ID : MRU_ 430309 | Date : Nov, 2025 | Pages : 255 | Region : Global | Publisher : MRU

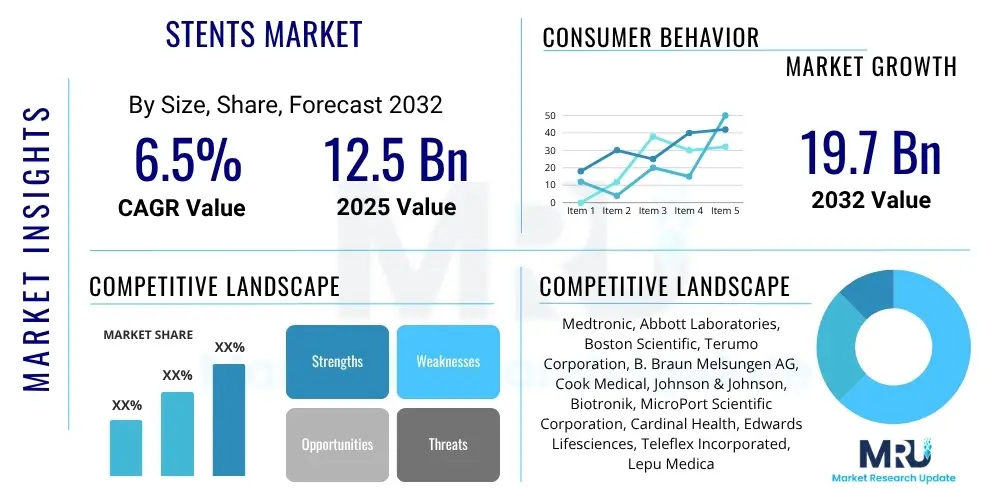

The Stents Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2032. The market is estimated at $12.5 Billion in 2025 and is projected to reach $19.7 Billion by the end of the forecast period in 2032.

The global Stents Market encompasses a broad range of medical devices designed to open and maintain the patency of narrowed or blocked bodily passageways, primarily blood vessels. These small, expandable tubes are crucial in treating various cardiovascular diseases, peripheral artery diseases, and conditions affecting other bodily conduits such as the esophagus, trachea, and biliary ducts. Initially developed as bare-metal structures, stents have evolved significantly with the introduction of drug-eluting stents (DES) and, more recently, bioresorbable stents (BRS), which offer enhanced therapeutic benefits and reduce long-term complications.

Major applications of stents include coronary interventions to restore blood flow to the heart, peripheral vascular interventions to treat blockages in limbs, and non-vascular procedures for conditions like esophageal strictures or biliary obstructions. The primary benefit of stent implantation is the immediate restoration of luminal patency, alleviating symptoms, preventing further tissue damage, and improving patient outcomes. This minimally invasive approach reduces recovery times compared to traditional open surgeries, making it a preferred treatment option for many patients globally. The continuous advancements in material science, coating technologies, and delivery systems further augment the efficacy and safety profile of modern stents.

Driving factors for the Stents Market include the escalating global prevalence of cardiovascular diseases (CVDs), an expanding geriatric population prone to age-related vascular conditions, and increasing awareness coupled with improved diagnostic capabilities. Furthermore, technological innovations leading to more biocompatible materials, advanced drug elution platforms, and patient-specific stent designs are continually expanding the therapeutic scope and market penetration. The growing adoption of minimally invasive surgical procedures across various medical disciplines also significantly contributes to the robust growth trajectory of the stent industry.

The Stents Market is currently experiencing dynamic shifts driven by significant business trends, evolving regional demands, and progressive segment developments. Business trends indicate a strong focus on research and development, particularly in creating next-generation stents that offer improved biodegradability, enhanced drug delivery, and smart features for better patient monitoring. Mergers and acquisitions are frequent as companies seek to consolidate market share, acquire advanced technologies, and expand their product portfolios. A key trend is the increasing collaboration between medical device manufacturers and biotechnology firms to integrate novel materials and biological agents into stent design, aiming for long-term clinical superiority and reduced adverse events.

Regionally, mature markets in North America and Europe continue to dominate due to established healthcare infrastructures, high adoption rates of advanced medical technologies, and a significant burden of chronic diseases. However, the Asia Pacific region, including countries like China and India, is emerging as a critical growth engine. This surge is fueled by rapidly improving healthcare access, increasing disposable incomes, a large patient pool, and government initiatives aimed at expanding medical tourism and upgrading healthcare facilities. Latin America and the Middle East and Africa also show promising growth, driven by increasing awareness, growing medical tourism, and investments in healthcare infrastructure development, though these regions still face challenges related to affordability and access.

Segment trends highlight the continued dominance of drug-eluting stents (DES) due to their superior efficacy in preventing restenosis compared to bare-metal stents (BMS). However, the bioresorbable stent (BRS) segment is poised for significant acceleration, driven by the promise of transient scaffolding and the restoration of natural vessel function without leaving permanent foreign material. Within applications, coronary stents maintain the largest share, but peripheral stents are gaining substantial traction due to the rising prevalence of peripheral artery disease (PAD) and diabetes-related complications. The end-user segment sees hospitals as the primary consumers, yet ambulatory surgical centers (ASCs) are increasingly becoming important due to their cost-effectiveness and efficiency for elective procedures.

The integration of Artificial Intelligence (AI) into the Stents Market is poised to address several key themes and expectations concerning enhanced precision, personalized treatment, and operational efficiency. Users are keenly interested in how AI can improve diagnostic accuracy for identifying vascular lesions, optimize stent sizing and placement through predictive modeling, and offer real-time guidance during interventional procedures. There are significant expectations for AI to minimize procedural complications, reduce radiation exposure, and ultimately lead to superior long-term patient outcomes by providing data-driven insights at every stage, from initial diagnosis to post-procedural follow-up. Concerns often revolve around data privacy, the validation of AI algorithms in diverse patient populations, and the integration challenges within existing clinical workflows, yet the overwhelming sentiment points towards AI as a transformative force.

AI's influence is expected to span the entire product lifecycle and clinical application of stents. In the initial stages, AI algorithms can analyze complex patient data, including imaging and physiological parameters, to predict the risk of disease progression and identify optimal candidates for stenting. During the procedure, AI-powered image analysis tools can provide detailed anatomical insights, guiding clinicians in selecting the most appropriate stent size and type, thereby reducing the chances of suboptimal placement or vessel injury. Post-procedure, AI can monitor patient recovery, predict potential complications like restenosis or thrombosis, and suggest personalized follow-up care plans. This comprehensive impact underscores AI's potential to elevate the standard of care in interventional cardiology and other stent-related specialties, moving towards a more predictive, preventive, and personalized medicine paradigm.

The Stents Market is shaped by a complex interplay of various driving forces, significant restraints, and emerging opportunities, all contributing to its overall impact dynamics. Key drivers include the ever-increasing global incidence of cardiovascular diseases (CVDs) such as coronary artery disease and peripheral artery disease, which necessitates a high volume of interventional procedures. The continuously expanding aging population worldwide, inherently more susceptible to vascular pathologies, further amplifies the demand for stent-based treatments. Moreover, persistent technological advancements in stent design, materials science, and drug-eluting capabilities have significantly improved clinical outcomes, making stenting a more attractive and effective option, thereby fueling market expansion. The growing preference for minimally invasive surgical procedures due to shorter recovery times and reduced patient morbidity also acts as a powerful market accelerator.

Conversely, the market faces several notable restraints. The high cost associated with advanced drug-eluting and bioresorbable stents, especially in developing economies, can limit their widespread adoption and accessibility. Risks inherent to stent implantation, such as in-stent restenosis (re-narrowing of the vessel) and stent thrombosis (blood clot formation), although mitigated by newer designs, remain clinical challenges that can deter some patients and clinicians. Furthermore, the stringent and lengthy regulatory approval processes for new stent technologies can delay market entry and increase development costs. The presence of alternative treatment options, including bypass surgery for severe cases or pharmacological management for less critical conditions, also presents a competitive restraint on the stent market's growth potential.

Despite these challenges, substantial opportunities exist to propel the Stents Market forward. The ongoing research and development in bioresorbable stents, which dissolve after restoring vessel patency, promises to eliminate the long-term presence of foreign material and associated complications, opening up new therapeutic avenues. Similarly, the advent of smart stents equipped with sensors for real-time monitoring of physiological parameters presents a revolutionary opportunity for personalized medicine. Geographic expansion into emerging economies with improving healthcare infrastructures, rising disposable incomes, and a growing burden of lifestyle diseases offers significant untapped market potential. The increasing integration of artificial intelligence and machine learning in optimizing stent design, improving procedural precision, and enhancing post-procedural patient management also represents a transformative opportunity for innovation and market growth.

The global Stents Market is extensively segmented based on several key parameters including product type, material type, application, and end-user, providing a granular view of market dynamics and potential growth areas. This detailed segmentation allows for a comprehensive understanding of diverse market needs, technological preferences, and adoption patterns across different clinical settings and patient populations. Each segment exhibits unique characteristics driven by factors such as disease prevalence, technological maturity, regulatory landscape, and healthcare infrastructure, influencing purchasing decisions and market share distribution.

Analyzing these segments reveals critical insights into market evolution. For instance, the product type segmentation highlights the shift from conventional bare-metal stents to advanced drug-eluting stents, and the emerging potential of bioresorbable stents. Material type differentiation underscores the importance of biocompatibility and mechanical properties, with metallic and polymeric stents addressing various clinical requirements. Application-based segmentation emphasizes the dominance of cardiovascular interventions while also recognizing the growth in peripheral and non-vascular stent uses. End-user analysis distinguishes between primary care settings like hospitals and specialized facilities such as ambulatory surgical centers, reflecting the diverse channels through which stent procedures are performed. This layered approach is vital for stakeholders to identify lucrative niches and tailor their strategies effectively.

The value chain for the Stents Market is characterized by several critical stages, beginning with the upstream supply of specialized raw materials. This upstream segment involves suppliers of high-grade metallic alloys such as cobalt-chromium, platinum-chromium, and nitinol, along with advanced polymers, both biodegradable and non-biodegradable, which form the foundational components of stent construction. These raw material providers must adhere to stringent quality and purity standards to ensure the biocompatibility, mechanical integrity, and overall safety of the final medical device. Innovation in material science at this stage directly influences the performance characteristics and therapeutic potential of new stent generations, driving continuous research and development efforts among material suppliers to meet evolving industry demands for enhanced flexibility, strength, and drug elution properties.

Moving downstream, the value chain encompasses the sophisticated processes of stent manufacturing, assembly, and sterilization, which are often highly automated and require specialized engineering expertise. This stage also includes the integration of drug coatings for DES and the development of intricate delivery systems designed for minimally invasive procedures. Once manufactured, stents are distributed through a complex network to reach the end-users. The distribution channels for stents are typically multifaceted, involving both direct sales forces employed by major manufacturers and indirect channels comprising authorized distributors, wholesalers, and group purchasing organizations (GPOs). Direct sales allow manufacturers to maintain close relationships with key opinion leaders and large hospital systems, providing specialized training and immediate support.

Indirect distribution channels, on the other hand, often serve broader markets, including smaller hospitals and clinics, by leveraging established logistical networks and local market knowledge of distributors. These channels are crucial for market penetration in geographically diverse and emerging regions. The end-users of stents are predominantly hospitals, specialized cardiac and vascular centers, and increasingly, ambulatory surgical centers (ASCs), where interventional cardiologists, radiologists, and vascular surgeons perform the implantation procedures. The efficiency of the distribution network, coupled with the effectiveness of sales and marketing strategies, plays a pivotal role in ensuring timely product availability and broad market reach, ultimately influencing patient access to these vital medical devices and impacting competitive positioning within the global Stents Market.

The primary potential customers and end-users within the Stents Market are healthcare institutions and medical professionals who perform interventional procedures to treat vascular and non-vascular obstructions. This predominantly includes hospitals, which represent the largest segment of end-users due to their comprehensive facilities, emergency care capabilities, and high patient volumes for complex procedures such as coronary stenting. Within hospitals, the key buyers are interventional cardiologists, interventional radiologists, and vascular surgeons, who are directly involved in selecting, implanting, and managing stent therapies. Their purchasing decisions are influenced by clinical efficacy, patient safety profiles, product innovation, and cost-effectiveness, often guided by clinical guidelines and institutional protocols. Moreover, hospital purchasing departments and pharmacy and therapeutics (P&T) committees play a crucial role in procurement decisions, evaluating the overall value proposition of different stent products.

Beyond traditional hospital settings, ambulatory surgical centers (ASCs) are emerging as significant potential customers, particularly for elective and less complex peripheral vascular procedures. ASCs offer a cost-effective alternative to hospitals for certain interventions, appealing to both patients and payers. These centers also employ interventional specialists who are decision-makers in stent procurement. Specialty clinics focusing on specific conditions like gastroenterology, pulmonology, and urology also constitute an important customer segment for non-vascular stents, addressing needs related to esophageal, tracheal, or biliary obstructions. The increasing shift towards outpatient care and procedure-specific centers underscores the expanding customer base for stent manufacturers, necessitating tailored sales and marketing approaches to address the unique needs and procurement processes of these diverse end-user environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2025 | $12.5 Billion |

| Market Forecast in 2032 | $19.7 Billion |

| Growth Rate | CAGR 6.5% |

| Historical Year | 2019 to 2023 |

| Base Year | 2024 |

| Forecast Year | 2025 - 2032 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Medtronic, Abbott Laboratories, Boston Scientific, Terumo Corporation, B. Braun Melsungen AG, Cook Medical, Johnson & Johnson, Biotronik, MicroPort Scientific Corporation, Cardinal Health, Edwards Lifesciences, Teleflex Incorporated, Lepu Medical Technology, AMG International GmbH, Alvimedica, Cordis, Endologix, Shockwave Medical, Koninklijke Philips N.V., W. L. Gore & Associates |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Stents Market is characterized by a rapidly evolving technological landscape, driven by continuous innovation aimed at improving clinical outcomes, reducing complications, and expanding therapeutic applications. A foundational technology revolves around advanced material science, which dictates the stent's mechanical properties, biocompatibility, and long-term performance. This includes the development of sophisticated metallic alloys like cobalt-chromium and platinum-chromium for enhanced radial strength and radiopacity, as well as the pioneering use of biodegradable polymers for drug-eluting coatings and entirely bioresorbable stent scaffolds. These material advancements are crucial for achieving optimal vessel support while minimizing inflammation and promoting natural healing, forming the core of next-generation stent designs.

Another pivotal technological area is drug elution systems. Drug-eluting stents (DES) incorporate a polymeric coating that slowly releases anti-proliferative drugs to prevent restenosis, the re-narrowing of the artery. Recent innovations in DES technology focus on developing polymer-free designs or using biodegradable polymers that resorb after drug delivery, addressing concerns about long-term polymer persistence and associated inflammatory responses. Furthermore, advancements in stent delivery systems, including smaller profiles, enhanced flexibility, and improved trackability, are critical for navigating tortuous anatomies and ensuring precise placement during minimally invasive interventional procedures. These delivery system innovations directly contribute to procedural safety and success, reducing the risk of complications.

Emerging technologies like artificial intelligence (AI) and machine learning (ML) are beginning to play a transformative role, particularly in image analysis for optimal stent sizing and placement, predictive modeling for patient outcomes, and personalized treatment planning. Robotic-assisted systems are also gaining traction, offering enhanced precision and stability during complex stent implantations. Furthermore, the development of "smart stents" equipped with integrated sensors for real-time monitoring of physiological parameters such as blood flow or pressure represents a futuristic frontier. These technological advancements collectively aim to provide more effective, safer, and patient-centric solutions, continually pushing the boundaries of interventional medicine and solidifying the stent market's innovative trajectory.

The primary types of stents include Bare-Metal Stents (BMS), which are simple metallic scaffolds; Drug-Eluting Stents (DES), coated with medication to prevent re-narrowing; and Bioresorbable Stents (BRS), which dissolve over time after serving their purpose.

The Stents Market growth is driven by the increasing global prevalence of cardiovascular diseases, an expanding geriatric population, continuous technological advancements in stent design and materials, and the rising preference for minimally invasive surgical procedures.

AI impacts the Stents Market by enhancing diagnostic accuracy through advanced imaging analysis, optimizing stent sizing and placement with predictive analytics, providing real-time procedural guidance, and facilitating personalized treatment planning for better patient outcomes.

Beyond cardiovascular conditions, stents are widely used in non-vascular applications such as gastroenterology for esophageal or biliary strictures, pulmonology for tracheal blockages, and urology for ureteral obstructions, expanding their therapeutic utility.

Key challenges include the high cost of advanced stent technologies, potential risks of in-stent restenosis and thrombosis, stringent regulatory approval processes, and competition from alternative treatment options like bypass surgery or pharmacological interventions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.