ID : MRU_ 431994 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

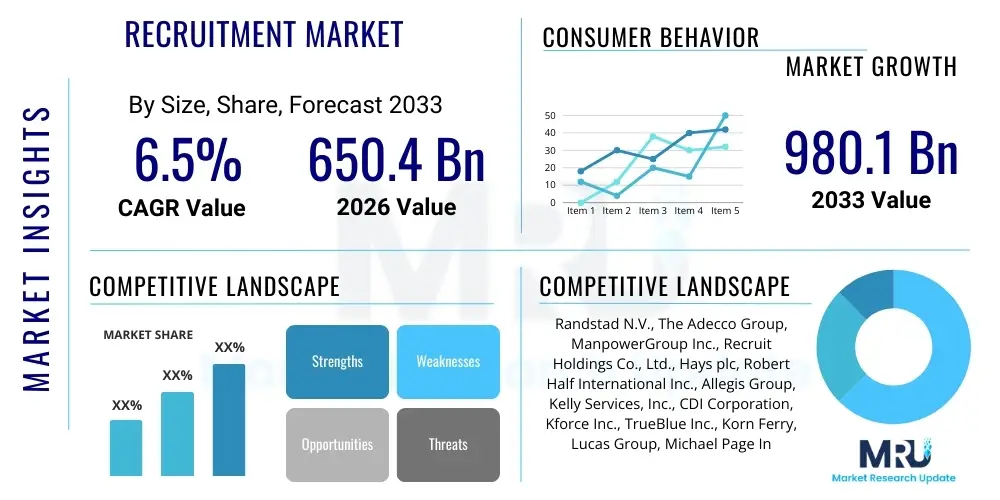

The Recruitment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033. The market is estimated at USD 650.4 Billion in 2026 and is projected to reach USD 980.1 Billion by the end of the forecast period in 2033.

The global recruitment market encompasses all activities and processes involved in sourcing, attracting, screening, selecting, and hiring qualified candidates for job openings within an organization. This vast ecosystem includes staffing agencies, executive search firms, recruitment process outsourcing (RPO) providers, job boards, and technology vendors supplying Applicant Tracking Systems (ATS) and sophisticated sourcing tools. The primary objective of the recruitment market is to bridge the talent gap experienced by businesses globally, ensuring that enterprises possess the specialized human capital necessary for innovation, expansion, and operational continuity. The recent shift towards flexible employment models, the explosive growth of the gig economy, and the heightened demand for niche technological skills are fundamentally reshaping the services offered by market participants, moving the industry away from purely transactional placements toward strategic talent advisory partnerships. Furthermore, the digitization of the workplace, accelerated by global events, has necessitated faster, more efficient, and often remote recruitment processes, bolstering the adoption of cloud-based solutions and integrated talent acquisition suites across various enterprise sizes and geographical locations, thereby driving market expansion and evolution.

Major applications of recruitment services span virtually every industry vertical, including Information Technology (IT) and Telecommunications, Healthcare, Banking, Financial Services, and Insurance (BFSI), Manufacturing, and Retail. In IT, recruitment focuses on securing specialized roles such as AI engineers, cybersecurity experts, and cloud architects, where talent scarcity is acute. For the healthcare sector, the emphasis is on high-volume nursing, specialized medical practitioners, and administrative staff, often requiring complex compliance screening. Key benefits derived from utilizing professional recruitment services include significant reductions in time-to-hire, improved quality of candidates, enhanced organizational diversity, and crucial cost savings associated with internal HR time allocation. The specialized expertise provided by external recruiters allows organizations to tap into passive candidate pools that are inaccessible through traditional job postings, ensuring a competitive edge in acquiring superior talent, which directly impacts organizational performance metrics such as productivity and innovation capability.

Driving factors propelling the market forward include intense global competition for specialized skills, the increasing complexity of regulatory compliance regarding employment laws across different jurisdictions, and the constant need for digital transformation initiatives across industries. Economic recovery in major developed and developing nations also stimulates hiring volumes across both permanent and contract roles. Moreover, technological advancements, particularly the integration of Artificial Intelligence and Machine Learning into sourcing and screening phases, are accelerating process efficiency and scalability, enabling recruiters to handle larger pipelines with greater precision. The persistent skill mismatch between available labor and required technical expertise across critical sectors ensures a sustained reliance on specialized recruitment firms capable of navigating these complex talent landscapes. These combined elements create a robust foundation for continuous market growth, cementing the role of professional recruitment services as essential strategic partners for modern businesses.

The global recruitment market is experiencing a period of profound transformation, marked by significant business model shifts towards technology integration and flexibility. Current business trends highlight the rapid adoption of Recruitment Process Outsourcing (RPO) by large enterprises seeking variable cost structures and specialized expertise in volume hiring, contrasting with the continued dominance of contingency staffing models for niche or immediate talent needs. The trend towards hyper-specialization, where firms focus exclusively on sectors like renewable energy or fintech, allows them to command higher fees due to unparalleled knowledge of specific talent pools and competitive compensation benchmarks. From a regional perspective, North America and Europe continue to lead the market in terms of technology spending and RPO adoption, driven by stringent labor requirements and the mature nature of their corporate ecosystems. Conversely, the Asia Pacific (APAC) region is demonstrating the fastest growth trajectory, fueled by rapid industrialization, massive infrastructure projects, and the expansion of global IT service centers, particularly in India and Southeast Asia, creating immense demand for scalable recruitment solutions and high-volume permanent placements. Segment trends indicate a clear preference for cloud-based Applicant Tracking Systems (ATS) over traditional on-premise solutions due to scalability and lower upfront investment costs, while the temporary staffing segment is outperforming permanent placement growth in many developed markets, reflecting employers' desire for workforce agility and reduced fixed labor costs in uncertain economic conditions. The overall market narrative is defined by the duality of human expertise combined with algorithmic efficiency, moving recruitment from a primarily transactional service to a data-driven, strategic business function.

Common user questions regarding AI's impact on the recruitment market typically center on themes of job displacement, fairness/bias in algorithms, and the measurable return on investment (ROI) of adopting AI tools. Users frequently inquire, "Will AI replace human recruiters entirely?" or "How can companies ensure that AI screening tools do not perpetuate bias against specific demographic groups?" There is also substantial interest in understanding how AI can optimize candidate experience and predict employee success beyond basic resume matching. Analysis reveals that users view AI primarily as a powerful augmentation tool rather than a replacement mechanism, capable of automating repetitive tasks like screening and scheduling, thereby freeing human recruiters to focus on high-touch activities such as negotiation and candidate relationship management. Concerns about algorithmic bias remain paramount, driving demand for explainable AI (XAI) models in talent acquisition. Expectations are high regarding AI's ability to unlock predictive capabilities, moving beyond historical data matching to forecast long-term fit and retention risk, establishing AI as a core strategic differentiator for leading recruitment firms and internal talent acquisition teams.

The recruitment market is profoundly influenced by a complex interplay of drivers, restraints, opportunities, and internal impact forces that dictate its direction and volatility. A primary driver is the accelerating pace of digital transformation across all industries, which mandates continuous upskilling and creates acute talent gaps in specialized fields like cybersecurity, cloud infrastructure, and data science, making external recruitment services indispensable. Concurrently, the increasing globalization of labor markets necessitates sophisticated cross-border talent sourcing capabilities, further bolstering the role of international recruitment firms. However, market growth is restrained by global economic instability and geopolitical uncertainties, which often lead to hiring freezes or significant delays in corporate expansion plans, particularly in volatile emerging markets. Additionally, stringent data privacy regulations, such as GDPR in Europe and similar frameworks globally, impose high compliance costs and complexity on firms managing vast amounts of sensitive candidate data, acting as a frictional constraint on seamless cross-border recruitment activities.

Opportunities for expansion are primarily centered around the exponential growth of the gig economy and the rise of remote work models, which necessitate new staffing solutions focused on temporary, contract, and freelance placements, often facilitated through dedicated platform technologies. Niche specialization in high-growth sectors, such as Environmental, Social, and Governance (ESG) consulting and biotechnology, presents highly lucrative avenues for boutique recruitment agencies. Impact forces within the market structure itself include intensified competition from internal corporate talent acquisition teams that are increasingly sophisticated, forcing external agencies to focus on providing highly specialized, value-added services rather than routine contingency placements. Furthermore, the rapid commoditization of entry-level sourcing tasks by AI-powered tools exerts downward pressure on the pricing models of traditional staffing firms, compelling them to invest heavily in technology to maintain competitive margins and offer strategic consulting alongside placement services. This dynamic environment requires continuous adaptation and technological investment for sustained market leadership.

The recruitment market segmentation provides a granular view of service specialization, end-user adoption patterns, and technological preferences across the global landscape. Segmentation is typically performed based on the type of service provided, the industry served, the technology utilized, and the deployment model chosen by clients. The dominant segmentation based on service type distinguishes between permanent staffing (focusing on long-term employment), temporary staffing (addressing short-term workforce needs and seasonal demands), and Recruitment Process Outsourcing (RPO), which involves comprehensive outsourcing of all or parts of the client's internal recruitment functions. Industry segmentation clearly delineates the demand intensity and skill specialization required across various sectors; for instance, the IT and Healthcare sectors consistently represent the largest and fastest-growing segments due to perpetual innovation and demographic pressures, respectively. Analyzing these segments is crucial for market participants to tailor their offerings, optimize resource allocation, and identify high-potential growth verticals, enabling targeted marketing and sales strategies that maximize penetration within specialized market niches globally.

The recruitment market value chain is characterized by several distinct stages, beginning with upstream technology and data providers and culminating in the downstream delivery of human capital to the end-user organization. Upstream activities involve technology development, where vendors create sophisticated tools such as Applicant Tracking Systems (ATS), Candidate Relationship Management (CRM) platforms, and AI-driven sourcing engines. These technology providers are essential as they determine the efficiency and scalability of the entire recruitment process. Further upstream are data aggregators and job board platforms that collect and structure candidate information, forming the fundamental pool of talent. The core value-add is generated in the midstream, where recruitment agencies (staffing, RPO, executive search) utilize these tools and data to perform specialized activities: candidate attraction, screening, assessment, and placement. The profitability and competitive advantage in the midstream depend heavily on the recruiter's ability to maintain a strong network, demonstrate expertise in niche domains, and efficiently manage the candidate experience from initial contact through onboarding.

Downstream analysis focuses on the interaction between the recruitment service provider and the end-user client, which is typically the corporate entity seeking talent. This stage involves contractual agreements, negotiation of fees, and strategic workforce consulting, where the recruiter acts as a strategic advisor on market salary benchmarks and labor trends. The distribution channel in the recruitment market is multi-faceted, encompassing both direct and indirect methods. Direct channels involve the client's internal Human Resources department or Talent Acquisition team utilizing proprietary software and direct sourcing techniques. Indirect channels are far more prevalent and involve the utilization of third-party recruitment agencies, RPO providers, and specialized staffing firms. The trend favors indirect channels for volume hiring, executive roles, and specialized skill acquisition, largely because external providers offer immediate scale and deeply specialized knowledge that is often impractical or costly for internal teams to replicate, particularly across diverse global markets. Effective value chain management requires seamless integration between the technological backbone and the human expertise, ensuring data flows efficiently from sourcing tools upstream to the client's reporting systems downstream, optimizing the overall time-to-hire metric and enhancing the quality of placement outcomes.

Potential customers, or end-users/buyers, of recruitment services are inherently diverse, ranging from multinational Fortune 500 corporations requiring large-scale Recruitment Process Outsourcing (RPO) contracts to small and medium-sized enterprises (SMEs) seeking contingency placement for a single critical role. The customer base is largely categorized by industry vertical and company size, with distinct needs defining the type of service sought. Large enterprises, especially those in fast-moving sectors like technology and finance, are perpetual buyers of strategic recruitment services, often engaging executive search firms for C-level positions and utilizing temporary staffing firms to manage fluctuating project workloads and ensure workforce scalability during economic peaks and troughs. Their primary focus is on ensuring global consistency in hiring practices, compliance with international labor laws, and achieving aggressive diversity targets, making them ideal candidates for RPO solutions that integrate technology and consulting.

SMEs, conversely, often lack the dedicated internal recruitment infrastructure or specialized expertise, making them heavy users of contingency and retained search firms for specialized roles where internal sourcing proves challenging. These smaller organizations value cost-effectiveness and speed, prioritizing providers who can deliver high-quality candidates rapidly without demanding extensive setup or long-term commitments. Beyond the commercial sector, governmental agencies and non-profit organizations also represent significant customer segments, though their hiring processes are often more regulated and slower, requiring specialized recruitment firms familiar with public sector compliance and unique budgetary constraints. The common thread across all potential customers is the critical need to secure human capital efficiently to meet organizational goals, thereby defining the recruitment service provider as an essential external resource for talent supply chain management, regardless of the client's scale or specific industry specialization.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 650.4 Billion |

| Market Forecast in 2033 | USD 980.1 Billion |

| Growth Rate | 6.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Randstad N.V., The Adecco Group, ManpowerGroup Inc., Recruit Holdings Co., Ltd., Hays plc, Robert Half International Inc., Allegis Group, Kelly Services, Inc., CDI Corporation, Kforce Inc., TrueBlue Inc., Korn Ferry, Lucas Group, Michael Page International, Hudson Global, Inc., CI&T, PeopleStrong, LinkedIn (Microsoft), Indeed (Recruit Holdings), Greenhouse Software. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the recruitment market is rapidly evolving, driven by the necessity for speed, efficiency, and objectivity in hiring decisions. The cornerstone technology remains the Applicant Tracking System (ATS), which has moved beyond simple data storage to become integrated talent lifecycle management platforms. Modern ATS solutions leverage cloud infrastructure to offer scalable storage and seamless integration with other enterprise tools, such as Human Resource Information Systems (HRIS) and payroll software. However, the most significant shift involves the proliferation of Artificial Intelligence (AI) and Machine Learning (ML) capabilities embedded throughout the recruitment process. These technologies are used to automate routine, high-volume tasks, specifically in the sourcing and initial screening phases. For instance, ML algorithms are deployed for automated resume parsing, matching candidate profiles to job descriptions based on semantic relevance and predicting candidate flight risk, thereby drastically increasing the productivity of human recruiters and reducing the initial screening cycle time.

Beyond traditional ATS, the landscape is defined by specialized tools targeting specific pain points. Candidate Relationship Management (CRM) software is crucial for managing talent pipelines, nurturing passive candidates, and maintaining long-term engagement, effectively treating candidates like high-value sales leads. Furthermore, assessment technology, including cognitive and psychometric testing platforms, is becoming increasingly sophisticated, often utilizing gamification and virtual reality simulations to evaluate soft skills and job-specific competencies in an objective manner, reducing human subjective bias. Tools focused on diversity and inclusion (D&I) are also gaining prominence, utilizing AI to redact potentially identifying information from resumes or audit job descriptions for gender-biased language, ensuring compliance and fostering an equitable hiring environment. The strategic integration of these specialized tools, rather than the reliance on a single monolithic system, defines the technological maturity of leading recruitment firms and corporate talent acquisition departments.

Blockchain technology, while still nascent, holds strong potential for transforming credential verification within the recruitment value chain. By creating immutable, decentralized records of educational qualifications, professional certifications, and employment history, blockchain can eliminate fraudulent claims and significantly reduce the time and cost associated with background checks, establishing a new standard of trust and transparency in candidate data. Furthermore, the rise of specialized sourcing tools utilizing advanced boolean logic, social listening, and passive candidate scraping capabilities ensures that recruiters can reach talent that is not actively seeking new employment. This technological evolution demands continuous investment and retraining for recruiters, as proficiency in utilizing these interconnected platforms is now essential for maintaining competitiveness and delivering superior talent acquisition outcomes in a market increasingly defined by algorithmic precision and data-driven insights.

The Recruitment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2026 and 2033, driven primarily by globalization, technology skill shortages, and the increasing adoption of flexible staffing solutions globally.

AI is transforming recruitment by automating high-volume, repetitive tasks like resume screening and scheduling, allowing human recruiters to pivot their focus to strategic, high-value activities such as complex negotiation, candidate experience management, and acting as specialized talent advisors to their clients, thereby enhancing overall efficiency and quality of placement.

The Temporary Staffing segment, followed closely by Recruitment Process Outsourcing (RPO), is expected to drive significant growth. This trend reflects the corporate desire for greater workforce agility, scalability during economic shifts, and the strategic outsourcing of complex, high-volume hiring functions, particularly in IT and healthcare sectors.

Primary restraints include global economic instability leading to unpredictable corporate hiring freezes, stringent and complex international data privacy regulations (like GDPR) affecting cross-border sourcing, and persistent skill mismatches that prolong time-to-hire for niche roles, increasing recruitment costs and complexity for organizations worldwide.

North America currently holds the largest market share, characterized by mature RPO adoption and high technology spending. However, the Asia Pacific (APAC) region is projected to register the fastest growth rate due to rapid industrialization, massive investments in infrastructure, and the expansion of global manufacturing and IT services centers across the region.

The Permanent Staffing segment remains the foundational pillar of the recruitment market, focusing on placing candidates into long-term, full-time employment roles within client organizations. This segment demands a high level of expertise from recruitment professionals, as successful placement requires not only matching technical skills but also ensuring a strong cultural and long-term fit, which directly impacts employee retention rates and long-term organizational stability. Growth in this segment is strongly correlated with positive macroeconomic indicators and robust corporate confidence, as companies are more willing to commit to the fixed costs associated with permanent employees during periods of sustained expansion. Key drivers for permanent staffing include the requirement for highly specialized, mission-critical roles that cannot be outsourced or filled temporarily, such as senior leadership, specialized R&D staff, and core engineering talent. The permanent placement process is often more rigorous, involving multiple interview stages, comprehensive background checks, and strategic negotiation advice, justifying higher contingency or retained fees compared to temporary placements.

Despite the rise of flexible labor, permanent staffing holds irreplaceable value for building corporate knowledge capital and maintaining a stable core workforce. The segment is experiencing technological enhancements, leveraging AI to improve predictive modeling for long-term job performance and cultural compatibility. Recruitment firms specializing in permanent placements are increasingly adopting hybrid models, offering strategic consulting services alongside core placement, helping clients define future workforce needs and organizational design. Challenges persist, however, mainly due to the time-intensive nature of executive search and the intense competition for scarce talent, particularly in tech and healthcare, where bidding wars for candidates are common. Therefore, the segment's future resilience relies on its ability to evolve into a strategic partnership model, offering advisory capacity rather than just transactional candidate delivery, utilizing advanced data analytics to forecast talent needs accurately.

The Temporary Staffing segment, encompassing contract and contingency workers, is witnessing accelerated growth, often outpacing permanent placement growth, particularly in economies prioritizing workforce flexibility. This segment provides organizations with the critical ability to scale their operations quickly in response to market fluctuations, manage cyclical demands (e.g., retail holidays, seasonal manufacturing peaks), and execute specific, time-bound projects without expanding their permanent headcount or incurring high severance costs during downturns. The appeal of temporary staffing lies in its cost variability and speed of deployment; firms can fill roles within days or weeks, bypassing the lengthy processes often required for permanent hires. Furthermore, the expansion of the gig economy and the increasing acceptance of remote project-based work globally have significantly broadened the pool of available contract workers, bolstering the supply side of this market segment.

From the worker’s perspective, temporary staffing offers flexibility, diverse project experience, and greater autonomy, making it attractive to specialized contractors and younger generations seeking variety. This structural shift necessitates robust operational capabilities from staffing agencies, requiring efficient payroll management, compliance handling across multiple jurisdictions, and sophisticated talent pools ready for immediate deployment. Key applications include high-volume administrative support, project-based IT deployments (e.g., system upgrades), and clinical staffing during public health crises. The technological evolution in this segment focuses heavily on platform economies and instantaneous matching tools. Staffing agencies are investing in proprietary platforms that enable self-service job matching and rapid deployment tracking, reducing administrative overhead and increasing the speed at which contingent labor can be mobilized. The long-term outlook remains highly positive, as economic uncertainty and the constant need for specialized, project-specific skills solidify temporary staffing as a crucial risk mitigation and operational tool for businesses of all sizes.

Recruitment Process Outsourcing (RPO) involves an organization transferring ownership of all or part of its recruitment process to an external provider. Unlike traditional contingency staffing, RPO is a strategic partnership where the provider manages infrastructure, technology, and staff to deliver holistic, often high-volume, talent acquisition solutions. The RPO segment has seen massive uptake among large multinational corporations seeking standardized global hiring practices, improved candidate experience metrics, and significant reductions in variable recruitment costs. The comprehensive nature of RPO allows clients to benefit from the service provider's economies of scale, dedicated technology stacks (including advanced ATS and assessment tools), and expertise in complex regulatory environments, particularly across regions like Europe and Asia Pacific.

The value proposition of RPO extends beyond mere efficiency; it provides strategic insights. RPO providers often become embedded partners, offering detailed workforce planning, salary benchmarking, and talent market intelligence, transforming recruitment from a reactive function into a proactive strategic lever. Growth in this segment is being fueled by the demand for complex RPO models, such as specialized RPO focusing only on technical or executive hiring, or hybrid RPO models that augment internal teams during specific hiring spikes. Furthermore, the increased focus on corporate diversity and inclusion (D&I) goals has driven demand for RPO providers who can demonstrably improve sourcing pipelines to meet these targets. Success in the RPO segment depends heavily on the provider's ability to seamlessly integrate their technology and processes with the client’s existing HR infrastructure, ensuring transparent communication and maintaining the integrity of the client’s employment brand throughout the candidate journey.

Applicant Tracking Systems (ATS) and Candidate Relationship Management (CRM) tools form the essential technological backbone of modern recruitment. ATS is a software application designed to help recruiters manage the workflow of finding, hiring, and tracking job candidates, often acting as the centralized repository for all application data. The shift from on-premise to cloud-based ATS solutions has lowered barriers to entry, providing SMEs with access to robust features previously only available to large enterprises. Modern ATS capabilities are increasingly focused on automation, including automated job posting, standardized compliance reporting (especially important for US federal contractors), and seamless integration with external job boards and social media platforms. The efficiency gains from ATS are measurable through metrics like reduction in time-to-hire and cost-per-hire.

CRM platforms, on the other hand, focus on the proactive engagement and nurturing of passive talent pools. Unlike ATS, which manages active applicants, CRM is designed for long-term relationship building, enabling recruiters to segment candidates, send personalized outreach, and maintain consistent communication, ensuring that when a specialized role opens up, a ready supply of pre-qualified, engaged talent is available. The convergence of ATS and CRM functionalities is a defining trend. Providers are integrating these systems to create holistic Talent Acquisition Suites that manage the entire journey from initial passive sourcing (CRM) through active application and placement (ATS). This integrated approach provides recruiters with a 360-degree view of the candidate, significantly enhancing the effectiveness of talent pipeline management and reducing reliance on costly reactive job advertisements, thereby maximizing the ROI on technology investments in talent acquisition.

The integration of Artificial Intelligence and Machine Learning represents the most disruptive force in the recruitment technology landscape. AI's primary utility lies in enhancing speed and objectivity in sourcing and preliminary assessment. AI-powered sourcing tools utilize sophisticated algorithms to scan millions of online profiles, identifying candidates whose skills and experience match job requirements with a precision far exceeding traditional keyword matching. These tools can analyze subtle semantic cues in resumes and online professional profiles, inferring skills not explicitly listed, thereby broadening the potential talent pool and significantly reducing the labor involved in manual candidate discovery.

In the assessment phase, ML models are trained on large datasets to predict candidate performance and cultural fit based on various input parameters, including responses to screening questions, behavioral data, and performance in standardized digital assessments. Chatbots and conversational AI are increasingly used as the first point of contact for candidates, handling frequently asked questions and conducting preliminary, structured interviews 24/7, dramatically improving responsiveness and candidate experience. Crucially, the focus of development is now shifting towards "fair" AI, with providers implementing explainability features (XAI) to audit and mitigate algorithmic bias that could arise from training data reflective of historical hiring patterns. This commitment to ethical AI is essential for mass adoption and maintaining compliance in global labor markets, cementing AI as a mandatory component for any recruitment organization seeking competitive technological parity.

The distinction between deployment modes, specifically Cloud-Based versus On-Premise solutions, has become a significant factor in technology adoption across the recruitment market, heavily influencing operational flexibility and total cost of ownership (TCO). Cloud-based deployment, delivered via Software-as-a-Service (SaaS) models, is the dominant and fastest-growing segment. The attractiveness of the cloud stems from its inherent scalability, enabling recruitment firms and corporate clients to rapidly adjust capacity based on fluctuating hiring volumes without capital expenditure on hardware or extensive IT support. Cloud solutions offer continuous automatic updates, ensuring users always have access to the latest security features, AI algorithms, and compliance modules, which is critical in a fast-moving regulatory and technological environment. Furthermore, accessibility from any location supports the global nature of modern recruitment and the trend toward remote talent acquisition teams, facilitating seamless collaboration across continents and time zones.

Conversely, On-Premise deployment, where software is installed and managed entirely within the client's internal servers and IT infrastructure, is rapidly declining, primarily retained by highly regulated industries such as government, defense, or financial institutions with stringent legacy data security protocols that necessitate absolute physical control over sensitive candidate information. While on-premise solutions offer maximum customization and perceived data security control, they require substantial upfront investment, dedicated internal IT teams for maintenance and updates, and lack the inherent flexibility and rapid iteration cycles characteristic of cloud environments. For the vast majority of market participants, particularly RPO providers and staffing agencies that need to manage thousands of client accounts and tens of thousands of candidates simultaneously, the economic and operational advantages of cloud deployment—lower TCO, faster deployment, and inherent scalability—make it the preferred and necessary standard for modern talent acquisition technology.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.