ID : MRU_ 431640 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

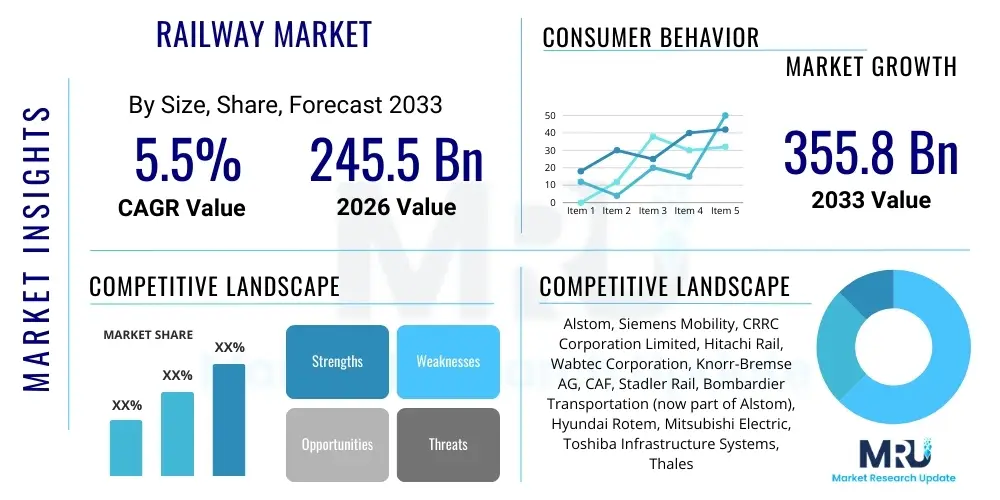

The Railway Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.46% between 2026 and 2033. The market is estimated at USD 245.5 Billion in 2026 and is projected to reach USD 355.8 Billion by the end of the forecast period in 2033. This substantial growth trajectory is underpinned by global governmental investments in sustainable public transport infrastructure, rapid urbanization leading to increased demand for efficient commuter rail systems, and the strategic expansion of freight rail networks to mitigate supply chain complexities associated with road transport. The shift towards electrification and the adoption of advanced signaling systems further contribute significantly to this market valuation.

The Railway Market encompasses the entire ecosystem involved in the design, construction, operation, maintenance, and modernization of rail networks globally, covering rolling stock, infrastructure (track, signaling, power supply), and specialized services. Products range from high-speed trains and light rail vehicles to advanced traffic management systems (TMS) and comprehensive predictive maintenance solutions. Major applications include passenger transport (commuter, regional, intercity, high-speed rail) and freight transport (bulk cargo, intermodal shipping). The fundamental benefits of rail transport—including high capacity, superior energy efficiency, reduced carbon emissions compared to road transport, and improved safety—establish its enduring relevance in the global logistics and mobility landscape. Governments increasingly view modern railway systems as critical national assets necessary for economic connectivity and achieving net-zero emission targets.

Driving factors for the market expansion are manifold and deeply embedded in macroeconomic trends and technological advancements. These include massive global investments in high-speed rail development, particularly across Asia and Europe, the necessity of replacing aging infrastructure in mature markets like North America and parts of Europe, and the pervasive integration of digital technologies such as the Internet of Things (IoT) and Artificial Intelligence (AI) to enhance operational efficiency and safety. Furthermore, the persistent challenge of urban congestion necessitates robust, high-capacity commuter rail solutions, fueling demand for modern metro and light rail transit (LRT) systems.

The transition toward sustainable mobility is perhaps the strongest current driver, pushing operators to adopt electric traction, explore hydrogen fuel cell technologies for non-electrified lines, and implement sophisticated resource management systems. This green transition mandates significant investment in modernizing power infrastructure, optimizing energy consumption through smart signaling, and ensuring that all components meet increasingly stringent environmental regulations. The combined effect of infrastructure development and technological enhancement secures the market's long-term growth prospects, making rail a pivotal element of future multimodal transport networks.

The global Railway Market is characterized by robust resilience and strategic growth, driven predominantly by large-scale public investment programs aimed at infrastructure modernization and decarbonization. Key business trends indicate a strong focus on Public-Private Partnerships (PPPs) to finance capital-intensive projects, a surge in mergers and acquisitions among signaling and rolling stock manufacturers to consolidate technological capabilities, and a pronounced shift towards 'Rail-as-a-Service' models where maintenance and digital services are bundled. Regional trends highlight the Asia Pacific region, led by China and India, as the primary growth engine due to aggressive high-speed and metro rail expansion plans. Europe is defined by mandatory digitalization through initiatives like the European Rail Traffic Management System (ERTMS) deployment and a strong push for cross-border interoperability. North America, while slower in passenger rail development, shows significant investment in freight digitalization, primarily driven by Class I railroads seeking operational efficiencies.

Segment trends confirm that the Infrastructure segment, particularly signaling and control systems, is experiencing the fastest growth, largely due to the mandatory replacement of legacy analog systems with digital solutions like Communication-Based Train Control (CBTC) and Positive Train Control (PTC). Within Rolling Stock, electric multiple units (EMUs) and high-speed trainsets dominate new procurement cycles, reflecting the global focus on electrification. The Services segment, encompassing maintenance, repair, and overhaul (MRO), is expanding rapidly, fueled by the adoption of predictive maintenance software utilizing big data analytics and AI to minimize downtime and extend asset life. Furthermore, specialized components related to cybersecurity for operational technology (OT) are seeing escalating demand as rail networks become more interconnected and susceptible to digital threats.

Overall, the market trajectory is irreversibly intertwined with sustainability and technological integration. The integration of advanced diagnostics and remote monitoring systems is becoming standard practice, enhancing safety and reliability across diverse operating environments. Strategic market participants are repositioning themselves from traditional hardware suppliers to integrated solution providers, offering end-to-end digital lifecycle management for rail assets. This strategic pivot ensures sustained competitive advantage in a market increasingly valuing optimized uptime and data-driven decision-making, setting the foundation for autonomous train operations in the long term.

User inquiries concerning AI's influence on the Railway Market frequently revolve around how artificial intelligence enhances safety, optimizes operations, and facilitates cost reduction. Common questions explore the feasibility of fully Autonomous Train Operations (ATO), the reliability of predictive maintenance systems (PM) based on machine learning algorithms, and the ethical and workforce implications of automation. Users are highly interested in understanding how AI algorithms handle real-time traffic management, dynamic scheduling, and complex failure diagnostics. The consensus expectation is that AI will transition railways from reactive maintenance models to proactive, highly efficient systems, although concerns persist regarding system resilience against cyberattacks and the high initial investment required for sensor installation and data infrastructure.

AI's primary transformative impact lies in its ability to process vast, disparate datasets—generated by IoT sensors, trackside monitoring systems, and rolling stock diagnostics—into actionable insights. This capability is fundamentally changing maintenance schedules, moving away from time-based routines towards condition-based interventions, resulting in optimized component lifespan and reduced inventory costs. In traffic management, AI-driven solutions dynamically adjust speeds, routing, and headway in real time, absorbing minor delays proactively and significantly improving network throughput and passenger satisfaction. Furthermore, sophisticated computer vision systems, powered by deep learning, are increasingly used for automated track inspection and monitoring, detecting subtle flaws or encroachments faster and more reliably than traditional human-led inspections.

The long-term influence of AI extends into strategic planning and resource allocation. Machine learning models are utilized to forecast passenger demand and freight volume with greater accuracy, allowing operators to optimize train length, staffing levels, and energy consumption profiles. This data-centric approach minimizes wasted resources and enhances the overall profitability of rail operations. Despite initial skepticism, the demonstrable returns on investment (ROI) derived from reduced derailments, minimal unscheduled downtime, and optimized energy usage are driving accelerated adoption across major national and private railway operators globally, positioning AI as the foundational layer for next-generation rail infrastructure.

The Railway Market is powerfully shaped by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO), which collectively define the Impact Forces governing strategic decisions and investment cycles. Key drivers include aggressive governmental policy support for public transport infrastructure modernization, the imperative for sustainable, low-carbon transport solutions, and the critical need to alleviate persistent urban congestion through efficient commuter systems. These drivers are amplified by technological advancements in digitalization (IoT, 5G connectivity) which enhance safety and operational efficiency, making rail increasingly competitive against road and air transport modalities. Conversely, significant restraints include the extremely high capital expenditure required for greenfield projects and system modernization, long project development timelines characterized by complex regulatory and bureaucratic processes, and the persistent shortage of highly specialized technical talent skilled in modern railway engineering and digital systems integration.

Opportunities in the market primarily reside in the rapid expansion of high-speed rail corridors, particularly in emerging economies, and the strategic rollout of freight digitalization solutions, such as implementing sophisticated asset tracking and capacity planning tools. Furthermore, the development and deployment of alternative traction technologies—specifically hydrogen fuel cells and advanced battery electric storage systems for non-electrified routes—represent substantial market niches. The primary impact force driving current spending is the mandatory requirement for safety and interoperability upgrades, led by global standards organizations and regional regulatory bodies (e.g., ERTMS in Europe, PTC in North America). This regulatory force necessitates substantial, non-discretionary spending on signaling and control systems, overriding some investment hesitations related to immediate economic downturns.

Another major impact force is the evolving geopolitical landscape, which affects global supply chains and commodity prices (like steel and energy). This volatility pushes railway operators to seek resilient, localized supply chains for components and prioritize long-term energy independence through electrification. The long asset lifespan of rail infrastructure means investment decisions must account for decades of potential operational and climate changes, compelling stakeholders toward modular, future-proof digital architectures. The balance between required initial investment (a restraint) and the long-term operational cost savings and sustainability benefits (a driver and opportunity) defines the market's current velocity and strategic direction.

The Railway Market segmentation provides a detailed framework for understanding market structure and identifying core investment areas, typically divided based on Component, Application, and Type of Technology. The Component segment breaks down the expenditure across Rolling Stock (trains, locomotives, passenger cars), Infrastructure (tracks, bridges, tunnels, power supply), and Services (MRO, consulting, software solutions). Application segmentation differentiates between Passenger Rail (urban transit, intercity, high-speed) and Freight Rail, each having unique demands for speed, capacity, and durability. Technology segmentation focuses on key enabling systems such as Signaling & Control Systems (CBTC, PTC, ERTMS), Power Supply & Electrification, and Rail Communication Systems, highlighting the areas of fastest digital transition.

The complexity within these segments is increasing due to integration. For instance, modern Rolling Stock must be equipped with digital subsystems for telemetry, diagnostics, and communication, blurring the lines between the hardware and services segments. Similarly, Infrastructure modernization efforts are heavily focused on installing smart trackside equipment that feeds data into advanced Signaling & Control systems, driving demand for specialized IoT devices and robust cybersecurity measures. Regional disparities also influence segmentation priorities: mature markets focus heavily on maintenance and system upgrades (Services and Signaling), while developing markets prioritize procurement of new Rolling Stock and construction of new physical Infrastructure.

Strategic analysis shows that the Signaling & Control segment is poised for the most rapid technological advancement, fueled by the global push for higher Grade of Automation (GoA) and the urgent need to enhance network safety standards. Freight rail is exhibiting a distinct segmentation demand centered around heavy-haul locomotives, specialized wagons for intermodal transport, and real-time asset visibility software. This multifaceted segmentation approach allows manufacturers, service providers, and governmental agencies to strategically allocate resources toward segments offering the highest return on investment and alignment with national transportation goals.

The Railway Market value chain is extensive and highly specialized, beginning with upstream activities focused on the procurement of raw materials and complex components. Upstream analysis involves suppliers of high-grade steel for tracks and rolling stock bodies, sophisticated electronic components (microprocessors, sensors) for signaling systems, and specialized materials for traction motors and power supply units. Manufacturers in this stage must adhere to stringent railway safety and quality standards (e.g., CENELEC standards), necessitating complex certification processes. The competitive landscape upstream is often dominated by a few global specialized suppliers with high barriers to entry due to required technical expertise and long qualification periods.

Midstream activities involve the design, manufacturing, assembly, and testing of Rolling Stock, Infrastructure components, and Signaling systems. This phase is characterized by large multinational integrators (e.g., Alstom, Siemens, CRRC) who manage complex project cycles, often involving significant customization based on regional specifications (gauge, climate, regulatory environment). The integration of digital components, such as onboard diagnostic systems and advanced networking hardware, adds layers of complexity and cost. Furthermore, extensive research and development (R&D) focused on lightweight materials, energy efficiency, and cybersecurity are critical determinants of competitiveness in this stage.

Downstream activities center around installation, commissioning, operation, and lifecycle maintenance. Distribution channels are predominantly direct, involving government railway agencies, national operators, or private freight carriers purchasing directly from manufacturers via public tenders or long-term contracts. The Services segment (MRO, software support) forms a crucial downstream element, generating stable recurring revenue streams. Indirect channels are limited but exist for standardized spare parts or specialized software through authorized distributors and system integrators. The entire value chain is characterized by high capital intensity, long sales cycles, and a strong dependence on governmental procurement policies and infrastructure spending cycles.

The potential customers and end-users of the Railway Market are highly institutional and fall primarily into two major categories: public sector entities and private commercial operators. Public entities, which form the core market demand, include national railway authorities (such as Deutsche Bahn, SNCF, Indian Railways), metropolitan transit agencies managing subway and commuter rail networks, and government departments responsible for infrastructure development and maintenance. These public sector buyers are driven by mandates related to public service, safety standards, environmental compliance, and network capacity expansion, often procuring through regulated competitive bidding processes governed by national procurement laws.

Private commercial operators represent the second crucial customer segment, particularly prominent in freight transport. This includes Class I freight railroads in North America, specialized logistics companies that own and operate private wagons, and, increasingly, private passenger operators utilizing open-access rail lines in liberalized markets (e.g., certain European countries). These private buyers prioritize Total Cost of Ownership (TCO), operational efficiency, durability, and integration capabilities (e.g., seamless integration of rail assets with their broader logistics IT systems). Their procurement is generally more focused on highly specialized rolling stock (heavy haul locomotives, intermodal wagons) and advanced digital services (predictive maintenance, rail management software).

A third, emerging customer group includes developers and operators of new urban mobility systems, such as airports and smart city developers planning automated people movers (APMs) or innovative tramway extensions. These customers seek compact, highly automated, and aesthetically integrated solutions. Essentially, any entity responsible for moving large volumes of goods or people efficiently and sustainably over medium to long distances represents a key customer, with long-term relationships and after-sales service capabilities being paramount factors in securing contracts.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 245.5 Billion |

| Market Forecast in 2033 | USD 355.8 Billion |

| Growth Rate | 5.46% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Alstom, Siemens Mobility, CRRC Corporation Limited, Hitachi Rail, Wabtec Corporation, Knorr-Bremse AG, CAF, Stadler Rail, Bombardier Transportation (now part of Alstom), Hyundai Rotem, Mitsubishi Electric, Toshiba Infrastructure Systems, Thales Group, Huawei, General Electric (GE) Transportation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Railway Market's technological landscape is undergoing a profound transformation, moving rapidly toward full digitalization and automation, centered around safety, connectivity, and efficiency. Central to this evolution is the widespread deployment of advanced Signaling and Train Control systems. In Europe and globally, the European Rail Traffic Management System (ERTMS) Level 2 and Level 3 adoption is mandatory for cross-border interoperability and higher capacity, replacing legacy national systems. Simultaneously, in urban transit, Communication-Based Train Control (CBTC) systems utilize continuous, high-speed radio communication to achieve minimal headways and higher throughput, enabling Grade of Automation (GoA) levels 2 and 3. In North America, Positive Train Control (PTC) is the dominant federally mandated safety technology, focusing on collision avoidance and speed enforcement.

Connectivity is another core technological pillar, driven by the rollout of dedicated railway communication networks utilizing 4G/LTE-R (Long-Term Evolution for Railways) and the preparatory work for 5G-R. These networks provide the necessary high bandwidth and low latency for mission-critical applications like ATO, real-time video surveillance, and complex operational data transmission, supporting the transition from traditional GSM-R technology. Furthermore, the proliferation of the Industrial Internet of Things (IIoT) sensors—embedded in tracks, power lines, and rolling stock components—enables massive data collection. This data fuels sophisticated cloud-based analytics platforms, providing the foundation for predictive maintenance and operational intelligence, effectively transforming physical assets into digital ones.

Sustainability technologies are also fundamentally reshaping the landscape, specifically the shift towards alternative traction power. While large-scale electrification remains the primary route for decarbonization, significant R&D is invested in hydrogen fuel cell trains and high-capacity battery-electric trains for non-electrified branch lines, particularly in Germany, the UK, and Japan. These technologies reduce reliance on diesel locomotives and necessitate specialized infrastructure like hydrogen refueling stations or high-power charging depots. Lastly, cybersecurity resilience, particularly for protecting operational technology (OT) systems such as interlocking and SCADA, is rapidly becoming a fundamental technological requirement, demanding integration of advanced threat detection and secure communication protocols across the entire network architecture.

Regional dynamics play a crucial role in shaping the demand, technology adoption, and competitive intensity within the global Railway Market, reflecting distinct investment priorities and maturity levels.

The primary driver is governmental and regulatory commitment to decarbonization and sustainable transport infrastructure. Global mandates to achieve net-zero emissions are forcing significant investment in electrification, high-speed rail development, and modernizing existing networks to improve energy efficiency and reduce environmental impact.

Digitalization, powered by AI, IoT sensors, and high-speed communication (LTE-R/5G-R), enhances safety through predictive maintenance, allowing operators to fix components before failure. Operationally, systems like ERTMS and CBTC enable higher traffic capacity, better punctuality, and reduced human error through increasing levels of automation.

The Signaling and Control Systems segment, falling under Infrastructure and Services, is projected for the fastest growth. This acceleration is due to the mandatory replacement of outdated legacy signaling with digital, interconnected systems (e.g., ERTMS Level 2/3, CBTC) necessary for interoperability and enabling future autonomous operation capabilities.

Hydrogen fuel cells are a critical component for decarbonizing non-electrified railway lines. They provide a zero-emission alternative to diesel locomotives where the cost or complexity of overhead wire electrification is prohibitive, offering the rail industry a viable path to fully sustainable traction power.

APAC focuses on deploying new HSR and metro infrastructure and new rolling stock procurement. Europe prioritizes digital migration (ERTMS, predictive analytics) for interoperability and modernization. North America concentrates heavily on freight rail efficiency, safety compliance (PTC), and optimizing heavy-haul logistics through IoT.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.