continuous requirement for high-volume residential and commercial construction, particularly in developing economies like India and Southeast Asia.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.