ID : MRU_ 434654 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

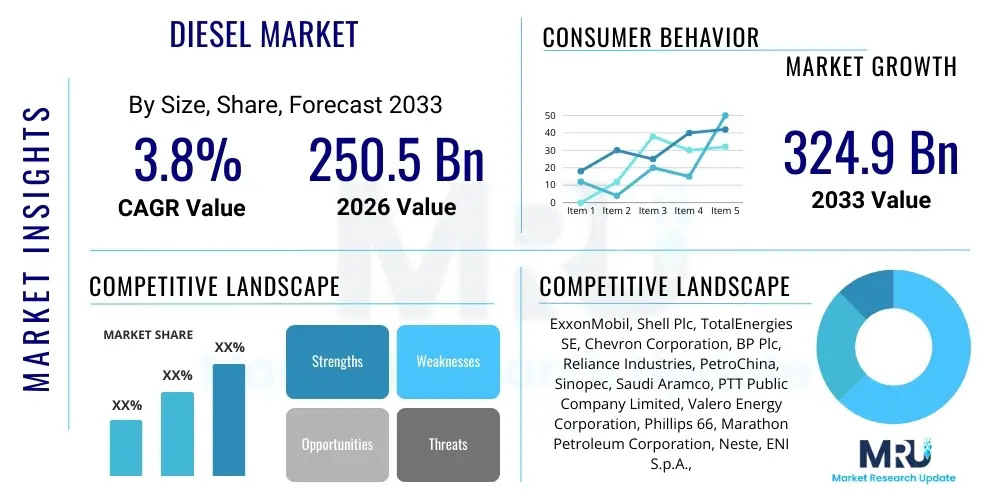

The Diesel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.8% between 2026 and 2033. The market is estimated at USD 250.5 Billion in 2026 and is projected to reach USD 324.9 Billion by the end of the forecast period in 2033.

The Diesel Market encompasses the production, distribution, and consumption of diesel fuel, a crucial refined petroleum product primarily used for powering compression-ignition engines. Diesel fuel is a vital energy source for global transportation, particularly in heavy-duty commercial vehicles, marine vessels, railway locomotives, and various industrial machinery, including construction and agricultural equipment. Its high energy density, superior fuel efficiency, and robust performance characteristics, especially under high-load conditions, cement its status as an indispensable component of the logistics and industrial sectors worldwide. The market scope includes various grades of diesel, such as high-speed diesel (HSD), ultra-low sulfur diesel (ULSD), and emerging bio-diesel blends (B5, B20), reflecting ongoing shifts towards stringent environmental standards.

A key characteristic of modern diesel is the continuous evolution mandated by regulatory bodies to reduce harmful emissions. The implementation of sulfur limits, notably shifting toward ULSD standards globally, has significantly influenced refining processes and infrastructure investments. Beyond transportation, diesel generators are critical for backup power across commercial facilities, hospitals, and data centers, particularly in regions with unreliable electrical grids. The persistent demand from these sectors, coupled with the slow pace of full electrification in long-haul heavy transport, ensures sustained market relevance, even amid intense competitive pressure from alternative energy sources.

Driving factors sustaining the market include rapid industrialization and expansion of global trade, which heavily rely on diesel-powered logistics networks. Furthermore, the agricultural sector's dependence on diesel-powered machinery for large-scale operations maintains a steady demand curve. Despite these drivers, the market faces significant headwinds from global climate mandates, the aggressive deployment of electric vehicles (EVs) in light and medium-duty segments, and increasing investment in renewable diesel and sustainable aviation fuels (SAF). Market stakeholders are therefore focused on optimizing refining efficiencies, integrating bio-components, and managing complex geopolitical supply chain dynamics to navigate this period of energy transition.

The Diesel Market is currently characterized by a dichotomy: stable demand from core industrial and heavy-duty sectors contrasting sharply with intense regulatory pressure and the accelerating energy transition towards decarbonization. Business trends reflect significant capital expenditure in upgrading refineries to produce Ultra-Low Sulfur Diesel (ULSD) and integrating hydro-processing capabilities to handle renewable feedstocks, indicating a strategic shift toward cleaner fuels. Companies are focusing on diversified energy portfolios, recognizing that while fossil diesel consumption will decline in the long term, high-quality, efficient diesel remains critical for hard-to-abate sectors like shipping and mining over the medium term. Geopolitical instability continues to influence pricing volatility and supply chain security, necessitating robust inventory management and hedging strategies across the value chain.

Regionally, Asia Pacific (APAC) stands out as the primary growth engine, fueled by burgeoning infrastructure development, massive manufacturing output, and expanding commercial vehicle fleets in countries like China and India. This high demand growth in APAC significantly offsets slower or stabilizing consumption trends observed in mature markets like North America and Europe, where stringent emission regulations and aggressive EV adoption policies are actively suppressing diesel use, particularly in non-commercial passenger vehicles. The Middle East and Africa (MEA) play a vital role primarily on the supply side, leveraging vast crude reserves and expanding export-oriented refining capacities, positioning the region as a critical global supplier of refined products.

Segment trends reveal that the highest resilience is found in the High-Speed Diesel (HSD) segment used for heavy trucking and marine bunker fuel, driven by global trade volumes. Conversely, the market is seeing rapid growth in the Bio-Diesel and Renewable Diesel segment (HVO/RD), supported by blending mandates and governmental incentives aimed at reducing carbon intensity in the transport sector. The application segmentation confirms the continued dominance of the transportation sector, though consumption for stationary power generation remains crucial, particularly in developing economies facing persistent energy reliability issues. The overall executive outlook points towards a highly competitive and regulated market requiring innovation in fuel quality and sustainable sourcing to maintain profitability.

Common user inquiries regarding AI's impact on the Diesel Market frequently center on three core themes: operational efficiency, predictive maintenance, and the optimization of supply chain logistics. Users are keen to understand how AI can mitigate the inherent volatility and high costs associated with diesel production and distribution. Key concerns revolve around whether AI-driven predictive modeling can accurately forecast shifting demand curves influenced by renewable energy adoption and global economic cycles, thereby optimizing refinery throughput and reducing inventory waste. Furthermore, significant interest exists regarding AI’s role in managing complex crude sourcing, refining process controls (especially for high-value low-sulfur products), and enhancing asset integrity management within pipelines and storage facilities to prevent costly downtime and environmental incidents. The collective user expectation is that AI will primarily serve as a critical tool for resilience and margin preservation in an increasingly constrained and regulated market environment.

The Diesel Market is subject to a complex interplay of Drivers, Restraints, and Opportunities (DRO), underpinned by powerful external impact forces that dictate its medium to long-term trajectory. A primary driver remains the fundamental need for high-density, reliable energy in the global heavy-duty transportation, maritime, and industrial sectors, where viable, cost-effective alternatives are still maturing. The expansion of global infrastructure, mining operations, and agriculture, particularly in emerging economies, necessitates continuous reliance on diesel-powered machinery, thereby stabilizing baseline demand. However, this stability is constantly challenged by the paramount restraint: the global decarbonization imperative, manifested through tightening emission standards (e.g., Euro VI, Tier 4) and aggressive governmental policies promoting electrification and hydrogen adoption across road transport. These opposing forces create a volatile market environment characterized by both critical strategic importance and existential long-term threat.

Opportunities in the market are largely centered around sustainability and efficiency. The growing mandate for reducing carbon intensity has created significant opportunities for renewable diesel (HVO) and bio-diesel blending, allowing existing infrastructure to accommodate cleaner fuel types without massive immediate overhauls. Furthermore, technological advancements in engine efficiency and the development of high-performance synthetic diesel fuels offer pathways to extend the longevity and improve the environmental profile of the internal combustion engine (ICE). Companies that invest heavily in flexible refining capabilities capable of processing diverse feedstocks—including used cooking oil (UCO) and tallow for HVO production—are best positioned to capture these emerging market opportunities and satisfy growing regulatory demands for sustainable sourcing.

The overarching impact forces shaping the market include geopolitical instability, which directly affects crude oil supply and pricing volatility, rendering stable operational planning challenging. Regulatory pressures, especially those emanating from the IMO (for marine fuel) and regional environmental protection agencies, act as non-negotiable constraints demanding continuous adaptation in fuel quality and processing. The competitive impact from disruptive technologies, such as battery electric vehicles (BEVs) and hydrogen fuel cell technology for medium-duty transport, constitutes a long-term existential force. The Diesel Market must navigate these political, environmental, and technological crosscurrents, requiring significant strategic foresight focused on high-quality, compliant, and sustainably sourced products to maintain market share.

The Diesel Market segmentation provides a granular view of demand distribution and consumption patterns across various fuel types, applications, and end-users, reflecting the diverse requirements of the global economy. Analyzing the market by Type allows stakeholders to distinguish between traditional fossil-derived diesel grades and increasingly mandated renewable alternatives. This distinction is critical for understanding future refining needs and capital deployment strategies, particularly as regulations favor Ultra-Low Sulfur Diesel (ULSD) and incentivized bio-blends (B5, B20, HVO). The Type segment is undergoing the most rapid transformation due to environmental policy.

Segmentation by Application highlights the crucial reliance of specific industrial and logistics sectors on diesel power, contrasting the diminishing use in light-duty passenger vehicles. While consumer passenger vehicle use is rapidly shifting toward electrification globally, the demand from sectors like freight logistics, construction, and agriculture remains robust and inelastic in the short to medium term. Understanding these application segments helps in targeted marketing and distribution strategies, emphasizing performance, reliability, and fuel quality specific to high-load operational environments, such as marine bunkering or heavy earthmoving. The resilience of the heavy-duty transportation segment is the market’s primary stabilizing force.

Geographic segmentation is paramount, demonstrating the stark contrast in market maturity and growth potential. Developed regions like North America and Europe are characterized by sophisticated regulation and gradual decline in volume due to energy transition policies, focusing on premium, clean diesel. Conversely, the rapidly industrializing economies of Asia Pacific and parts of the Middle East and Africa exhibit high volume growth, driven by infrastructure development and expanding commercial activity. This geographic diversity mandates regionalized supply chain planning and product specification adjustments to comply with varied local emission standards and consumer demand profiles.

The value chain for the Diesel Market is extensive and highly capital-intensive, starting with upstream activities involving the exploration and extraction of crude oil, which serves as the fundamental raw material. Upstream analysis focuses on securing stable, cost-effective access to diverse crude feedstocks, a process heavily influenced by geopolitical risk and commodity market volatility. Stability in crude supply is paramount as it dictates refinery input costs and production schedules. Critical decisions at this stage involve optimizing the sourcing mix—balancing heavy versus light crude—to maximize the yield of middle distillates suitable for diesel production, while increasingly evaluating non-fossil feedstocks like vegetable oils and animal fats for renewable diesel production pathways.

The midstream phase encompasses the complex and highly technical refining process, where crude oil is distilled, hydrotreated, and blended to produce finished diesel products conforming to specific regulatory standards, such as ULSD. This phase requires substantial investment in hydro-desulfurization units and advanced processing technologies to meet stringent environmental specifications. The downstream analysis focuses on the efficient storage, transportation (via pipelines, rail, truck, and tankers), and distribution of the refined diesel fuel to end-users. Distribution channels are highly fragmented, involving a blend of direct sales to large industrial consumers (e.g., shipping lines, mining operations) and indirect sales through wholesale distributors and vast networks of retail fueling stations.

Direct distribution channels are generally utilized for high-volume, bulk consumers, offering streamlined logistics and negotiated pricing, ensuring fuel supply directly to depots or remote operational sites. Indirect distribution involves various intermediaries, including jobbers, branded distributors, and franchised retail outlets, which are crucial for reaching smaller commercial fleets and individual consumers. Optimizing this distribution network is essential for market penetration and margin realization. Given the rising demand for cleaner fuels, the integration of bio-diesel blending facilities at distribution terminals represents a key area of current investment, linking the upstream sourcing of sustainable feedstocks with the final consumption point efficiently and compliantly, minimizing logistical friction in a time-sensitive market.

The primary consumers of diesel fuel are diverse, spanning critical sectors that form the backbone of the global economy, making demand highly inelastic in many segments. The core group of end-users consists of bulk buyers in the logistics and transport sector, specifically fleet operators managing heavy-duty Class 8 trucks, which are essential for long-haul freight and national distribution networks. These customers prioritize high-quality fuel that ensures engine longevity, maximizes fuel economy, and meets rigorous operational standards under challenging conditions. Their purchase decisions are heavily influenced by the reliability of supply and competitive bulk pricing agreements, often seeking long-term supply contracts with major oil companies or large distributors.

Another major category comprises industrial and commercial entities requiring stationary or mobile power. This includes construction companies utilizing bulldozers, excavators, and cranes; agricultural enterprises relying on tractors and harvesters; and mining operations dependent on massive haul trucks and specialized equipment. For these segments, performance and resilience are critical, as downtime due to fuel quality issues can result in catastrophic operational losses. Additionally, data centers, hospitals, and critical infrastructure facilities globally depend on diesel generators for reliable backup power, particularly where grid stability is a concern, positioning them as non-negotiable consumers of fuel for emergency readiness.

Furthermore, the marine and rail sectors represent substantial, consolidated customer bases. Global shipping lines are major consumers of marine diesel oil (MDO) and low-sulfur bunker fuels, driven by international maritime regulations (IMO 2020) that mandate cleaner operations. Similarly, national and private railway operators utilize diesel-electric locomotives for freight and passenger transport across vast distances. These end-users demand fuels that adhere to highly specific sulfur and quality parameters, often purchasing directly from specialized bunkering or railside distribution services. The future potential customers are increasingly leaning toward suppliers who can guarantee compliance and offer certified renewable diesel options to meet their own corporate sustainability targets.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 250.5 Billion |

| Market Forecast in 2033 | USD 324.9 Billion |

| Growth Rate | CAGR 3.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ExxonMobil, Shell Plc, TotalEnergies SE, Chevron Corporation, BP Plc, Reliance Industries, PetroChina, Sinopec, Saudi Aramco, PTT Public Company Limited, Valero Energy Corporation, Phillips 66, Marathon Petroleum Corporation, Neste, ENI S.p.A., Repsol S.A., Indian Oil Corporation Ltd., ConocoPhillips, LUKOIL, Equinor ASA |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Diesel Market is primarily defined by advanced refining processes necessary to meet escalating quality standards and the integration of sustainable feedstock conversion capabilities. The adoption of hydro-processing technology, particularly hydrocracking and hydrotreating, is paramount. Hydrotreating facilities are essential for lowering the sulfur content in diesel to meet Ultra-Low Sulfur Diesel (ULSD) specifications (typically 10-15 ppm sulfur), a regulatory requirement across major consuming regions. Investment in highly efficient hydro-desulfurization units allows refiners to process a wider variety of crudes while ensuring compliance, directly influencing competitive positioning and market access. Furthermore, process intensification techniques, leveraging catalysts and advanced separation technologies, are being used to maximize the yield of high-value middle distillates over lower-value products, improving overall refinery economics.

A second critical area of technological innovation is the rapid development and scaling of technologies for producing Renewable Diesel (HVO - Hydrotreated Vegetable Oil). Unlike traditional bio-diesel (FAME), HVO is chemically identical to fossil diesel, allowing for seamless integration into existing infrastructure and high-percentage blending without performance compromises. Technologies like Neste’s NEXBTL process enable the conversion of diverse waste and residual oils (used cooking oil, animal fats) into high-quality, low-carbon HVO. This requires refiners to pivot from purely petroleum-based inputs to integrating complex bio-feedstock pre-treatment and hydrogenation units, marking a fundamental technological shift that diversifies the market's raw material base and supports decarbonization goals. The successful deployment of HVO technologies is a key differentiator in the modern diesel market.

Finally, technology related to fuel additives and engine efficiency plays a continuous role. Modern diesel engines, particularly those in heavy-duty vehicles, are complex systems requiring advanced fuel formulations to protect intricate emission control systems (such as Diesel Particulate Filters, DPFs, and Selective Catalytic Reduction, SCR). Research into detergent additives, cold flow improvers, and lubricity enhancers ensures that diesel meets both performance and environmental requirements, especially critical in harsh operating environments. Simultaneously, digitalization, leveraging IoT sensors and advanced control systems (often augmented by AI), is being implemented across the distribution and storage infrastructure to monitor fuel quality, minimize evaporation losses, and ensure tamper-proof logistics, enhancing supply chain integrity and efficiency.

The primary driver is the sustained, high-volume demand from the global heavy-duty transportation sector (trucking and marine) and crucial industrial sectors like construction, mining, and agriculture, particularly in high-growth economies across the Asia Pacific region. These sectors currently lack scalable, high-energy-density alternatives to diesel fuel.

Environmental regulations, such as the mandated transition to Ultra-Low Sulfur Diesel (ULSD) and IMO 2020 for marine fuel, necessitate significant capital investment in advanced hydro-processing technologies at refineries. These rules increase operational complexity and cost but ensure the fuel meets stringent global emission standards, thereby reducing sulfur dioxide and particulate matter pollution.

Bio-Diesel (FAME) is produced via transesterification and has blending limits due to storage and performance issues. Renewable Diesel (HVO/RD), produced via hydrotreatment, is chemically identical to fossil diesel and can be used as a 100% drop-in fuel. HVO is increasingly influential because it offers superior performance and significantly higher greenhouse gas reduction potential without requiring extensive infrastructure modification.

Currently, the Asia Pacific region dominates in terms of consumption growth due to rapid industrialization and expanding commercial activity. Historically, North America and Europe were primary consumers. The shift is occurring because mature markets are actively reducing fossil diesel use through electrification policies, while emerging economies continue to scale industrial and logistical reliance on diesel.

The key long-term risks are the rapid adoption of alternative power solutions, specifically large-scale battery electric and hydrogen fuel cell technology penetration into the medium-duty and short-haul heavy-duty segments. Additionally, sustained high crude oil price volatility and increasing carbon pricing mechanisms pose significant threats to the cost-competitiveness of fossil-derived diesel.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.